Title: Question 1

QA_Ori:

(a) FIFO: The cost of the first (earliest) items purchased in inventory flow to cost

(b) LIFO: The cost of the last (most recent) items purchased in inventory flow to cost

Title: Question 2

QA_Ori:

Merchandise inventory is disclosed on the balance sheet as a current asset. It

Title: Question 3

QA_Ori:

Incidental costs sometimes are ignored in computing the cost of inventory

because the expense of tracking such costs on a precise basis can outweigh the

Title: Question 4

QA_Ori:

LIFO will result in the lower cost of goods sold when costs are declining

QA_Ori:

The full-disclosure principle requires that the nature of the accounting change,

Title: Question 6

QA_Ori:

Title: Question 7

QA_Ori:

No; the consistency concept does not preclude changes in accounting methods

Title: Question 8

QA_Ori:

Many people make important business decisions based on period-to-period

fluctuations in a company’s financial numbers, including gross profit and net income.

Title: Question 9

QA_Ori:

An inventory error that causes an understatement (or overstatement) for net

income in one accounting period, if not corrected, will cause an overstatement (or

Title: Question 10

QA_Ori:

Market usually means replacement cost of inventory when applied in the LCM.

Title: Question 11

QA_Ori:

The accounting constraint of conservatism guides preparers of accounting

Title: Question 12

QA_Ori:

Title: Question 13

QA_Ori:

QA_Ori:

Title: Question 14

QA_Ori:

Title: Question 15

QA_Ori:

Cost of goods available for sale equals ending inventory plus cost of sales. As

of March 31, 2011, this is computed as ($ thousands):

Title: Question 16

QA_Ori:

Cost of goods available for sale equals ending inventory plus cost of sales. As

Title: Question 17

QA_Ori:

Merchandise inventory (EUR thousands) comprises 46.5% (236,988 / 509,708)

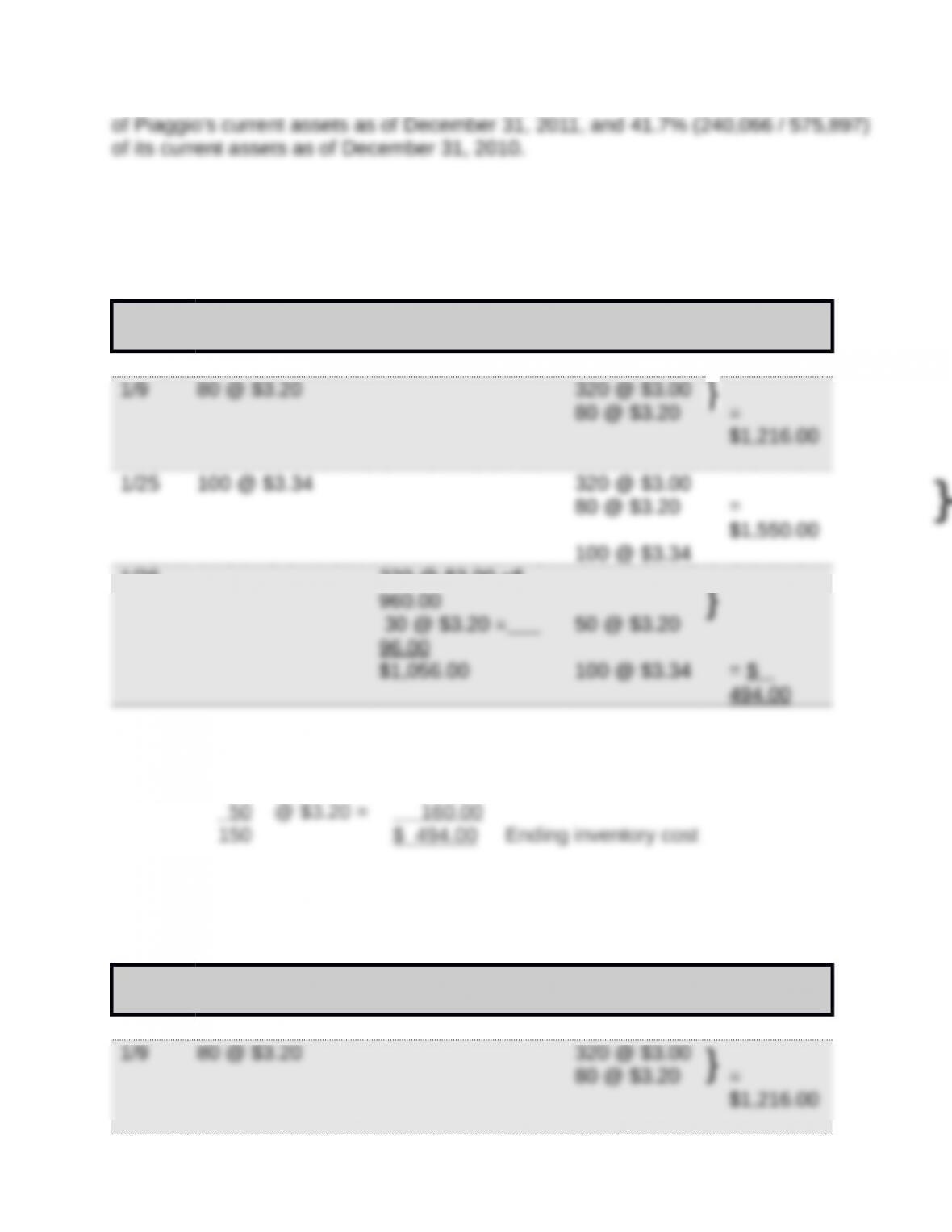

Title: Quick Study 6-1

QA_Ori:

FIFO—Perpetual

Date Goods

Purchased

Cost of Goods Sold Inventory Balance

1/1 320 @ $3.00 = $ 960.00

1/26 320 @ $3.00 =$

Alternate solution format

FIFO: 100 @ $3.34 = $ 334.00

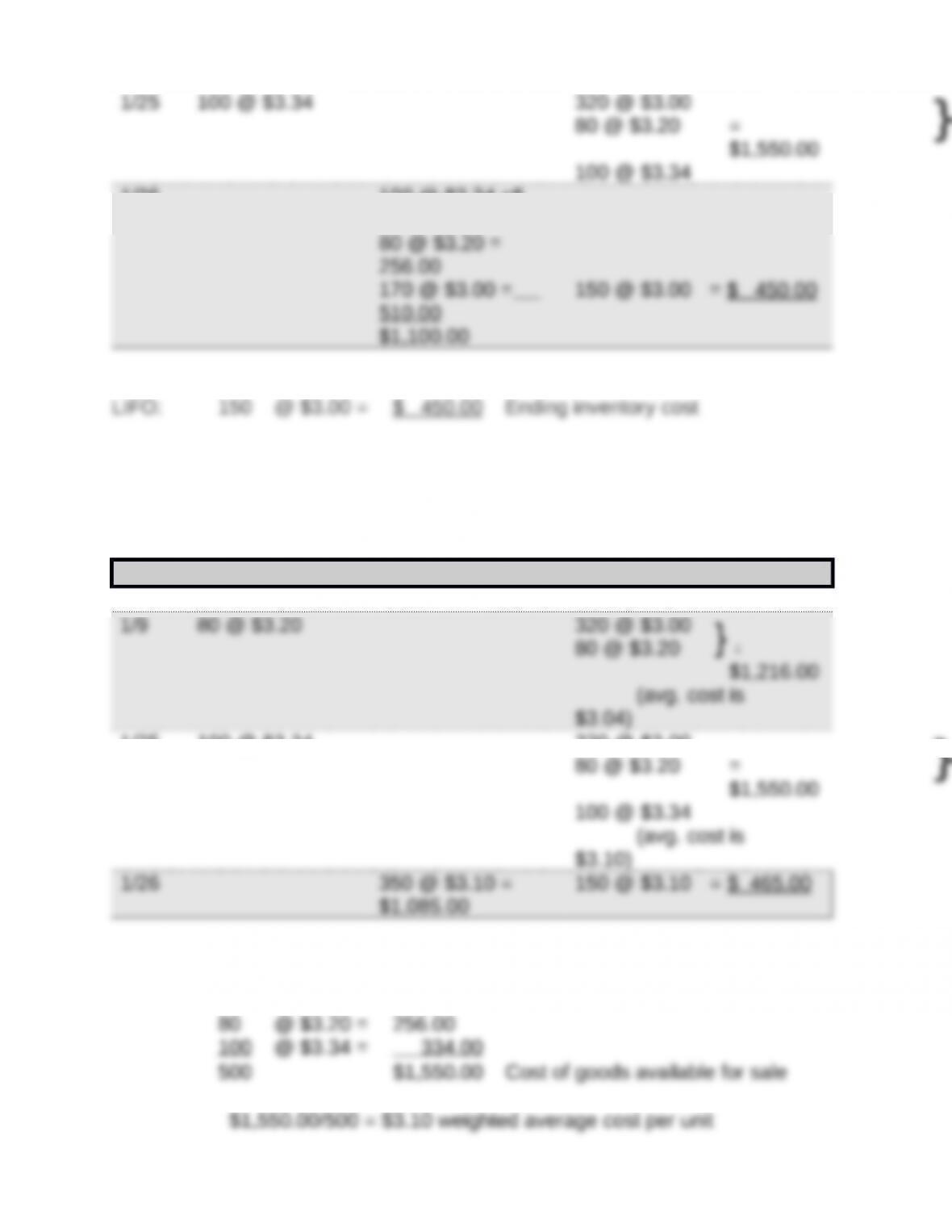

Title: Quick Study 6-2

QA_Ori:

LIFO—Perpetual

Date Goods

Purchased

Cost of Goods Sold Inventory Balance

1/1 320 @ $3.00 = $ 960.00

1/26 100 @ $3.34 =$

334.00

Alternate solution format

Title: Quick Study 6-3

Weighted Average—Perpetual

QA_Ori:

Date Goods Purchased Cost of Goods Sold Inventory Balance

1/1 320 @ $3.00 = $ 960.00

1/25 100 @ $3.34 320 @ $3.00

Alternate solution format

Weighted average:

320 @ $3.00 = $ 960.00

Title: Quick Study 6-4A

QA_Ori:

Ending Cost of

FIFO—Periodic Inventory Goods Sold

FIFO

Title: Quick Study 6-5A

QA_Ori:

Ending Cost of

LIFO—Periodic Inventory Goods Sold

LIFO

Title: Quick Study 6-6A

QA_Ori:

Ending Cost of

Weighted Average—Periodic Inventory Goods Sold

Weighted Average ($1,550/ 500 = $3.10 cost per

unit)

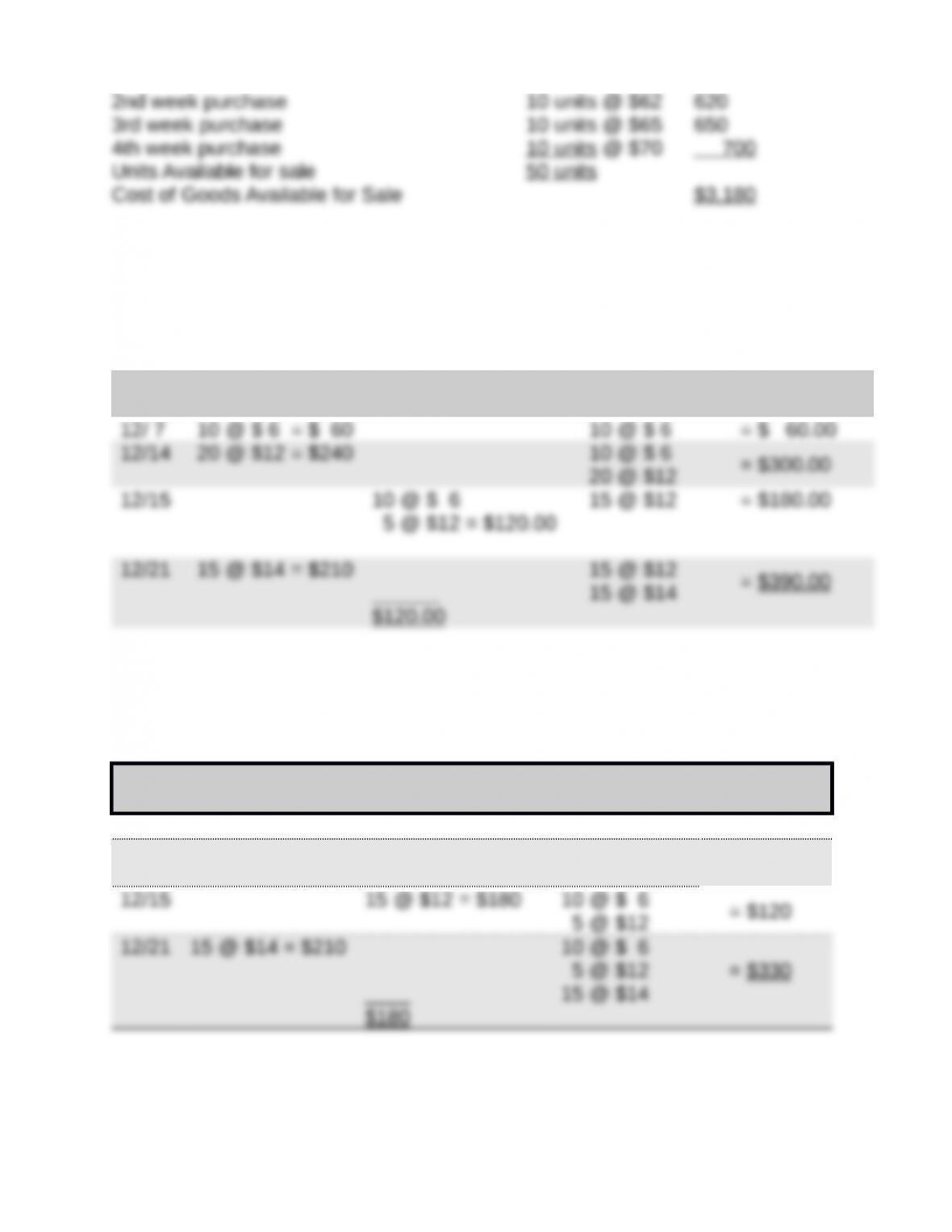

Title: Quick Study 6-7

QA_Ori:

Beginning inventory 10 units @ $60 $ 600

Plus

Title: Quick Study 6-8

QA_Ori:

FIFO—Perpetual

Date Goods

Purchased

Cost of Goods Sold Inventory Balance

Title: Quick Study 6-9

QA_Ori:

LIFO—Perpetual

Date Goods

Purchased

Cost of Goods

Sold

Inventory Balance

12/7 10 @ $ 6 = $ 60 10 @ $ 6 = $ 60

12/14 20 @ $12 = $240 10 @ $ 6 = $300

20 @ $12

Title: Quick Study 6-10

Weighted Average—Perpetual

QA_Ori:

Date Goods

Purchased

Cost of Goods

Sold

Inventory Balance

12/7 10 @ $6 = $60 10 @ $6 = $ 60

Title: Quick Study 6-11

QA_Ori:

Specific Identification— Perpetual

Ending inventory under specific identification:

Title: Quick Study 6-12A

QA_Ori:

Ending Cost of

FIFO— Periodic Inventory Goods Sold

FIFO

Title: Quick Study 6-13A

QA_Ori:

Ending Cost of

LIFO—Periodic Inventory Goods Sold

LIFO

Title: Quick Study 6-14A

QA_Ori:

Ending Cost of

Weighted Average—Periodic Inventory Goods Sold

unit)*

*If unit cost is not rounded, then ending inventory is $340 and goods sold is $170.

Title: Quick Study 6-15A

QA_Ori:

Ending Cost of

Specific Identification—Periodic Inventory Goods Sold

Specific Identification

Title: Quick Study 6-16

QA_Ori:

1. LIFO

Title: Quick Study 6-17

QA_Ori:

Units in ending inventory

Units stored in basement 1,300 units

Title: Quick Study 6-18

QA_Ori:

Cost $14,000

Plus

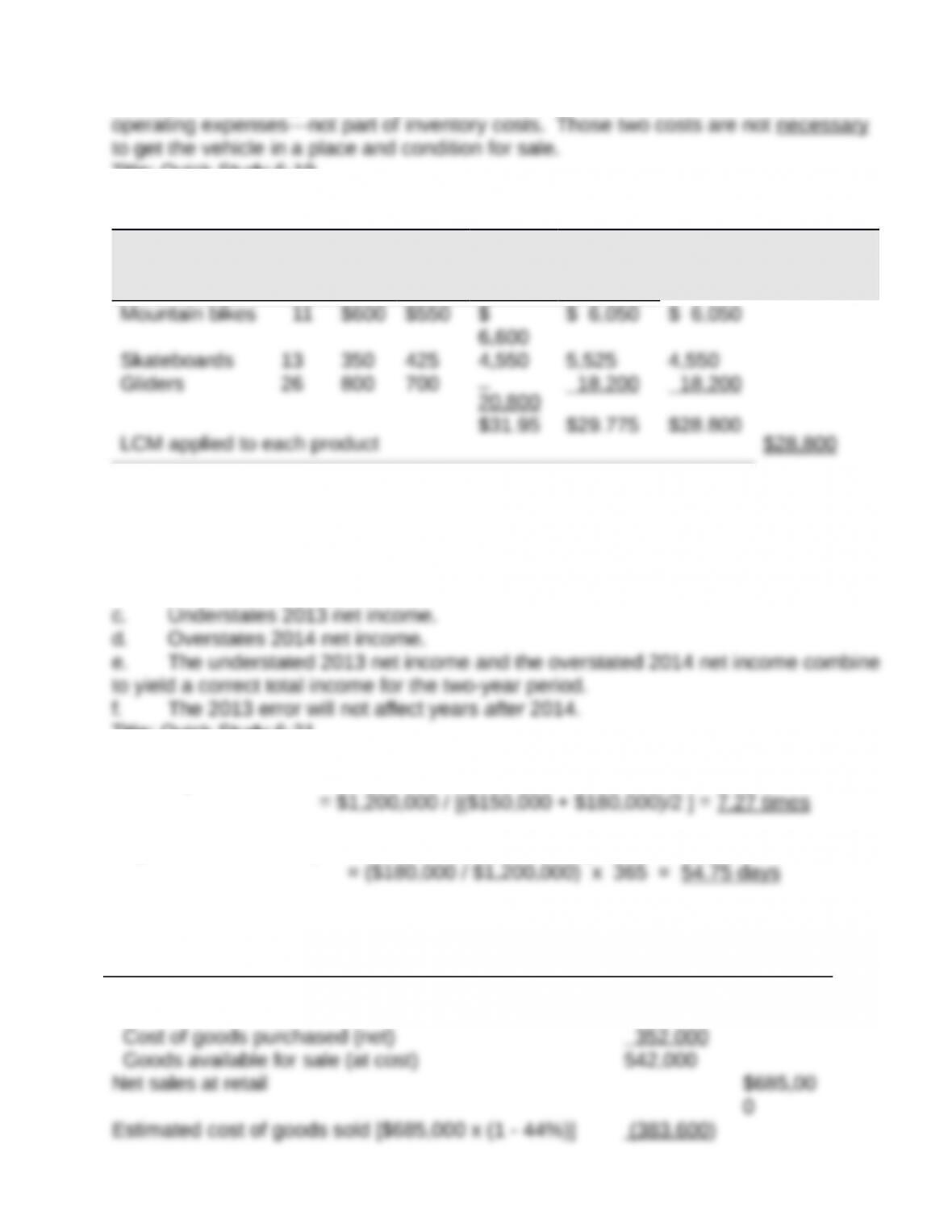

The $150 advertising cost and the $1,250 cost for sales staff salaries are included in

Title: Quick Study 6-19

QA_Ori:

Per Unit Total Total LCM – Items

Inventory Items Unit

s

Cost Marke

t

Cost Market

Title: Quick Study 6-20

QA_Ori:

a.Overstates 2013 cost of goods sold.

b.Understates 2013 gross profit.

Title: Quick Study 6-21

QA_Ori:

Inventory turnover = Cost of goods sold/Average merchandise inventory

Days’ sales in inventory = Ending Inventory/Costs of goods sold x 365

Title: Quick Study 6-22B

QA_Ori:

Goods available for sale

Inventory, January 1 $190,000

Title: Quick Study 6-23

QA_Ori:

a. Both IFRS and U.S. GAAP provide broad and similar guidance on the

accounting for items and costs making up merchandise inventory. Specifically,

b. Yes, companies reporting under IFRS can apply cost flow assumptions in

c. U.S. GAAP prohibits any later increase in the recorded value of inventory that