23–41

95. Bok Company’s output for the current period was assigned a $200,000 standard direct

materials cost. The direct materials variances included a $5,000 favorable price variance and a

$3,000 unfavorable quantity variance. What is the actual total direct materials cost for the

current period?

A. $208,000.

B. $198,000.

C. $202,000.

D. $192,000.

E. $205,000.

96. Bok Company’s output for the current period was assigned a $400,000 standard direct

labor cost. The direct labor variances included a $10,000 unfavorable direct labor rate

variance and a $4,000 favorable direct labor efficiency variance. What is the actual total direct

labor cost for the current period?

A. $414,000.

B. $386,000.

C. $394,000.

D. $406,000.

E. $410,000.

97. Brewer Company specializes in selling used cars. During the month, the dealership sold

22 cars at an average price of $15,000 each. The budget for the month was to sell 20 cars at an

average price of $16,000. Compute the dealership’s sales price variance for the month.

A. $22,000 unfavorable.

B. $10,000 favorable.

C. $22,000 favorable.

D. $32,000 unfavorable.

E. $32,000 favorable.

23–42

98. Brewer Company specializes in selling used cars. During the month, the dealership sold

22 cars at an average price of $15,000 each. The budget for the month was to sell 20 cars at an

average price of $16,000. Compute the dealership’s sales volume variance for the month.

A. $22,000 unfavorable.

B. $10,000 favorable.

C. $22,000 favorable.

D. $32,000 unfavorable.

E. $32,000 favorable.

99. Cabot Company collected the following data regarding production of one of its products.

Compute the direct materials cost variance.

Direct materials standard (6 lbs. @ $2/lb.) $12 per finished unit

Actual direct materials used 243,000 lbs.

Actual finished units produced 40,000 units

Actual cost of direct materials used $483,570

A. $6,000 favorable.

B. $3,570 unfavorable.

C. $2,430 favorable.

D. $6,000 unfavorable.

E. $3,570 favorable.

100. Cabot Company collected the following data regarding production of one of its products.

Compute the direct materials price variance.

Direct materials standard (6 lbs. @ $2/lb.) $12 per finished unit

Actual direct materials used 243,000 lbs.

Actual finished units produced 40,000 units

Actual cost of direct materials used $483,570

A. $2,430 unfavorable.

B. $3,570 unfavorable.

C. $2,430 favorable.

D. $6,000 unfavorable.

E. $3,570 favorable.

23–44

101. Cabot Company collected the following data regarding production of one of its products.

Compute the direct materials quantity variance.

Direct materials standard (6 lbs. @ $2/lb.)

$12 per finished unit

Actual direct materials used 243,000 lbs.

Actual finished units produced 40,000 units

Actual cost of direct materials used $483,570

A. $2,430 unfavorable.

B. $3,570 unfavorable.

C. $2,430 favorable.

D. $6,000 unfavorable.

E. $3,570 favorable.

102. Cabot Company collected the following data regarding production of one of its products.

Compute the direct labor cost variance.

Direct labor standard (2 hrs. @ $13/hr.) $26 per finished unit

Actual direct labor hours 81,000 hrs.

Actual finished units produced 40,000 units

Actual cost of direct labor $1,093,500

A. $53,500 unfavorable.

B. $40,500 favorable.

C. $53,500 favorable.

D. $13,000 unfavorable.

E. $40,500 unfavorable.

103. Cabot Company collected the following data regarding production of one of its products.

Compute the direct labor rate variance.

Direct labor standard (2 hrs. @ $13/hr.) $26 per finished unit

Actual direct labor hours 81,000 hrs.

Actual finished units produced 40,000 units

Actual cost of direct labor $1,093,500

A. $53,500 unfavorable.

B. $40,500 favorable.

C. $53,500 favorable.

D. $13,000 unfavorable.

E. $40,500 unfavorable.

23–46

104. Cabot Company collected the following data regarding production of one of its products.

Compute the direct labor efficiency variance.

Direct labor standard (2 hrs. @ $13/hr.) $26 per finished unit

Actual direct labor hours 81,000 hrs.

Actual finished units produced 40,000 units

Actual cost of direct labor $1,093,500

A. $13,000 favorable.

B. $40,500 favorable.

C. $53,500 favorable.

D. $13,000 unfavorable.

E. $40,500 unfavorable.

105. Cabot Company collected the following data regarding production of one of its products.

Compute the variable overhead cost variance.

Direct labor standard (2 hrs. @ $13/hr.) $26.00 per finished unit

Actual direct labor hours 81,000 hrs.

Budgeted units 42,000 units

Actual finished units produced 40,000 units

Standard variable OH rate (2 hrs. @ $14.30/hr.) $28.60 per finished unit

Standard fixed OH rate ($336,000/42,000 units) $8.00 per unit

Actual cost of variable overhead costs incurred $1,140,000

Actual cost of fixed overhead costs incurred $ 338,000

A. $18,000 favorable.

B. $4,000 favorable.

C. $18,000 unfavorable.

D. $18,300 favorable.

E. $14,300 unfavorable.

106. Cabot Company collected the following data regarding production of one of its products.

Compute the fixed overhead cost variance.

Direct labor standard (2 hrs. @ $13/hr.) $26.00 per finished unit

Actual direct labor hours 81,000 hrs.

Budgeted units 42,000 units

Actual finished units produced 40,000 units

Standard variable OH rate (2 hrs. @ $14.30/hr.) $28.60 per finished unit

Standard fixed OH rate ($336,000/42,000 units) $8.00 per unit

Actual cost of variable overhead costs incurred $1,140,000

Actual cost of fixed overhead costs incurred $ 338,000

A. $18,300 favorable.

B. $18,000 favorable.

C. $18,000 unfavorable.

D. $18,300 unfavorable.

E. $14,300 unfavorable.

107. Cabot Company collected the following data regarding production of one of its products.

Compute the variable overhead spending variance.

Direct labor standard (2 hrs. @ $13/hr.) $26.00 per finished unit

Actual direct labor hours 81,000 hrs.

Budgeted units 42,000 units

Actual finished units produced 40,000 units

Standard variable OH rate (2 hrs. @ $14.30/hr.) $28.60 per finished unit

Standard fixed OH rate ($336,000/42,000 units) $8.00 per unit

Actual cost of variable overhead costs incurred $1,140,000

Actual cost of fixed overhead costs incurred $ 338,000

A. $18,300 favorable.

B. $18,000 favorable.

C. $18,000 unfavorable.

D. $18,300 unfavorable.

E. $14,300 unfavorable.

23–49

108. Cabot Company collected the following data regarding production of one of its products.

Compute the variable overhead efficiency variance.

Direct labor standard (2 hrs. @ $13/hr.) $26.00 per finished unit

Actual direct labor hours 81,000 hrs.

Budgeted units 42,000 units

Actual finished units produced 40,000 units

Standard variable OH rate (2 hrs. @ $14.30/hr.) $28.60 per finished unit

Standard fixed OH rate ($336,000/42,000 units) $8.00 per unit

Actual cost of variable overhead costs incurred $1,140,000

Actual cost of fixed overhead costs incurred $ 338,000

A. $14,300 favorable.

B. $18,000 favorable.

C. $18,000 unfavorable.

D. $18,300 unfavorable.

E. $14,300 unfavorable.

109. Presented below are terms preceded by letters a through j and followed by a list of

definitions 1 through 10. Enter the letter of the term with the definition, using the space

preceding the definition.

(a) Cost variance

(b) Volume variance

(c) Price variance

(d) Quantity variance

(e) Standard costs

(f) Controllable variance

(g) Fixed budget

(h) Flexible budget

(i) Variance analysis

(j) Management by exception

__________ (1) The difference between the total budgeted overhead cost and the overhead

cost that was allocated to products using the predetermined fixed overhead rate.

__________ (2) A planning budget based on a single predicted amount of sales or production

volume; unsuitable for evaluations if the actual volume differs from the predicted volume.

__________ (3) Preset costs for delivering a product, component, or service under normal

conditions.

__________ (4) A process of examining the differences between actual and budgeted sales or

costs and describing them in terms of the amounts that resulted from price and quantity

differences.

__________ (5) The difference between actual and budgeted sales or cost caused by the

difference between the actual price per unit and the budgeted price per unit.

__________ (6) A budget prepared based on predicted amounts of revenues and expenses

corresponding to the actual level of output.

__________ (7) The difference between actual and budgeted cost caused by the difference

between the actual quantity and the budgeted quantity.

__________ (8) The combination of both overhead spending variances (variable and fixed)

and the variable overhead efficiency variance.

__________ (9) A management process to focus on significant variances and give less

attention to areas where performance is close to the standard.

__________ (10) The difference between actual cost and standard cost, made up of a price

variance and a quantity variance.

110. Presented below are terms preceded by letters a through h and followed by a list of

definitions 1 through 8. Enter the letter of the term with the definition, using the space

preceding the definition.

(a) Unfavorable variance

(b) Fixed budget performance report

(c) Overhead cost variance

(d) Budgetary control

(e) Spending variance

(f) Flexible budget performance report

(g) Quantity variance

(h) Favorable variance

__________(1) Difference in sales or costs, when the actual value is compared to the

budgeted value, that contributes to a lower income.

__________(2) A report that compares results with fixed budgeted amounts and identifies the

differences as favorable or unfavorable variances.

__________(3) The difference between the actual price of an item and its standard price.

__________(4) Difference in sales or costs, when the actual value is compared to the

budgeted value, that contributes to a higher income.

__________(5) Use of budgets by management to monitor and control the operations of a

company.

__________(6) Difference between actual quantity of an input and the standard quantity of

the input.

__________(7) Difference between the total overhead cost applied to products and the total

overhead cost actually incurred.

__________(8) A report that compares actual revenues and costs with their variable budgeted

amounts based on actual sales volume (or other level of activity) and identifies the differences

as variances.

111. Define standard costs. How do they assist management?

112. Explain variance analysis. Describe how variance analysis assists managers.

113. What are the four steps in the effective management of variance analysis?

114. Should both favorable and unfavorable variances be investigated, or only the unfavorable

ones? Explain.

115. Briefly describe the procedure of management by exception.

116. Identify and explain the primary differences between fixed and flexible budgets.

117. Identify the four steps in the budgetary control process.

118. Flexible budgets may be prepared before or after an actual period of activity. Why would

management prepare such budgets at differing time frames?

119. What are sales variances? How are they used?

23-6

120. Whistler Company determined that in the production of their products last period; they

had a favorable price variance and an unfavorable quantity variance for direct materials. What

might be the cause of this pattern of variances?

121. What are some causes of direct labor rate and efficiency variances?

122. What is the overhead volume variance? What would be the cause of a favorable volume

variance?

123. How are unfavorable variances recorded? How are favorable variances recorded?

23-8

Problems

124. Abrams, Inc., provides the following results of March’s operations:

Direct materials price variance ………….. $ 400F

Direct materials quantity variance ………. 2,000U

Direct labor rate variance ……………….. 100U

Direct labor efficiency variance …………. 1,200F

Variable overhead spending variance …… 400U

Variable overhead efficiency variance ….. 800F

Fixed overhead spending variance ………. 100U

Fixed overhead volume variance ………… 600F

Required:

(a) Determine the total overhead cost variance for March.

(b) Applying the management by exception approach, which of the variances shown are of

greatest concern? Why?

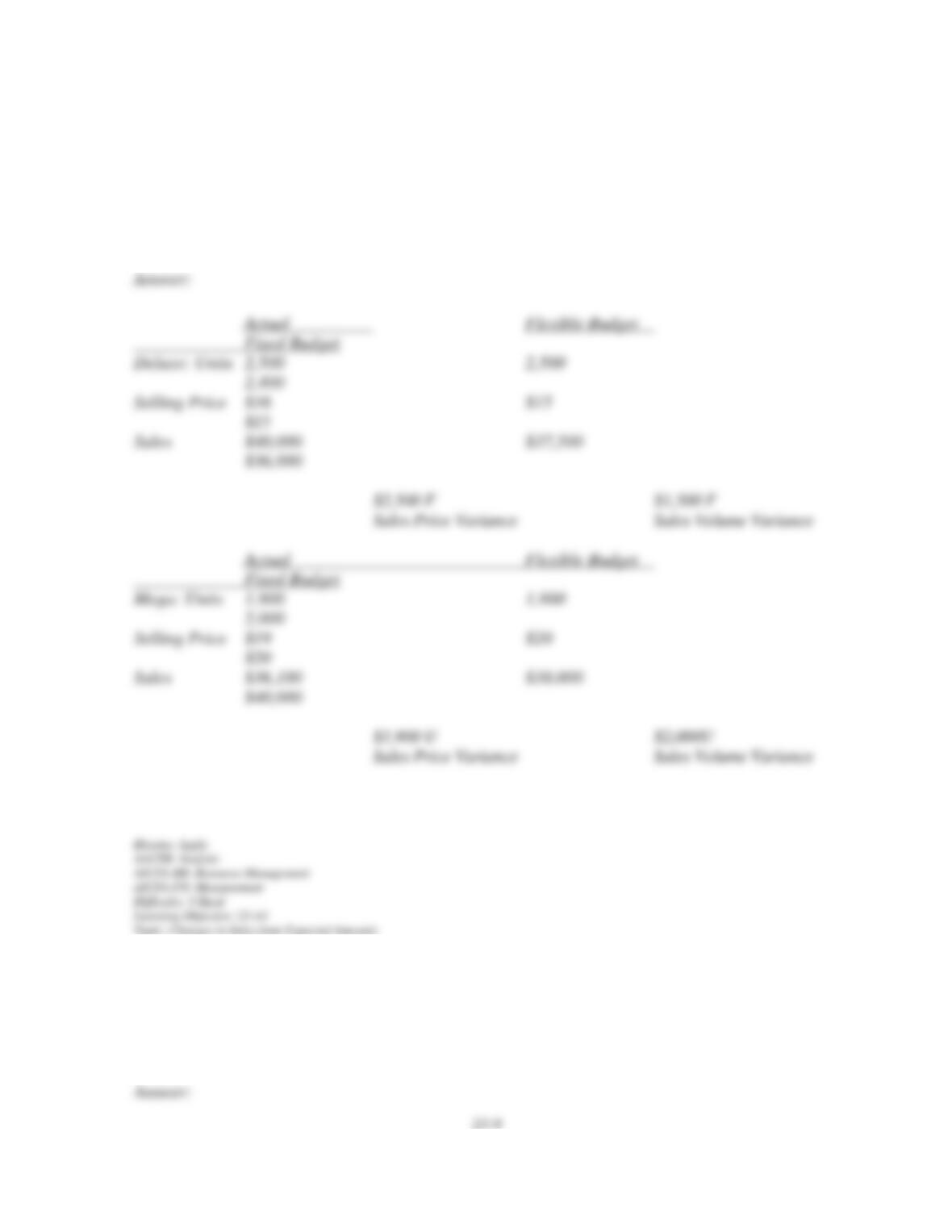

125. Stanton Co. produces and sells two lines of t-shirts, Deluxe and Mega. Stanton provides

the following data. Compute the sales price and the sales volume variances for each product.

Budget Actual

Unit sales price — Deluxe …. $15 $16

Unit sales price—Mega ……. $20 $19

Unit sales—Deluxe ………… 2,400 2,500

Unit sales—Mega ………….. 2,000 1,900

126. A company’s flexible budget for 60,000 units of production showed sales of $96,000,

variable costs of $36,000, and fixed costs of $26,000. What operating income would be

expected if the company produces and sells 70,000 units?

127. Based on predicted production of 25,000 units, Best Co. anticipates $175,000 of fixed

costs and $137,500 of variable costs. What are the flexible budget amounts of total costs for

20,000 and 30,000 units?

128. Casco Co. planned to produce and sell 40,000 units. At that volume level, variable costs

are determined to be $320,000 and fixed costs are $30,000. The planned selling price is $10

per unit. Casco actually produced and sold 42,000 units.

Using a contribution margin format:

(a) Prepare a fixed budget income statement for the planned level of sales and production.

(b) Prepare a flexible budget income statement for the actual level of sales and production.

129. A product has a sales price of $20. Based on a 15,000-unit production level, the variable

costs are $12 per unit and the fixed costs are $6 per unit. Using a flexible budget for an actual

production and sales level of 18,000 units, what is the budgeted operating income?

130. Thomas Co. provides the following fixed budget data for the year:

Sales (20,000 units) ……………………………. $600,000

Cost of sales:

Direct materials …………………………….. $200,000

Direct labor ………………………………… 160,000

Variable overhead ………………………….. 60,000

Fixed overhead …………………………….. 80,000 500,000

Gross profit ……………………………………. $100,000