Title: Exercise 23-1

QA_Ori:

Item Cost

a. Bike frames Variable

b. Screws for assembly Variable

c. Repair expense for tools (If these costs are only remotely

related to volume, they may be better classified as fixed)

Variable

* Incoming shipping expenses are variable with respect to the number (volume)

of incoming shipments, not production.

** Gas used for heating is often a mixed cost rather than strictly variable.

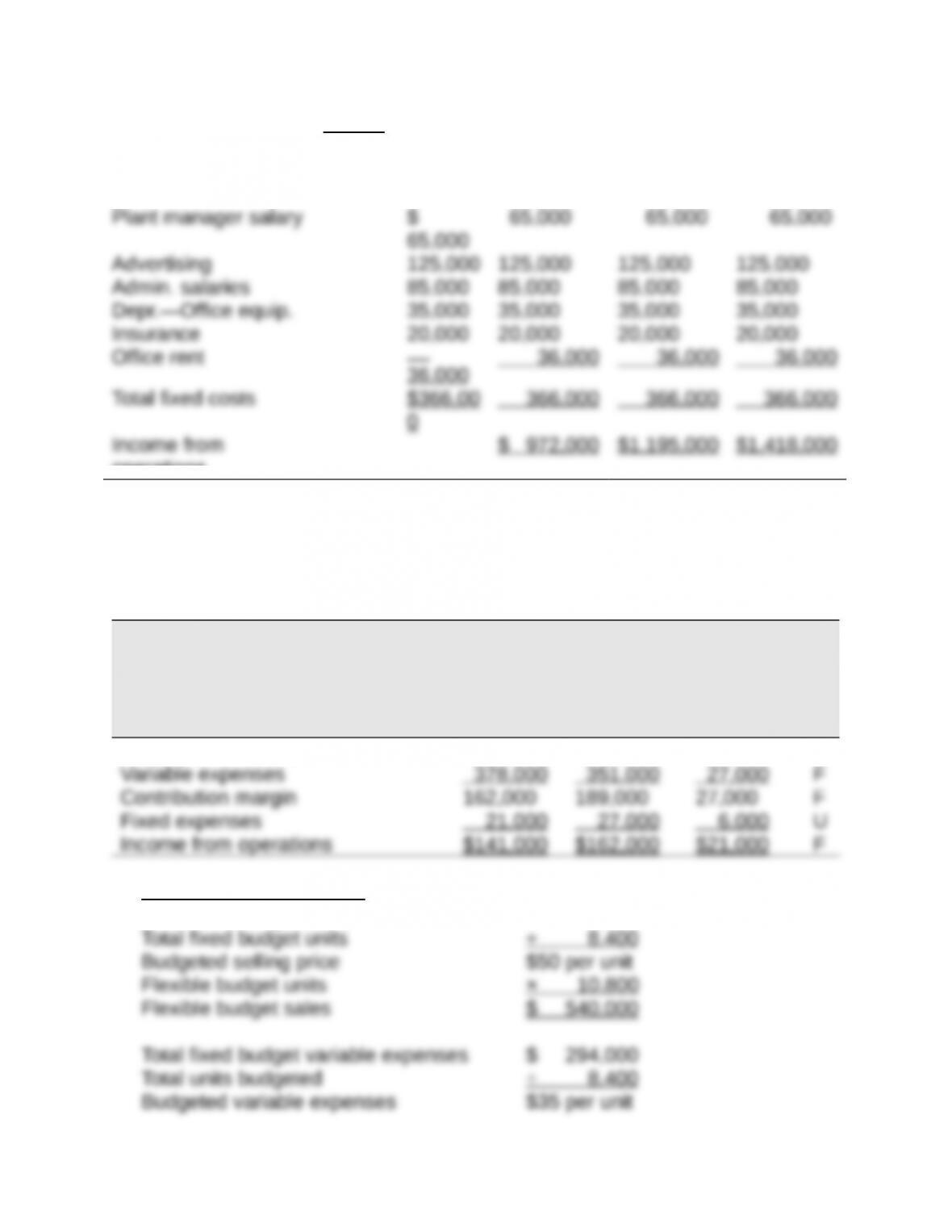

Title: Exercise 23-2

QA_Ori:

TEMPO COMPANY

Flexible Budgets

For Quarter Ended March 31, 2013

Flexible Budget Flexible Flexible Flexible

Variable

Amount

per

Unit*

Total

Fixed

Cost

Budget for

Unit Sales

of 6,000

Budget for

Unit Sales

of 7,000

Budget for

Unit Sales

of 8,000

Sales $400.0

0

$2,400,000 $2,800,000 $3,200,000

Variable costs

Direct materials 40.00 240,000 280,000 320,000

177.00

Contribution margin $223.0

0

1,338,000 1,561,000 1,784,000

Fixed costs

operations

* Equals total variable costs divided by the volume of 7,000 units.

Title: Exercise 23-3

QA_Ori:

SOLITAIRE COMPANY

Flexible Budget Performance Report

For Month Ended June 30

Flexible Actual

Budget Results Variances

Sales (10,800 units) $540,000 $540,000 $ 0

Supporting computations

Total fixed budget sales $ 420,000

QA_Edit:

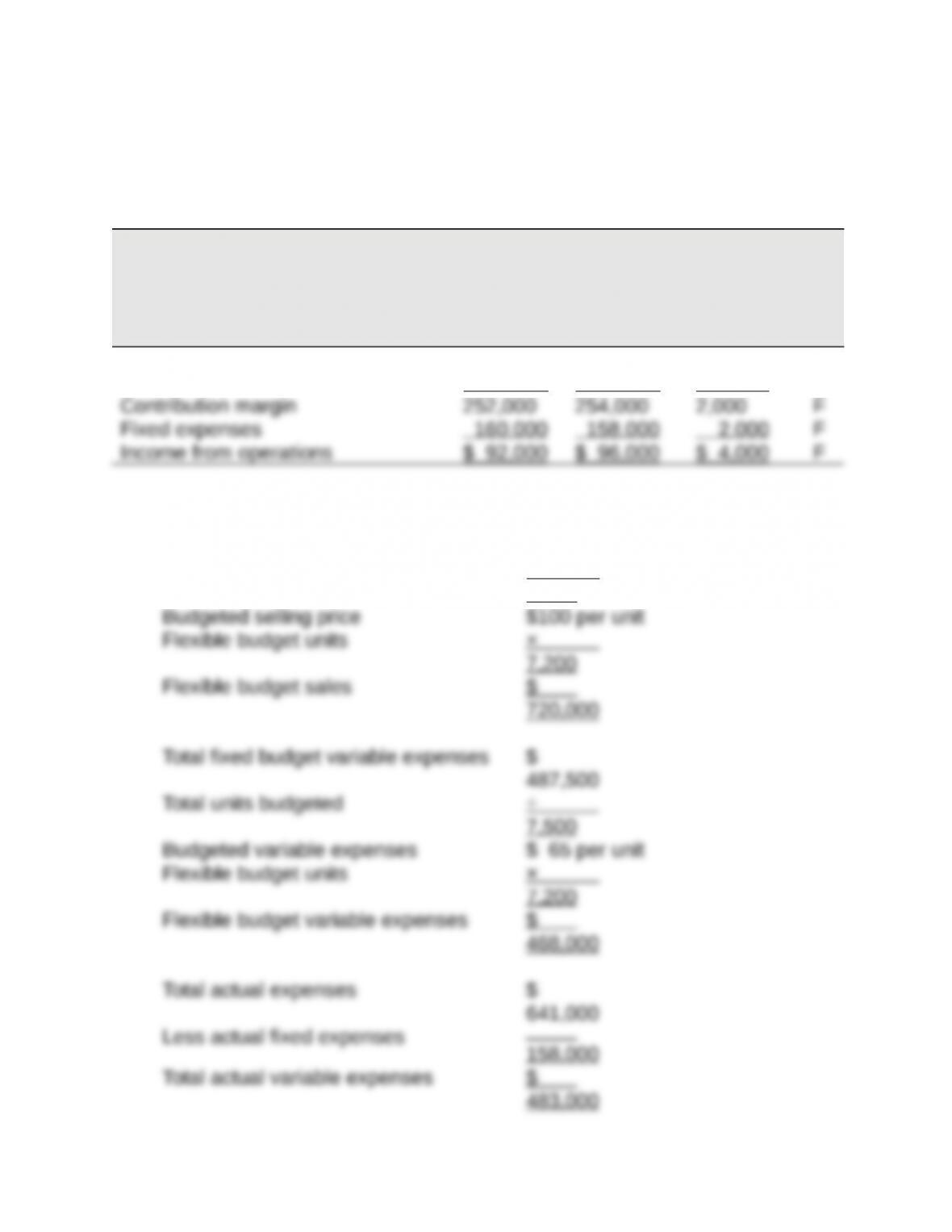

Title: Exercise 23-4

QA_Ori:

BAY CITY COMPANY

Flexible Budget Performance Report

For Month Ended July 31

Flexible Actual

Budget Results Variances

Sales (7,200 units) $720,000 $737,000 $17,000 F

Variable expenses 468,000 483,000 15,000 U

Supporting computations

Total fixed budget sales $

750,000

Total units budgeted ÷

7,500

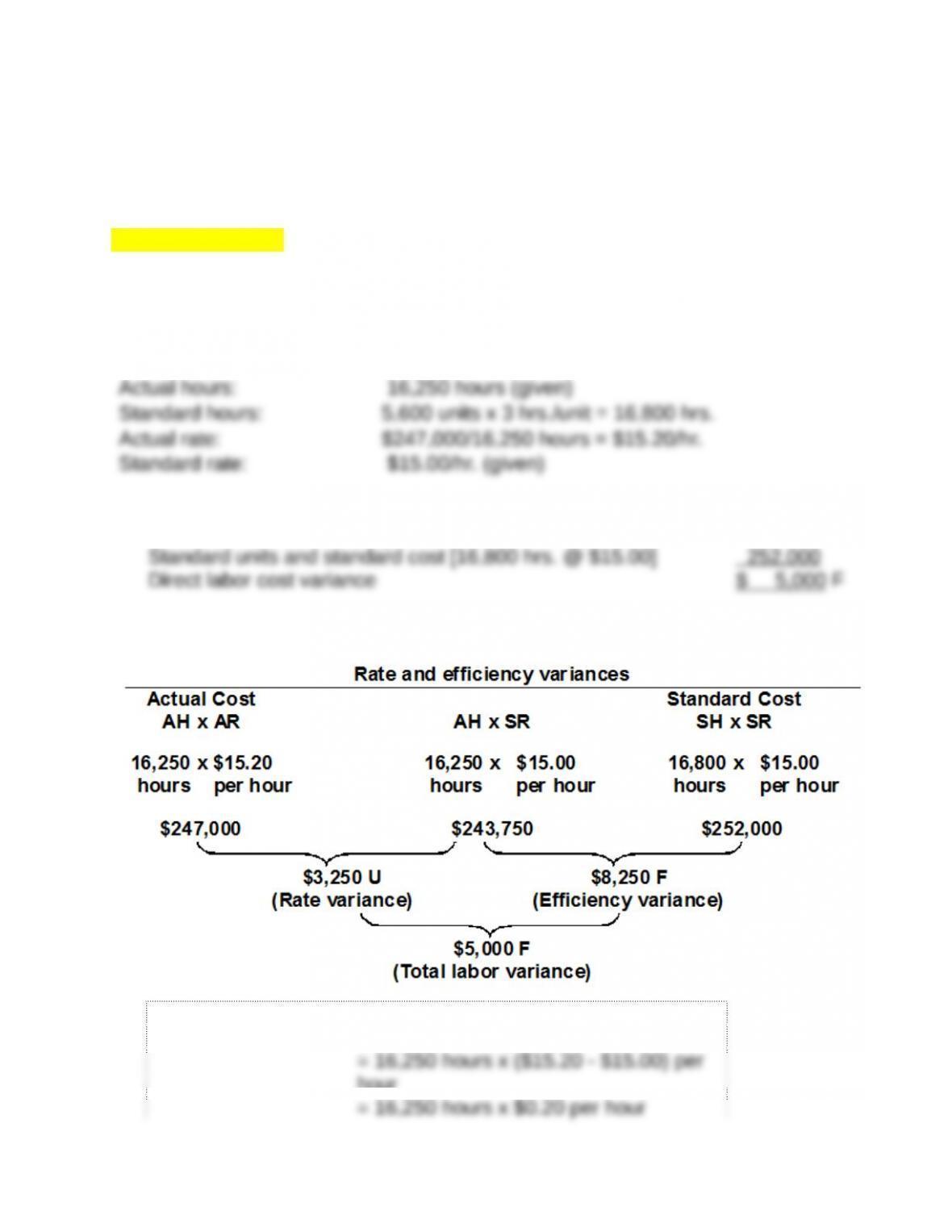

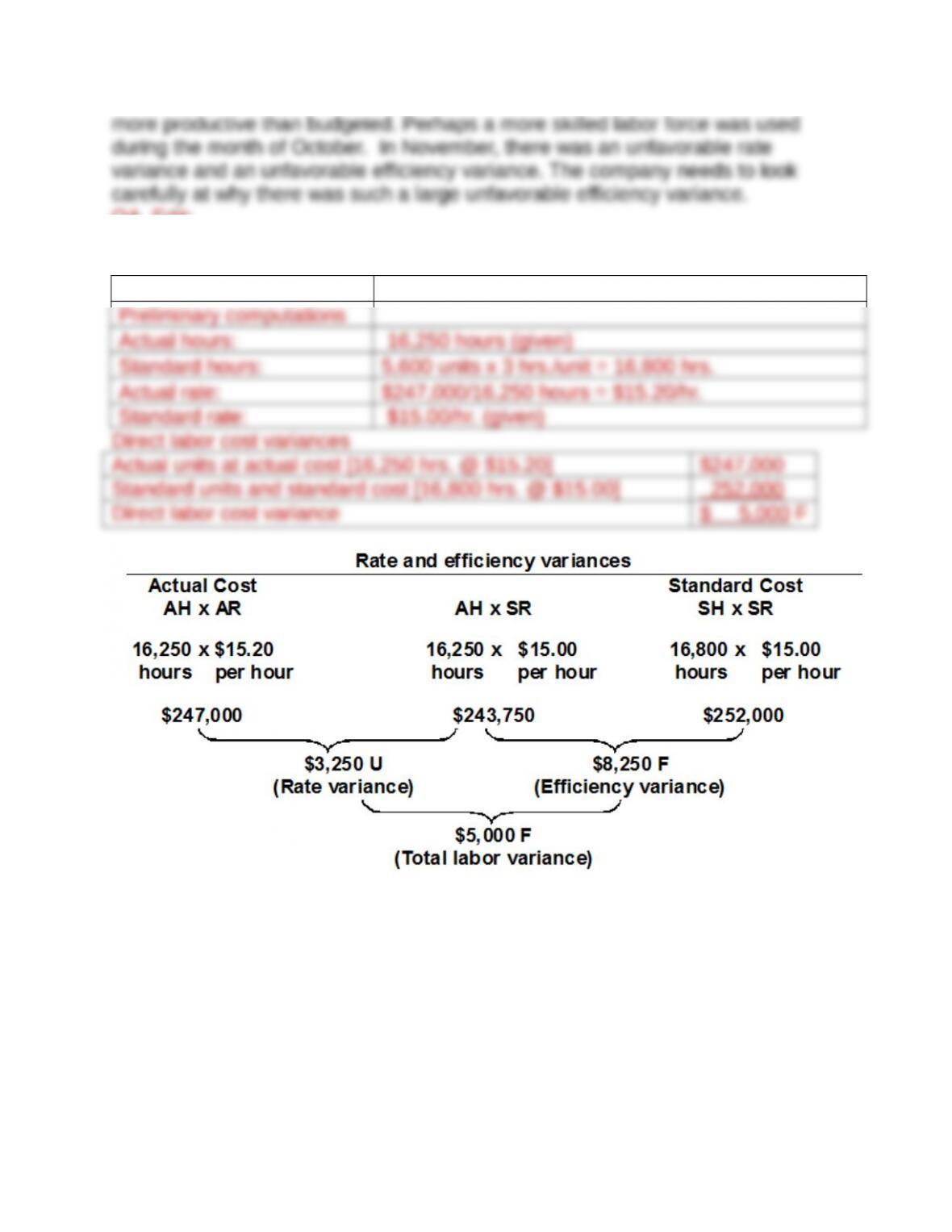

Title: Exercise 23-5

QA_Ori:

1.

October variances

October variances

Preliminary computations

Direct labor cost variances

Actual units at actual cost [16,250 hrs. @ $15.20] $247,000

Alternate solution format

Rate variance = AH x (AR – SR)

hour

Efficiency variance = (AH – SH) x SR

hour

November variances

Preliminary computations

Actual hours: 22,000 hours (given)

Direct labor cost variances

hours per hour hours per hour hours per hour

(Rate variance)

(Efficiency variance)

(Total labor variance)

2.

The unfavorable labor rate variance in October means the actual rate for an hour

of labor is greater than budgeted. The favorable labor efficiency variance means

QA_Edit:

1.

October variances

October variances

Title: Exercise 23-6

QA_Ori:

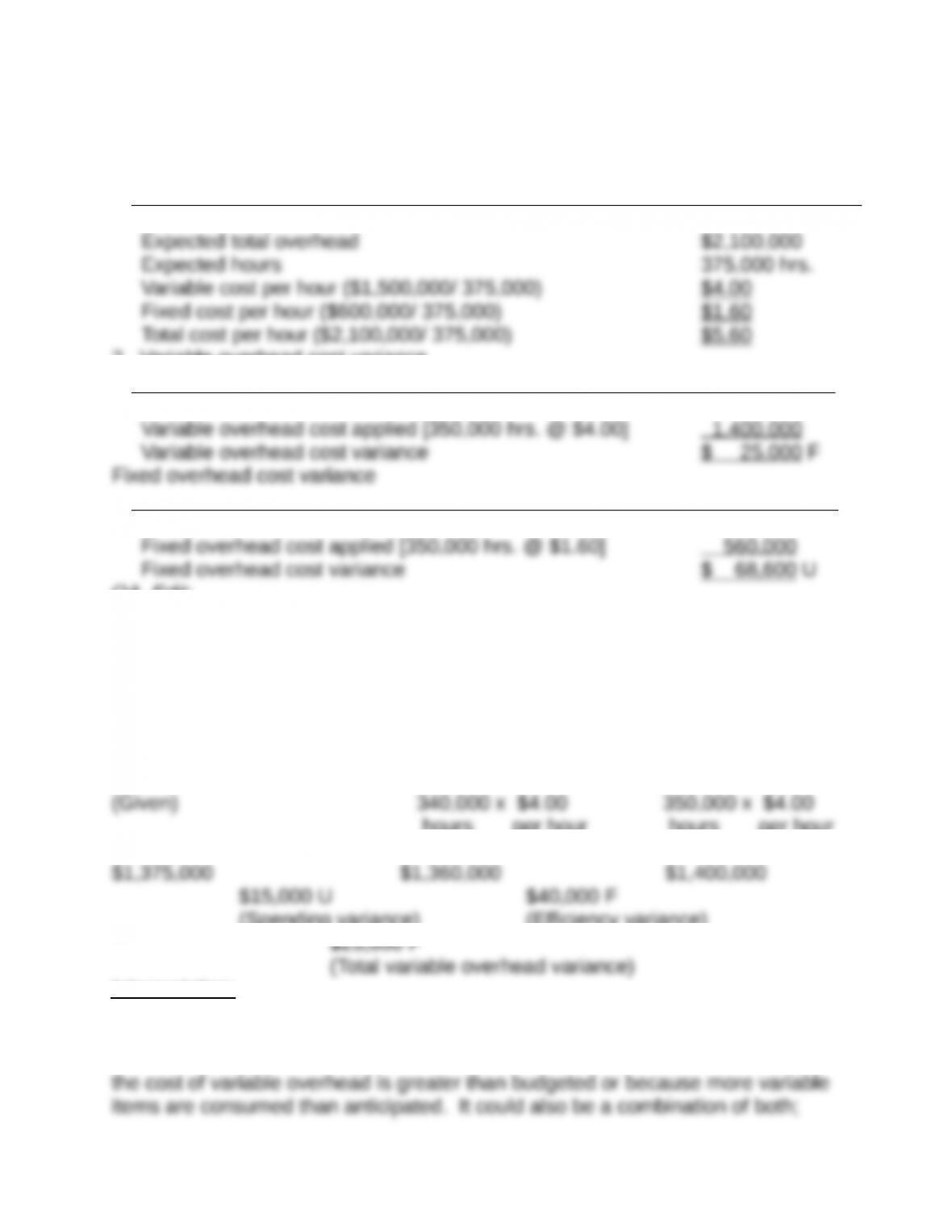

1. Predetermined overhead rate computations

Expected volume 75%

2. Variable overhead cost variance

Variable overhead cost incurred [given] $1,375,000

Fixed overhead cost incurred [given] $ 628,600

QA_Edit:

Title: Exercise 23-7A

QA_Ori:

1.

Variable overhead spending and efficiency variances

Actual Overhead

AH x AVR AH x SVR

Applied Overhead

SH x SVR

hours per hour hours per hour

(Spending variance)

(Efficiency variance)

(Total variable overhead variance)

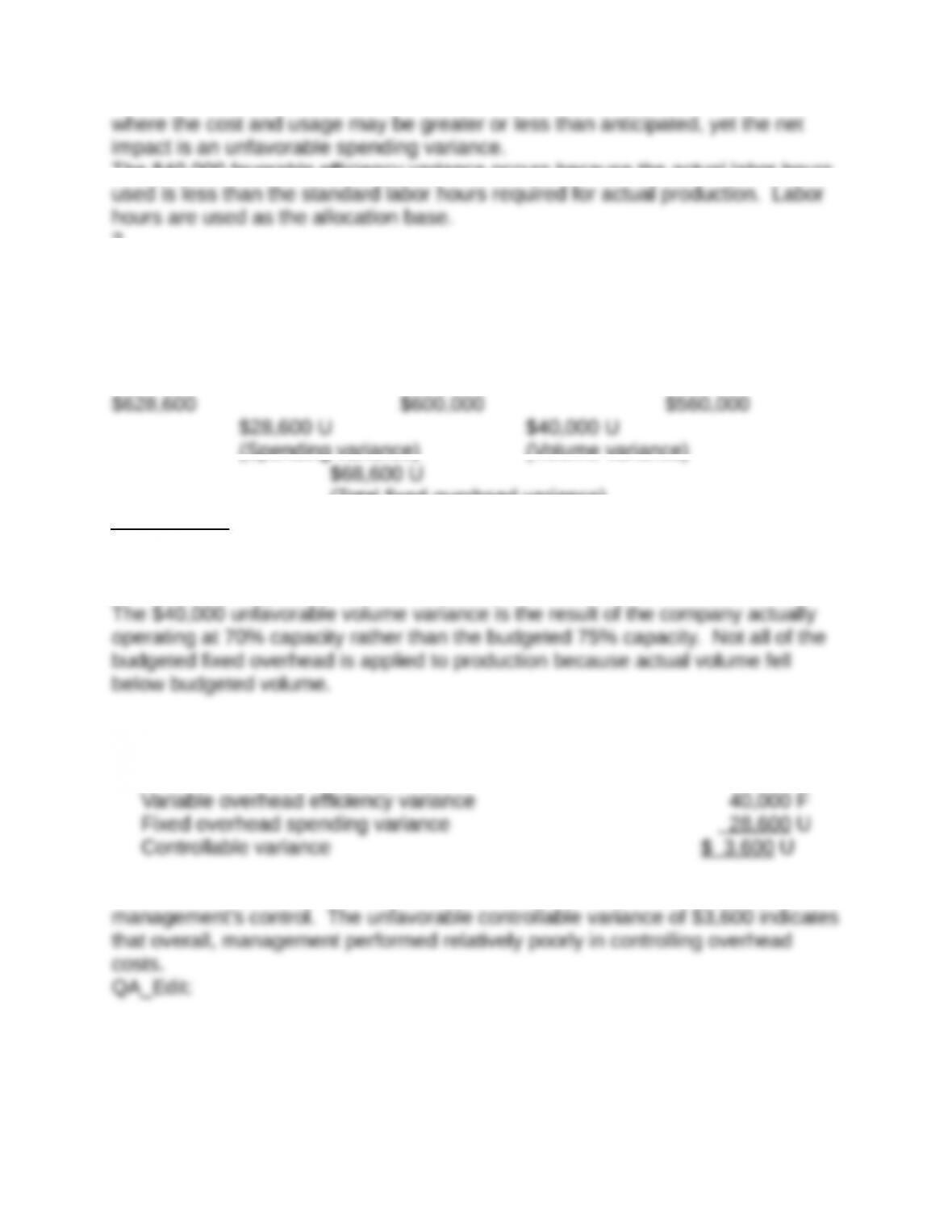

Interpretation:

The $15,000 unfavorable spending variance means the actual cost of variable

overhead is more than budgeted. This unfavorable variance can occur because

The $40,000 favorable efficiency variance occurs because the actual labor hours

2.

Fixed overhead spending and volume variances

Actual Overhead Budgeted Overhead Applied Overhead

(Given) (Given) 350,000 x $1.60

hours per hour

(Spending variance)

(Volume variance)

(Total fixed overhead variance)

Interpretation

The $28,600 unfavorable spending variance means actual cost of fixed overhead

is more than budgeted.

3. The controllable variance is computed as:

Variable overhead spending variance $15,000 U

The controllable variance refers to activities that are considered within

Title: Exercise 23-8

QA_Ori:

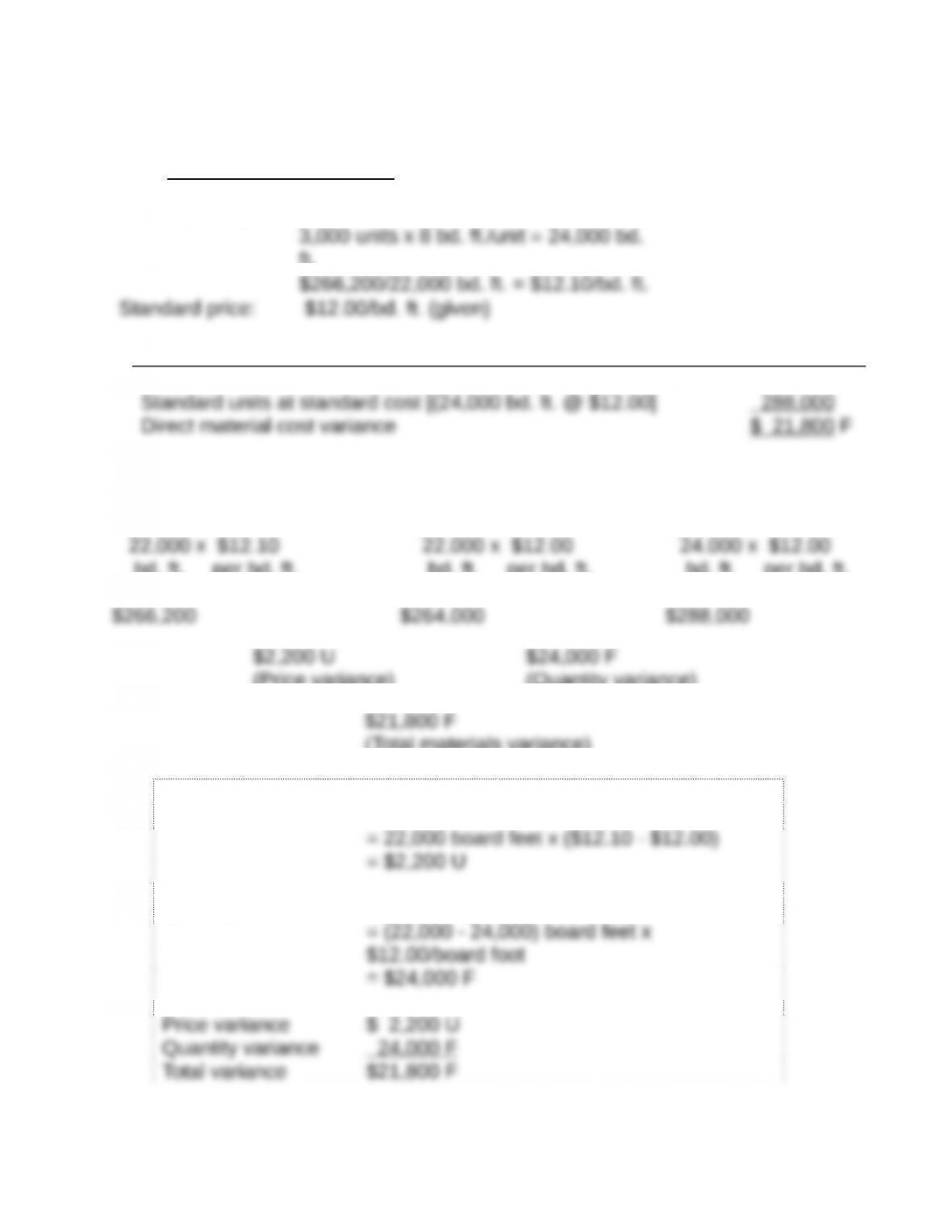

1. Preliminary computations

Actual quantity: 22,000 bd. ft. (given)

ft.

Direct material cost variances

Actual units at actual cost [22,000 bd. ft. @ $12.10] $266,200

Price and quantity variances

Actual Cost

AQ x AP AQ x SP

Standard Cost

SQ x SP

bd. ft. per bd. ft. bd. ft. per bd. ft. bd. ft. per bd. ft.

(Price variance)

(Quantity variance)

(Total materials variance)

Alternate solution format

Price variance = AQ x (AP – SP)

Quantity variance = (AQ – SQ) x SP

2. The unfavorable price variance means the actual price paid is more than the