Fundamental Accounting Principles, 21st Edition

1478

Exercise 25-11 (20 minutes)

ALTERNATIVE A: INCREASE OR (DECREASE) IN NET INCOME

Cost to buy new machine ……………………………………………………....

$(115,000)

Cash received to trade in old machine …………………………………..………….

52,000

Reduction in variable manufacturing costs* …………………………..

85,000

Total change in net income …………………………………………………..…..

$ 22,000

*(36,000 – $19,000) X 5 years

ALTERNATIVE B: INCREASE OR (DECREASE) IN NET INCOME

Cost to buy new machine ……………………………………………………....

$(125,000)

Cash received to trade in old machine …………………………………..………….

52,000

Reduction in variable manufacturing costs** …………………………..

105,000

Total change in net income …………………………………………………..…..

$ 32,000

**(36,000 – $15,000) X 5 years

Exercise 25-12 (15 minutes)

(2)

INCREMENTAL INCOME FROM REWORK

Sale of reworked units (22,000 units @ $8.50) …………………………………..

$ 187,000

Less cost to rework units (22,000 @ $4.50) …………………………………..…..

(99,000)

Less opportunity cost of not making new units (22,000 @ $2.50)* ……..

(55,000)

Incremental income ……………………………………………………………………..…..

$ 33,000

*Sales price per unit – cost per unit = $8.50 – $6 = $2.50.

Exercise 25-13 (25 minutes)

Normal

Additional

Combined

Volume

Volume*

Total

Sales …………………………………………..

$2,250,000

$180,000

$2,430,000

Costs and expenses

Direct materials …………………………

300,000

30,0001

330,000

Direct labor ……………………………….

600,000

60,0002

660,000

Overhead ………………………………….

150,000

22,500

172,500

Selling expenses ……………………….

225,000

225,000

Administrative expenses …………..

385,500

64,500

450,000

Total costs and expenses ………….

$1,660,500

$177,000

$1,837,500

Net income ………………………………….

$ 589,500

$ 3,000

$ 592,500

1 (15,000 x $2) 2 (15,000 x $4)

* ADDITIONAL VOLUME COMPUTATIONS

Additional sales revenue = 15,000 units @ $12 = $180,000

Fundamental Accounting Principles, 21st Edition

1480

Exercise 25-14 (20 minutes)

INCREMENTAL COST OF MAKING THE PART

Variable costs (65,000 units @ $1.95) ………………………………………………..

$126,750

Incremental fixed costs …………………………………………………………..………..

65,000

Total incremental cost of making 65,000 units …………………………..

$191,750

INCREMENTAL COST OF BUYING THE PART

Cost per unit to buy ………………………………………………………………..………..

$ 3.50

Total incremental cost of buying 65,000 units …………………………..

$227,500

RECOMMENDATION: Note that the allocated fixed costs of $58,500 are not

relevant to this managerial decision because they will continue whether the

Exercise 25-15 (25 minutes)

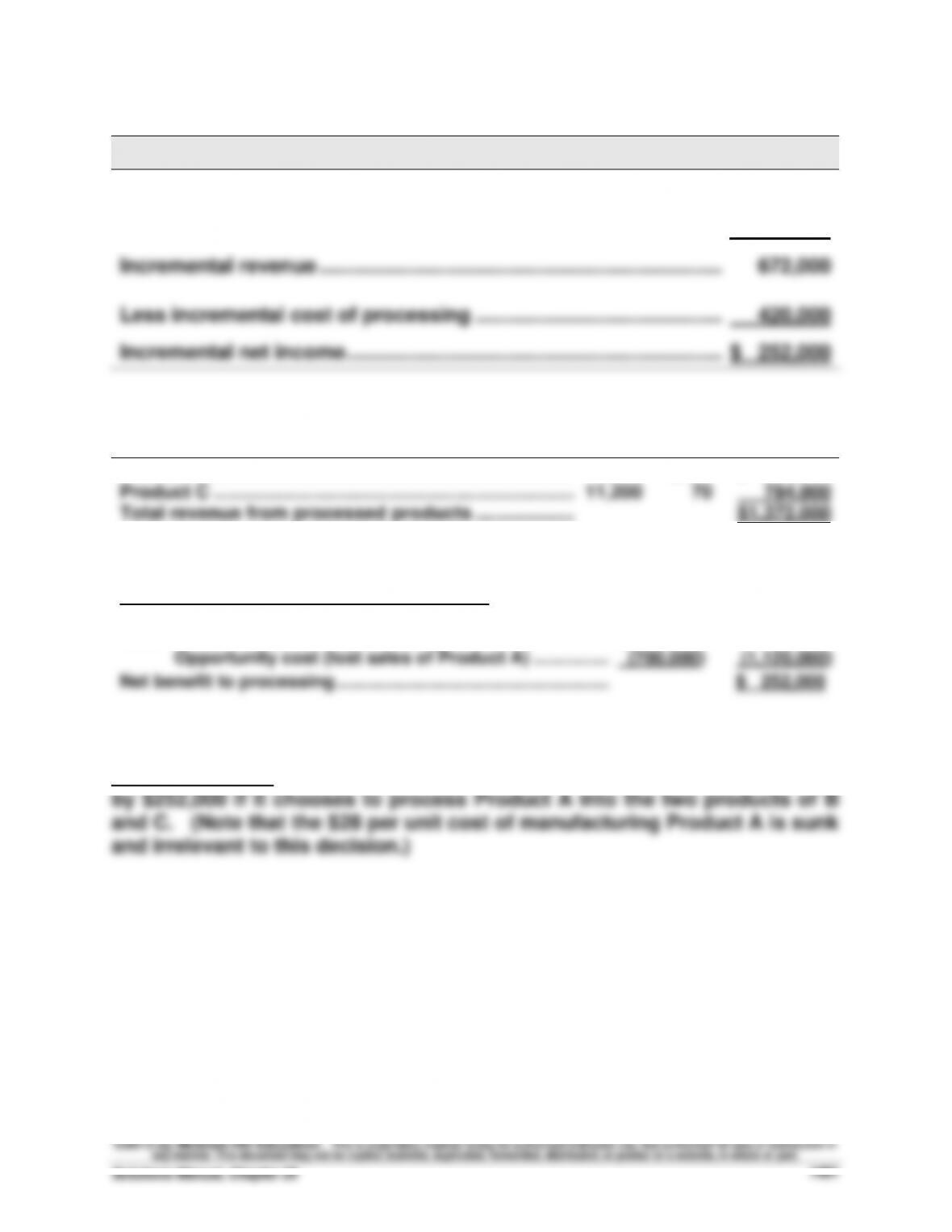

INCREMENTAL REVENUE AND COST OF ADDITIONAL PROCESSING

Revenue if processed further* ………………………………………………..…

$1,372,000

Revenue if sold as is ……………………………………………………………..…

700,000

Incremental revenue …………………………………………………………………

672,000

Less incremental cost of processing ……………………………………..…

420,000

Incremental net income ………………………………………………………….…

$ 252,000

*Revenue from processed products

Units

Price

Total

Product B ……………………………………………………………………

5,600

$105

$ 588,000

Product C ……………………………………………………………………

11,200

70

784,000

Total revenue from processed products ……………….………

$1,372,000

ALTERNATE SOLUTION FORMAT

Net income (loss) from processed products

Revenue if processed further…………………………………………

$1,372,000

Less: Additional costs of processing…………………………...

$(420,000)

Opportunity cost (lost sales of Product A) ……………

(700,000)

(1,120,000)

Net benefit to processing ………………………………………………

$ 252,000

RECOMMENDATION: This analysis shows that the company will be better off

Fundamental Accounting Principles, 21st Edition

1482

Exercise 25-16 (30 minutes)

Instructor note: In all three cases, the total unavoidable expenses of $107,800 remain the

same because they cannot be avoided by eliminating departments.

1. NO DEPARTMENTS ELIMINATED

Total

M

N

O

P

T

Sales…………………..………

$224,000

$63,000

$35,000

$56,000

$42,000

$28,000

Expenses

Avoidable ………….……….

120,400

9,800

36,400

22,400

14,000

37,800

Unavoidable ……………….

107,800

51,800

12,600

4,200

29,400

9,800

Total expenses ….……….

228,200

61,600

49,000

26,600

43,400

47,600

Net income (loss) …………

$ (4,200)

$ 1,400

$(14,000)

$29,400

$ (1,400)

$(19,600)

2. DEPARTMENTS WITH EXPECTED NET LOSSES ELIMINATED

Total

M

N

O

P

T

Sales…………………………..

$119,000

$63,000

$ 0

$56,000

$ 0

$ 0

Expenses

Avoidable …………..………………

32,200

9,800

0

22,400

0

0

Unavoidable ……….………………….

107,800

51,800

12,600

4,200

29,400

9,800

Total expenses …..………………………

140,000

61,600

12,600

26,600

29,400

9,800

Net income (loss) …………………………..

$ (21,000)

$ 1,400

$(12,600)

$29,400

$(29,400)

$(9,800)

Explanation: This income statement reflects elimination of Departments N,

P, and T. The sales and avoidable expenses are the combined amounts for

3. DEPARTMENTS WITH LESS SALES THAN AVOIDABLE EXPENSES ELIMINATED

Total

M

N

O

P

T

Sales…………………………..

$161,000

$63,000

$ 0

$56,000

$42,000

$ 0

Expenses

Avoidable …………..………………

46,200

9,800

0

22,400

14,000

0

Unavoidable ……….………………….

107,800

51,800

12,600

4,200

29,400

9,800

Total expenses …..………………………

154,000

61,600

12,600

26,600

43,400

9,800

Net income (loss) …………………………..

$ 7,000

$ 1,400

$(12,600)

$29,400

$ (1,400)

$(9,800)

Explanation: This income statement reflects the Departments M, O, and P.

Departments N and T are eliminated because their sales dollars do not

cover their avoidable costs.

Exercise 25-17 (30 minutes)

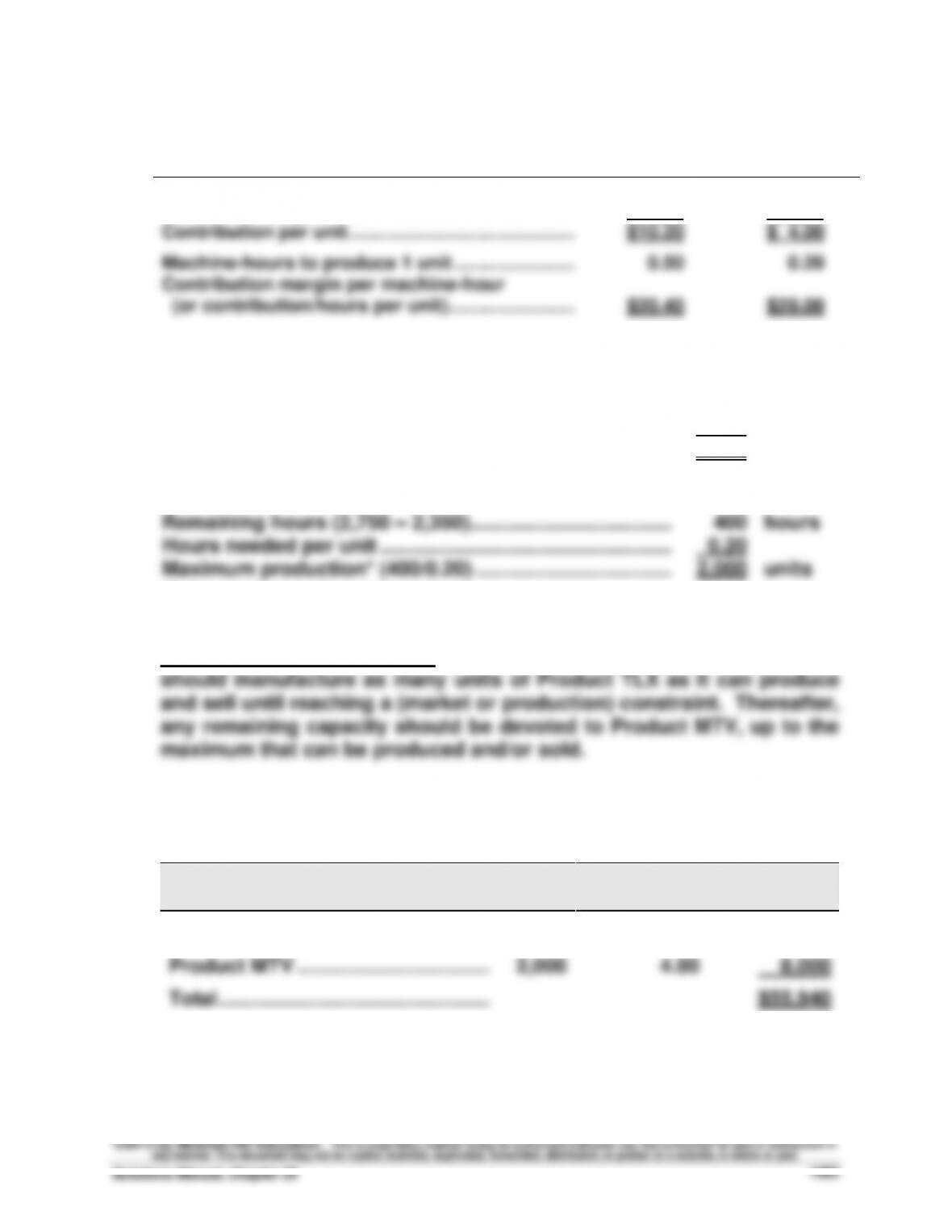

Preliminary computations

Contribution margin per hour

Product TLX

Product MTV

Selling price per unit …………………………………….……

$15.00

$ 9.50

Variable costs per unit ………………………………….……

4.80

5.50

Contribution per unit …………………………………….……

$10.20

$ 4.00

Machine-hours to produce 1 unit …………………..……

0.50

0.20

Contribution margin per machine-hour

(or contribution/hours per unit) …………………………

$20.40

$20.00

1. FOR PRODUCT TLX

Maximum sales ……………………………………………………….

4,700

units

Hours needed per unit …………………………………………….……..

0.50

Total hours used (4,700 x 0.50) ………………………………..……..

2,350

hours

FOR PRODUCT MTV

Remaining hours (2,750 – 2,350)……………………………………..

400

hours

Hours needed per unit …………………………………………….……..

0.20

Maximum production* (400/0.20) ……………………………..……..

2,000

units

*Below market maximum production.

SALES MIX RECOMMENDATION: These results suggest the company

2. CONTRIBUTION MARGIN FROM THE RECOMMENDED SALES MIX

Units

Contribution

per Unit

Total

Product TLX …………………………..…...

4,700

$10.20

$47,940

Product MTV ……………………………....

2,000

4.00

8,000

Total …………………………………………...

$55,940

Fundamental Accounting Principles, 21st Edition

1484

Exercise 25-18 (15 minutes)

1. Recovery time computation

Payback Period

Break-Even Time

$90,000 / $35,000 = 2.57 years

3.2 years (see answer for QS 25-15)

2. The advantage of break-even time is that it considers the time value of

3. When (1) the interest rate is very low, 1% for example, and (2) the

PROBLEM SET A

Problem 25-1A (50 minutes)

Part 1

Part 2

Net

Net Cash

Income

Flow

Expected annual sales of new product ……………...

$1,840,000

$1,840,000

Expected costs of new product

Direct materials ……………………………………………...

(480,000)

(480,000)

Direct labor …………………………………………………....

(672,000)

(672,000)

Overhead excluding depr. on new asset ………....

(336,000)

(336,000)

Depreciation on new asset ……………………………..

(115,000)

Selling and administrative expenses ……………....

(160,000)

(160,000)

Income before taxes ………………………………………....

77,000

Income taxes (30%) …………………………………………..

(23,100)

(23,100)

Net income ……………………………………………………….

$ 53,900

Net cash flow* …………………………………………………..

$ 168,900

Part 3

4 years

Fundamental Accounting Principles, 21st Edition

1486

Problem 25-1A (Continued)

Part 4

Accounting rate of return = = 21.56%

* Average investment

Asset cost ………………………………………………………………..……..

$480,000

Final year’s book value ……………………………………………..……..

20,000

Sum ………………………………………………………………………………..

$500,000

Average (Sum /2) ……………………………………………………….

$250,000

Part 5

Present Value of Net Cash Flows

Present

Present

Net Cash

Value of

Value of Net

Flows

1 at 7%

Cash Flows

Year 1 ………………………………………………….

$168,900

0.9346

$ 157,854

Year 2 ………………………………………………….

168,900

0.8734

147,517

Year 3 ………………………………………………….

168,900

0.8163

137,873

Year 4* ……………………………………………..….

188,900

0.7629

144,112

Totals ………………………………………………….

$695,600

587,356

Amount invested ………………………………….

(480,000)

Net present value ……………………………..….

$ 107,356

* Year 4’s cash flow includes the $20,000 salvage value.

$53,900

$250,000*

Problem 25-2A (55 minutes)

Part 1

PROJECT Y

Net income ……………………………………………………………………………...

$ 56,000

Depreciation expense* …………………………………………………………….

87,500

Net cash flow …………………………………………………………………………..

$143,500

*Annual depreciation = = $87,500

PROJECT Z

Net income ……………………………………………………………………………...

$ 36,400

Depreciation expense* …………………………………………………………….

116,667

Net cash flow …………………………………………………………………………..

$153,067

$350,000 – $0

3 years

Part 2

PROJECT Y

Payback Period = = 2.44 years

PROJECT Z

$350,000

$350,000 – $0

4 years

$350,000

$143,500

PROJECT Z

Problem 25-2A (Continued)

Part 3

PROJECT Y

Accounting rate of return = = 32%

$56,000

$175,000*

Problem 25-2A (Continued)

Part 4

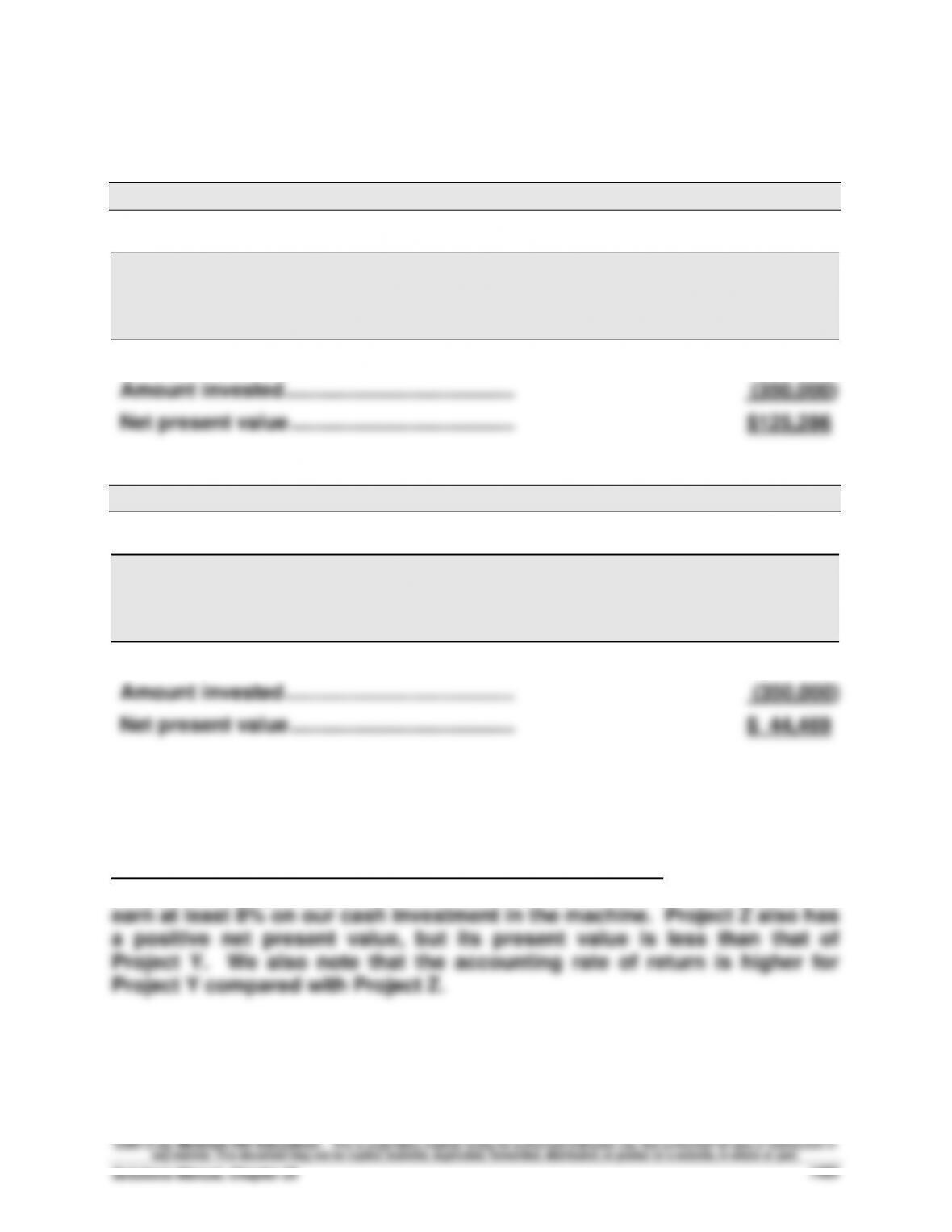

PROJECT Y

Present Value of Net Cash Flows

Present

Present

Value of

Value of

Net Cash

Flows

1 at 8%

Annuity

Net Cash

Flows

Years 1-4 ………………………………………………

$143,500

3.3121

$475,286

Amount invested …………………………………..

(350,000)

Net present value ………………………………….

$125,286

PROJECT Z

Present Value of Net Cash Flows

Present

Present

Value of

Value of

Net Cash

Flows

1 at 8%

Annuity

Net Cash

Flows

Years 1-3 ………………………………………………

$153,067

2.5771

$394,469

Amount invested …………………………………..

(350,000)

Net present value ………………………………….

$ 44,469

Part 5

Recommendation to management is to pursue Project Y. This is because

Project Y has a positive net present value, which means that we expect it to

Fundamental Accounting Principles, 21st Edition

1490

Problem 25-3A (60 minutes)

Part 1

RESULTS USING STRAIGHT-LINE DEPRECIATION

(a)

Income

Before

Deprec.

(b)

Straight–

Line

Deprec.

(c)

Taxable

Income

(a) – (b)

(d)

40%

Income

Taxes

(e)

Net Cash

Flows

(a) – (d)

Year 1 ……….………………

$66,000

$ 9,000

$57,000

$22,800

$43,200

Year 2 ……….………………

66,000

18,000

48,000

19,200

46,800

Year 3 ……….………………

66,000

18,000

48,000

19,200

46,800

Year 4 ……….………………

66,000

18,000

48,000

19,200

46,800

Year 5 ……….………………

66,000

18,000

48,000

19,200

46,800

Year 6 ……….………………

66,000

9,000

57,000

22,800

43,200

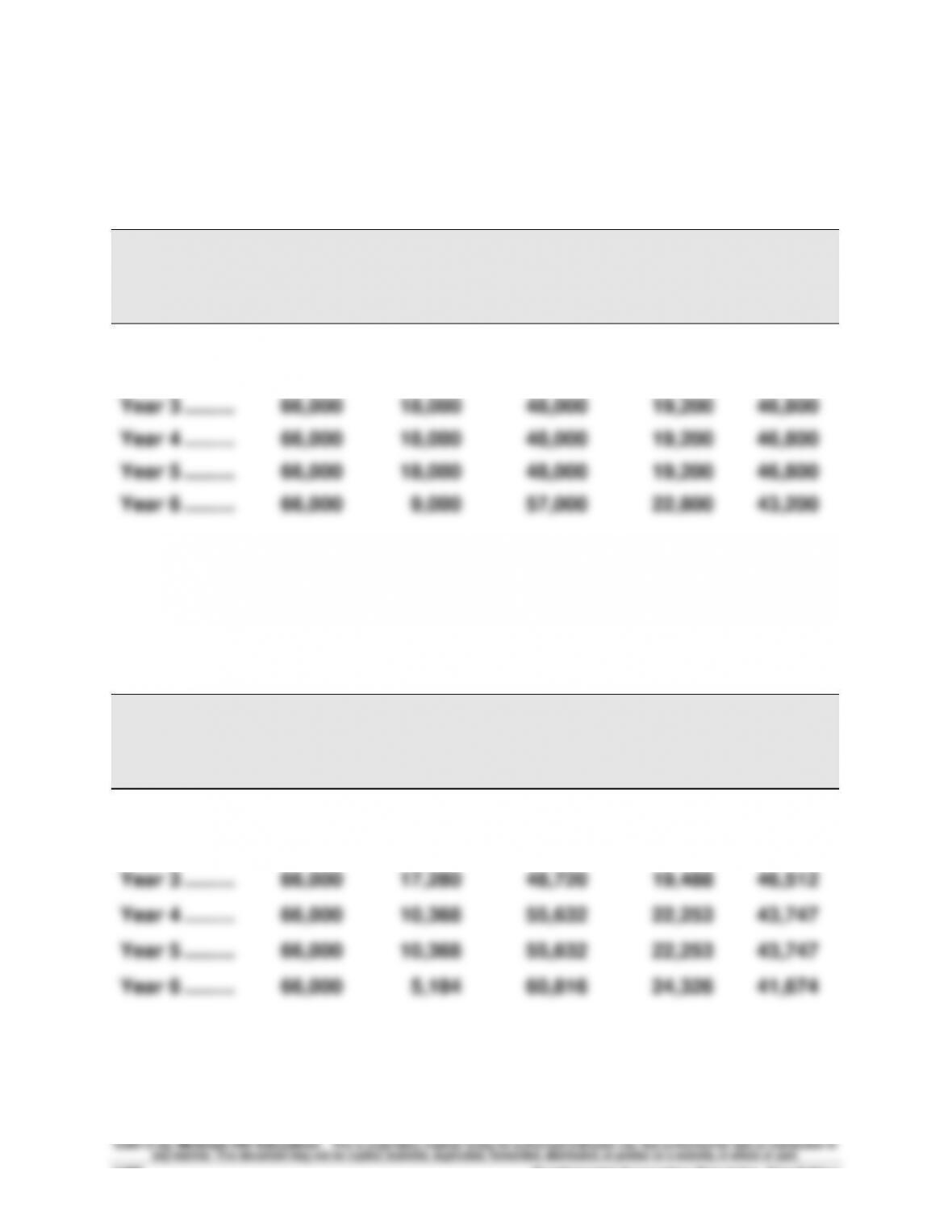

Part 2

RESULTS USING MACRS DEPRECIATION

(a)

Income

Before

Deprec.

(b)

MACRS

Deprec.

(c)

Taxable

Income

(a) – (b)

(d)

40%

Income

Taxes

(e)

Net Cash

Flows

(a) – (d)

Year 1 ……….………………

$66,000

$18,000

$48,000

$19,200

$46,800

Year 2 ……….………………

66,000

28,800

37,200

14,880

51,120

Year 3 ……….………………

66,000

17,280

48,720

19,488

46,512

Year 4 ……….………………

66,000

10,368

55,632

22,253

43,747

Year 5 ……….………………

66,000

10,368

55,632

22,253

43,747

Year 6 ……….………………

66,000

5,184

60,816

24,326

41,674

Problem 25-3A (Continued)

Part 3

NET PRESENT VALUE OF ASSET USING STRAIGHT-LINE DEPRECIATION

Present

Present

Value of

Net Cash

Flows

Value of

1 at 10%

Net Cash

Flows

Year 1 ………………………………………………….

$ 43,200

0.9091

$ 39,273

Year 2 ………………………………………………….

46,800

0.8264

38,676

Year 3 ………………………………………………….

46,800

0.7513

35,161

Year 4 ………………………………………………….

46,800

0.6830

31,964

Year 5 ………………………………………………….

46,800

0.6209

29,058

Year 6 ………………………………………………….

43,200

0.5645

24,386

Totals ………………………………………………….

$273,600

198,518

Amount invested ………………………………….

(90,000)

Net present value …………………………………

$108,518

Part 4

NET PRESENT VALUE OF ASSET USING MACRS DEPRECIATION

Present

Present

Value of

Net Cash

Flows

Value of

1 at 10%

Net Cash

Flows

Year 1 ………………………………………………….

$ 46,800

0.9091

$ 42,546

Year 2 ………………………………………………….

51,120

0.8264

42,246

Year 3 ………………………………………………….

46,512

0.7513

34,944

Year 4 ………………………………………………….

43,747

0.6830

29,879

Year 5 ………………………………………………….

43,747

0.6209

27,163

Year 6 ………………………………………………….

41,674

0.5645

23,525

Totals ………………………………………………….

$273,600

200,303

Amount invested ………………………………….

(90,000)

Net present value …………………………………

$110,303

Part 5

Analysis: The net present value using MACRS depreciation is greater than the

Fundamental Accounting Principles, 21st Edition

1492

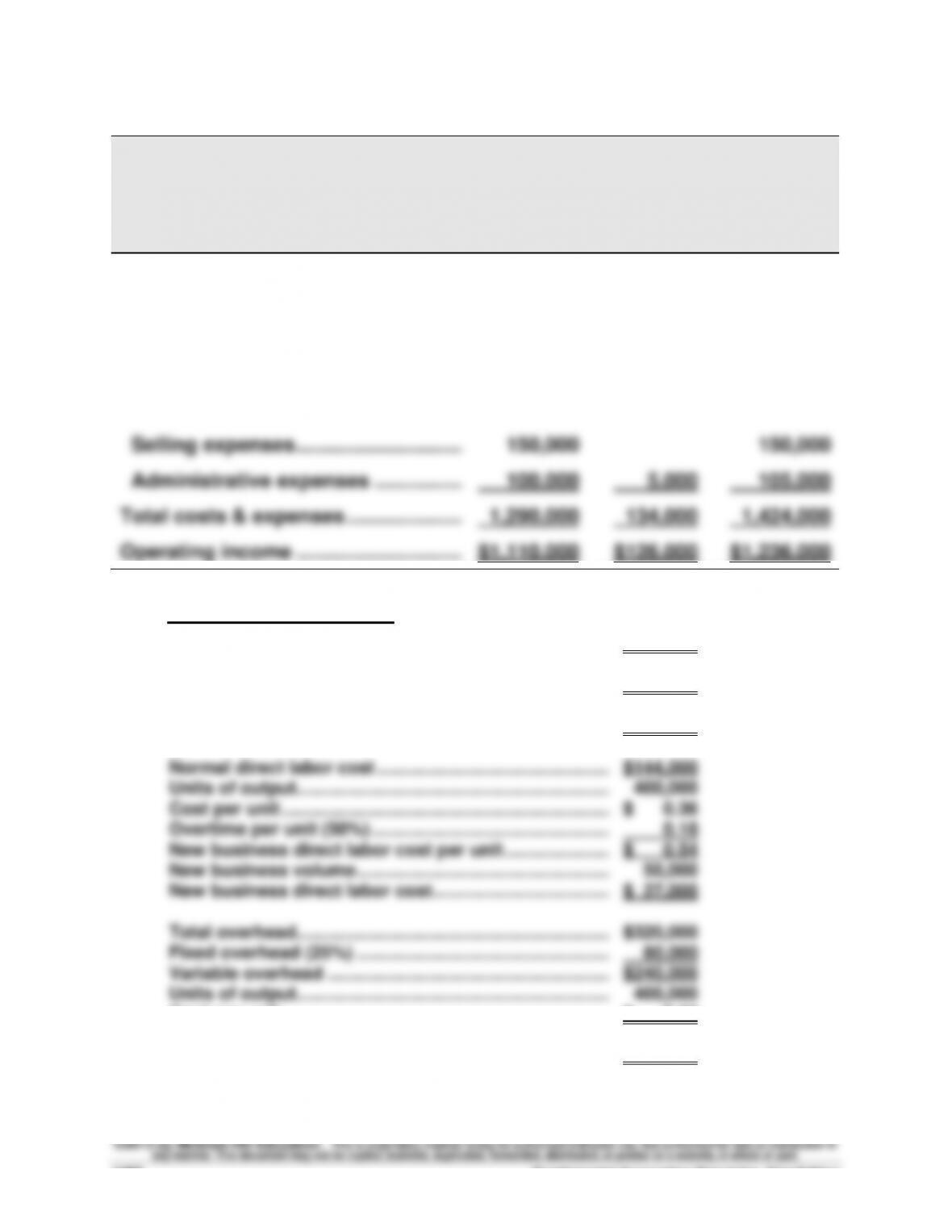

Problem 25-4A (45 minutes)

JONES PRODUCTS

COMPARATIVE INCOME STATEMENTS

(1)

(2)

(3)

Normal

New

Volume

Business

Combined

Sales …………………………………………….……..

$2,400,000

$260,000

$2,660,000

Costs and expenses

Direct materials …………………………..

576,000

72,000

648,000

Direct labor ………………………………………..

144,000

27,000

171,000

Overhead …………………………………………..

320,000

30,000

350,000

Selling expenses …………………………..

150,000

150,000

Administrative expenses …………….……..

100,000

5,000

105,000

Total costs & expenses ………………………..

1,290,000

134,000

1,424,000

Operating income …………………………..

$1,110,000

$126,000

$1,236,000

Supporting computations

Normal direct materials cost ………………………………….

$576,000

Units of output ……………………………………………………...

400,000

Cost per unit ………………………………………………………...

$ 1.44

New business volume …………………………………………...

50,000

New business direct materials cost ………………………..

$ 72,000

Normal direct labor cost ………………………………………..

$144,000

Units of output ……………………………………………………...

400,000

Cost per unit ………………………………………………………...

$ 0.36

Overtime per unit (50%) ………………………………………...

0.18

New business direct labor cost per unit ………………….

$ 0.54

New business volume …………………………………………...

50,000

New business direct labor cost ……………………………...

$ 27,000

Total overhead ……………………………………………………...

$320,000

Fixed overhead (25%) …………………………………………...

80,000

Variable overhead ………………………………………………...

$240,000

Units of output ……………………………………………………...

400,000

Cost per unit ………………………………………………………...

$ 0.60

New business volume …………………………………………...

50,000

New business variable overhead cost …………………….

$ 30,000