Serial Problem, SP 3 (Continued)

Part 6

SUCCESS SYSTEMS

Balance Sheet

December 31, 2013

Assets

Cash …………………………………………………………………….. $ 58,160

Accounts receivable …………………………………………….. 5,668

Computer supplies ……………………………………………….. 580

Prepaid insurance ………………………………………………… 1,665

Liabilities

Accounts payable ………………………………………………….. $ 1,100

Wages payable ……………………………………………………… 500

Unearned computer services revenue ……………………. 1,500

Total liabilities ………………………………………………………. 3,100

Equity

Serial Problem, SP 3 (Continued)

[Note: Ledger includes all entries from prior three months. The Working Papers shorten

the solution by showing account balances as of November 30.]

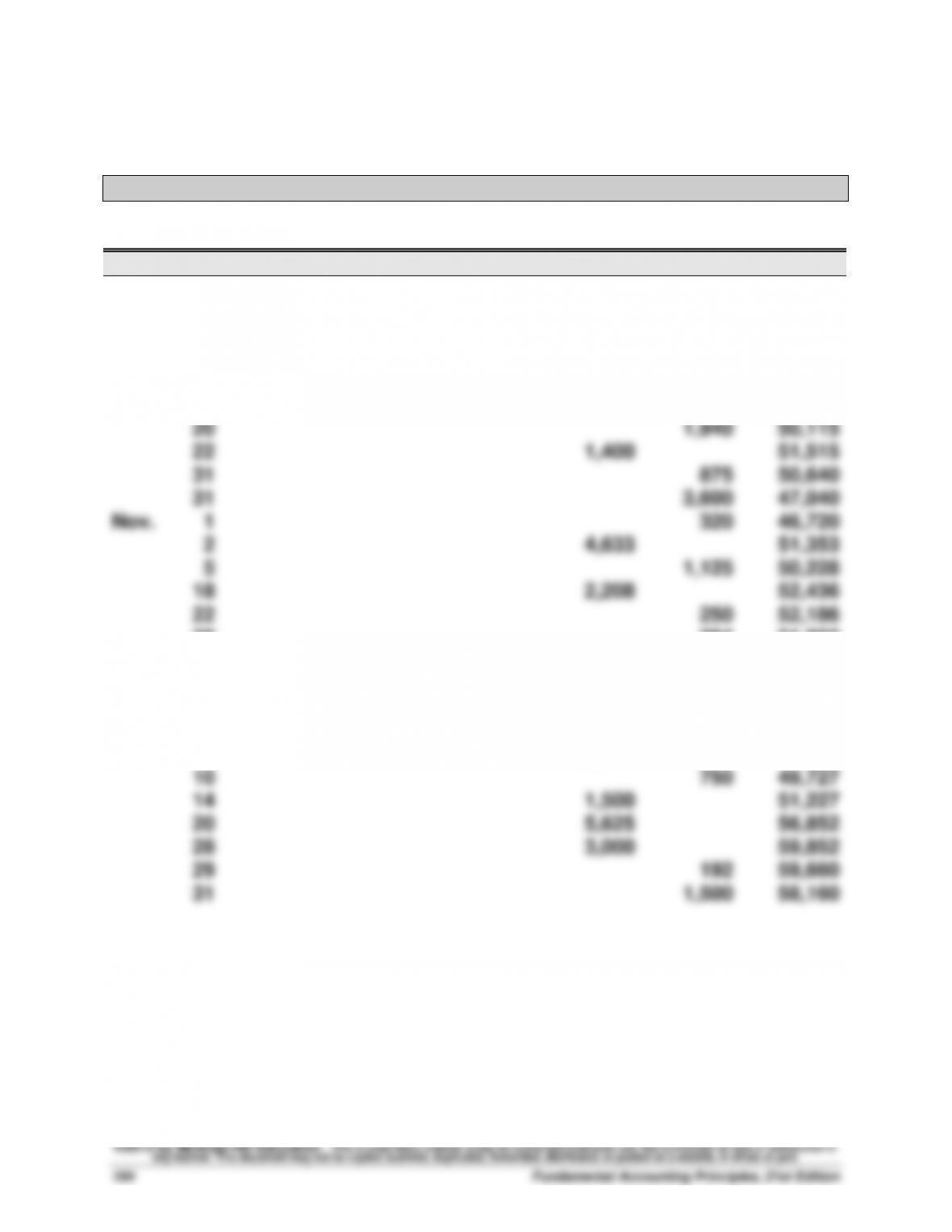

General Ledger

Cash

Acct. No. 101

Date

Explanation

PR

Debit

Credit

Balance

Oct.

1

55,000

55,000

2

3,300

51,700

5

2,220

49,480

8

1,420

48,060

15

4,800

52,860

17

805

52,055

20

1,940

50,115

22

1,400

51,515

31

875

50,640

31

3,600

47,040

Nov.

1

320

46,720

2

4,633

51,353

5

1,125

50,228

18

2,208

52,436

22

250

52,186

28

384

51,802

30

1,750

50,052

30

2,000

48,052

Dec.

2

1,025

47,027

3

500

46,527

4

3,950

50,477

10

750

49,727

14

1,500

51,227

20

5,625

56,852

28

3,000

59,852

29

192

59,660

31

1,500

58,160

Serial Problem, SP 3 (Continued)

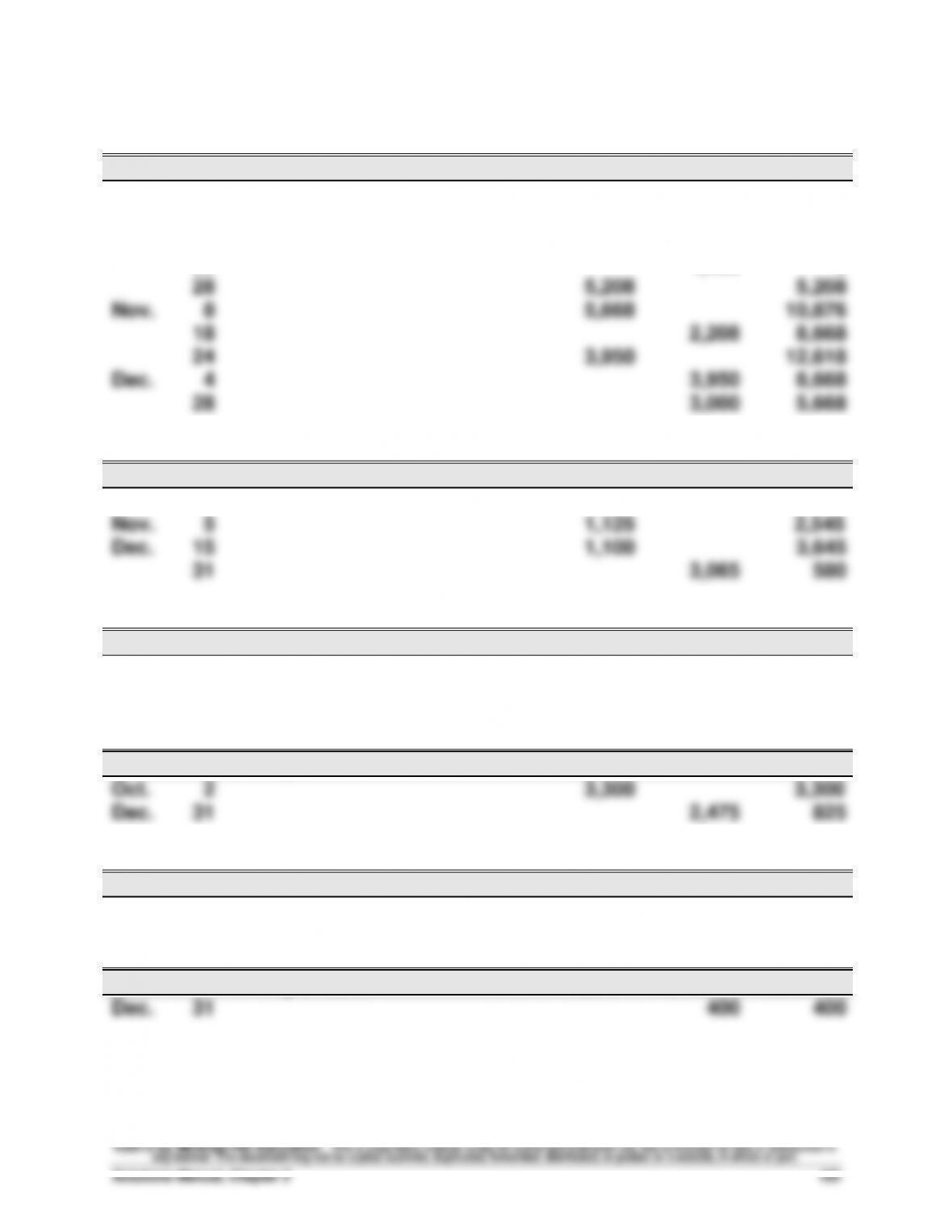

Accounts Receivable

Acct. No. 106

Date

Explanation

PR

Debit

Credit

Balance

Oct.

6

4,800

4,800

12

1,400

6,200

15

4,800

1,400

22

1,400

0

28

5,208

5,208

Nov.

8

5,668

10,876

18

2,208

8,668

24

3,950

12,618

Dec.

4

3,950

8,668

28

3,000

5,668

Computer Supplies

Acct. No. 126

Date

Explanation

PR

Debit

Credit

Balance

Oct.

3

1,420

1,420

Nov.

5

1,125

2,545

Dec.

15

1,100

3,645

31

3,065

580

Prepaid Insurance

Acct. No. 128

Date

Explanation

PR

Debit

Credit

Balance

Oct.

5

2,220

2,220

Dec.

31

555

1,665

Prepaid Rent

Acct. No. 131

Date

Explanation

PR

Debit

Credit

Balance

Oct.

2

3,300

3,300

Dec.

31

2,475

825

Office Equipment

Acct. No. 163

Date

Explanation

PR

Debit

Credit

Balance

Oct.

1

8,000

8,000

Accumulated Depreciation—Office Equipment

Acct. No. 164

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

400

400

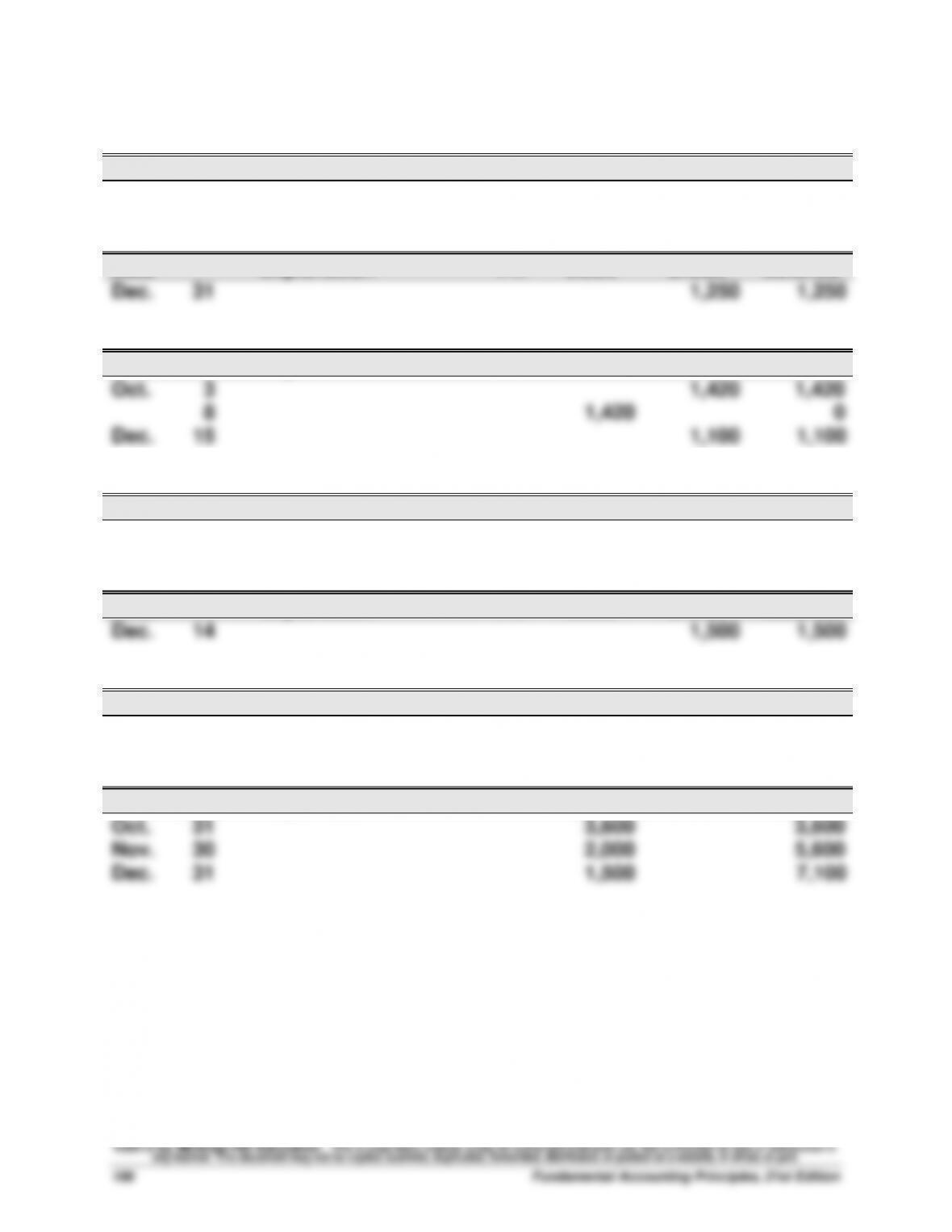

Serial Problem, SP 3 (Continued)

Computer Equipment

Acct. No. 167

Date

Explanation

PR

Debit

Credit

Balance

Oct.

1

20,000

20,000

Accumulated Depreciation—Computer Equipment

Acct. No. 168

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

1,250

1,250

Accounts Payable

Acct. No. 201

Date

Explanation

PR

Debit

Credit

Balance

Oct.

3

1,420

1,420

8

1,420

0

Dec.

15

1,100

1,100

Wages Payable

Acct. No. 210

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

500

500

Unearned Computer Services Revenue

Acct. No. 236

Date

Explanation

PR

Debit

Credit

Balance

Dec.

14

1,500

1,500

A. Lopez, Capital

Acct. No. 301

Date

Explanation

PR

Debit

Credit

Balance

Oct.

1

83,000

83,000

A. Lopez, Withdrawals

Acct. No. 302

Date

Explanation

PR

Debit

Credit

Balance

Oct.

31

3,600

3,600

Nov.

30

2,000

5,600

Dec.

31

1,500

7,100

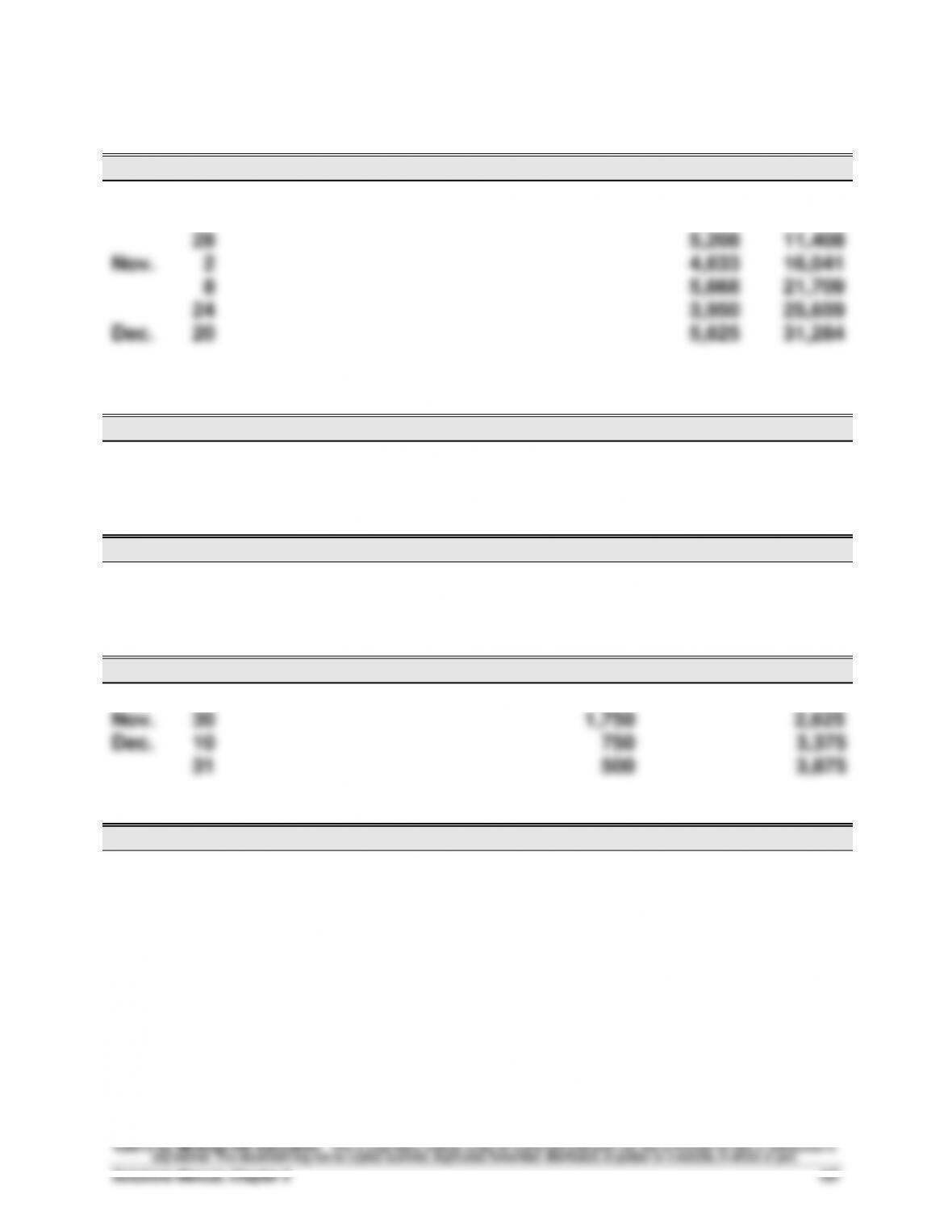

Serial Problem, SP 3 (Continued)

Computer Services Revenue

Acct. No. 403

Date

Explanation

PR

Debit

Credit

Balance

Oct.

6

4,800

4,800

12

1,400

6,200

28

5,208

11,408

Nov.

2

4,633

16,041

8

5,668

21,709

24

3,950

25,659

Dec.

20

5,625

31,284

Depreciation Expense—Office Equipment

Acct. No. 612

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

400

400

Depreciation Expense—Computer Equipment

Acct. No. 613

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

1,250

1,250

Wages Expense

Acct. No. 623

Date

Explanation

PR

Debit

Credit

Balance

Oct.

31

875

875

Nov.

30

1,750

2,625

Dec.

10

750

3,375

31

500

3,875

Insurance Expense

Acct. No. 637

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

555

555

Serial Problem, SP 3 (Concluded)

Rent Expense

Acct. No. 640

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

2,475

2,475

Computer Supplies Expense

Acct. No. 652

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

3,065

3,065

Advertising Expense

Acct. No. 655

Date

Explanation

PR

Debit

Credit

Balance

Oct.

20

1,940

1,940

Dec.

2

1,025

2,965

Mileage Expense

Acct. No. 676

Date

Explanation

PR

Debit

Credit

Balance

Nov.

1

320

320

28

384

704

Dec.

29

192

896

Miscellaneous Expense

Acct. No. 677

Date

Explanation

PR

Debit

Credit

Balance

Nov.

22

250

250

Repairs Expense—Computer

Acct. No. 684

Date

Explanation

PR

Debit

Credit

Balance

Oct.

17

805

805

Dec.

3

500

1,305

Reporting in Action — BTN 3-1

1. The revenue recognition principle requires that revenue be recorded

customers.

2. Polaris provides information on revenue recognition in its Note 1 titled

“Organization and Significant Accounting Policies.” They report that

3. For year-end December 31, 2010, the profit margin is ($ thousands):

$147,138 / $1,991,139 = 0.074 = 7.4%

4. Solution depends on the financial statements accessed.

Comparative Analysis — BTN 3-2

($ in thousands)

1. Polaris

Current year, profit margin = $227,575 / $2,656,949 = 0.086 = 8.6%

Prior year, profit margin = $147,138 / $1,991,139 = 0.074 = 7.4%

Arctic Cat

2. Polaris is more successful on the basis of profit margin in both the

current and prior years relative to Arctic Cat. Both companies

Ethics Challenge — BTN 3-3

1. GAAP requires that annual deprecation be accumulated in a contra–

asset account, called Accumulated Depreciation. While property, plant,

2. One strength of Smith’s method would be the ease of preparing the

balance sheet. The property, plant, and equipment balance in the

adjusted trial balance would be directly transferable to the balance sheet

3. While both approaches would lead to the same total assets on the

balance sheet, GAAP requires Boland’s approach. As a professional,

Communicating in Practice — BTN 3-4

This communication activity has no set solution. A class discussion of the

Taking It to the Net — BTN 3-5

1. The Gap’s main brands (stores) are The Gap, Old Navy, and Banana

2. The Gap’s fiscal year-end is January 28, 2012. It appears that The Gap’s

3. Net sales for the year ended January 28, 2012, are $14,549 million.

5. Profit margin = $833 million / $14,549 million = 5.73%

6. The company probably chose a fiscal year-end as the end of January or

Teamwork in Action — BTN 3-6

Note that there is no specific solution to this activity. Still, the presentation

of each expert team should reflect the following summary points:

Before Adjusting

Balance Sheet Income Statement

Type Account Account Adjusting Entry

Prepaid expenses Asset overstated Expense understated Dr. Expense

Cr. Asset*

* For depreciation, one would Credit the Accumulated Depreciation contra account.

Some implementation notes: This activity allows all students to be actively

involved in the learning process. Encourage students to take the opportunity

Entrepreneurial Decision — BTN 3-7

1. a. To record the collection of cash from sale of the gift certificate in

advance of delivery of merchandise to the customer:

b. To record the delivery of merchandise to the customer when he/she

uses the gift certificate:

2. Carrying less inventory would allows ash&dans to save the costs of

carrying that added inventory; such as warehousing costs, insurance,

3. If it carries additional inventory, ash&dans can potentially sell more

merchandise and increase its profits. This might further fuel increased

sales as additional customers might be attracted to its products. On

Hitting the Road — BTN 3-8

There is no formal solution to this field activity. The instructor may wish to

tally students’ findings to see what companies were selected, who

Global Decision — BTN 3-9

1. Piaggio’s Note 2.2 (Accounting Policies — Recognition of revenues)

reports that:

“According to IFRS, sales of goods are recognised when the goods are

dispatched and the company has transferred the significant risks and

accrual basis.”

2. (Euro in thousands)