Title: Exercise 21-7

QA_Ori:

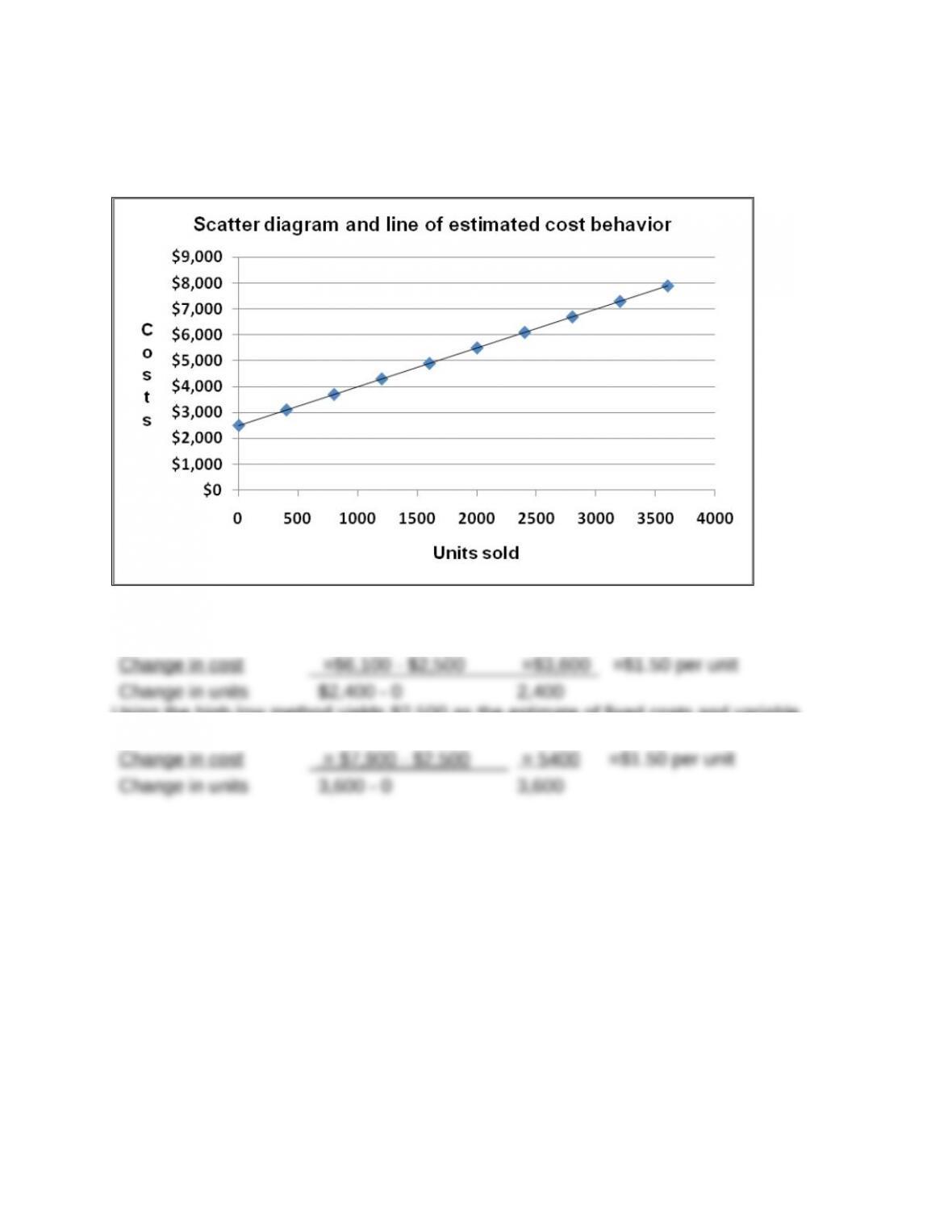

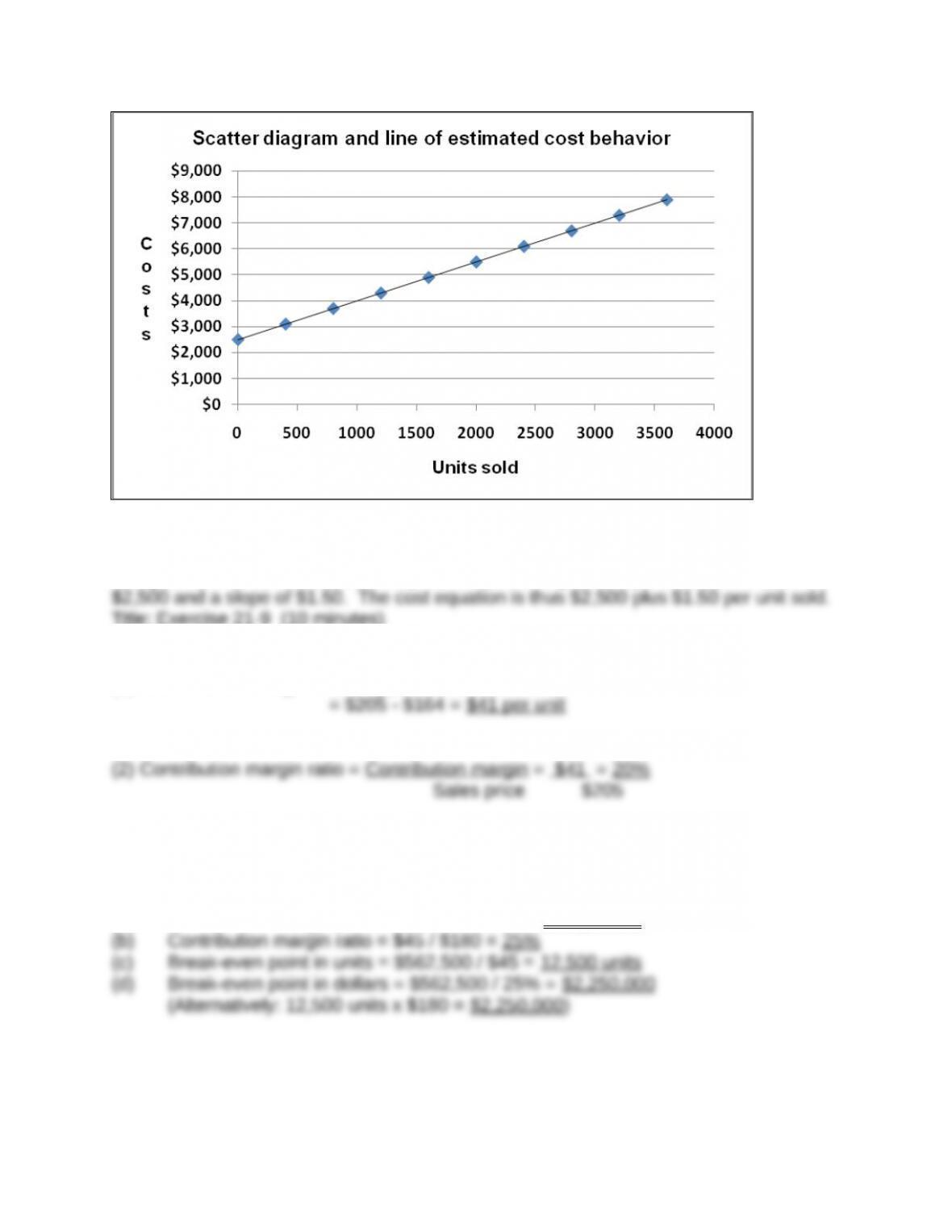

The scatter diagram and line of estimated cost behavior appear below.

Selecting 0 and 2,400 units sold as the activity levels yields $2,500 as the estimate of

fixed costs and the following estimate of variable costs per unit:

Using the high-low method yields $2,500 as the estimate of fixed costs and variable

costs per unit of:

Title: Exercise 21-8A

QA_Ori:

(3) The contribution margin of 20% implies that for each $1 in sales, the company has

$0.20 that contributes to fixed costs and profit.

Title: Exercise 21-10 (30 minutes)

QA_Ori:

(a) Contribution margin per unit = $180 – $135 = $45 per unit

Title: Exercise 21-12

QA_Ori:

1.

BLANCHARD COMPANY

Contribution Margin Income Statement (at Break-Even)

Sales (12,500 x $180) $2,250,000

2. Sales (in dollars) to break even with increased fixed costs

Break-even = (Original fixed costs + Additional fixed costs)

Contribution margin ratio

Title: Exercise 21-13 (25 minutes)

QA_Ori:

Preliminary computations

Pretax income = After-tax income / (1 – Tax rate)

Income taxes = Pretax income x tax rate

Unit sales at target income = Fixed costs + Pretax income

Contribution margin/unit

$45

Dollar sales at target income = Fixed costs + Pretax income

Contribution margin ratio

Title: Exercise 21-14

QA_Ori:

BLANCHARD COMPANY

Forecasted Contribution Margin Income Statement

Sales (40,000 x $200) $8,000,000

Variable costs (40,000 x $140) 5,600,000

Title: Exercise 21-15

QA_Ori:

1 Pretax income = Sales – Variable costs – Fixed costs

2 Instructor note: Use the equation in Exhibit 21.23 with no tax effects

Unit sales = fixed costs + Target Pretax income

Contribution margin per unit

Title: Exercise 21-16

QA_Ori:

(a) Total expected variable costs

= Variable costs per unit x units produced and sold

= $60* x 200,000 units

= $12,000,000

*The $60 variable costs per unit is computed by determining (i) sales

price per unit and (ii) subtracting contribution margin per unit:

Sales price per unit ($17,000,000 / 200,000 units) $ 85

Title: Exercise 21-17

QA_Ori:

1. Selling price per composite unit

8 windows @ $200 per unit $1,600

3. Break-even point in composite units

Fixed costs

= Contribution margin per composite unit

4. Unit sales of windows and doors at break-even point

QA_Edit:

2. Variable costs per composite unit

Title: Exercise 21-18

QA_Ori:

Contribution Percentage of Weighted

margin per unit x sales mix = unit CM

Weighted-average

contribution margin $90

(3) Unit sales of windows and doors at break-even point:

Title: Exercise 21-19

QA_Ori:

1. Selling price per composite unit

2. Variable costs per composite unit

3. Break-even point in composite units

Fixed costs .

= Contribution margin per composite unit

4. Unit sales of Easy, Moderate, and Business returns at break-even point

Easy: 5 x 30 units (from 3) 150 units

Title: Exercise 21-20

QA_Ori:

Contribution Percentage of

Weighte

d

1) Margin per unit x sales mix = Unit CM

50% $10

Weighted-average contribution margin $60

(3) Unit sales of Easy, Moderate, and Business returns at break-even point:

Easy: 50% x 300 units (from 2) 150 units

Title: Exercise 21-21

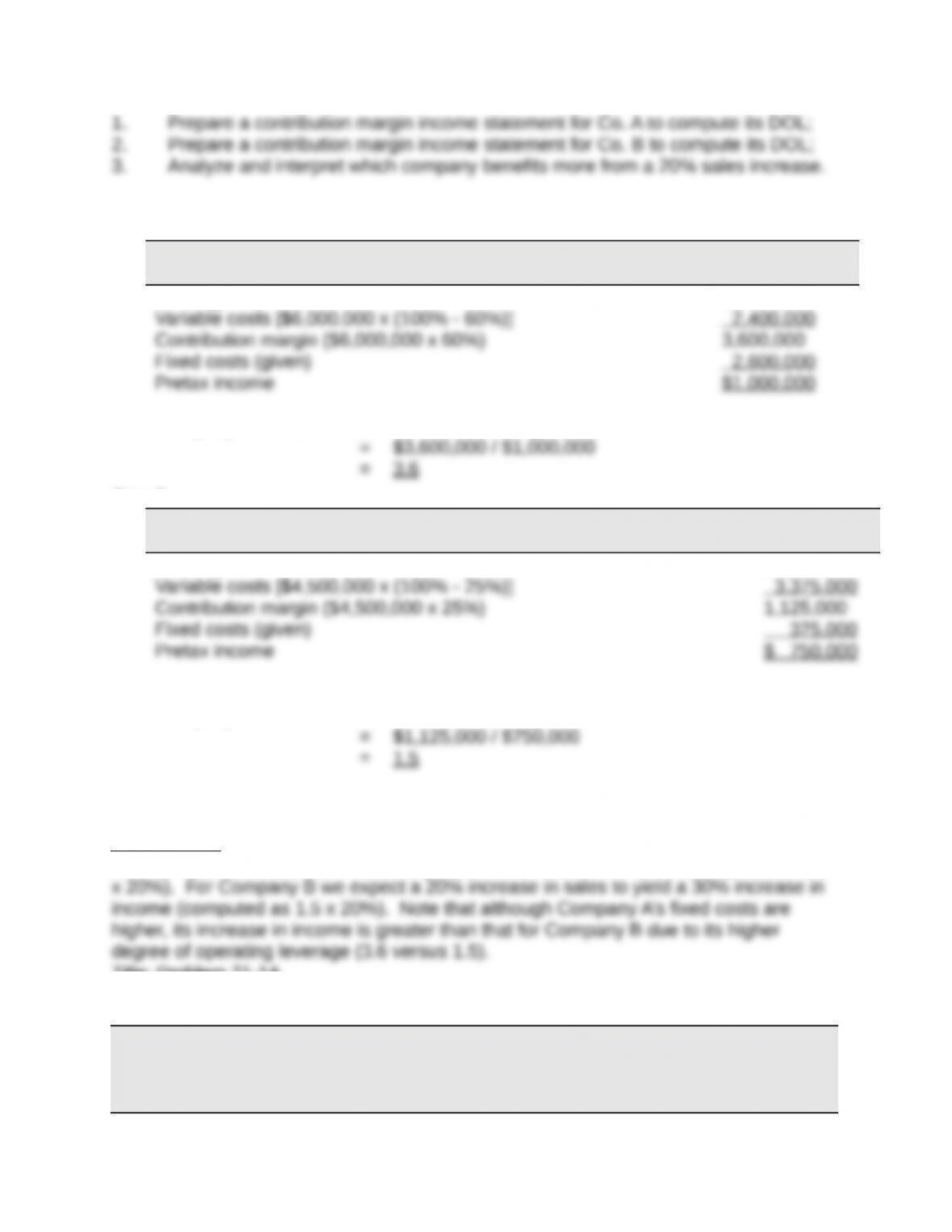

QA_Ori:

Instructor note: This exercise is solved in 3 steps

Step 1.

Company A

Contribution Margin Income Statement

Sales (given) $6,000,000

Company A’s DOL = Contribution margin in dollars / Pretax income

Step 2.

Company B

Contribution Margin Income Statement

Sales (given) $4,500,000

Company B’s DOL = Contribution margin in dollars / Pretax income

Step 3.

Interpretation: Company A benefits more from a 20% increase in sales. This is because

we expect a 20% increase in sales to yield a 72% increase in income (computed as 3.6

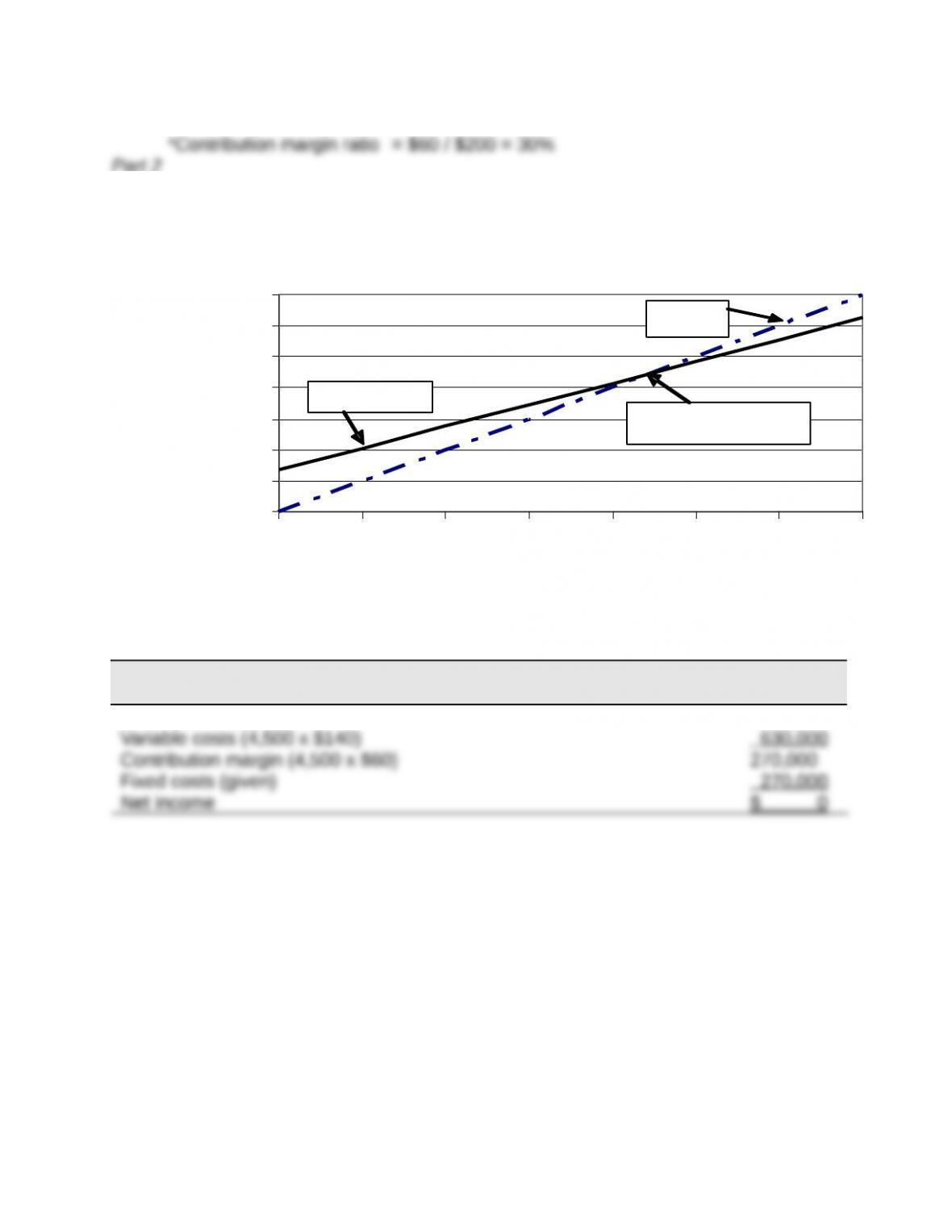

Title: Problem 21-1A

QA_Ori:

Parts 1 and 2

Tom Thompson Company

Contribution Margin Income Statement

For Year Ended December 31, 2013

(1,000 units) Per unit % of sales

Sales ($500 x 1,000) $500,000 $500 100%

Variable costs

Plastic for casing $17,000 $17

The contribution margin per unit is $360, and the contribution margin ratio is 72%.

Part 3 Analysis Component

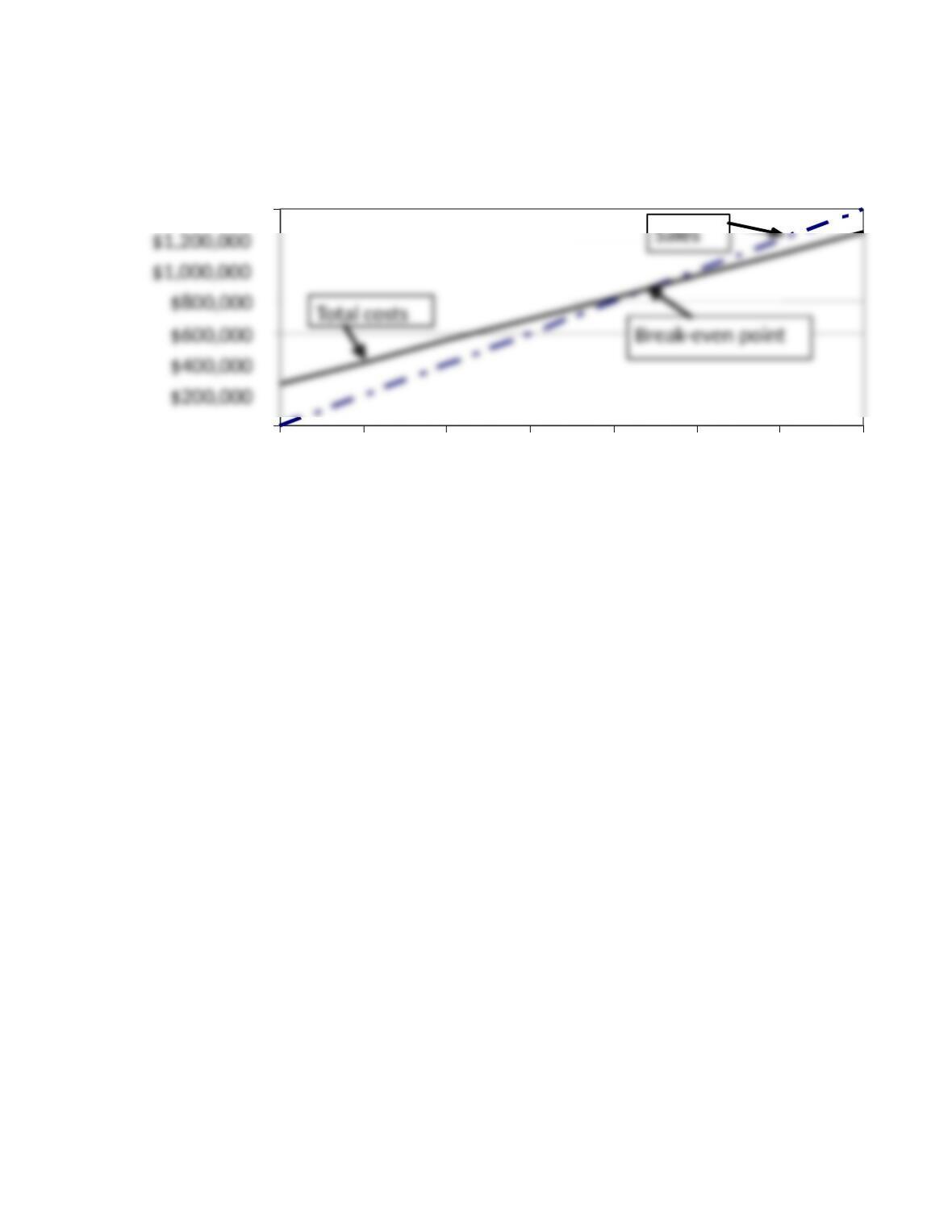

Title: Problem 21-2A

QA_Ori:

Part 1

Instructor note: Use the equation in Exhibit 21.11

Break-even in sales units = Fixed costs / Contribution margin per unit

Instructor note: Use the equation in Exhibit 21.12

Break-even in sales dollars = Fixed costs / Contribution margin ratio

$ 0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

0 1,000 2,000 3,000 4,000 5,000 6,000 7,000

Units (100 yards)

Total costs

Sales

Break-even point

Part 2

CVP Chart for Xcite Equipment Company

Part 3

XCITE EQUIPMENT CO.

Contribution Margin Income Statement (at Break-Even) — Product XT

Sales (4,500 x $200) $900,000

$ 0

$400,000

$1,400,000

0 1,000 2,000 3,000 4,000 5,000 6,000 7,000

Units (100 yards)

Sales