Chapter 20

Process Cost Accounting

QUESTIONS

1. The main deciding factor in choosing between a job order costing system or a

process costing system is the type of product or service. Examples where a

2. The main focus in process costing is the production department (process).

3. Yes, services can be delivered by processes. For example, Federal Express delivers

4. The journal entries to match cost flows with product flows are primarily the same

for both process costing and job order costing. In process costing, the materials

5. A materials consumption report is an alternative control document.

6. The computation of equivalent units of production focuses on converting partially

completed units to a measure in terms of completed units. We need to use EUP

7. The two main methods of process costing are the weighted-average and the first-in,

first-out (FIFO) methods. The weighted-average method considers “average flow”

Fundamental Accounting Principles, 21st Edition

1134

8. A process cost accounting system treats labor that is used entirely within one

9. Direct labor costs flow first from the Factory Payroll account to the Goods in

10. After all labor costs have been allocated to Goods in Process Inventory accounts

and/or Factory Overhead, the Factory Payroll account should have a zero balance.

11. Yes, it is possible to have either underapplied or overapplied overhead in a process

12. Equivalent units for direct materials differ from that for direct labor (and overhead) if

direct materials and direct labor (and overhead) are added at different stages in the

13. The four steps in accounting for production activity (for process operations) are: 1)

14. The process cost summary serves at least three purposes: (a) to help department

managers control their departments; (b) to help factory managers evaluate

15. Yes. Polaris might use process costing to determine the cost of manufacturing a

16. Likely processing steps for the snowmobiles include making the frame, assembly,

QUICK STUDIES

Quick Study 20-1 (5 minutes)

1. Job order operation

2. Process operation

3. Process operation

4. Job order operation

Quick Study 20-2 (10 minutes)

1.

Raw Materials Inventory ………………………………………..

62,000

Cash ………………………………………………………………..

62,000

Purchase of raw materials inventory.

2.

Goods in Process Inventory …………………………………..

50,000

Raw Materials Inventory …………………………………..

50,000

Direct materials used in production.

Quick Study 20-3 (10 minutes)

1.

Factory Payroll ………………………………………………….…..

135,000

Cash ………………………………………………………………..

135,000

To record factory payroll costs.

2.

Goods in Process Inventory …………………………………..

125,000

Factory payroll …………………………………………….…..

125,000

Direct labor used in production.

Fundamental Accounting Principles, 21st Edition

1136

Quick Study 20-4 (15 minutes)

1.

Factory Overhead ……………………………………………..…..

9,000

Raw Materials Inventory …………………………………..

9,000

To record indirect materials used in production.

2.

Factory Overhead ……………………………………………..…..

10,000

Factory Payroll …………………………………………….…..

10,000

To record indirect labor used in production.

3.

Factory Overhead ……………………………………………..…..

156,000

Other accounts …………………………………………..…..

156,000

To record other overhead costs.

4.

Goods in Process Inventory …………………………………..

175,000

Factory Overhead ……………………………………….…..

175,000

To record overhead applied ($125,000 x 140%).

Quick Study 20-5 (10 minutes)

Finished Goods Inventory ……………………………………..

275,000

Goods in Process Inventory …………………………..

275,000

Transfer of goods from production.

Quick Study 20-6 (10 minutes)

Equivalent units under the weighted-average method

Equivalent

EUP for Labor

Units

Units completed and transferred out (340,000 x 100%) …………………

340,000

Units of ending goods in process

Labor (120,000 x 25%) ………………………………………………………………

30,000

Equivalent units of production …………………………………………………….

370,000

Quick Study 20-7 (5 minutes)

The cost of beginning inventory plus the costs added during the period

Quick Study 20-8 (10 minutes)

The auto garage can use a process cost system for routine, repetitive

Quick Study 20-9 (15 minutes)

Equivalent units under the FIFO method

Equivalent

EUP for Labor

Units

Equivalent units to complete beginning work in process

(150,000 x 20%) ……………………………………………………….……………………..

30,000

Equivalent units started and completed* …………………………………………..

190,000

Equivalent units in ending goods in process (120,000 x 25%) ….………..

30,000

Total equivalent units of production ………………………………………..………..

250,000

* Units completed – Units in beginning work in process = Units started and completed

340,000 – 150,000 = 190,000

Quick Study 20-10 (5 minutes)

Quick Study 20-11 (5 minutes)

The process cost summary sections are Costs Charged to Production,

Equivalent Units of Production, and Cost Assignment and Reconciliation.

Quick Study 20-12 (5 minutes)

If the company is successful in reducing water usage, its raw materials

cost (water) should decline. Likewise, assuming water used in its cleaning

Quick Study 20-13 (5 minutes)

Quick Study 20-14 (10 minutes)

Equivalent units under the weighted-average method

Equivalent

EUP for Labor

Units

Units completed and transferred out (680,000 x 100%) …………………

680,000

Units of ending goods in process

Direct labor (240,000 x 75%) ……………………………………………………..

180,000

Equivalent units of production …………………………………………………….

860,000

Quick Study 20-15 (15 minutes)

Equivalent units under the FIFO method

Equivalent

EUP for Labor

Units

Equivalent units to complete beginning work in process

(320,000 x 75%) ……………………………………………………….……………………..

240,000

Equivalent units started and completed* …………………………………………..

360,000

Equivalent units in ending goods in process (240,000 x 75%) ….………..

180,000

Total equivalent units of production ………………………………………..………..

780,000

* Units completed – Units in beginning work in process = Units started and completed

680,000 – 320,000 = 360,000

EXERCISES

Exercise 20-1 (10 minutes)

Exercise 20-2 (25 minutes)

1.

Raw Materials Inventory …………………………………..……

80,000

Accounts Payable ……………………………………………

80,000

Purchased materials on credit.

2.

Goods in Process Inventory ……………………………..……

42,000

Raw Materials Inventory ……………………………..……

42,000

Used direct materials in production.

3.

Factory Overhead …………………………………………….……

22,500

Raw Materials Inventory ……………………………..……

22,500

Used indirect materials.

Exercise 20-3 (10 minutes)

1.

Factory Payroll ………………………………………………..……

95,000

Cash ………………………………………………………….……

95,000

Incurred direct labor costs.

2.

Goods in Process Inventory ……………………………..……

75,000

Factory Payroll …………………………………………..……

75,000

Used direct labor in production.

3.

Factory Overhead …………………………………………….……

20,000

Factory Payroll …………………………………………..……

20,000

Used indirect labor in production.

Fundamental Accounting Principles, 21st Edition

1140

Exercise 20-4 (5 minutes)

1.

Factory Overhead …………………………………………….……

38,750

Cash ………………………………………………………….……

38,750

Incurred overhead costs.

2.

Goods in Process Inventory ……………………………..……

82,500

Factory Overhead ……………………………………….……

82,500

Applied overhead: $75,000 x 110%

Exercise 20-5 (5 minutes)

1.

Finished Goods Inventory ………………………………………

135,600

Goods in Process Inventory ………………………..…

135,600

Transfer goods from production to finished goods.

2.

Accounts Receivable ………………………………………..……

315,000

Sales …………………………..……………………………………

315,000

Sale of goods on credit.

Cost of Goods Sold …………………………………………..……

175,000

Finished Goods Inventory …………………………………

175,000

Record cost of goods sold.

Exercise 20-6 (25 minutes)

1.

Oct. 31

Goods in Process Inventory …………………………..

522,000

Raw Materials Inventory …………………………..

522,000

Direct materials used in production.

2.

Oct. 31

Goods in Process Inventory …………………………..

130,000

Factory Payroll ……………………………………….……….

130,000

Direct labor used in production.

3.

Oct. 31

Goods in Process Inventory …………………………..

227,500

Factory Overhead …………………………………………….

227,500

Overhead applied: $130,000 x 175%

Exercise 20-6 (continued)

4.

Oct. 31

Finished Goods Inventory …………………………….……….

595,000

Goods in Process Inventory …………………….…….

595,000

Transfer goods from production to finished

goods.

5.

Oct. 31

Accounts Receivable …………………………………….……….

950,000

Sales ……………………………………………………….

950,000

Sales on credit.

Oct. 31

Cost of Goods Sold …………………………..………….……….

540,000

Finished Goods Inventory ……………………….….

540,000

Record cost of sales.

Exercise 20-7 (25 minutes)

a. Purchased raw materials on credit at a cost of $52,000.

b. Used direct materials costing $42,000 in production.

j. Sold products on credit for $250,000. Their accumulated cost is

$100,000.

Fundamental Accounting Principles, 21st Edition

1142

Exercise 20-8 (20 minutes)

1.

Units in beginning inventory …………………………………..

60,000

Units started and completed …………………………………..

240,000

Total units transferred to finished goods ………………..

300,000

2.

Equivalent units of production – weighted average

Equivalent Units of Production

Direct

Direct

Materials

Labor

Units completed & transferred out (300,000 x 100%) ………..

300,000

300,000

Units of ending goods in process

Direct materials, 82,000 x 80% ……………………………….……..

65,600

Direct labor, 82,000 x 30% ……………………………………..……..

_______

24,600

Equivalent units of production ………………………………………..

365,600

324,600

Exercise 20-9 (25 minutes)

1.

Cost per equivalent unit – Weighted average

Direct

Materials

Direct

Labor

Costs of beginning goods in process ………………………

$118,840

$ 47,890

Costs incurred this period ……………………………………….

850,000

650,000

Total costs ……………………………………………………………..

$968,840

$697,890

÷ Equivalent units of production (from Ex. 20–8) ………

365,600

324,600

Cost per equivalent unit of production …………………….

$2.65 per

EUP

$2.15 per

EUP

2. Cost Assignment and Reconciliation – weighted average

Costs of units transferred out

Direct materials (300,000 EUP x $2.65 per EUP) ……

$795,000

Direct labor (300,000 EUP x $2.15 per EUP) ………….

645,000

Total costs transferred out ……………………………………..

$1,440,000

Costs of ending goods in process

Direct materials (65,600 EUP x $2.65 per EUP) ……..

173,840

Direct labor (24,600 EUP x $2.15 per EUP) ……………

52,890

Total costs of ending goods in process ………………….

226,730

Total costs accounted for* ……………………………………..

$1,666,730

*Equals costs to account for of $1,666,730 ($968,840 + $697,890)

Exercise 20-10 (20 minutes)

Equivalent units of production—FIFO

Direct

Direct

Equivalent units of production

Materials

Labor

Units to complete beginning goods in process

Direct materials (60,000 x 40%) …………………………...

24,000

Direct labor (60,000 x 60%) ………………………………….

36,000

Units started and completed …………………………………

240,000

240,000

Units in ending work in process

Direct materials (82,000 x 80%) …………………………...

65,600

Direct labor (82,000 x 30%) ………………………………….

_______

24,600

Equivalent units of production ……………………………..

329,600

300,600

Fundamental Accounting Principles, 21st Edition

1144

Exercise 20-11 (25 minutes)

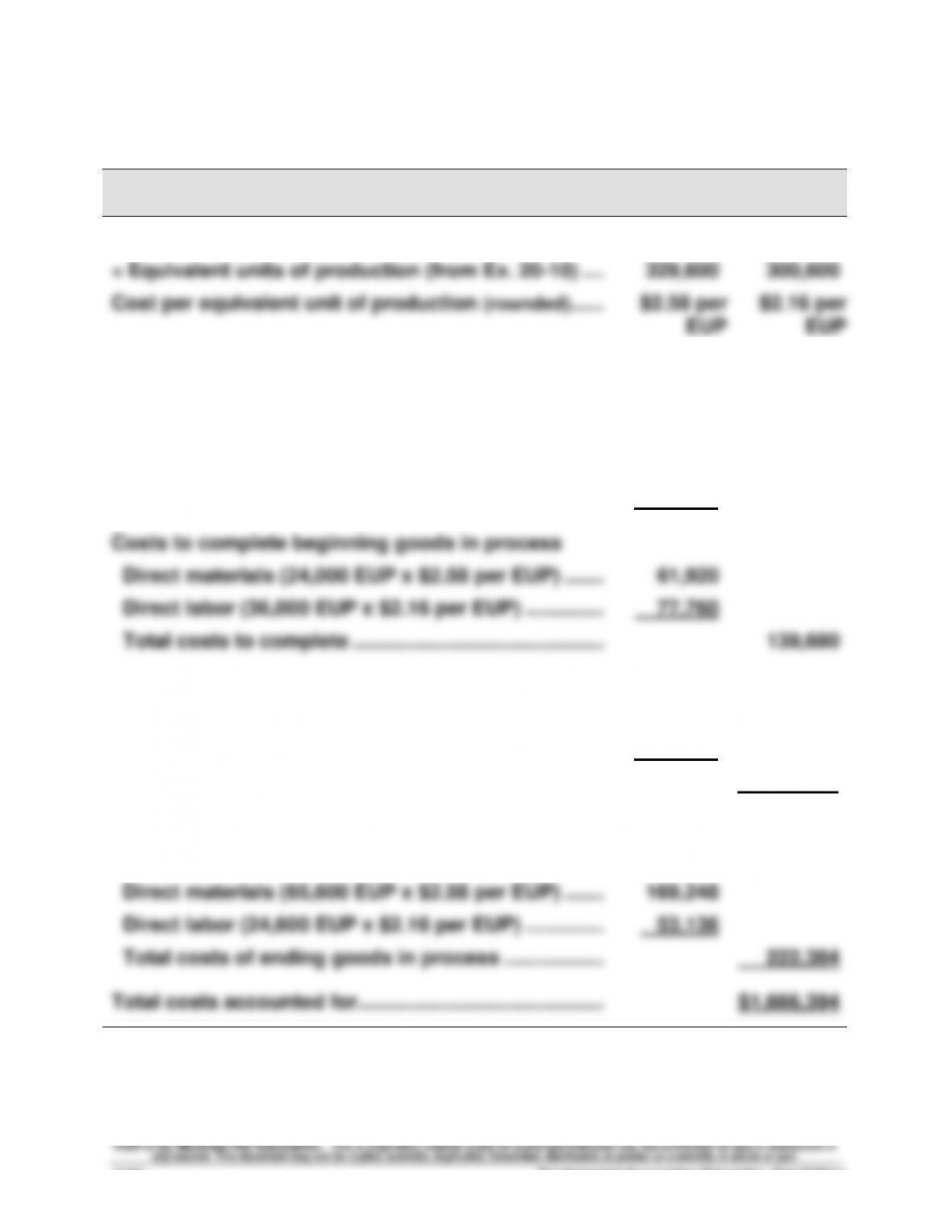

1. Cost per equivalent unit of direct materials and direct labor—FIFO

Direct

Direct

Materials

Labor

Costs incurred this period …………………………………….

$850,000

$650,000

÷ Equivalent units of production (from Ex. 20–10) ….

329,600

300,600

Cost per equivalent unit of production (rounded) ……

$2.58 per

EUP

$2.16 per

EUP

2. Assignment of costs to output of department—FIFO

Costs of goods transferred out

Cost of beginning goods in process inventory

Direct materials ………………………………………………….

$118,840

Direct labor ………………………………………………………..

47,890

$ 166,730

Costs to complete beginning goods in process

Direct materials (24,000 EUP x $2.58 per EUP) …….

61,920

Direct labor (36,000 EUP x $2.16 per EUP) …………..

77,760

Total costs to complete ………………………………………

139,680

Cost of units started and completed this period

Direct materials (240,000 EUP x $2.58 per EUP) …..

619,200

Direct labor (240,000 EUP x $2.16 per EUP) …………

518,400

Total cost of units started and completed ……………

1,137,600

Total costs of goods transferred out……………………..

1,444,010

Cost of ending goods in process inventory

Direct materials (65,600 EUP x $2.58 per EUP) …….

169,248

Direct labor (24,600 EUP x $2.16 per EUP) …………..

53,136

Total costs of ending goods in process ………………

222,384

Total costs accounted for ……………………………………..

$1,666,394

*Equals costs to account for of $1,666,730 after a rounding difference of $336.

Exercise 20-12 (30 minutes)

1. Beginning inventory is 100% complete with respect to materials.

Ending inventory is 100% complete with respect to materials.

EUP for Materials

Goods completed (80,000 EUP x 100%) ………………………………

80,000

Ending goods in process (16,000 EUP x 100%) ……………………

16,000

Total EUP …………………………………………………………………………..

96,000

2. Beginning inventory is 50% complete with respect to materials.

Ending inventory is 75% complete with respect to materials.

Units of

EUP for Materials

Product

Goods completed (80,000 EUP x 100%) ………………………………

80,000

Ending goods in process (16,000 EUP x 75%) ……………………..

12,000

Total EUP …………………………………………………………………………..

92,000

3. Beginning inventory is 50% complete with respect to materials.

Ending inventory is 50% complete with respect to materials.

Units of

EUP for Materials

Product

Goods completed (80,000 EUP x 100%) ………………………………

80,000

Ending goods in process (16,000 EUP x 50%) ……………………..

8,000

Total EUP …………………………………………………………………………..

88,000

Fundamental Accounting Principles, 21st Edition

1146

Exercise 20-13 (30 minutes)

1. Beginning inventory is 100% complete with respect to materials.

Ending inventory is 100% complete with respect to materials.

EUP for Materials

To complete beginning work in process (24,000 EUP x 0%) …..….

0

Units started and completed (56,000 EUP x 100%) ………………..….

56,000

Ending goods in process (16,000 EUP x 100%) ……………………..….

16,000

Total EUP …………………………………………………………………………….….

72,000

2. Beginning inventory is 50% complete with respect to materials.

Ending inventory is 75% complete with respect to materials.

Units of

EUP for Materials

Product

To complete beginning work in process (24,000 EUP x 50%) …….

12,000

Units started and completed (56,000 EUP x 100%) ………………..….

56,000

Ending goods in process (16,000 EUP x 75%) ……………………….….

12,000

Total EUP …………………………………………………………………………….….

80,000

3. Beginning inventory is 50% complete with respect to materials.

Ending inventory is 50% complete with respect to materials.

Units of

EUP for Materials

Product

To complete beginning work in process (24,000 EUP x 50%) …….

12,000

Units started and completed (56,000 EUP x 100%) ………………..….

56,000

Ending goods in process (16,000 EUP x 50%) ……………………….….

8,000

Total EUP …………………………………………………………………………….….

76,000

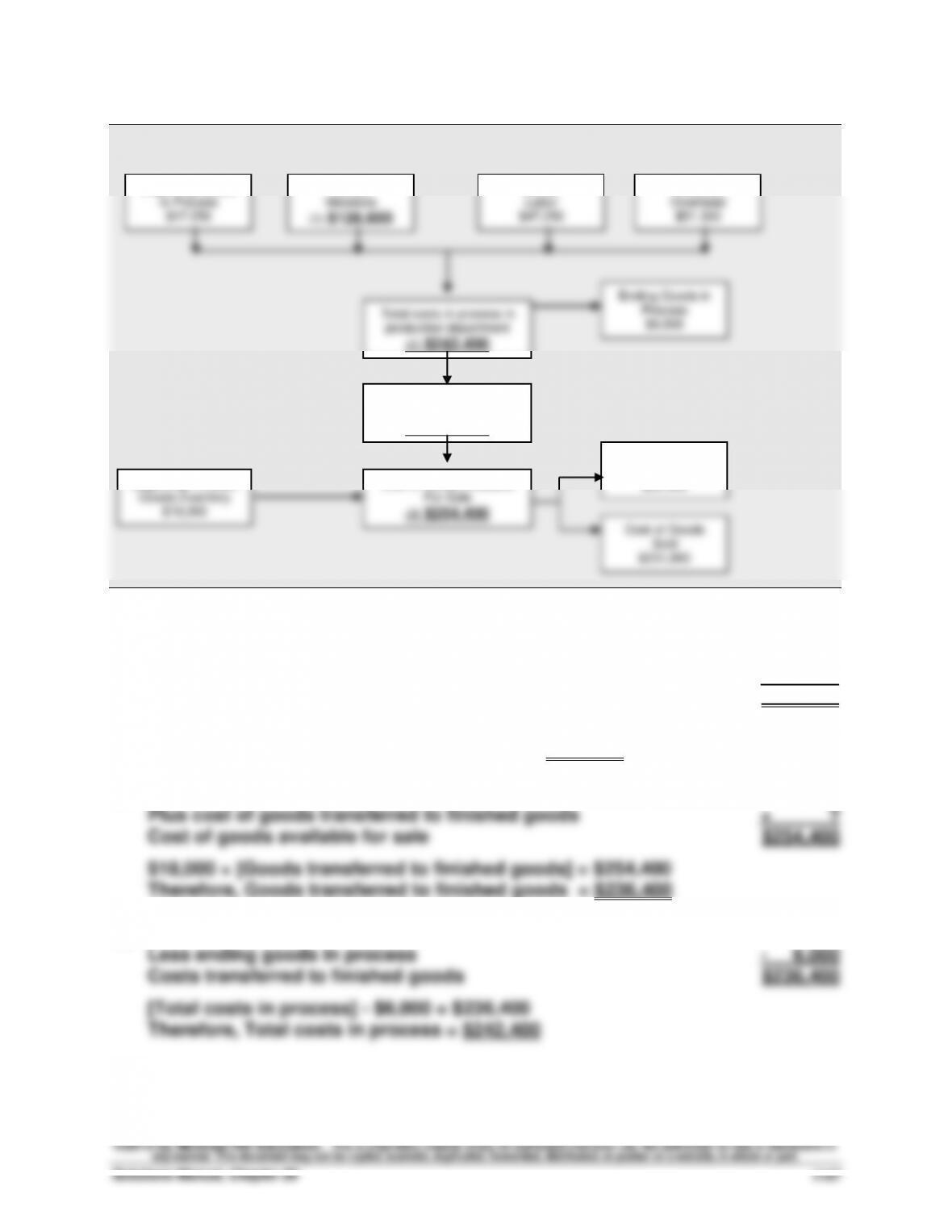

Exercise 20-14 (20 minutes)

Production

Warehouse

Key to solution of flowchart

To solve this problem, the missing items must be solved in reverse order: 4,3,2,1

(4)

Cost of goods available for sale

$ ?

Ending finished goods inventory

– 22,500

Cost of goods sold

$231,900

[Cost of goods available for sale] – $22,500 = $231,900

Therefore, cost of goods available for sale = $254,400

(3)

Beginning finished goods inventory

$ 18,000

Plus cost of goods transferred to finished goods

+ ?

Cost of goods available for sale

$254,400

$18,000 + [Goods transferred to finished goods] = $254,400

Therefore, Goods transferred to finished goods = $236,400

(2)

Total costs in process in production

$ ?

Less ending goods in process

– 6,000

Costs transferred to finished goods

$236,400

[Total costs in process] – $6,000 = $236,400

Therefore, Total costs in process = $242,400

Beginning Goods

in Process

Direct

Materials

Direct

Labor

Factory

Overhead

(2) $242,400

Costs transferred

to Finished Goods

(3) $236,400

Beginning Finished

Cost of Goods Available

Ending Finished

Goods Inventory

$22,500

$231,900