PROBLEM SET A

Problem 12-1A (50 minutes)

1.

Dec. 31

Income Summary …………………………………………..…

249,000

Kara Ries, Capital …………………………………….…

83,000

Tammy Bax, Capital ……………………………………

83,000

Joe Thomas, Capital ……………………………………

83,000

To close Income Summary.

2.

Dec. 31

Income Summary …………………………………………..…

249,000

Kara Ries, Capital …………………………………….…

62,250

Tammy Bax, Capital ……………………………………

87,150

Joe Thomas, Capital ……………………………………

99,600

To close Income Summary*.

*Supporting computations

($80,000/$320,000) x $249,000 = $62,250

($112,000/$320,000) x $249,000 = $87,150

($128,000/$320,000) x $249,000 = $99,600

3.

Dec. 31

Income Summary …………………………………………..…

249,000

Kara Ries, Capital …………………………………….…

79,000

Tammy Bax, Capital ……………………………………

72,200

Joe Thomas, Capital ……………………………………

97,800

To close Income Summary*.

*Supporting calculations

Ries

Bax

Thomas

Total

Net income ……………………………….………..

$249,000

Salary allowances

Ries ……………………………………….………..

$66,000

Bax………………………………………..………..

$56,000

Thomas …………………………………………..

$80,000

Total salaries ……………………………………..

202,000

Balance after salary allowances …………..

47,000

Interest allowances

Ries (10% on $80,000) …………….………..

8,000

Bax (10% on $112,000) ……………………..

11,200

Thomas (10% on $128,000) ……..………..

12,800

Total interest …………………………….………..

32,000

Bal. after interest and salaries ……………..

15,000

Balance allocated equally ………….………..

5,000

5,000

5,000

Total allocated equally ………………………..

15,000

Balance of income …………………….…….

______

______

______

$ 0

Shares of the partners……………….………..

$79,000

$72,200

$97,800

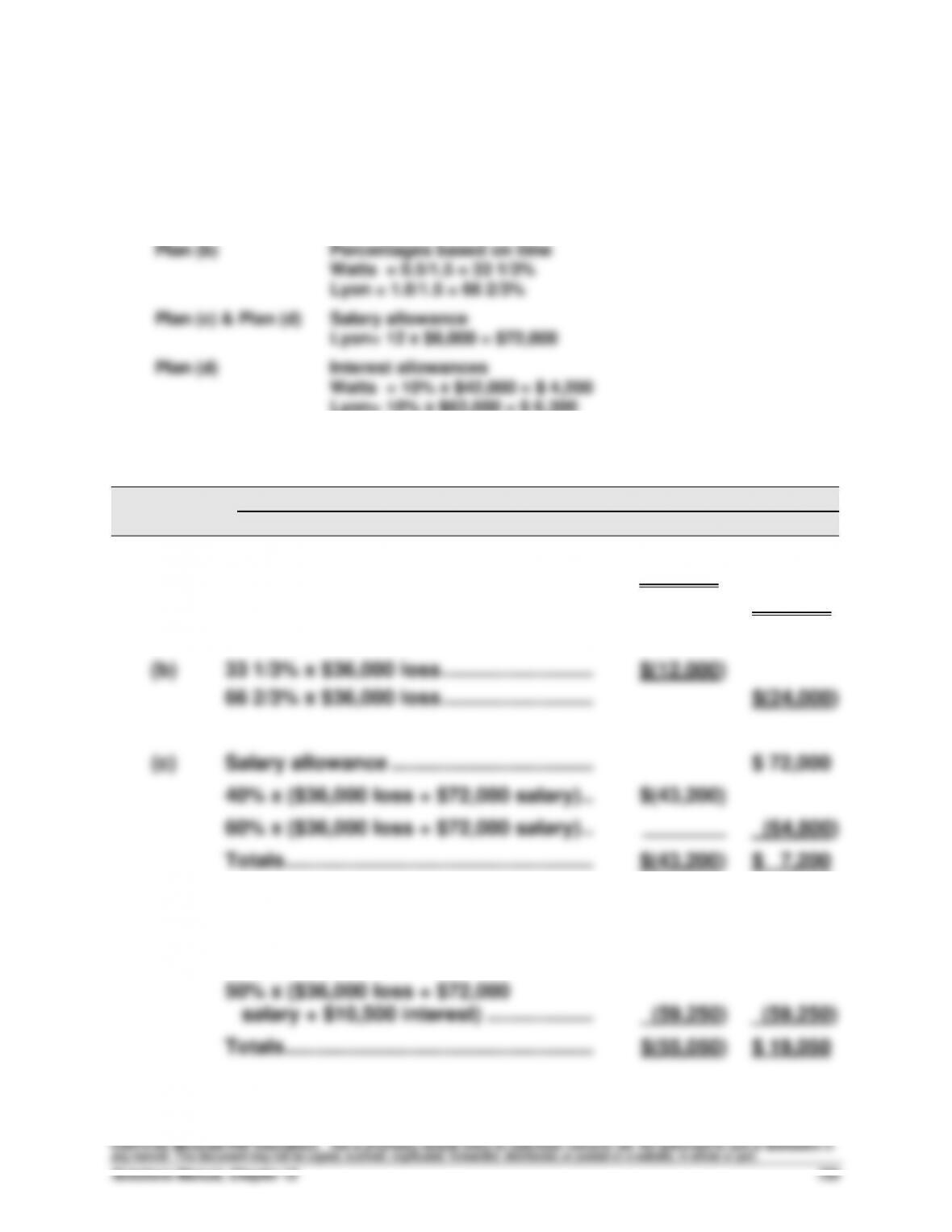

Problem 12-2A (45 minutes)

Preliminary calculations

Plan (a) & Plan (c)

Percentages based on initial investments

Watts = $42,000/$105,000 = 40%

Lyon = $63,000/$105,000 = 60%

Plan (b)

Percentages based on time

Watts = 0.5/1.5 = 33 1/3%

Lyon = 1.0/1.5 = 66 2/3%

Plan (c) & Plan (d)

Salary allowance

Lyon= 12 x $6,000 = $72,000

Plan (d)

Interest allowances

Watts = 10% x $42,000 = $ 4,200

Lyon= 10% x $63,000 = $ 6,300

Income (Loss)

Year 1

Sharing Plan

Calculations

Watts

Lyon

(a)

40% x $36,000 loss …………………………….……………..

$(14,400)

60% x $36,000 loss …………………………….……………..

$(21,600)

(b)

33 1/3% x $36,000 loss ……………………….….

$(12,000)

66 2/3% x $36,000 loss ……………………….….

$(24,000)

(c)

Salary allowance ……………………………….……………..

$ 72,000

40% x ($36,000 loss + $72,000 salary) ………………..

$(43,200)

60% x ($36,000 loss + $72,000 salary) ………………..

________

(64,800)

Totals ………………………………………………..……..

$(43,200)

$ 7,200

(d)

Salary allowance ……………………………….……………..

$ 72,000

Interest allowances …………………………………………..

$ 4,200

6,300

50% x ($36,000 loss + $72,000

salary + $10,500 interest) ………………..…………

(59,250)

(59,250)

Totals ………………………………………………..……..

$(55,050)

$ 19,050

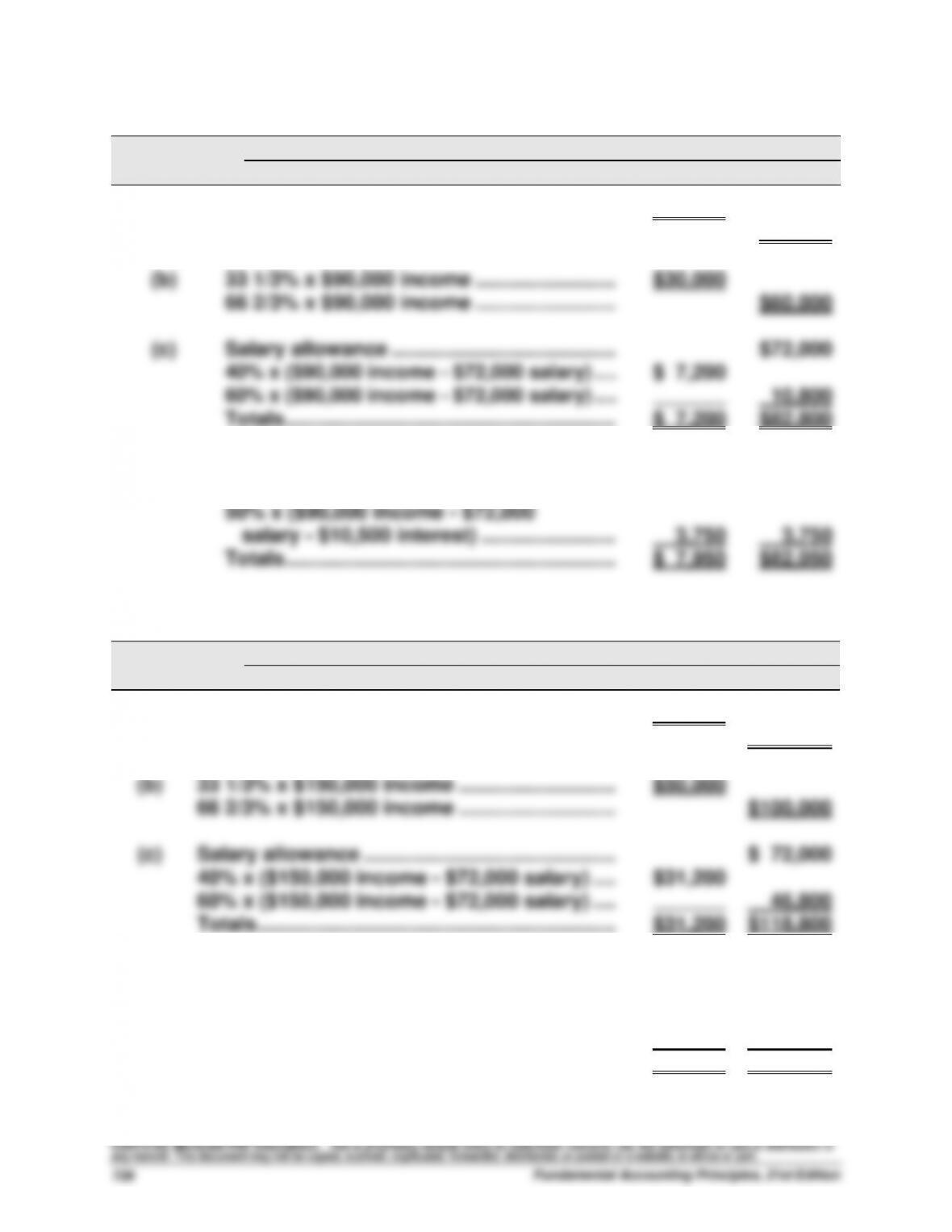

Problem 12-2A (Concluded)

Income (Loss)

Year 2

Sharing Plan

Calculations

Watts

Lyon

(a)

40% x $90,000 income …………………………..

$36,000

60% x $90,000 income …………………………..

$54,000

(b)

33 1/3% x $90,000 income …………………….…….

$30,000

66 2/3% x $90,000 income …………………….…….

$60,000

(c)

Salary allowance ………………………………….…………..

$72,000

40% x ($90,000 income – $72,000 salary) ….…………..

$ 7,200

60% x ($90,000 income – $72,000 salary) ….…………..

_______

10,800

Totals …………………………………………………..…..

$ 7,200

$82,800

(d)

Salary allowance ………………………………….…………..

$72,000

Interest allowances …………………………………………..

$ 4,200

6,300

50% x ($90,000 income – $72,000

salary – $10,500 interest) …………………………..

3,750

3,750

Totals …………………………………………………..…..

$ 7,950

$82,050

Income (Loss)

Year 3

Sharing Plan

Calculations

Watts

Lyon

(a)

40% x $150,000 income …………………………….………

$60,000

60% x $150,000 income …………………………….………

$ 90,000

(b)

33 1/3% x $150,000 income ……………………….….

$50,000

66 2/3% x $150,000 income ……………………….….

$100,000

(c)

Salary allowance ………………………………………………

$ 72,000

40% x ($150,000 income – $72,000 salary) ….………

$31,200

60% x ($150,000 income – $72,000 salary) ….………

_______

46,800

Totals ……………………………………………………….

$31,200

$118,800

(d)

Salary allowance ………………………………………………

$ 72,000

Interest allowances …………………………………..………

$ 4,200

6,300

50% x ($150,000 income – $72,000

salary – $10,500 interest) ………………………..…

33,750

33,750

Totals ……………………………………………………….

$37,950

$112,050

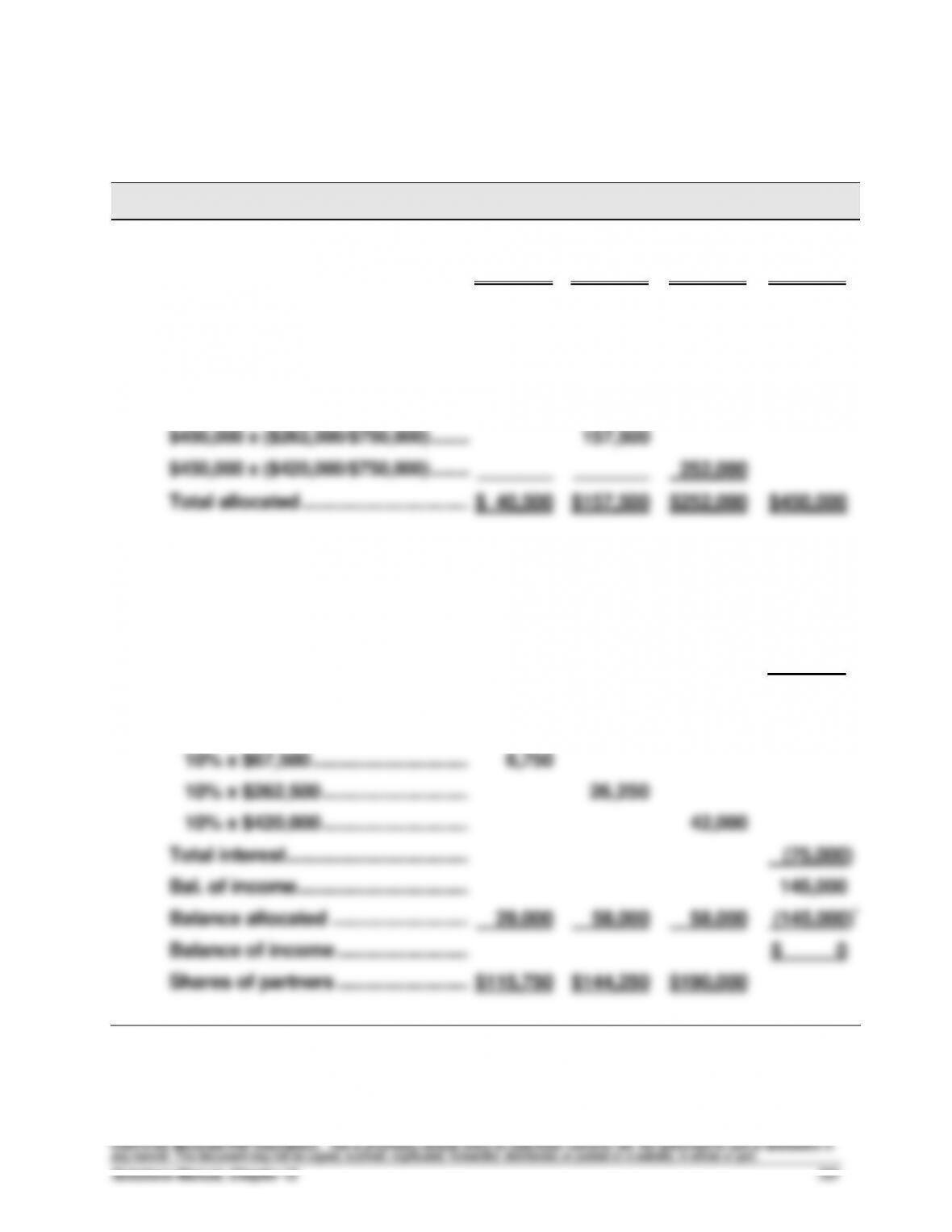

Problem 12-3A (40 minutes)

Part 1

Income (Loss)

Sharing Plan

Calculations

Bill

Bruce

Barb

Total

(a)

$450,000/3 ………………………………….……………………

$150,000

$150,000

$150,000

$450,000

(b)

$450,000 x ($67,500/$750,000) ……….………………….

40,500

$450,000 x ($262,500/$750,000) ……..……………………

157,500

$450,000 x ($420,000/$750,000) ……..……………………

_______

_______

252,000

Total allocated ……………………………………………………….

$ 40,500

$157,500

$252,000

$450,000

(c)

Net income ……………………………………………………….

$450,000

Salary allowances …………………………..

$ 80,000

$ 60,000

$ 90,000

(230,000)

Balance of income ……………………..……

220,000

Interest allowances

10% x $67,500 …………………………..

6,750

10% x $262,500 ………………………..…

26,250

10% x $420,000 ………………………..…

42,000

Total interest ……………………………………………………….

(75,000)

Bal. of income …………………………….…………………………

145,000

Balance allocated …………………………..

29,000

58,000

58,000

(145,000)*

Balance of income ……………………..……

$ 0

Shares of partners ……………………..……

$115,750

$144,250

$190,000

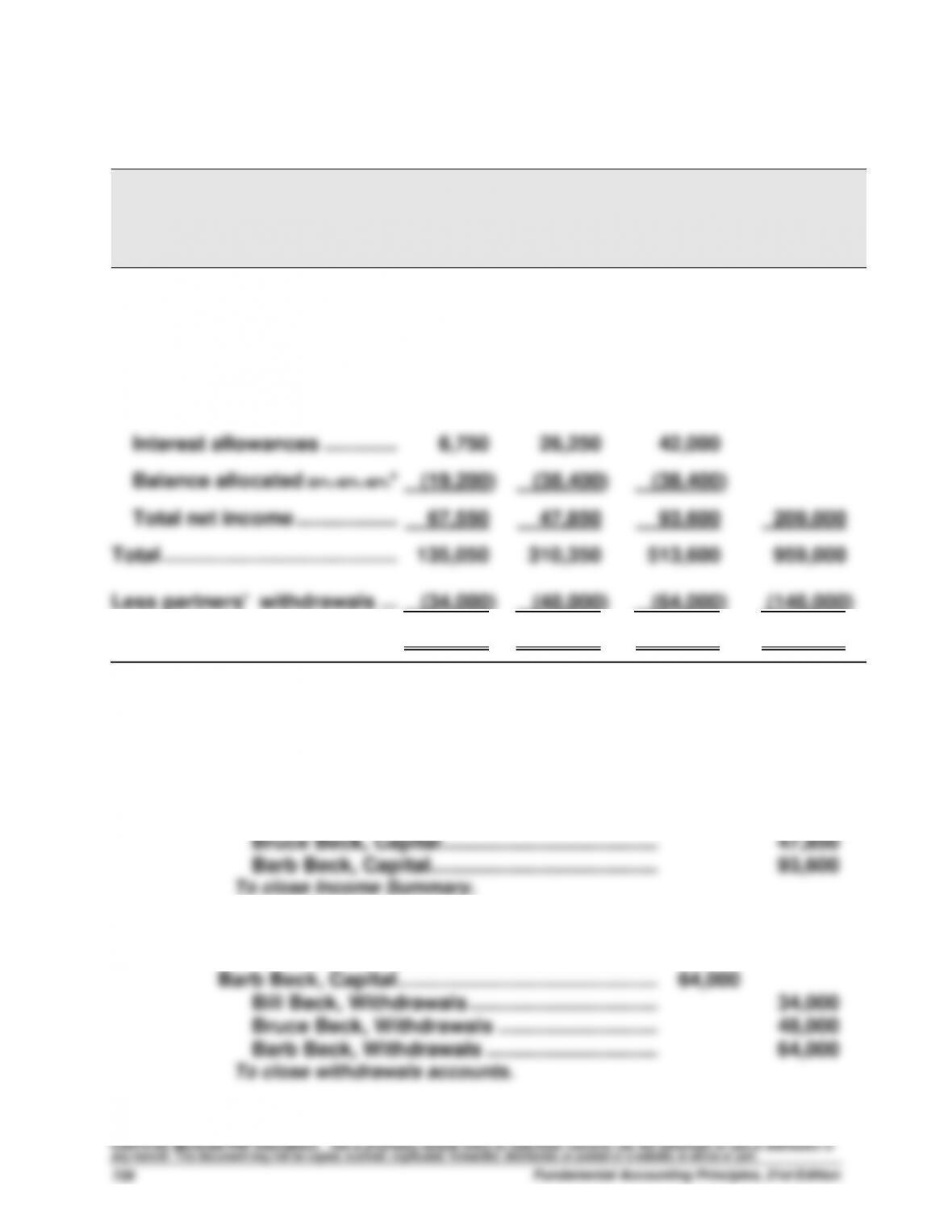

Problem 12-3A (Concluded)

Part 2

BBB PARTNERSHIP

Statement of Partners’ Equity

For Year Ended December 31

Bill

Bruce

Barb

Total

Beginning capital balances …..………

$ 0

$ 0

$ 0

$ 0

Plus

Investments by owners ………………

67,500

262,500

420,000

750,000

Net income

Salary allowances ……………..………

80,000

60,000

90,000

Interest allowances …………..………

6,750

26,250

42,000

Balance allocated 20%:40%:40%*

(19,200)

(38,400)

(38,400)

Total net income ……………….………

67,550

47,850

93,600

209,000

Total …………………………..………..………

135,050

310,350

513,600

959,000

Less partners’ withdrawals ….………

(34,000)

(48,000)

(64,000)

(146,000)

Ending capital balances ……….………

$101,050

$262,350

$449,600

$813,000

*[$209,000 – ($80,000 + $60,000 + $90,000) – ($6,750 + $26,250 + $42,000)]; then allocated 20%:40%:40%.

Part 3

Dec. 31

Income Summary ……………………………………………..

209,000

Bill Beck, Capital …………………………………….…..

67,550

Bruce Beck, Capital ……………………………………..

47,850

Barb Beck, Capital …………………………………..…..

93,600

To close Income Summary.

Dec. 31

Bill Beck, Capital ………………………………………….…..

34,000

Bruce Beck, Capital …………………………………………..

48,000

Barb Beck, Capital ………………………………………..…..

64,000

Bill Beck, Withdrawals …………………………….…..

34,000

Bruce Beck, Withdrawals ………………………..…

48,000

Barb Beck, Withdrawals …………………………..

64,000

To close withdrawals accounts.

Problem 12-4A (50 minutes)

Part 1

a)

Feb. 1

Benson, Capital ………………………………………………..

138,000

North, Capital ……………………………………………..

138,000

To record admission of North.

b)

Feb. 1

Benson, Capital ………………………………………………..

138,000

Schmidt, Capital ………………………………………….

138,000

To record admission of Schmidt.

c)

Feb. 1

Benson, Capital ………………………………………………..

138,000

Cash ……………………………………………………….….

138,000

To record withdrawal of Benson with no bonus.

d)

Feb. 1

Benson, Capital ………………………………………………..

138,000

Meir, Capital* …………………………………………………...

28,500

Lau, Capital** …………………………………………………...

47,500

Cash ……………………………………………………….….

214,000

To record withdrawal of Benson with bonus.

e)

Feb. 1

Benson, Capital ………………………………………………..

138,000

Accumulated Depreciation—Equipment …………...

23,200

Meir, Capital* ……………………………………………...

22,950

Lau, Capital** ……………………………………………...

38,250

Equipment ………………………………………………….

70,000

Cash ……………………………………………………….….

30,000

To record withdrawal of Benson with bonus to

old partners.

* [$138,000 – ($70,000 – $23,200 + $30,000)] x 3/8.

**[$138,000 – ($70,000 – $23,200 + $30,000)] x 5/8.

Problem 12-4A (Concluded)

Part 2

a)

Feb. 1

Cash ………………………………………………………………..

200,000

Rhodes, Capital* ………………………………………...

200,000

To record admission of Rhodes.

*Supporting calculations

$168,000 + $138,000 + $294,000 = $600,000

($600,000 + $200,000) x 25% = $200,000

Thus, no bonus is received or granted.

b)

Feb. 1

Cash ………………………………………………………………..

145,000

Meir, Capital ($41,250* x 3/10) …………………………..

12,375

Benson, Capital ($41,250* x 2/10) ……………………...

8,250

Lau, Capital ($41,250* x 5/10) …………………………..

20,625

Rhodes, Capital …………………………………………..

186,250

To record Rhode’s admission and bonus.

* Supporting calculations

($600,000 + $145,000) x 25% = $186,250

$145,000 – $186,250 = $(41,250)

Thus, the new partner receives a bonus.

c)

Feb. 1

Cash ………………………………………………………………..

262,000

Meir, Capital ($46,500* x 3/10) ……………………...

13,950

Benson, Capital ($46,500* x 2/10) ………………...

9,300

Lau, Capital ($46,500* x 5/10) ……………………....

23,250

Rhodes, Capital …………………………………………..

215,500

To record admission of Rhodes and bonus to old partners.

* Supporting calculations

($600,000 + $262,000) x 25% = $215,500

$262,000 – $215,500 = $46,500

Thus, the old partners receive a bonus.

Problem 12-5A (75 minutes)

Note: All entries in this problem are dated May 31.

1.

(a)

Cash ………………………………………………………………..

600,000

Inventory ……………………………………………..……..

537,200

Gain on Sale of Inventory …………………….…….

62,800

(b)

Gain on Sale of Inventory …………………………..

62,800

Kendra, Capital ($62,800 x 3/6) ……………..……..

31,400

Cogley, Capital ($62,800 x 2/6) ……………..……..

20,933

Mei, Capital ($62,800 x 1/6) …………………..……..

10,467

(c)

Accounts Payable ……………………………………..……..

245,500

Cash ……………………………………………………….

245,500

(d)

Kendra, Capital ($93,000+ $31,400) ……………….………

124,400

Cogley, Capital ($212,500 + $20,933) …………….………

233,433

Mei, Capital ($167,000 + $10,467) ……………….……..

177,467

Cash* …………………………………………………..…..

535,300

* $180,800 + $600,000 – $245,500

2.

(a)

Cash ………………………………………………………………..

500,000

Loss on Sale of Inventory …………………………..

37,200

Inventory ……………………………………………..……..

537,200

(b)

Kendra, Capital ($37,200 x 3/6) …………………..……..

18,600

Cogley, Capital ($37,200 x 2/6) …………………..……..

12,400

Mei, Capital ($37,200 x 1/6) ………………………..…

6,200

Loss on Sale of Inventory …………………….…….

37,200

(c)

Accounts Payable ……………………………………..……..

245,500

Cash ……………………………………………………….

245,500

(d)

Kendra, Capital ($93,000 – $18,600) …………….……..

74,400

Cogley, Capital ($212,500 – $12,400) …………..……..

200,100

Mei, Capital ($167,000 – $6,200) ………………….……..

160,800

Cash* …………………………………………………..…..

435,300

* $180,800 + $500,000 – $245,500

Problem 12-5A (Concluded)

3.

(a)

Cash ………………………………………………………………..

320,000

Loss on Sale of Inventory ………………………………...

217,200

Inventory …………………………………………………....

537,200

(b)

Kendra, Capital ($217,200 x 3/6) ………………………..

108,600

Cogley, Capital ($217,200 x 2/6) ………………………..

72,400

Mei, Capital ($217,200 x 1/6) ……………………………..

36,200

Loss on Sale of Inventory …………………………..

217,200

Cash ………………………………………………………………..

15,600

Kendra, Capital ($93,000 – $108,600) …………....

15,600

(c)

Accounts Payable …………………………………………....

245,500

Cash ……………………………………………………….....

245,500

(d)

Cogley, Capital ($212,500 – $72,400) ………………....

140,100

Mei, Capital ($167,000 – $36,200) ……………………....

130,800

Cash* ………………………………………………………....

270,900

*(180,800 + 320,000+15,600-245,500)

4.

(a)

Cash ………………………………………………………………..

250,000

Loss on Sale of Inventory ………………………………...

287,200

Inventory …………………………………………………....

537,200

(b)

Kendra, Capital ($287,200 x 3/6) ………………………..

143,600

Cogley, Capital ($287,200 x 2/6) ………………………..

95,733

Mei, Capital ($287,200 x 1/6) ……………………………..

47,867

Loss on Sale of Inventory …………………………..

287,200

Cogley, Capital ($50,600 x 2/3) ………………………....

33,733

Mei, Capital ($50,600 x 1/3) ……………………………....

16,867

Kendra, Capital ($93,000 – $143,600) …………….…

50,600

(c)

Accounts Payable …………………………………………....

245,500

Cash ……………………………………………………….....

245,500

(d)

Cogley, Capital*………………………………………………..

83,034

Mei, Capital** …………………………………………………...

102,266

Cash*** ……………………………………………………....

185,300

*$212,500 – $95,733 – $33,733

**$167,000 – $47,867 – $16,867 ***$180,800 + $250,000 – $245,500

PROBLEM SET B

Problem 12-1B (50 minutes)

1.

Dec. 31

Income Summary …………………………………………..…

270,000

Mark Albin, Capital …………………………………..…

90,000

Roland Peters, Capital ……………………………..…

90,000

Sam Ramsey, Capital ……………………………….…

90,000

To close Income Summary.

2.

Dec. 31

Income Summary …………………………………………..…

270,000

Mark Albin, Capital …………………………………..…

135,000

Roland Peters, Capital ……………………………..…

81,000

Sam Ramsey, Capital ……………………………….…

54,000

To close Income Summary.*

*Supporting computations

($164,000/$328,000) x $270,000 = $135,000

($98,400/$328,000) x $270,000 = $81,000

($65,600/$328,000) x $270,000 = $54,000

3.

Dec. 31

Income Summary …………………………………………..…

270,000

Mark Albin, Capital …………………………………..…

118,800

Roland Peters, Capital ……………………………..…

88,240

Sam Ramsey, Capital ……………………………….…

62,960

To close Income Summary.*

*Supporting calculations

Albin

Peters

Ramsey

Total

Net income …………………………………………

$270,000

Salary allowances

Albin ……………………………………….………

$ 96,000

Peters ……………………………………..………

$72,000

Ramsey …………………………………..………

$50,000

Total salaries ……………………………..………

218,000

Balance after salary allowances …..………

52,000

Interest allowances

Albin (10% on $164,000) ……………………

16,400

Peters (10% on $98,400) ……………………

9,840

Ramsey (10% on $65,600) …………………

6,560

Total interest ………………………………………

32,800

Bal. after interest and salaries ……..………

19,200

Balance allocated equally ……………………

6,400

6,400

6,400

Total allocated equally ………………..………

19,200

Balance of income …………………………..

_______

______

______

$ 0

Shares of the partners…………………………

$118,800

$88,240

$62,960

Problem 12-2B (45 minutes)

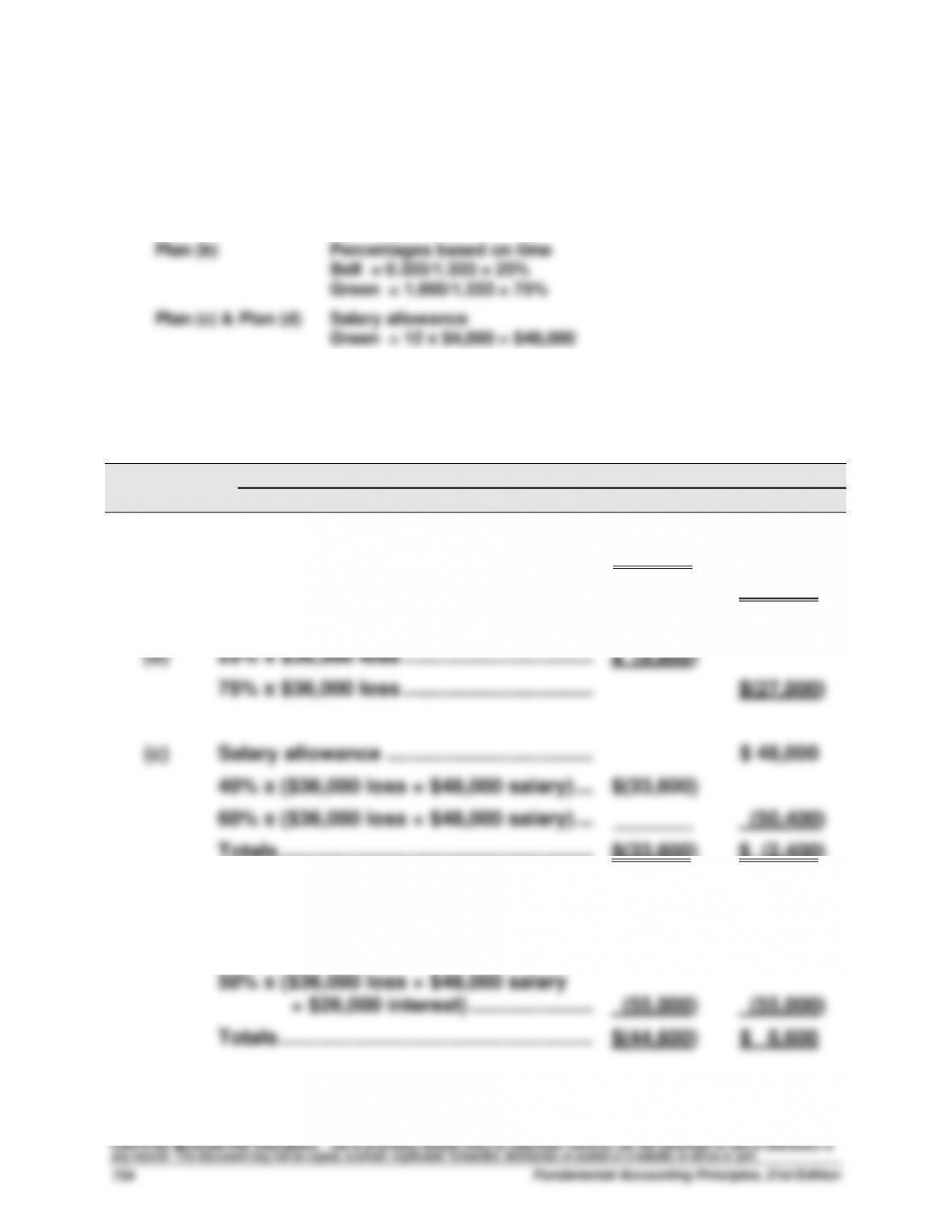

Preliminary calculations

Plan (a) & Plan (c)

Percentages based on initial investments

Bell = $104,000/$260,000 = 40%

Green = $156,000/$260,000 = 60%

Plan (b)

Percentages based on time

Bell = 0.333/1.333 = 25%

Green = 1.000/1.333 = 75%

Plan (c) & Plan (d)

Salary allowance

Green = 12 x $4,000 = $48,000

Plan (d)

Interest allowances

Bell = 10% x $104,000 = $10,400

Green = 10% x $156,000 = $15,600

Income (Loss)

Year 1

Sharing Plan

Calculations

Bell

Green

(a)

40% x $36,000 loss ……………………………..…………….

$(14,400)

60% x $36,000 loss ……………………………..…………….

$(21,600)

(b)

25% x $36,000 loss ……………………………..…………….

$ (9,000)

75% x $36,000 loss ……………………………..…………….

$(27,000)

(c)

Salary allowance ………………………………..…………….

$ 48,000

40% x ($36,000 loss + $48,000 salary) ….…………….

$(33,600)

60% x ($36,000 loss + $48,000 salary) ….…………….

_______

(50,400)

Totals …………………………..…………………….…….

$(33,600)

$ (2,400)

(d)

Salary allowance ………………………………..…………….

$ 48,000

Interest allowances …………………………….…………….

$ 10,400

15,600

50% x ($36,000 loss + $48,000 salary

+ $26,000 interest) …………………..………

(55,000)

(55,000)

Totals …………………………..…………………….…….

$(44,600)

$ 8,600

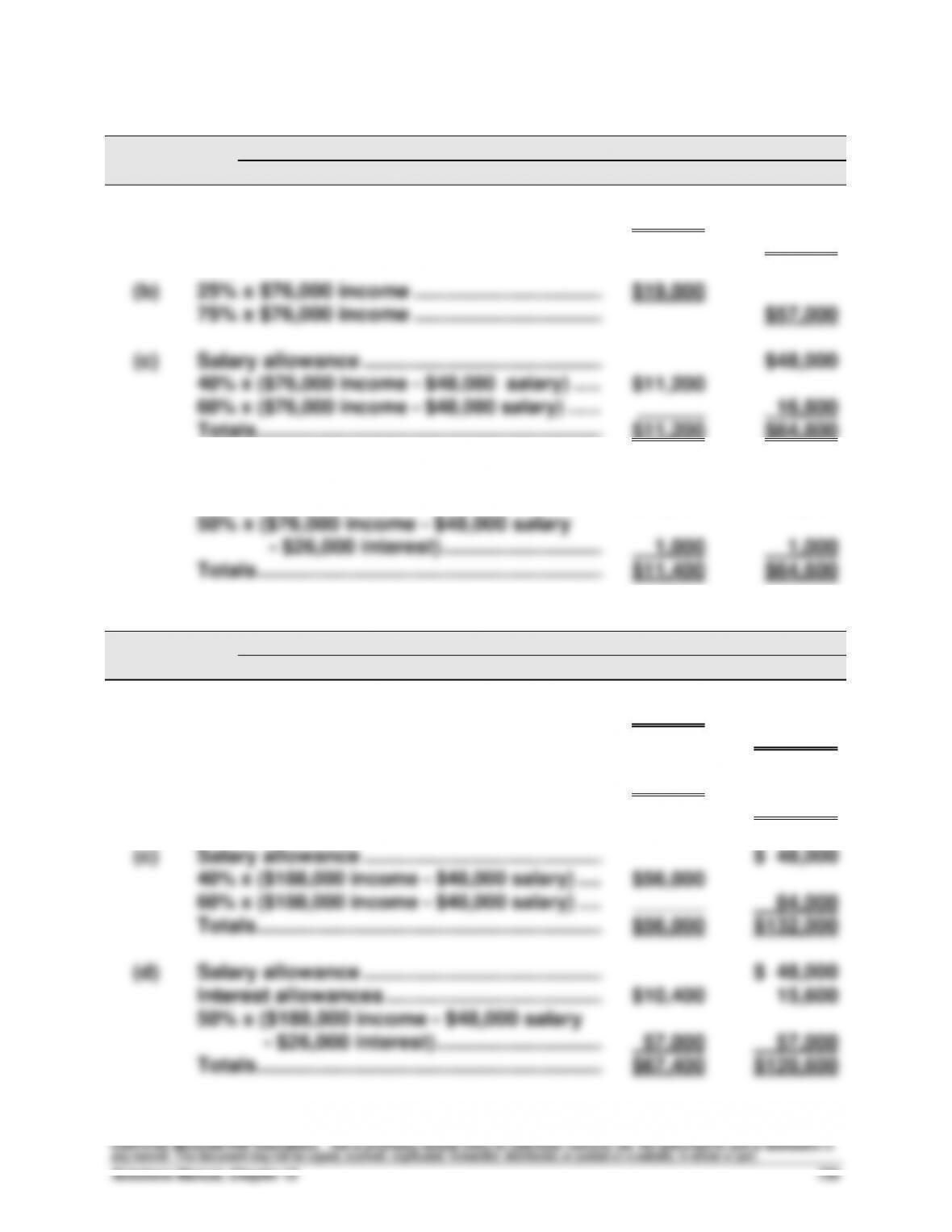

Problem 12-2B (Concluded)

Income (Loss)

Year 2

Sharing Plan

Calculations

Bell

Green

(a)

40% x $76,000 income …………………………….………..

$30,400

60% x $76,000 income …………………………….………..

$45,600

(b)

25% x $76,000 income …………………………….………..

$19,000

75% x $76,000 income …………………………….………..

$57,000

(c)

Salary allowance …………………………………….………..

$48,000

40% x ($76,000 income – $48,000 salary) ……………..

$11,200

60% x ($76,000 income – $48,000 salary) …….………..

______

16,800

Totals ……………………………………………………....

$11,200

$64,800

(d)

Salary allowance …………………………………….………..

$48,000

Interest allowances …………………………………………..

$10,400

15,600

50% x ($76,000 income – $48,000 salary

– $26,000 interest) ………………………..…

1,000

1,000

Totals ……………………………………………………....

$11,400

$64,600

Income (Loss)

Year 3

Sharing Plan

Calculations

Bell

Green

(a)

40% x $188,000 income …………………………..

$75,200

60% x $188,000 income …………………………..

$112,800

(b)

25% x $188,000 income …………………………..

$47,000

75% x $188,000 income …………………………..

$141,000

(c)

Salary allowance …………………………………….………..

$ 48,000

40% x ($188,000 income – $48,000 salary) …..………..

$56,000

60% x ($188,000 income – $48,000 salary) …..………..

_______

84,000

Totals ……………………………………………………....

$56,000

$132,000

(d)

Salary allowance …………………………………….………..

$ 48,000

Interest allowances …………………………………………..

$10,400

15,600

50% x ($188,000 income – $48,000 salary

– $26,000 interest) …………………………..

57,000

57,000

Totals ……………………………………………………....

$67,400

$120,600

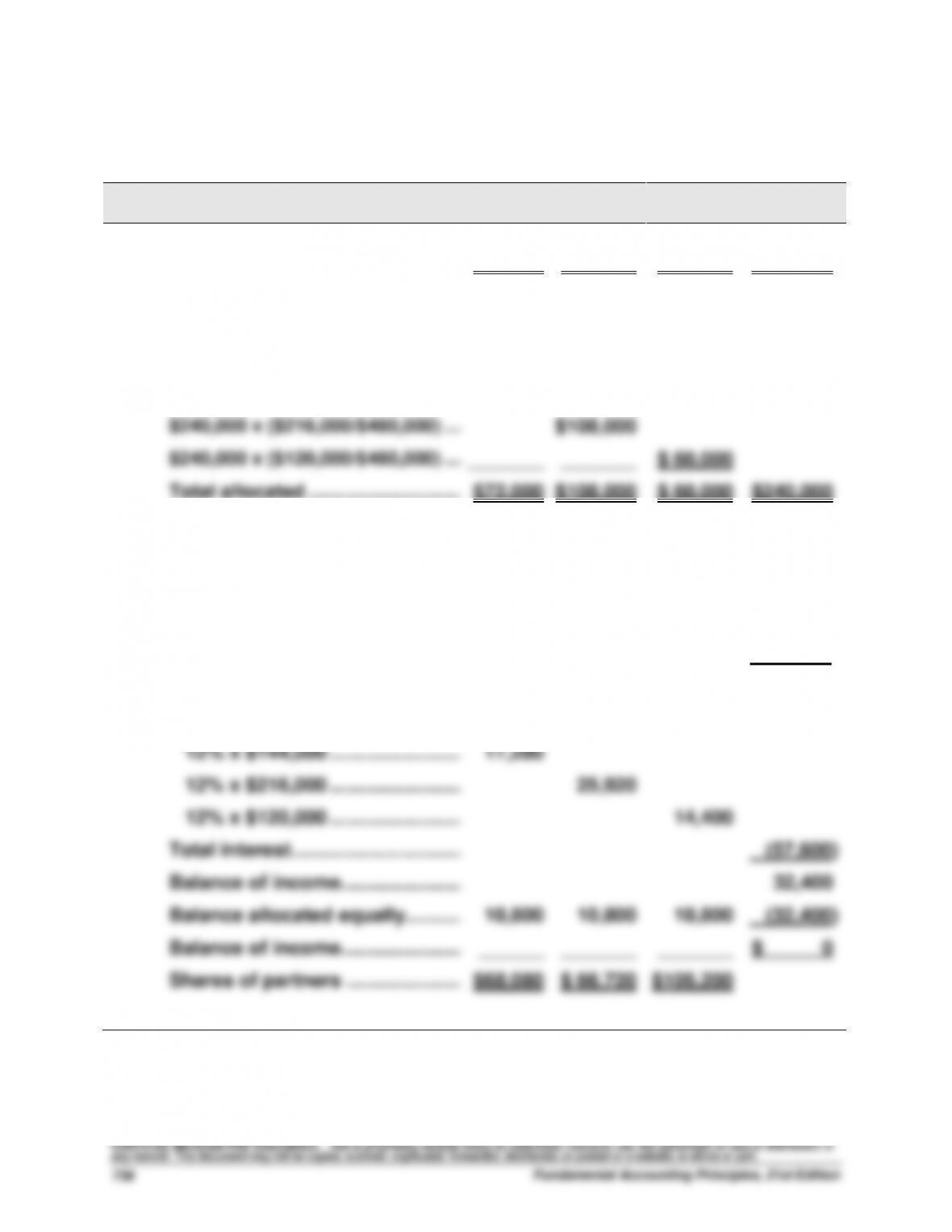

Problem 12-3B (30 minutes)

Part 1

Income (Loss)

Sharing Plan

Calculations

Cook

Xi

Schwartz

Total

(a)

$240,000/3 ……………………………………………

$80,000

$ 80,000

$ 80,000

$240,000

(b)

$240,000 x ($144,000/$480,000) ….…………….

$72,000

$240,000 x ($216,000/$480,000) ….…………….

$108,000

$240,000 x ($120,000/$480,000) ….…………….

_______

_______

$ 60,000

Total allocated ………………………..…

$72,000

$108,000

$ 60,000

$240,000

(c)

Net income ……………………………..……………

$240,000

Salary allowances …………………..………

$40,000

$ 30,000

$ 80,000

(150,000)

Balance of income…………………..………

90,000

Interest allowances

12% x $144,000 …………………….…….

17,280

12% x $216,000 …………………….…….

25,920

12% x $120,000 …………………….…….

14,400

Total interest …………………………..

(57,600)

Balance of income…………………..………

32,400

Balance allocated equally………..……………

10,800

10,800

10,800

(32,400)

Balance of income…………………..………

______

_______

_______

$ 0

Shares of partners ………………….……….

$68,080

$ 66,720

$105,200

Problem 12-3B (Concluded)

Part 2

CXS PARTNERSHIP

Statement of Partners’ Equity

For Year Ended December 31

Cook

Xi

Schwartz

Total

Beginning capital balances ..……………

$ 0

$ 0

$ 0

$ 0

Plus

Investments by owners ……..……………

144,000

216,000

120,000

480,000

Net income

Salary allowances ……………..……………

40,000

30,000

80,000

Interest allowances …………………………

17,280

25,920

14,400

Balance allocated equally* ………………

(40,000)

(40,000)

(40,000)

Total net income ……………….………….

17,280

15,920

54,400

87,600

Total ………………………………………………

161,280

231,920

174,400

567,600

Less partner withdrawals …..……………

(18,000)

(38,000)

(24,000)

(80,000)

Ending capital balance ……………………

$143,280

$193,920

$150,400

$487,600

* [$87,600 – ($40,000 + $30,000 + $80,000) – ($17,280 + $25,920 + $14,400)] /3

Part 3

Dec. 31

Income Summary ………………………………………….….

87,600

Cook, Capital …………………………………………..….

17,280

Xi, Capital ……………………………………………….….

15,920

Schwartz, Capital …………………………………….….

54,400

To close Income Summary.

Dec. 31

Cook, Capital ………………………………………………..….

18,000

Xi, Capital …………………………………………………….…

38,000

Schwartz, Capital ………………………………………….….

24,000

Cook, Withdrawals ………………………………….….

18,000

Xi, Withdrawals ……………………………………….….

38,000

Schwartz, Withdrawals …………………………….….

24,000

To close withdrawals accounts.