Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

1092 Fundamental Accounting Principles, 21st Edition

Exercise 19-18 (35 minutes)

1. Estimated cost of the architectural job

Labor type

Estimated

hours

Hourly rate

Total cost

Architects ................................

150

$300

$ 45,000

Staff ................................

300

75

22,500

Clerical ................................

500

20

10,000

Total labor cost.........................................................................

77,500

Overhead @ 175% of direct labor cost ................................

135,625

Total estimated cost................................................................

$213,125

2. Frey should first determine an estimated selling price, based on its cost

and desired profit for this job.

Total estimated cost ................................................................

$213,125

Desired profit ............................................................................

80,000

Estimated selling price ............................................................

$293,125

This $293,125 price may or may not be its bid. It must consider past

experiences and competition. It might make the bid at the low end of

what it believes the competition will bid. By bidding at about $285,000,

the profit on the job will only be $71,875 ($285,000 – $213,125). While

this may allow Frey to get the job, it must consider several other factors.

Among them:

a. How accurate are its estimates of costs? If costs are understated,

the bid may be too low. This will cause profits to be lower than

anticipated. If costs are overestimated, it may bid too high and lose

the job.

Exercise 19-19 (15 minutes)

(1)

Raw Materials Inventory ...............................................

3,108

Accounts Payable ....................................................

3,108

To record raw material purchases.

Goods in Process Inventory* ................................

3,106

Raw Materials Inventory .........................................

3,106

To record raw materials used in production.

* The amount of raw materials used in production is computed from the Raw Materials

Inventory account. Beginning balance plus purchases minus ending balance equals

raw materials used in production, or (in millions), €83 + €3,108 - €85 = €3,106.

(2) The amount of materials purchased is almost equal to the amount of

1094 Fundamental Accounting Principles, 21st Edition

PROBLEM SET A

Problem 19-1A (80 minutes)

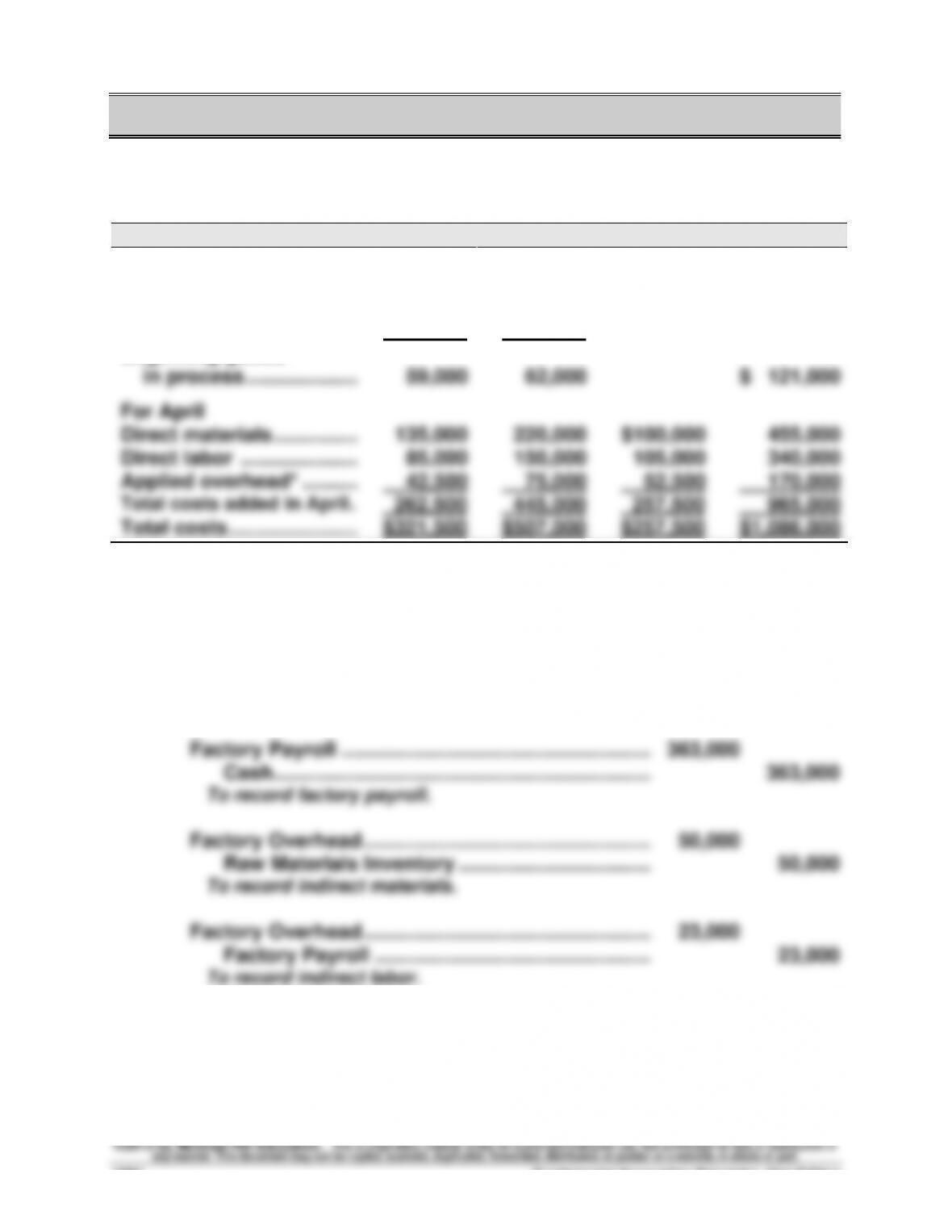

Part 1 Total manufacturing costs and the costs assigned to each job

306

307

308

April Total

From March

Direct materials ......................

$ 29,000

$ 35,000

Direct labor .............................

20,000

18,000

Applied overhead* .................

10,000

9,000

Beginning goods

in process ...........................

59,000

62,000

$ 121,000

For April

Direct materials ......................

135,000

220,000

$100,000

455,000

Direct labor ............................

85,000

150,000

105,000

340,000

Applied overhead* .................

42,500

75,000

52,500

170,000

Total costs added in April .........

262,500

445,000

257,500

965,000

Total costs ..............................

$321,500

$507,000

$257,500

$1,086,000

*Equals 50% of direct labor cost.

Part 2 Journal entries for April

a.

Raw Materials Inventory ................................................

500,000

Accounts Payable ....................................................

500,000

To record materials purchases.

Factory Payroll ...............................................................

363,000

Cash ...........................................................................

363,000

To record factory payroll.

Factory Overhead ...........................................................

50,000

Raw Materials Inventory ..........................................

50,000

To record indirect materials.

Factory Overhead ...........................................................

23,000

Factory Payroll .........................................................

23,000

To record indirect labor.

Factory Overhead ...........................................................

32,000

Cash ...........................................................................

32,000

To record factory rent.

Problem 19-1A (Continued)

a. [continued from prior page]

Factory Overhead ...........................................................

19,000

Cash ...........................................................................

19,000

To record factory utilities.

Factory Overhead ...........................................................

51,000

Accumulated Depreciation—Factory Equip ..........

51,000

To record other factory overhead.

b.

Goods in Process Inventory ..........................................

455,000

Raw Materials Inventory ..........................................

455,000

To assign direct materials to jobs.

Goods in Process Inventory ..........................................

340,000

Factory Payroll .........................................................

340,000

To assign direct labor to jobs.

Goods in Process Inventory ..........................................

170,000

Factory Overhead .....................................................

170,000

To apply overhead to jobs.

c.

Finished Goods Inventory (306 & 307) ..........................

828,500

Goods in Process Inventory ................................

828,500

To record jobs completed ($321,500 + $507,000).

d.

Cost of Goods Sold (306) ...............................................

321,500

Finished Goods Inventory ................................

321,500

To record cost of sale of job.

e.

Cash .................................................................................

635,000

Sales ..........................................................................

635,000

To record sale of job.

f.

Cost of Goods Sold ........................................................

5,000

Factory Overhead* ...................................................

5,000

To assign underapplied overhead.

*Overhead applied to jobs .....

$170,000

Overhead incurred

Indirect materials........................

$50,000

Indirect labor ..............................

23,000

Factory rent ................................

32,000

Factory utilities ...........................

19,000

Factory equip. depreciation. .....

51,000

175,000

Underapplied overhead .............

$ 5,000

1096 Fundamental Accounting Principles, 21st Edition

Problem 19-1A (Continued)

Part 3

CIOLINO COMPANY

Manufacturing Statement

For Month Ended April 30

Direct materials used ................................................................

$ 455,000

Direct labor used .........................................................................

340,000

Factory overhead

Indirect materials................................................................

$50,000

Indirect labor.............................................................................

23,000

Factory rent...............................................................................

32,000

Factory utilities .........................................................................

19,000

Depreciation of equipment ......................................................

51,000

175,000

Total manufacturing costs .........................................................

970,000

Add goods in process March 31 (Jobs 306 & 307) ...................

121,000

Total cost of goods in process ..................................................

1,091,000

Deduct goods in process, April 30 (Job 308) ...........................

(257,500)

Deduct underapplied overhead* ................................................

(5,000)

Cost of goods manufactured .....................................................

$ 828,500

*Alternatively, the underapplied overhead can be listed among factory overhead items.

Part 4

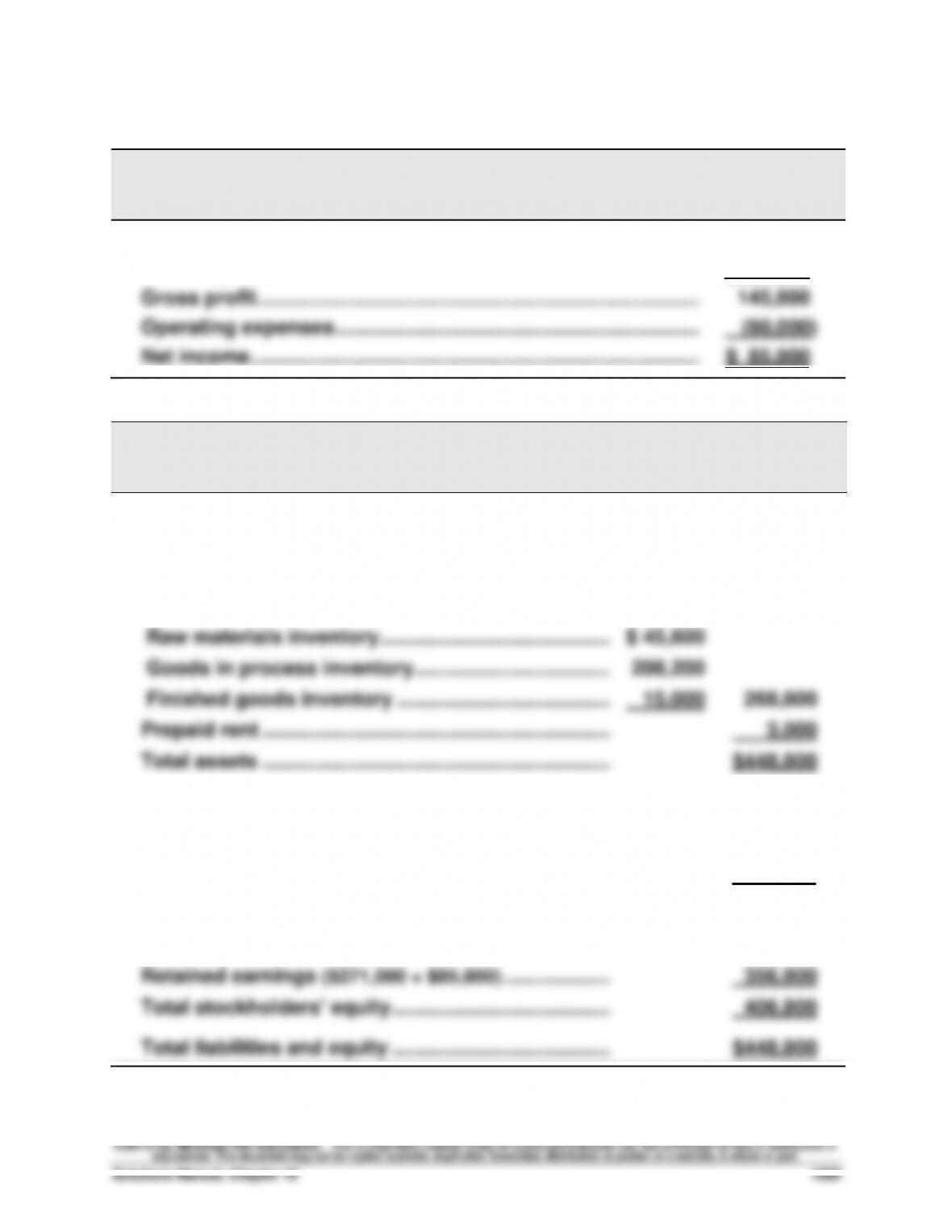

Gross profit on the income statement for the month ended April 30

Sales ..........................................................................................................

$ 635,000

Cost of goods sold ($321,500 + $5,000) ..................................................

(326,500)

Gross profit ...............................................................................................

$ 308,500

Presentation of inventories on the April 30 balance sheet

Inventories

Raw materials ..........................................................................................

$ 75,000*

Goods in process (Job 308).....................................................................

257,500

Finished goods (Job 307) ........................................................................

507,000

Total inventories ......................................................................................

$ 839,500

* Beginning raw materials inventory ................................

$ 80,000

Purchases ................................................................

500,000

Direct materials used ................................................................

(455,000)

Indirect materials used ................................................................

(50,000)

Ending raw materials inventory ................................

$ 75,000

Part 5

Overhead is underapplied by $5,000, meaning that individual jobs or batches of

jobs are under-costed. Thus, profits at the job (and batch) level are overstated.

Problem 19-2A (75 minutes)

Part 1

a.

Dec. 31

Goods in Process Inventory ................................

28,800

Raw Materials Inventory ................................

28,800

To record direct materials costs for

Jobs 402 and 404 ($10,200 + 18,600).

b.

Dec. 31

Goods in Process Inventory ................................

59,800

Factory Payroll .........................................................

59,800

To record direct labor costs for

Jobs 402 and 404 ($36,000 + $23,800).

c.

Dec. 31

Goods in Process Inventory ................................

119,600

Factory Overhead .....................................................

119,600

To allocate overhead to Jobs 402 and 404

at 200% of direct labor cost assigned.

d.

Dec. 31

Factory Overhead ...........................................................

5,600

Raw Materials Inventory ................................

5,600

To add cost of indirect materials

to actual factory overhead.

e.

Dec. 31

Factory Overhead ...........................................................

8,200

Factory Payroll .........................................................

8,200

To add cost of indirect labor to

actual factory overhead.

Part 2

Revised Factory Overhead account

Ending balance from trial balance .............................................

$115,000

debit

Applied to Jobs 402 and 404 ......................................................

(119,600)

credit

Additional indirect materials ......................................................

5,600

debit

Additional indirect labor .............................................................

8,200

debit

Underapplied overhead ..............................................................

$ 9,200

debit

Dec. 31

Cost of Goods Sold ........................................................

9,200

Factory Overhead .....................................................

9,200

To close underapplied overhead.

1098 Fundamental Accounting Principles, 21st Edition

Problem 19-2A (continued)

Part 3

FARINA BAY COMPANY

Trial Balance

December 31, 2013

Debit

Credit

Cash ...................................................................................

$102,000

Accounts receivable ..........................................................

75,000

Raw materials inventory * .................................................

45,600

Goods in process inventory ** .........................................

208,200

Finished goods inventory ................................................

15,000

Prepaid rent .......................................................................

3,000

Accounts payable .............................................................

$ 17,000

Notes payable ....................................................................

25,000

Common stock ................................................................

50,000

Retained earnings .............................................................

271,000

Sales ...................................................................................

373,000

Cost of goods sold ($218,000 + $9,200) ................................

227,200

Factory payroll ................................................................

0

Factory overhead ...............................................................

0

Operating expenses...........................................................

60,000

_______

Totals ..................................................................................

$736,000

$736,000

* Raw materials inventory

Balance per trial balance ................................................................

$80,000

Less: Amounts recorded for Jobs 402 and 404 ...............................

(28,800)

Less: Indirect materials ................................................................

(5,600)

Ending balance ...................................................................................

$45,600

** Goods in process inventory

Job 402

Job 404

Total

Direct materials .................

$ 10,200

$18,600

$ 28,800

Direct labor ........................

36,000

23,800

59,800

Overhead ...........................

72,000

47,600

119,600

Total cost ...........................

$118,200

$90,000

$208,200

Problem 19-2A (continued)

Part 4

FARINA BAY COMPANY

Income Statement

For Year Ended December 31, 2013

Sales ................................................................................................

$373,000

Cost of goods sold .........................................................................

(227,200)

Gross profit .....................................................................................

145,800

Operating expenses .......................................................................

(60,000)

Net income ......................................................................................

$ 85,800

FARINA BAY COMPANY

Balance Sheet

December 31, 2013

Assets

Cash ......................................................................................

$102,000

Accounts receivable ............................................................

75,000

Inventories

Raw materials inventory .....................................................

$ 45,600

Goods in process inventory...............................................

208,200

Finished goods inventory ..................................................

15,000

268,800

Prepaid rent ................................................................

3,000

Total assets ................................................................

$448,800

Liabilities and equity

Accounts payable ................................................................

$ 17,000

Notes payable ................................................................

25,000

Total liabilities ................................................................

42,000

Common stock ................................................................

50,000

Retained earnings ($271,000 + $85,800) ...............................

356,800

Total stockholders' equity ...................................................

406,800

Total liabilities and equity ...................................................

$448,800

1100 Fundamental Accounting Principles, 21st Edition

Problem 19-2A (concluded)

Part 5

This $5,600 error would cause the costs for Job 404 to be understated.

Since Job 404 is in process at the end of the period, goods in process

inventory and total assets would both be understated on the balance sheet.

Problem 19-3A (70 minutes)

Part 1

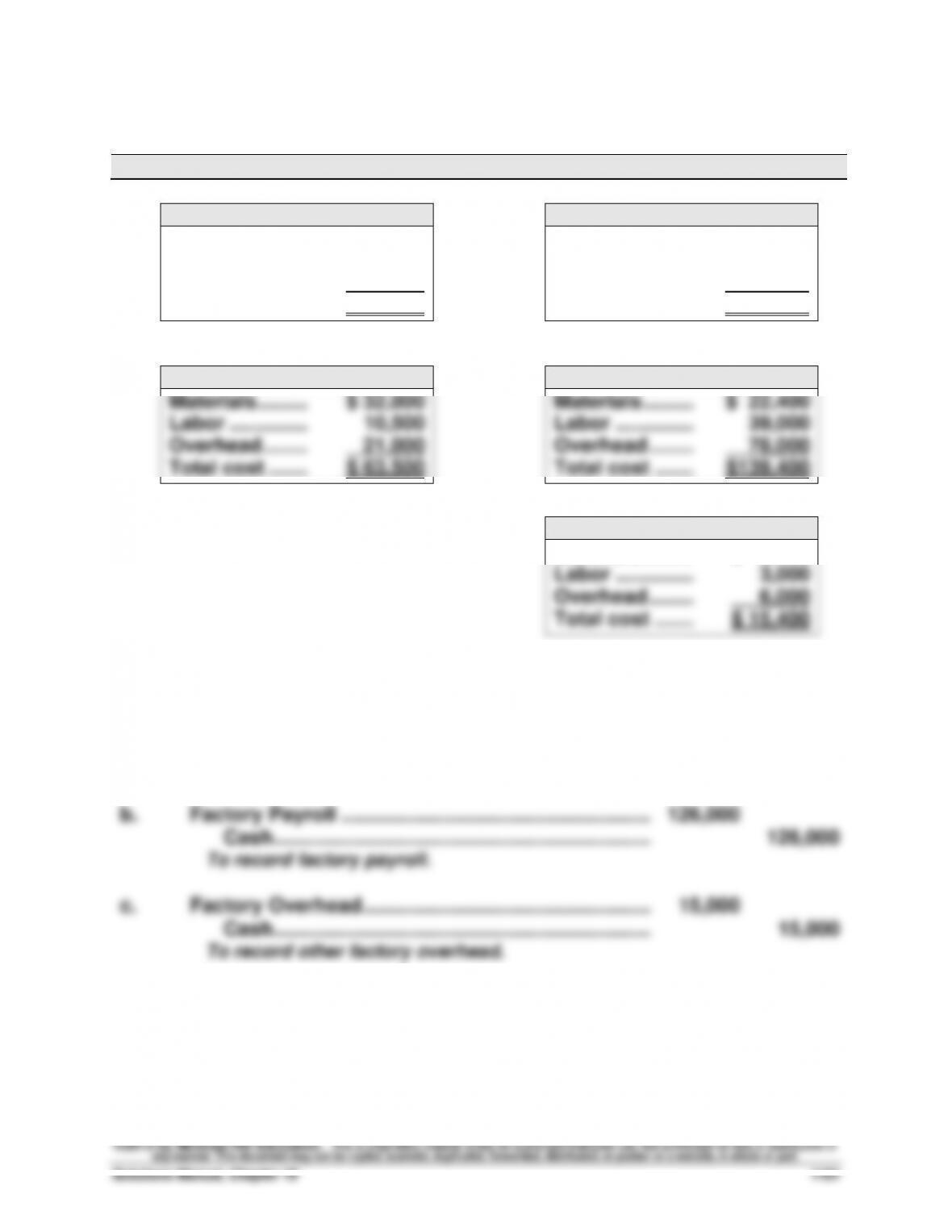

JOB COST SHEETS

Job No. 136

Job No. 138

Materials ..............

$ 48,000

Materials ..............

$ 19,200

Labor ...................

12,000

Labor ...................

37,500

Overhead .............

24,000

Overhead .............

75,000

Total cost ............

$ 84,000

Total cost ............

$131,700

Job No. 137

Job No. 139

Materials ..............

$ 32,000

Materials ..............

$ 22,400

Labor ...................

10,500

Labor ...................

39,000

Overhead .............

21,000

Overhead .............

78,000

Total cost ............

$ 63,500

Total cost ............

$139,400

Job No. 140

Materials ..............

$ 6,400

Labor ...................

3,000

Overhead .............

6,000

Total cost ............

$ 15,400

Part 2

a.

Raw Materials Inventory ................................................

200,000

Accounts Payable ....................................................

200,000

To record materials purchases.

b.

Factory Payroll ...............................................................

126,000

Cash ...........................................................................

126,000

To record factory payroll.

c.

Factory Overhead ...........................................................

15,000

Cash ...........................................................................

15,000

To record other factory overhead.

d.

Goods in Process Inventory ..........................................

128,000

Factory Overhead ...........................................................

19,500

Raw Materials Inventory ..........................................

147,500

To record direct & indirect materials.

1102 Fundamental Accounting Principles, 21st Edition

Problem 19-3A (Continued)

[continued from prior page]

e.

Goods in Process Inventory ..........................................

102,000

Factory Overhead ...........................................................

24,000

Factory Payroll .........................................................

126,000

To record direct & indirect labor.

f.

Goods in Process Inventory ..........................................

177,000

Factory Overhead .....................................................

177,000

To apply overhead to jobs

[($12,000 + $37,500 + $39,000) x 200%].

g.

Finished Goods Inventory .............................................

355,100

Goods in Process Inventory ................................

355,100

To record completion of jobs

($84,000 + $131,700 + $139,400).

h.

Accounts Receivable .....................................................

525,000

Sales ..........................................................................

525,000

To record sales on account.

Cost of Goods Sold ........................................................

215,700

Finished Goods Inventory ................................

215,700

To record cost of sales ($84,000 + $131,700).

i.

Factory Overhead ...........................................................

149,500

Accum. Depreciation—Factory Building ...............

68,000

Accum. Depreciation—Factory Equipment ...........

36,500

Prepaid Insurance ....................................................

10,000

Property Taxes Payable ...........................................

35,000

To record other factory overhead.

j.

Goods in Process Inventory ..........................................

27,000

Factory Overhead .....................................................

27,000

To apply overhead to jobs

[($10,500 + $3,000) x 200%].

Problem 19-3A (Continued)

Part 3

GENERAL LEDGER ACCOUNTS

Raw Materials Inventory

Factory Payroll

(a)

200,000

(d)

147,500

(b)

126,000

(e)

126,000

Bal.

52,500

Bal.

0

Goods in Process Inventory

Factory Overhead

(d)

128,000

(g)

355,100

(c)

15,000

(f)

177,000

(e)

102,000

(d)

19,500

(j)

27,000

(f)

177,000

(e)

24,000

(j)

27,000

(i)

149,500

Bal.

78,900

Bal.

4,000

Finished Goods Inventory

Cost of Goods Sold

(g)

355,100

(h)

215,700

(h)

215,700

Bal.

139,400

Bal.

215,700

Part 4

Reports of Job Costs*

Goods in Process Inventory

Job 137 ........................................

$ 63,500

Job 140 ........................................

15,400

Balance ........................................

$ 78,900

Finished Goods Inventory

Job 139 ........................................

$139,400

Balance ........................................

$139,400

Cost of Goods Sold

Job 136 ........................................

$ 84,000

Job 138 ........................................

131,700

Balance ........................................

$215,700

*Individual totals reconcile with account balances in part 3.

1104 Fundamental Accounting Principles, 21st Edition

Problem 19-4A (35 minutes)

Part 1

a. Predetermined overhead rate

b. Overhead costs charged to jobs

Direct

Applied

Job No.

Labor

Overhead (60%)

201 .........................................................................

$ 604,000

$ 362,400

202 .........................................................................

563,000

337,800

203 .........................................................................

298,000

178,800

204 .........................................................................

716,000

429,600

205 .........................................................................

314,000

188,400

206 .........................................................................

17,000

10,200

Total ................................................................

$2,512,000

$1,507,200

c. Overapplied or underapplied overhead determination

Actual overhead cost...........................................

$1,520,000

Less applied overhead cost ................................

1,507,200

Underapplied overhead ................................

$ 12,800

Part 2

Dec. 31

Cost of Goods Sold ........................................................

12,800

Factory Overhead ......................................................

12,800

To assign underapplied overhead.

Problem 19-5A (80 minutes)

JOB COST SHEET

Customer's Name

Worldwide Company

Job No.

102

Direct Materials

Direct Labor

Overhead Costs Applied

Date

Requisition

Number

Amount

Time

Ticket

Number

Amount

Date

Rate

Amount

#35

33,750

#1-10

90,000

May ---

80%

72,000

#36

12,960

SUMMARY OF COSTS

Dir. Materials ................................

46,710

Dir. Labor................................

90,000

Overhead ................................

72,000

Total cost of Job ................................

208,710

Total

46,710

Total

90,000

FI N I S H E D

JOB COST SHEET

Customer's Name

Reuben Company

Job No.

103

Direct Materials

Direct Labor

Overhead Costs Applied

Date

Requisition

Number

Amount

Time

Ticket

Number

Amount

Date

Rate

Amount

#37

17,500

#11-30

65,000

May ---

80%

52,000

#38

6,840

SUMMARY OF COSTS

Dir. Materials ................................

Dir. Labor................................

Overhead ................................

______

Total cost of Job ................................

.

Total

Total

1106 Fundamental Accounting Principles, 21st Edition

Problem 19-5A (Continued)

MATERIALS LEDGER CARD

Item

Material M

Received

Issued

Balance

Date

Receiving

Report

Units

Unit

Price

Total

Price

Requi-

sition

Units

Unit

Price

Total

Price

Units

Unit

Price

Total

Price

May 1

200

250

50,000

#426

250

250

62,500

450

250

112,500

#35

135

250

33,750

315

250

78,750

#37

70

250

17,500

245

250

61,250

MATERIALS LEDGER CARD

Item

Material R

Received

Issued

Balance

Date

Receiving

Report

Units

Unit

Price

Total

Price

Requi-

sition

Units

Unit

Price

Total

Price

Units

Unit

Price

Total

Price

May 1

95

180

17,100

#427

90

180

16,200

185

180

33,300

#36

72

180

12,960

113

180

20,340

#38

38

180

6,840

75

180

13,500

MATERIALS LEDGER CARD

Item

Paint

Received

Issued

Balance

Date

Receiving

Report

Units

Unit

Price

Total

Price

Requi-

sition

Units

Unit

Price

Total

Price

Units

Unit

Price

Total

Price

May 1

55

75

4,125

#39

15

75

1,125

40

75

3,000