Title: Exercise 23-9A

QA_Ori:

1.

Goods in Process Inventory 288,000

To record the favorable price and quantity variances.

* This price variance can alternatively be computed and recorded when the direct

materials are

purchased.

2.

To close the unfavorable price and favorable quantity

variances to cost of goods sold.

3. The $24,000 materials quantity variance should be investigated because of its

QA_Edit:

Title: Exercise 23-10

QA_Ori:

Information given

Planned units to be produced = 80% x 50,000 capacity = 40,000 units

1. Total overhead planned at 80% level (25,000 direct labor hours)

Predetermined

Cost

Cost per

Hour

2. Total overhead variance

Total actual overhead (given) $305,000

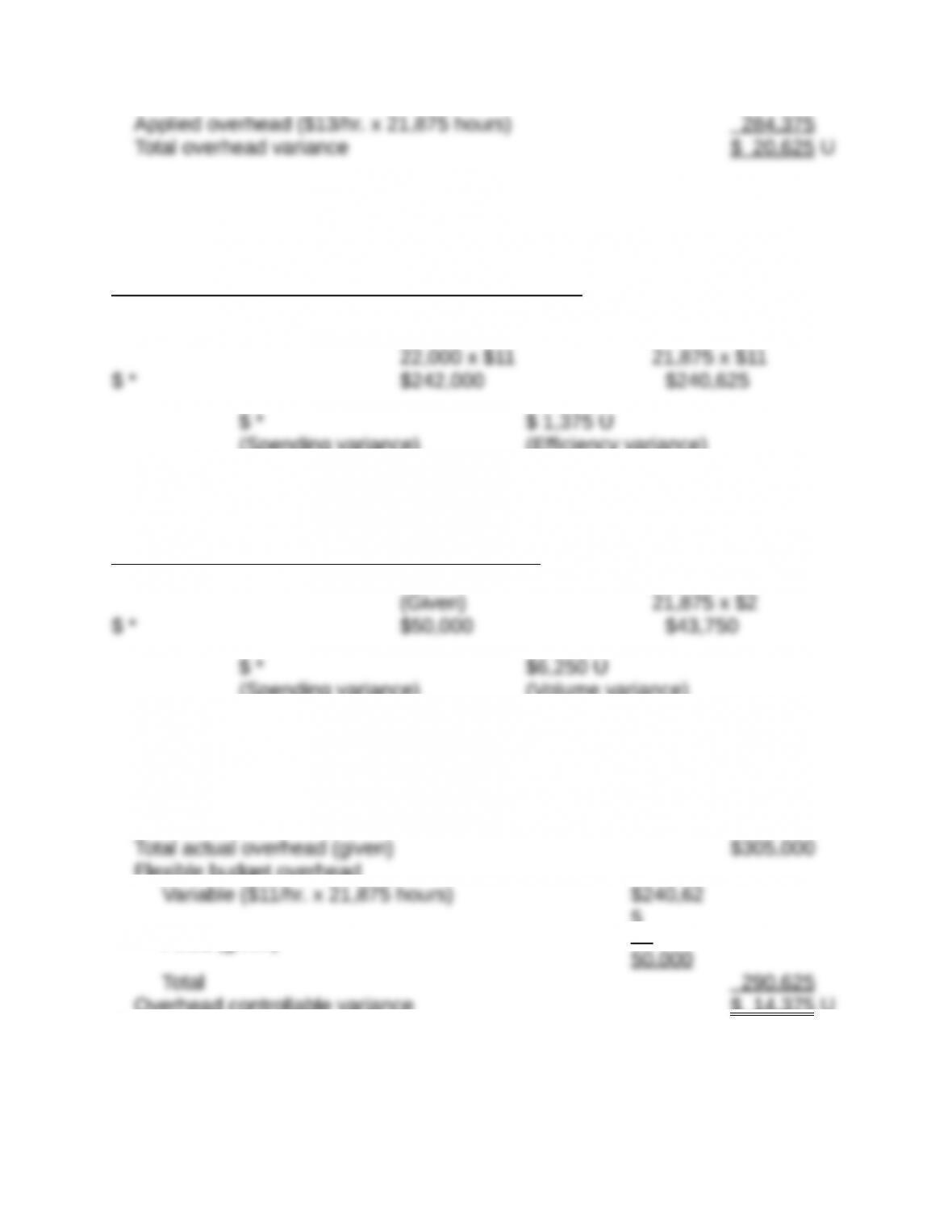

Title: Exercise 23-11

QA_Ori:

1. Preliminary variance computations

Variable overhead spending and efficiency variances

Actual Overhead

AH x AVR AH x SVR

Applied Overhead

SH x SVR

(Spending variance)

(Efficiency variance)

$ *

(Total variable overhead variance)

Fixed overhead spending and volume variances

Actual Overhead Budgeted Overhead Applied Overhead

(Spending variance)

(Volume variance)

$ *

(Total fixed overhead variance)

* Not computable from information given

2. Overhead controllable variance*

Flexible budget overhead

5

Fixed (given)

Overhead controllable variance $ 14,375 U

* Alternative solution approach: We know the overhead controllable variance

is equal to the total overhead variance less the overhead volume variance. Then,

using the results from parts 1 and 2, we can compute the overhead controllable

variance as

Title: Exercise 23-12

QA_Ori:

1. Sales price and sales volume variances

Sales Actual Sales Flexible Budget Fixed Budget

Units 350 350 365

2. Interpretation

The $35,000 favorable sales price variance implies it sold computers for a higher

Title: Exercise 23-13

QA_Ori:

a. 4

Title: Exercise 23-14

QA_Ori:

Title: Exercise 23-15

QA_Ori:

Following management by exception, the company should focus on those

variances that exhibit the greatest differences from the standard. This would

Title: Exercise 23-16

QA_Ori:

Part 1

Direct materials price variance:

Actual cost of direct materials used (16,000 x $4.05) $ 64,800

Direct materials quantity variance:

Actual quantity used x Standard price (16,000 x $4.00) $ 64,000

Part 2

Direct labor rate variance:

Actual hours x Actual rate per hour (5,545 x $19.00***) $105,355

Direct labor efficiency variance:

Actual hours x Standard rate per hour (5,545 x $20.00) $110,900

Title: Problem 23-1A

QA_Ori:

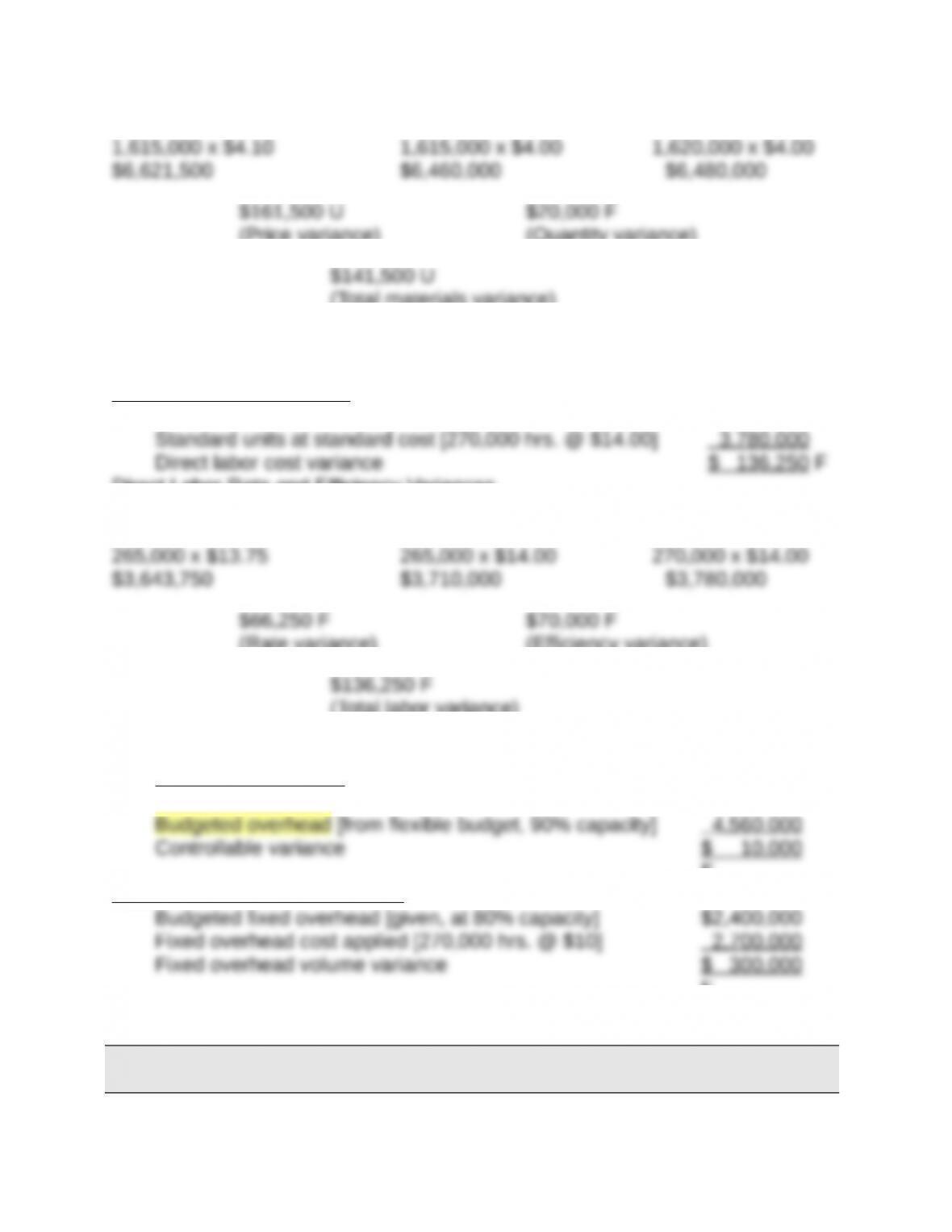

Part 1 Direct Materials Variances

Direct materials cost variances

Actual units at actual cost [1,615,000 lbs. @ $4.10] $6,621,500

Direct Materials Price and Quantity Variances

Actual Cost Standard Cost

AQ x AP AQ x SP SQ x SP

(Price variance)

(Quantity variance)

(Total materials variance)

Part 2 Direct Labor Variances

Direct labor cost variances

Actual units at actual cost [265,000 hrs. @ $13.75] $3,643,750

Direct Labor Rate and Efficiency Variances

Actual Cost

AH x AR AH x SR

Standard Cost

SH x SR

(Rate variance)

(Efficiency variance)

(Total labor variance)

Part 3 Overhead Variances

Controllable variance

Actual overhead [$2,350,000 + $2,200,000] $4,550,000

F

Fixed overhead volume variance

F

Title: Problem 23-3A

Part 1

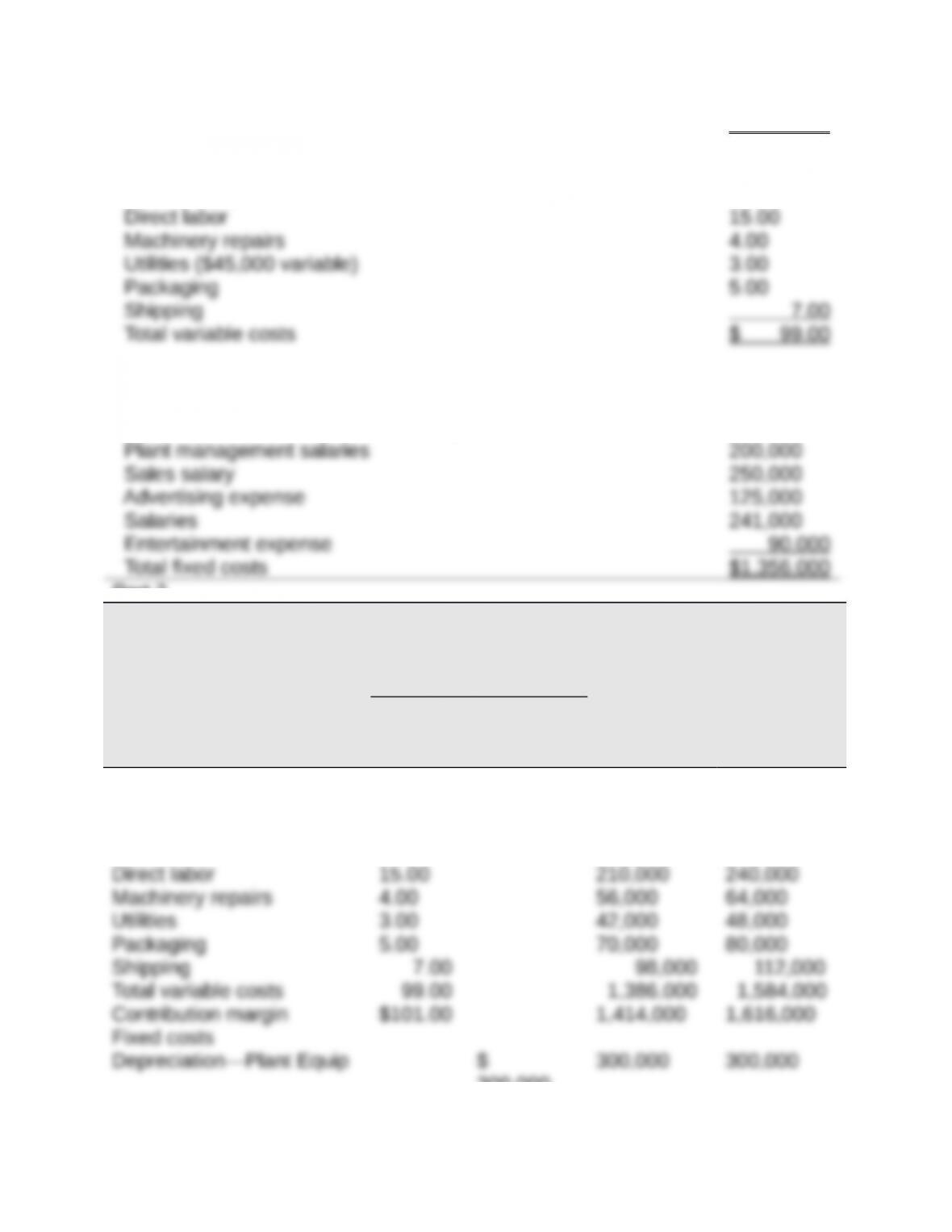

Variable or Fixed Classification

Amount

per unit

Variable sales (total divided by 15,000 units)

Sales $ 200.00

Variable costs (total divided by 15,000 units)

Direct materials $ 65.00

Fixed costs

Depreciation—Plant equipment $ 300,000

Utilities ($195,000 – $45,000 variable) 150,000

Part 2

PHOENIX COMPANY

Flexible Budgets

For Year Ended December 31, 2013

Flexible Budget Flexible Flexible

Variable

Amount

per Unit

Total

Fixed

Cost

Budget for

Unit Sales

of 14,000

Budget for

Unit Sales

of 16,000

Sales

$200.00 $2,800,000 $3,200,000

Variable costs

Direct materials 65.00 910,000 1,040,000

300,000

Utilities 150,000 150,000 150,000

Part 3

Operating income increase for a 15,000 to 18,000 unit sales increase

Possible sales (units) 18,000 Units

*Alternate solution format

Unit increase 3,000 Unit

s

Part 4

Operating income (loss) at 12,000 units

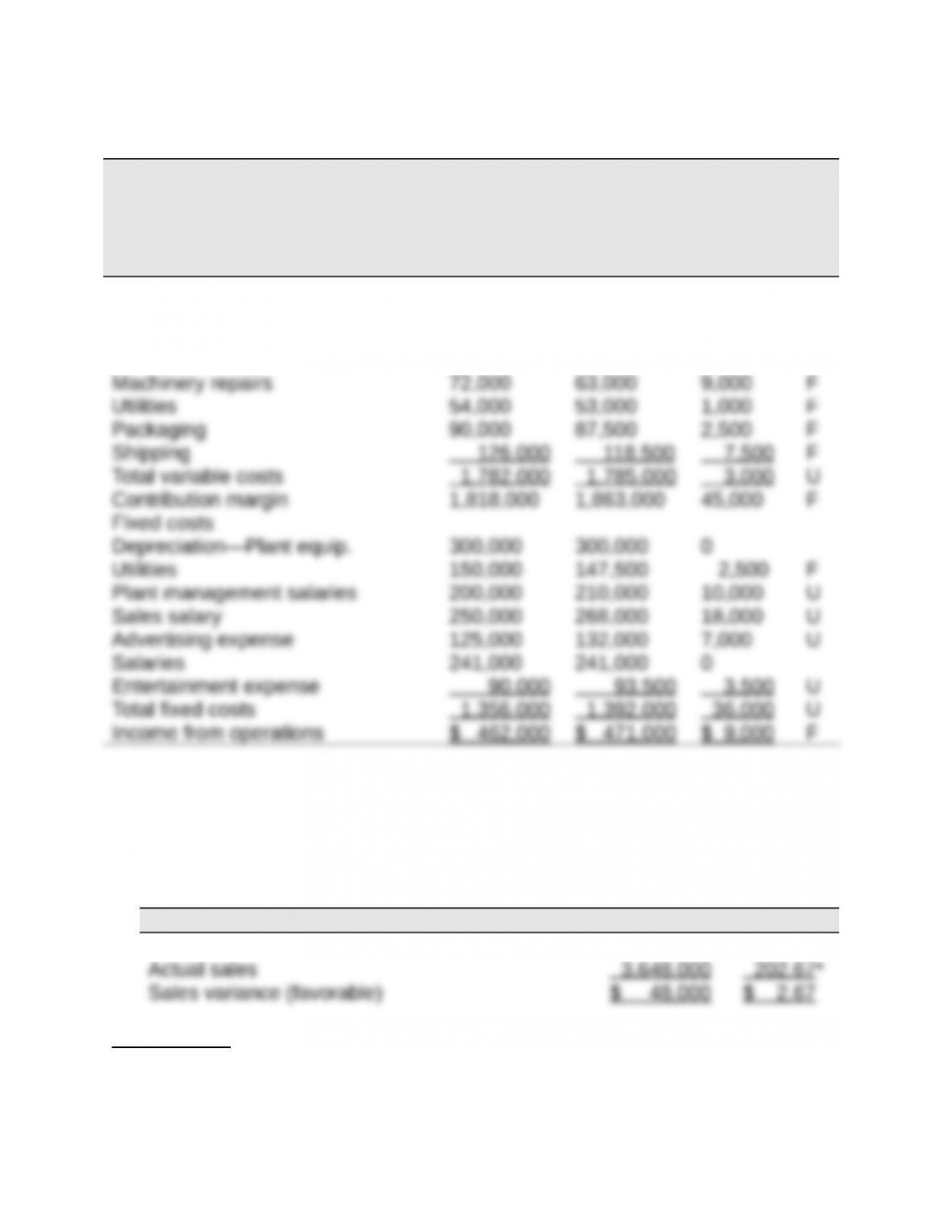

Title: Problem 23-4A

QA_Ori:

Part 1

PHOENIX COMPANY

Flexible Budget Performance Report

For Year Ended December 31, 2013

Flexible Actual

Budget Results Variances*

Sales (18,000 units) $3,600,000 $3,648,000 $48,000 F

Variable costs

Direct materials 1,170,000 1,185,000 15,000 U

Direct labor 270,000 278,000 8,000 U

*F = Favorable variance; and U = Unfavorable variance.

Part 2

Analysis of sales variance

Total Per unit

Budgeted sales $3,600,000 $200.00

Interpretation: The sales variance is favorable because the actual price was

higher than planned.

* (rounded)

Analysis of direct materials variance

Total Per unit

Budgeted materials $1,170,000 $ 65.00

Interpretation: The direct materials variance is unfavorable for two possible