Title: Problem 25-2A

QA_Ori:

Part 1

PROJECT Y

Net income $ 56,000

Title: Problem 25-2A

QA_Ori:

Part 3

PROJECT Y

*Average investment

PROJECT Z

*Average investment

Title: Problem 25-2A

QA_Ori:

Part 4

PROJECT Y

Present Value of Net Cash Flows

Present Present

Value of Value of

Net Cash

Flows

1 at 8%

Annuity

Net Cash

Flows

Years 1-4 $143,500 3.3121 $475,286

PROJECT Z

Present Value of Net Cash Flows

Present Present

Value of Value of

Net Cash

Flows

1 at 8%

Annuity

Net Cash

Flows

Years 1-3 $153,067 2.5771 $394,469

Amount invested (350,000)

Net present value $ 44,469

$56,000

$175,000*

$36,400

$175,000*

Part 5

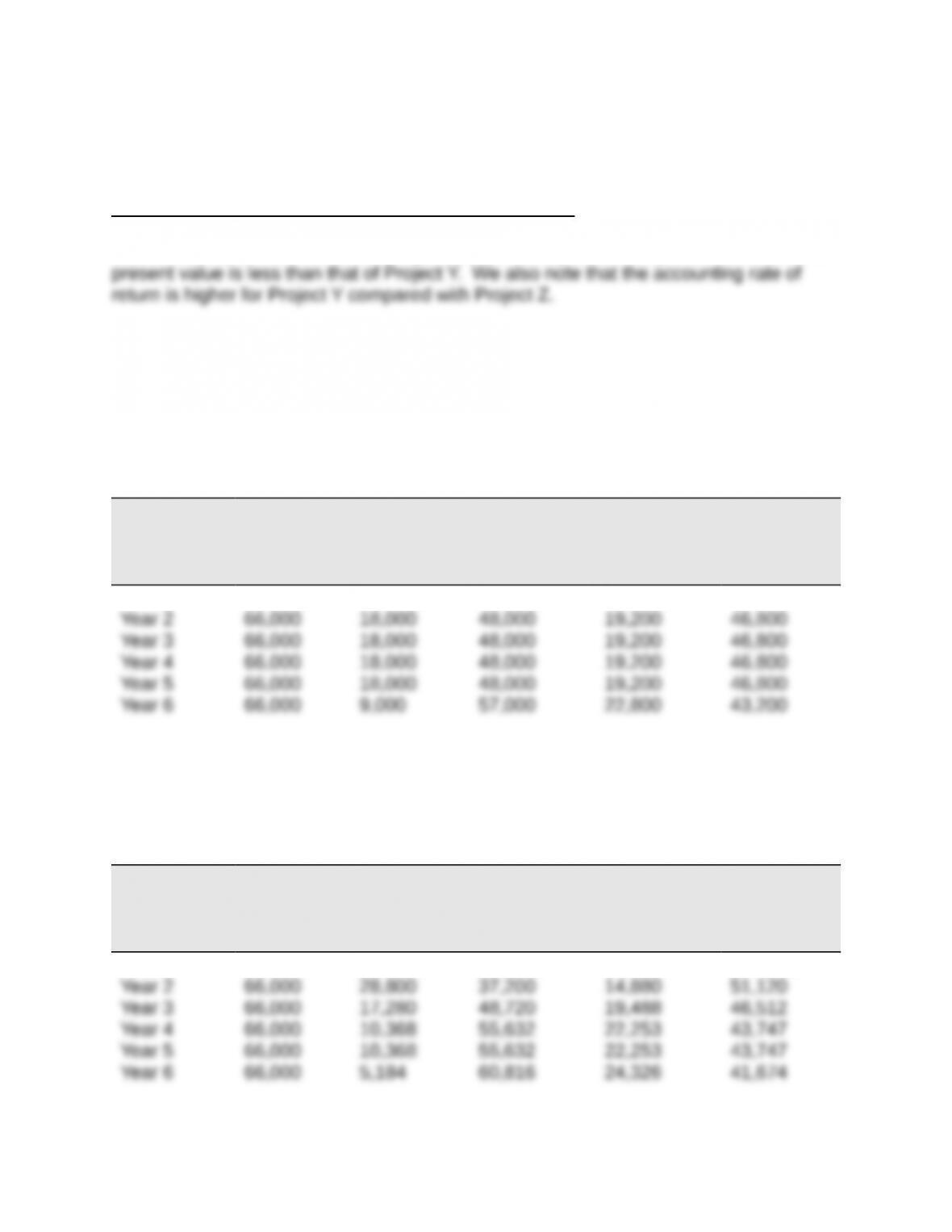

Recommendation to management is to pursue Project Y. This is because Project Y has

a positive net present value, which means that we expect it to earn at least 8% on our

cash investment in the machine. Project Z also has a positive net present value, but its

Title: Problem 25-3A

QA_Ori:

Part 1

RESULTS USING STRAIGHT-LINE DEPRECIATION

(a)

Income

Before

Deprec.

(b)

Straight-Line

Deprec.

(c)

Taxable

Income

(a) – (b)

(d)

40% Income

Taxes

(e)

Net Cash

Flows

(a) – (d)

Year 1 $66,000 $ 9,000 $57,000 $22,800 $43,200

Part 2

RESULTS USING MACRS DEPRECIATION

(a)

Income

Before

Deprec.

(b)

MACRS

Deprec.

(c)

Taxable

Income

(a) – (b)

(d)

40% Income

Taxes

(e)

Net Cash

Flows

(a) – (d)

Year 1 $66,000 $18,000 $48,000 $19,200 $46,800

Part 3

NET PRESENT VALUE OF ASSET USING STRAIGHT-LINE DEPRECIATION

Present

Present Value of

Net Cash

Flows

Value of

1 at 10%

Net Cash

Flows

Year 1 $ 43,200 0.9091 $ 39,273

Part 4

NET PRESENT VALUE OF ASSET USING MACRS DEPRECIATION

Present

Present Value of

Net Cash

Flows

Value of

1 at 10%

Net Cash

Flows

Year 1 $ 46,800 0.9091 $ 42,546

Part 5

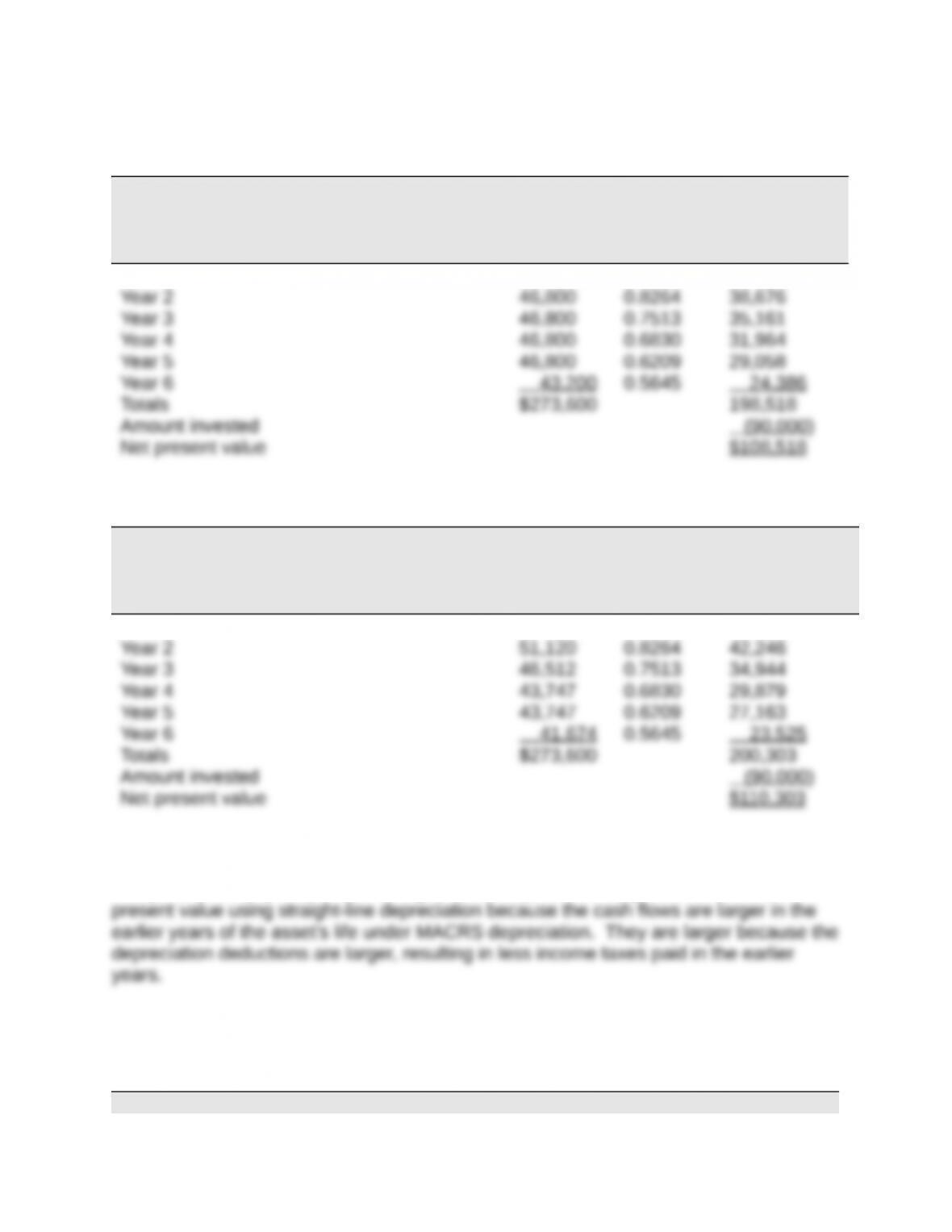

Analysis: The net present value using MACRS depreciation is greater than the net

Title: Problem 25-4A

QA_Ori:

JONES PRODUCTS

COMPARATIVE INCOME STATEMENTS

(1) (2) (3)

Normal New

Volume Business Combined

Sales $2,400,000 $260,000 $2,660,000

Costs and expenses

Direct materials 576,000 72,000 648,000

Supporting computations

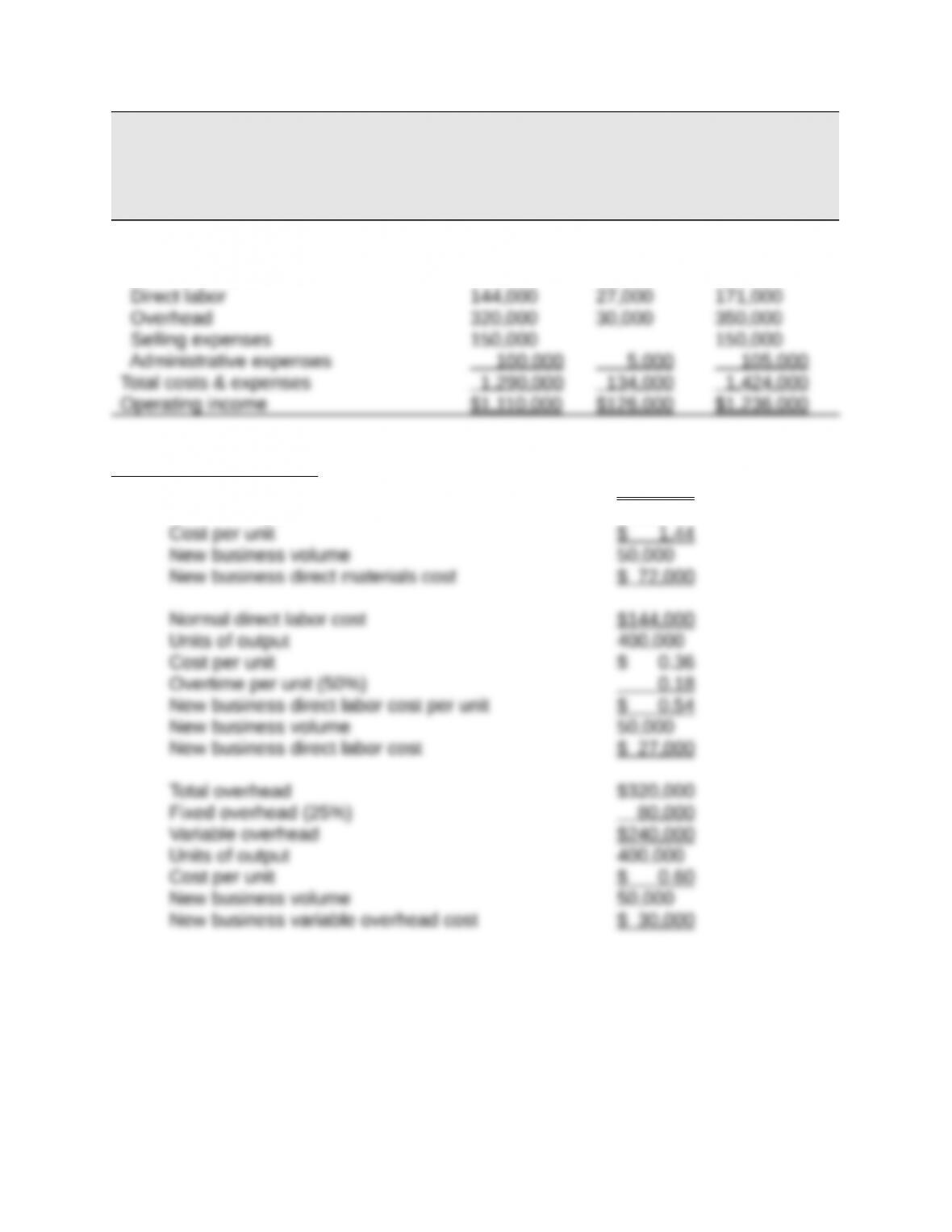

Normal direct materials cost $576,000

Units of output 400,000

Title: Problem 25-5A

QA_Ori:

Part 1

Product G Product B

Selling price per unit $120 $160

Variable costs per unit 40 90

Part 2

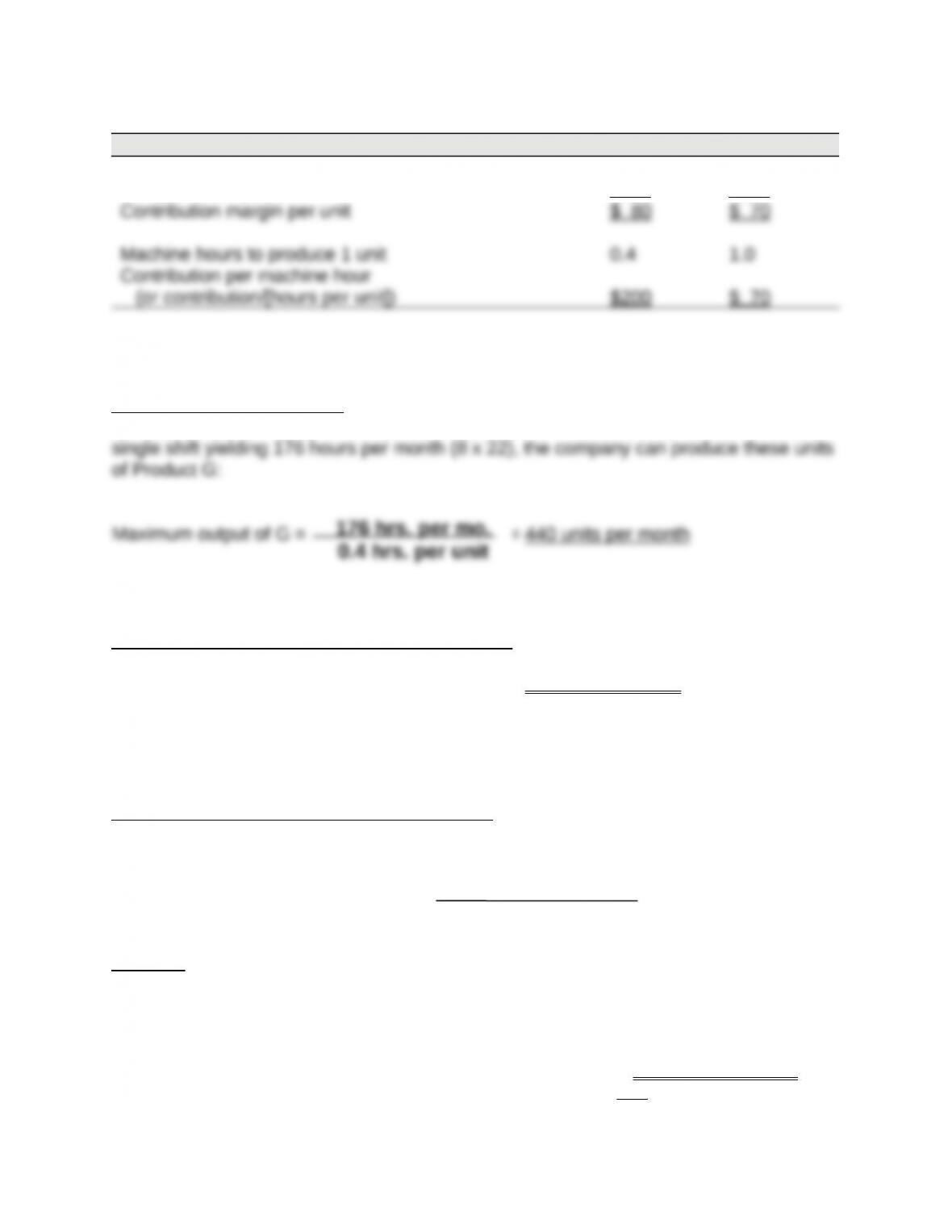

Sales Mix Recommendation. To the extent allowed by production and market

constraints, the company should produce as much of Product G as possible. With a

Contribution Margin at Recommended Sales Mix

Contribution margin = 440 units x $80 per unit = $35,200 per month

Part 3

Sales Mix Recommendation with Second Shift. If the second shift is added, the

maximum possible output of G will double

Maximum possible output of G = = 880 units per mo.

However, this level of output exceeds the company’s market constraint of 600 units of G

per month. This means the company should produce 600 units of Product G, and

commit the remainder of the productive capacity to Product B. This is computed as

follows

Units of Product G = 600 units per month

Hours per unit 0.4

352 hrs. per mo.

0.4 hrs. per unit

The output of Product B with 112 production hours is

Contribution Margin at This Sales Mix

Units Contr./unit Total

112 hrs. per mo.

From G 700 $80 $56,000

Management decision. This contribution margin of $34,040 is less than the contribution

margin of $40,840 generated under the existing market constraint (see part 3).

Therefore, the marginal benefits generated do not warrant the marketing efforts.