Part 7

aDVENTURE TRAVEL

Post-Closing Trial Balance

30-Apr-13

Debit Credit

Cash $27,000

Accounts receivable 1,750

Ledger as of April 30

Cash Acct. No. 101

Date Explanation PR Debit Credit Balance

1 30000 30000

2 1800 28200

3 1000 27200

Accounts Receivable Acct. No. 106

Date Explanation PR Debit Credit Balance

Office Supplies Acct. No. 124

Date Explanation PR Debit Credit Balance

Prepaid Insurance Acct. No. 128

Date Explanation PR Debit Credit Balance

Computer Equipment Acct. No. 167

Date Explanation PR Debit Credit Balance

Accumulated Depreciation–Computer Equipment Acct. No. 168

Date Explanation PR Debit Credit Balance

Salaries Payable Acct. No. 209

Date Explanation PR Debit Credit Balance

J. Nozomi, Capital Acct. No. 301

Date Explanation PR Debit Credit Balance

J. Nozomi, Withdrawals Acct. No. 302

Date Explanation PR Debit Credit Balance

Commissions Earned Acct. No. 405

Date Explanation PR Debit Credit Balance

Depreciation Expense–Computer Equipment Acct. No. 612

Date Explanation PR Debit Credit Balance

Salaries Expense Acct. No. 622

Date Explanation PR Debit Credit Balance

14 1600 1600

Insurance Expense Acct. No. 637

Date Explanation PR Debit Credit Balance

Rent Expense Acct. No. 640

Date Explanation PR Debit Credit Balance

O4ce Supplies Expense Acct. No. 650

Date Explanation PR Debit Credit Balance

Repairs Expense Acct. No. 684

Date Explanation PR Debit Credit Balance

Telephone Expense Acct. No. 688

Date Explanation PR Debit Credit Balance

Income Summary Acct. No. 901

Date Explanation PR Debit Credit Balance

Title: Problem 4-3A

QA_Ori:

Part 1

ACE CONSTRUCTION CO.

Work Sheet

For Year Ended June 30, 2013

Unadjusted

Trial Balance Adjustments

Adjusted

Trial Balance

Income

Statement

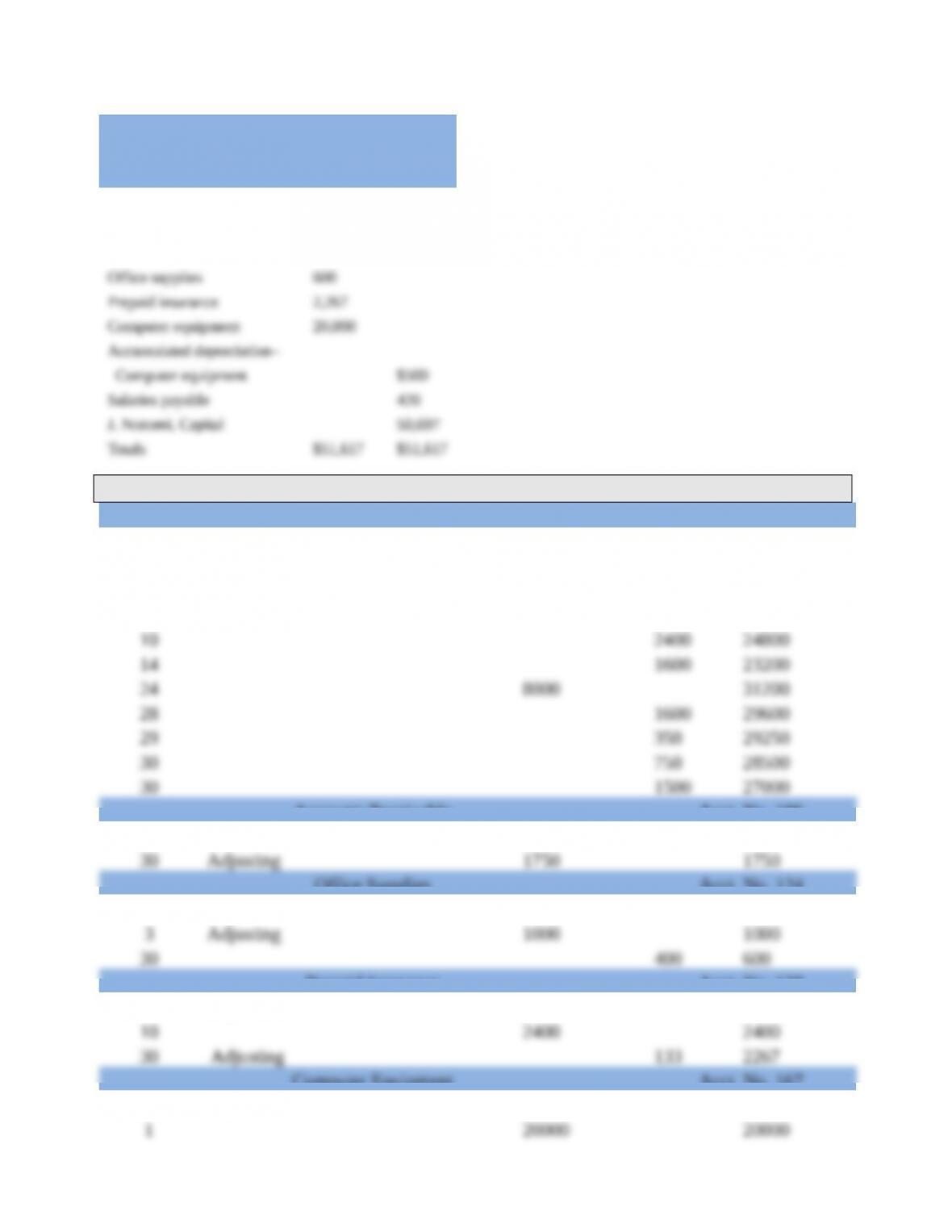

No. Account Title Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr.

101 Cash……………………………………

18,500 18,500

126 Supplies………………………………..

9,900 (a) 6,600 3,300

128 Prepaid insurance…………………….

7,200 (b) 3,800 3,400

167 Equipment……………………………..

132,000 132,000

168 Accumulated depreciation—

Equipment………………………………. 26,250 (c) 8,400 34,650

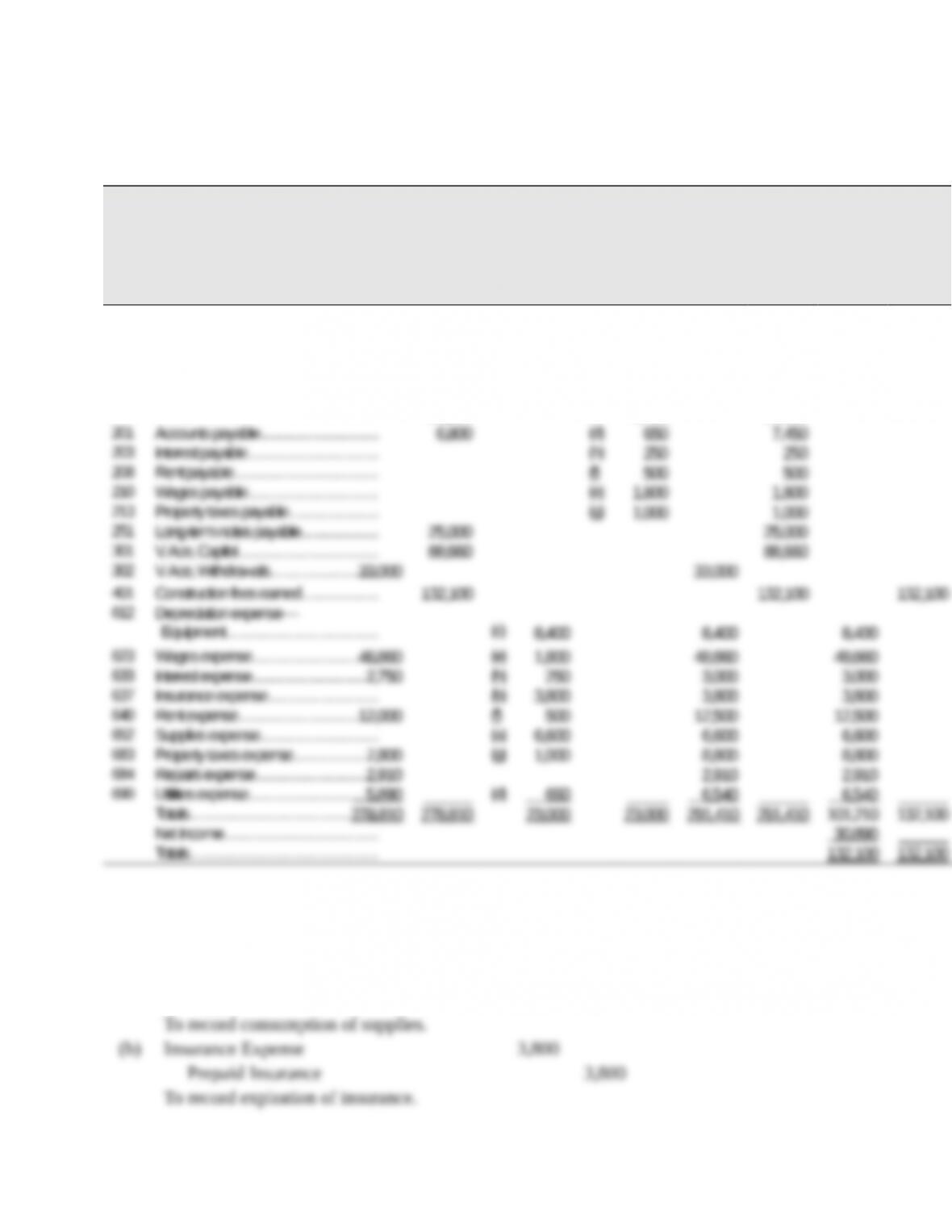

Part 2 Adjusting entries (all dated June 30, 2013)

Instructor note: Entries are shown without an account reference column because no posting is required.

(a) Supplies Expense 6,600

Supplies 6,600

(c) Depreciation Expense—Equipment 8,400

Accumulated Depreciation—Equipment 8,400

To record depreciation.

To record interest expense for June.

Closing entries (all dated June 30, 2013)

Instructor note: Entries are shown without an account reference column because no posting is required.

1 Construction Fees Earned 132,100

Income Summary 132,100

To close the revenue account.

2 Income Summary 101,210

Depreciation Expense–Equipment 8,400

Wages Expense 48,660

To close the Income Summary account.

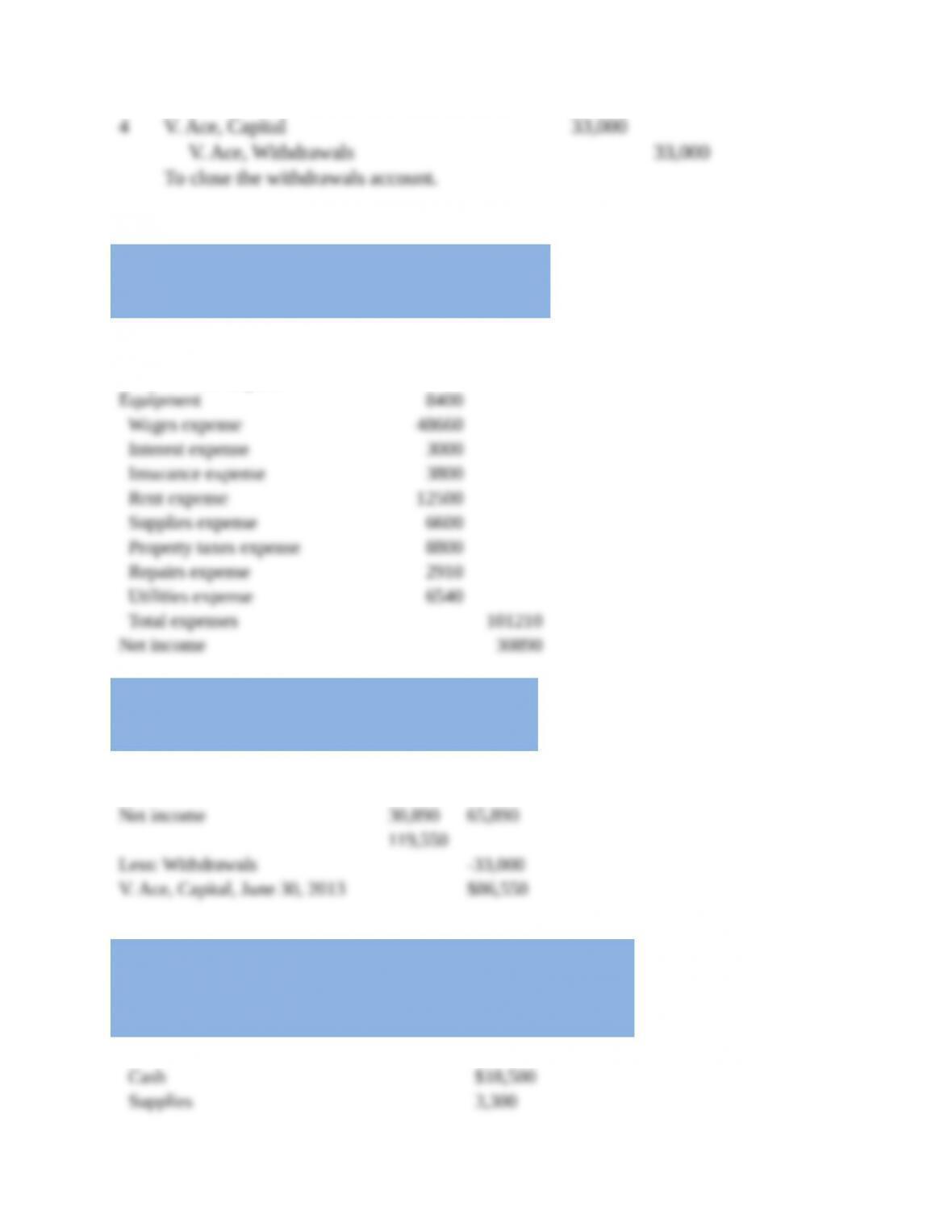

Part 3

ACE Construction Co.

Income Statement

For Year Ended June 30, 2013

Construction fees earned 132100

Expenses

Depreciation expense—

ACE COnstruction Co.

Statement of Owner’s Equity

For Year Ended June 30, 2013

V. Ace, Capital, June 30, 2012 $53,660

Add: Owner contribution $35,000

ACE Construction Co.

Balance Sheet

30-Jun-13

Assets

Current assets

Total current assets $25,200

Plant assets

Equipment 132,000

Accumulated depreciation—Equipment -34,650 97,350

Equity

Part 4

(a) This error enters the wrong amount in the correct accounts. The ending

balance of the Supplies account should be $3,300, but the entry reduces

The adjusted trial balance columns in the work sheet will be equal, but the

This error is not likely to be detected as a result of completing the work

(b) This error inserts a credit in the adjusted trial balance when a debit should

have been inserted. As a result, the trial balance will not balance (the

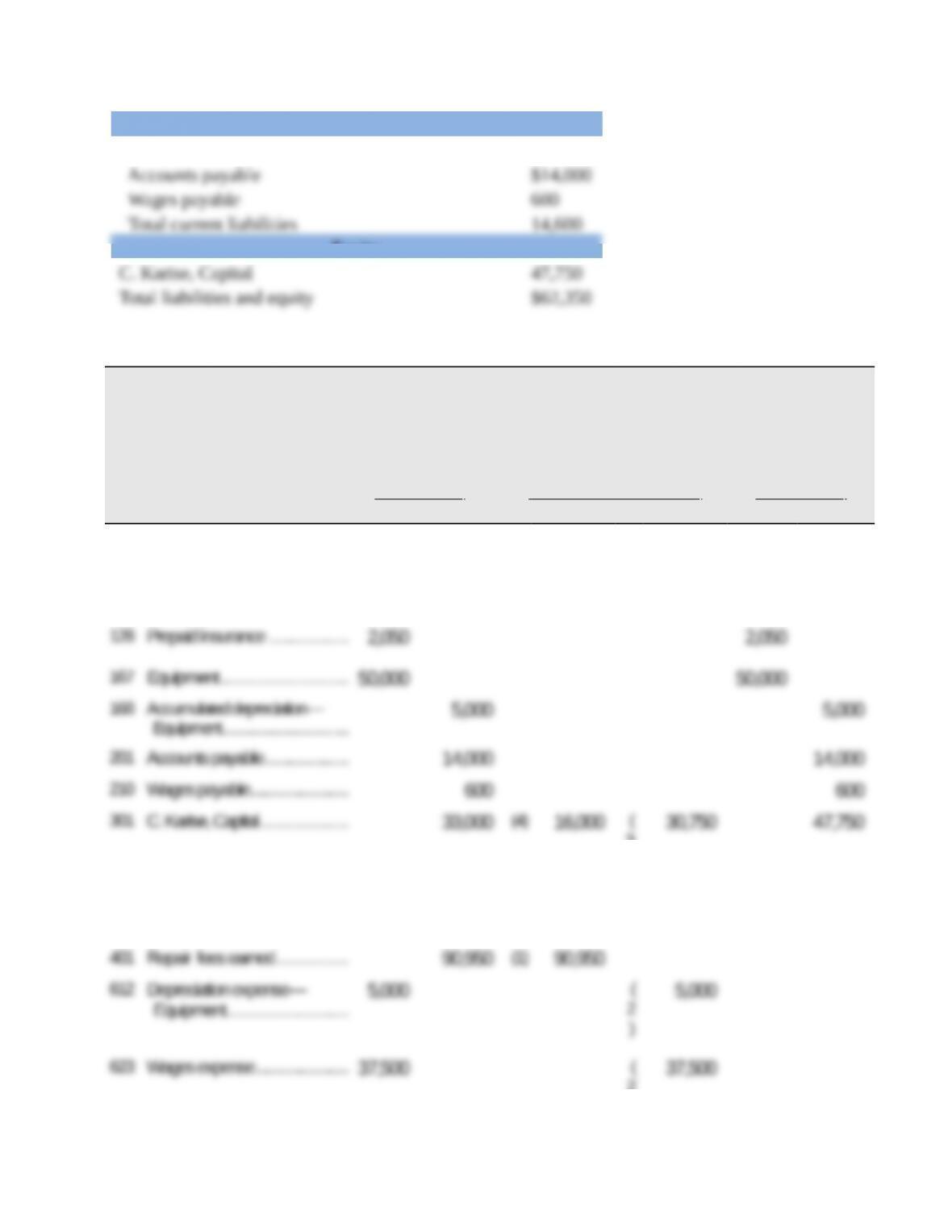

Title: Problem 4-4A

QA_Ori:

Part 1

KARISE REPAIRS

Income Statement

For Year Ended December 31, 2013

Repair fees earned $90,950

Expenses

Depreciation expense—Equipment $5,000

Wages expense 37,500

KARISE REPAIRS

Statement of Owner’s Equity

For Year Ended December 31, 2013

C. Karise, Capital, Jan. 1, 2013 $33,000

Karise REPAIRS

Balance Sheet

31-Dec-13

Assets

Current assets

Cash $14,000

Liabilities

Current liabilities

Equity

Parts 2 and 3

KARISE REPAIRS

Work Sheet

For Year Ended December 31, 2013

Adjusted

Trial Balance

Closing Entry Information

Post-Closing

Trial Balance

No. Account Title Dr. Cr. Dr. Cr. Dr. Cr.

101 Cash……………………………. 14,000 14,000

124 Office supplies…………………. 1,300 1,300

3

)

302 C. Karise, Withdrawals……….. 16,000 (

4

)

16,000

2

)

637 Insurance expense…………… 800 (

2

)

800

1 Repair Fees Earned 90,950

Income Summary 90,950

To close the revenue account.

Part 4

(a) If none of the $800 insurance expense had expired, the income statement

(b) If there were no earned and unpaid wages (meaning Wages Payable equals

Financial Statement Changes

The income statement would reflect the following:

Net income would be increased by $800 + $600 = $1,400.

The balance sheet would reflect the following:

Parts 2 and 3