Problem 13-2B (Concluded)

Part 2

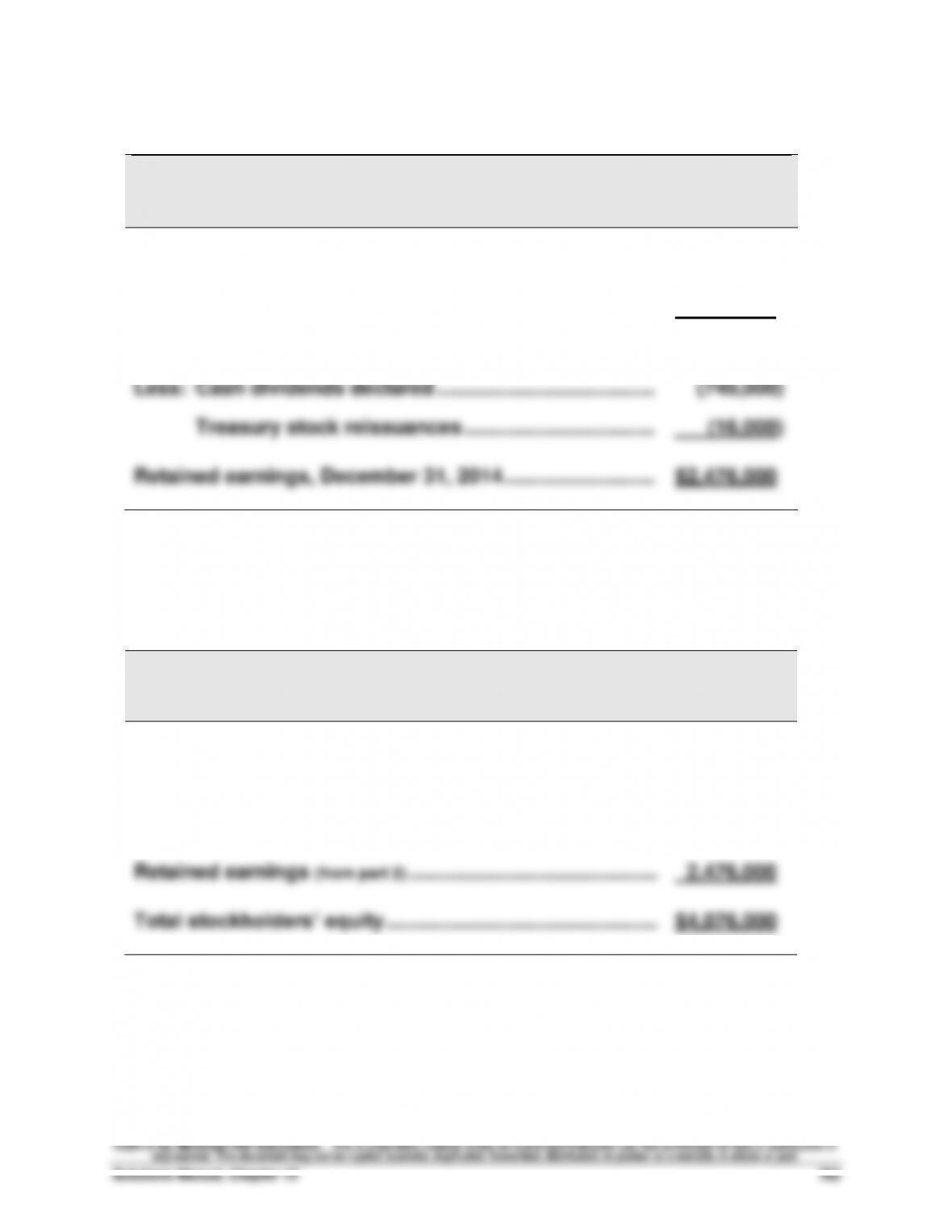

BALTHUS CORP.

Statement of Retained Earnings

For Year Ended December 31, 2014

Retained earnings, December 31, 2013 ……………………….

$2,160,000

Plus net income ………………………………………………………...

1,072,000

3,232,000

Less: Cash dividends declared ………………………………….

(740,000)

Treasury stock reissuances ……………………………..

(16,000)

Retained earnings, December 31, 2014 ……………………….

$2,476,000

Part 3

BALTHUS CORP.

Stockholders’ Equity Section of the Balance Sheet

December 31, 2014

Common stock⎯$1 par value, 320,000 shares

authorized, 200,000 shares issued and outstanding ….

$ 200,000

Paid in capital in excess of par value, common stock …

1,400,000

Retained earnings (from part 2) ………………………………………

2,476,000

Total stockholders’ equity ………………………………………….

$4,076,000

Problem 13-3B (45 minutes)

Part 1

Explanations for each of the journal entries

Jan. 17

Declared a cash dividend of $1 per share of common stock.

($96,000 / 96,000 shares)

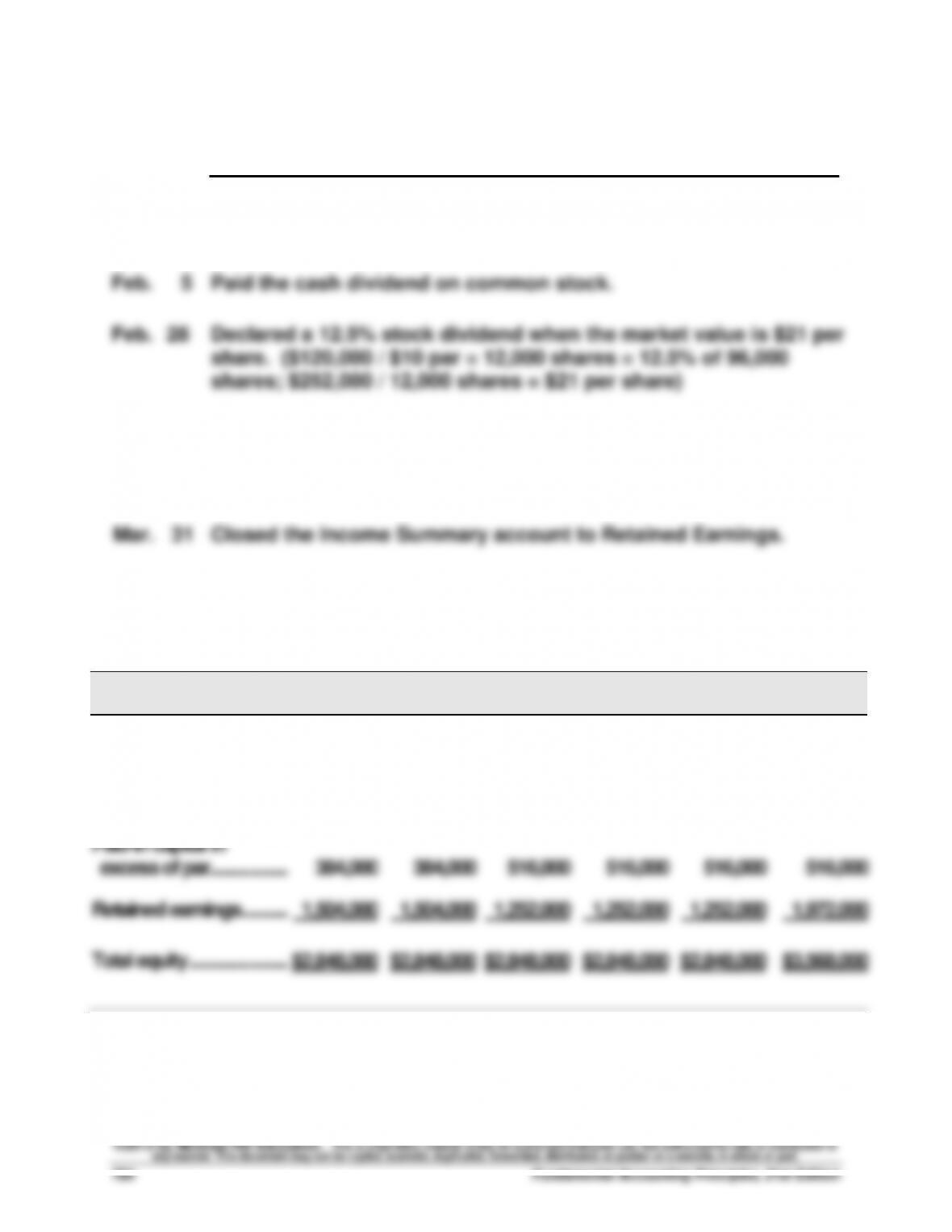

Feb. 5

Paid the cash dividend on common stock.

Feb. 28

Declared a 12.5% stock dividend when the market value is $21 per

share. ($120,000 / $10 par = 12,000 shares = 12.5% of 96,000

shares; $252,000 / 12,000 shares = $21 per share)

Mar. 14

Distributed the common stock dividend.

Mar. 25

Executed a 2-for-1 stock split. ($10 par / $5 par = 2-for-1 ratio)

Mar. 31

Closed the Income Summary account to Retained Earnings.

Part 2

Jan. 17

Feb. 5

Feb. 28

Mar. 14

Mar. 25

Mar. 31

Common stock ……………..

$ 960,000

$ 960,000

$ 960,000

$1,080,000

$1,080,000

$1,080,000

Common stock

dividend distributable ….

0

0

120,000

0

0

0

Paid–in capital in

excess of par………………..

384,000

384,000

516,000

516,000

516,000

516,000

Retained earnings ………...

1,504,000

1,504,000

1,252,000

1,252,000

1,252,000

1,972,000

Total equity …………………….

$2,848,000

$2,848,000

$2,848,000

$2,848,000

$2,848,000

$3,568,000

Problem 13-4B (45 minutes)

Part 1

Outstanding common shares

Feb. 15

May 15

Aug. 15

Nov. 15

Beginning balance ………………………

17,000

17,000

17,000

17,000

Less treasury stock (Mar. 2) …………

(1,000)

(1,000)

(1,000)

Plus dividend shares (Oct. 4)* ………

______

______

______

2,000

Outstanding shares …………………..…

17,000

16,000

16,000

18,000

*(12.5% x 16,000)

Part 2

Cash dividend amounts

Feb. 15

May 15

Aug. 15

Nov. 15

Outstanding shares …………………..…

17,000

16,000

16,000

18,000

Dividend per share ………………………

$ 0.40

$ 0.40

$ 0.40

$ 0.40

Total dividend …………………………..

$6,800

$6,400

$6,400

$7,200

Part 3

Capitalization of retained earnings for small stock dividend

Number of shares ……………………………………………..………..

2,000

Market value per share ……………………………………..………………..

$ 42

Total capitalized ……………………………………………….………

$ 84,000

Part 4

Cost per share of treasury stock

Total amount paid …………………………………………….…………

$ 40,000

Shares purchased …………………………………………….…………

1,000

Cost per share ………………………………………………….……

$ 40

Part 5

Net income

Retained earnings, beginning balance ……………..……………

$270,000

Less dividends: Feb. 15 ………………………………….……………………

(6,800)

May 15 ………………………………….……………………

(6,400)

Aug. 15 ……………………………………………………….

(6,400)

Oct. 4 ……………………………………………………….

(84,000)

Nov. 15 ………………………………….……………………

(7,200)

Total before net income ……………………………………………………….

$159,200

Plus net income ……………………………………………….………

?

Retained earnings, ending balance …………………..………

$295,200

Problem 13-5B (40 minutes)

1. Market price = $90 per share (current stock exchange price given)

2. Computation of stock par values

3. Book values with no dividends in arrears

Book value per preferred share = par value (when not callable)

= $ 250

Common stock

Total equity…………………………..……………

$2,400,000

Less equity for preferred ……………………

(375,000)

Common stock equity ……………………..…

$2,025,000

Number of outstanding shares ………..…

18,000

Book value per common share ………..…

$ 112.50

($2,025,000 / 18,000)

4. Book values with two years’ dividends in arrears

Preferred stock

Preferred stock par value …………………..

$ 375,000

Plus two years’ dividends in arrears* ....

60,000

Preferred equity ………………………………...

$ 435,000

*2 years’ dividends = 2 x ($375,000 x 8%) = $60,000

Number of outstanding shares …………..

1,500

Book value per preferred share ………....

$ 290.00

($435,000 / 1,500)

Common stock

Total equity…………………………..…………...

$2,400,000

Less equity for preferred …………………...

(435,000)

Common stock equity ………………………..

$1,965,000

Number of outstanding shares …………..

18,000

Book value per common share …………..

$ 109.17

($1,965,000 / 18,000) rounded

Problem 13-5B (Concluded)

5. Book values with call price and two years’ dividends in arrears

Preferred stock

Preferred stock call price (1,500 x $280)

$ 420,000

Plus two years’ dividends in arrears* ……….

60,000

Preferred equity ………………………………………

$ 480,000

*2 years’ dividends = 2 x ($375,000 x 8%) = $60,000

Number of outstanding shares ………………..

1,500

Book value per preferred share ……………….

$ 320.00

($480,000/1,500)

Common stock

Total equity…………………………..…………………

$2,400,000

Less equity for preferred …………………………

(480,000)

Common stock equity ……………………………..

$1,920,000

Number of outstanding shares ………………..

18,000

Book value per common share ………………..

$ 106.67

($1,920,000/18,000) rounded

6. Dividend allocation in total

Preferred

Common

Total

2 years’ dividends in arrears …

$ 60,000

$ 0

$ 60,000

Current year dividends ………….

30,000

—

30,000

Remainder to common ………….

—

10,000

10,000

Totals ……………………………………

$ 90,000

$ 10,000

$100,000

Dividends per share for the common stock

7. Equity represents the residual interest of owners in the assets of the

business after subtracting claims of creditors. With few exceptions, these

SERIAL PROBLEM — SP 13

Serial Problem — SP 13, Success Systems (25 minutes)

1a. Journal entry for issuance of common stock to Cicely

Cash ……………………………………………………………..……….

86,000

Common Stock ………………………………………..……….

86,000

Issuance of common stock.

1b. Journal entry for issuance of preferred stock to Marcello

Cash ……………………………………………………………..……….

86,000

Preferred Stock ………………………………………..……….

86,000

Issuance of $100 par 7% preferred stock.

1c. Journal entry to record $86,000 borrowed from the bank

Cash ……………………………………………………………..……….

86,000

Notes Payable ………………………………………….……….

86,000

Borrowed $86,000 on a 10-year, 7% note payable

2. Evaluation of the three proposals

a. Cicely’s investment as a common shareholder would mean that

Adria would have a second person who would be an owner. Adria

has been working on her own business for about 15 months, and

may not wish to have a second person who may have authority to

Serial Problem (concluded)

b. Having a preferred shareholder means that Adria’s Uncle Marcello

will not have the same voting rights as Adria. Marcello may be

expecting regular dividends, however, so Adria should be prepared

wishes to be a preferred shareholder.

c. The loan requires regular monthly payments, so Adria will need to

budget the $1,000 each month as a cash outflow. The loan may be

Reporting in Action — BTN 13-1

(All shares in thousands.)

1. As of December 31, 2011, the shares of common stock issued and

68,468.

The weighted-average common shares used in calculating earnings per

share are disclosed on the Statement of Income. At December 31, 2011,

share repurchases, issuances, and retirements.)

2. Total stockholders’ equity as of December 31, 2011 ……. $500,056,000

can be considered to represent the book value of the common stock.

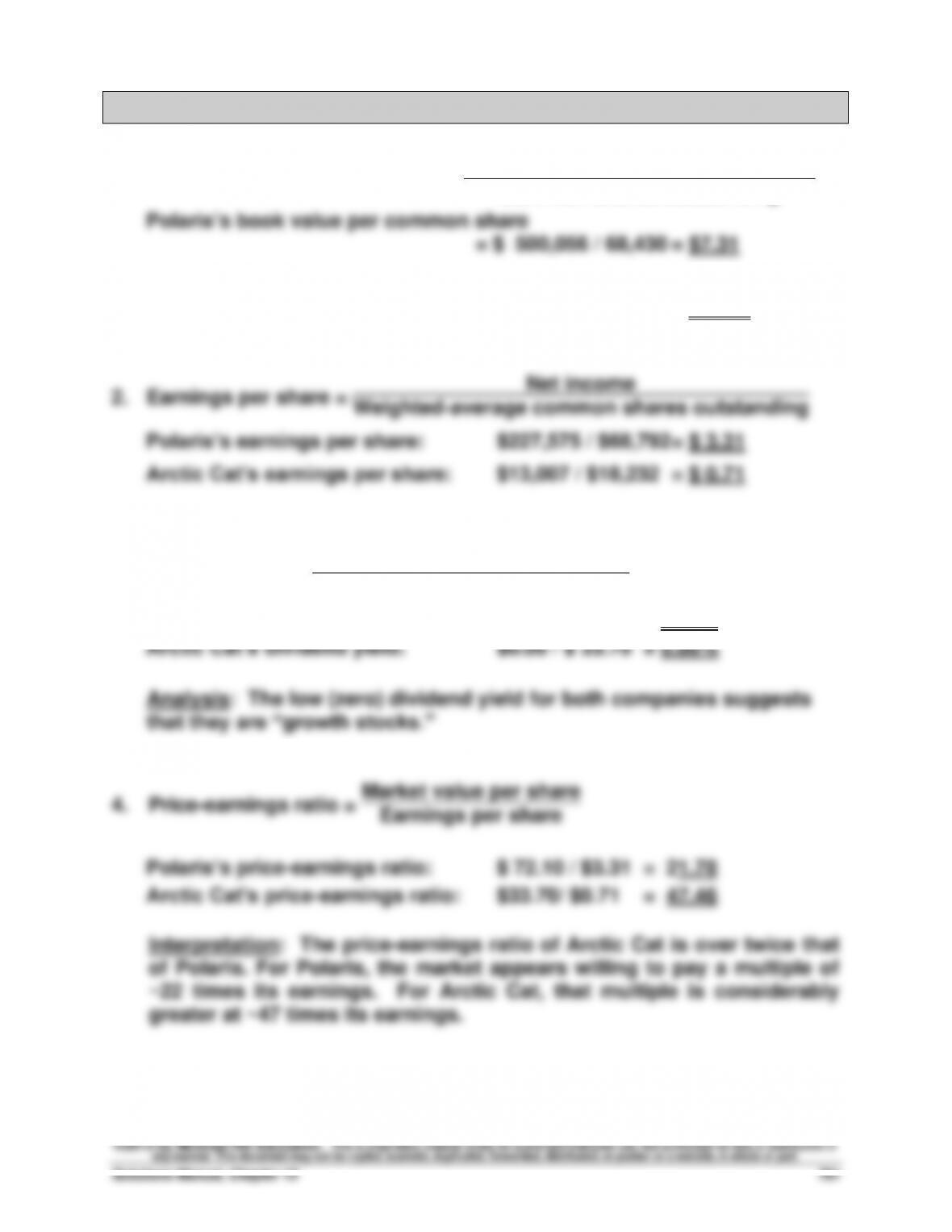

4. Polaris’s income statement reports the following

2011

2010

2009

Basic earnings per common share …………….. $3.31 $2.20 $1.56

5. Polaris’s consolidated balance sheet reports no shares of treasury stock

in 2011 and 2010.

Comparative Analysis — BTN 13-2

1. Book value per common share = Equity applicable to common shares

Common shares outstanding

Arctic Cat’s book value per common share

= $183,036 / 18,301 = $10.00

3. Dividend yield = Annual cash dividends per share

Market value per share

Polaris’s dividend yield: $0.90 / $ 72.10 = 1.25%

Ethics Challenge — BTN 13-3

During the course of her duties, Harriet has learned information that others

might not know. If she uses this information to trade in New World

Communicating in Practice — BTN 13-4

There is no set solution to this activity. Solutions will vary based on the

industry and the companies selected.

Taking It to the Net — BTN 13-5

1. The balance sheet of McDonald’s shows that they have both preferred

and common stock authorized, but it has only issued common stock.

2. The preferred stock has no par value. There are 165.0 million preferred

Teamwork in Action — BTN 13-6

1. The team statement should include the following:

a. When a corporation “buys back” its stock (engages in a treasury

b. Reasons for “buybacks”:

• to use shares to acquire another corporation.

2. The team should establish the acquisition entry as follows

Treasury Stock, Common ……………………………..……

13,400

Cash ……………………………………………………….

13,400

Reacquired 100 shares of $100 par value

common stock at a cost of $134 per share.

Each member should prepare one of the following reissue entries:

a.

Cash ………………………………………………………………………………

13,400

Treasury Stock, Common ……………………….….

13,400

Received $134 per share for 100 treasury

shares costing $134 per share.

b.

Cash ………………………………………………………………………………

15,000

Paid-In Capital, Treasury Stock ……………….………….

1,600

Treasury Stock, Common ……………………….….

13,400

c.

Cash ………………………………………………………………………………

12,000

Paid-In Capital, Treasury Stock …………………….…….

1,400

Treasury Stock, Common ……………………….….

13,400

Teamwork in Action (Continued)

d.

Cash ………………………………………………………………………………

12,000

Paid-In Capital, Treasury Stock …………………….…….

1,000

Retained Earnings ………………………………………..……………..

400

Treasury Stock, Common ……………………….….

13,400

Received $120 per share for 100 treasury

shares costing $134 per share.

e.

Cash ………………………………………………………………………………

12,000

Retained Earnings ………………………………………..……………..

1,400

Treasury Stock, Common ……………………….….

13,400

Received $120 per share for 100 treasury

shares costing $134 per share.

3. When presenting and explaining the above entries to the team, the

following points should be made by the team members:

The similarities in all reissue entries a through e are:

• The net affect of the transaction is to increase assets and equity by

the amount received on reissue.

The differences in reissue entries b through e are:

(b) Reissuing above cost creates additional Paid-In Capital.*

Entrepreneurial Decision — BTN 13-7

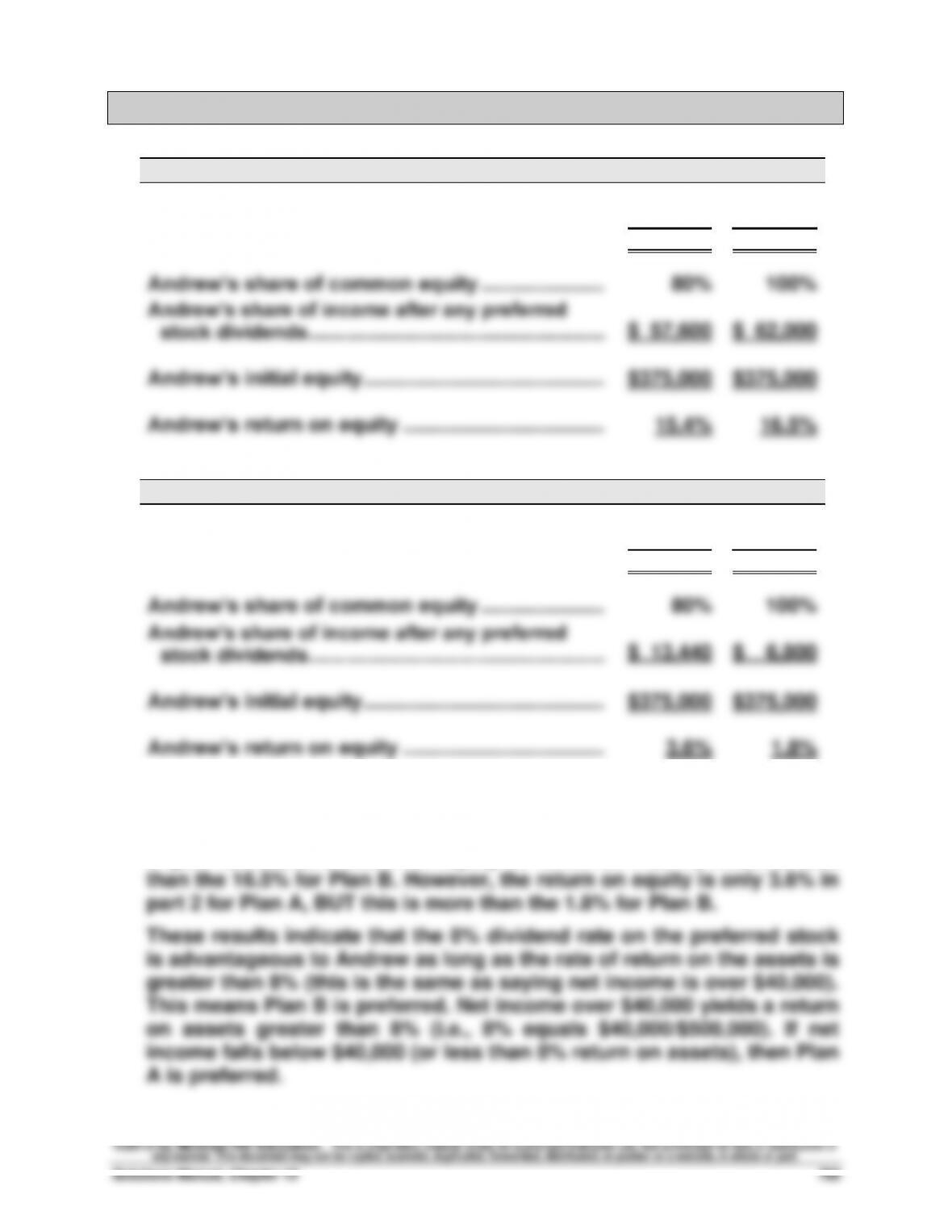

1.

Plan A

Plan B

Net income ……………………………………………………..

$ 72,000

$ 72,000

Less preferred dividends ………………………………..

0

(10,000)

Net income for common stockholders …………….

$ 72,000

$ 62,000

Andrew’s share of common equity ………………….

80%

100%

Andrew’s share of income after any preferred

stock dividends ……………………………………………….

$ 57,600

$ 62,000

Andrew’s initial equity …………………………………….

$375,000

$375,000

Andrew’s return on equity ………………………………

15.4%

16.5%

2.

Plan A

Plan B

Net income ……………………………………………………..

$ 16,800

$ 16,800

Less preferred dividends ………………………………..

0

(10,000)

Net income for common stockholders …………….

$ 16,800

$ 6,800

Andrew’s share of common equity ………………….

80%

100%

Andrew’s share of income after any preferred

stock dividends ……………………………………………….

$ 13,440

$ 6,800

Andrew’s initial equity …………………………………….

$375,000

$375,000

Andrew’s return on equity ………………………………

3.6%

1.8%

3. The difference between the answers for parts 1 and 2 arises from the

percent of return generated with the assets invested in the corporation.

In part 1, Andrew’s return on equity is 15.4% for Plan A, which is less

Hitting the Road — BTN 13-8

There is no formal solution for this field activity. Students often find this

assignment interesting as it highlights the relevance of their accounting

Global Decision — BTN 13-9

1. Book value per common share = Equity applicable to common shares

Common shares outstanding

$1.24. This means that KTM’s BVPS is about $25.93, and its EPS is about $2.46)

3. KTM’s EPS is €1.98, and its statement of changes in shareholders’

equity reports that KTM declared no cash dividends during 2011.