Title: Problem 21-3A

QA_Ori:

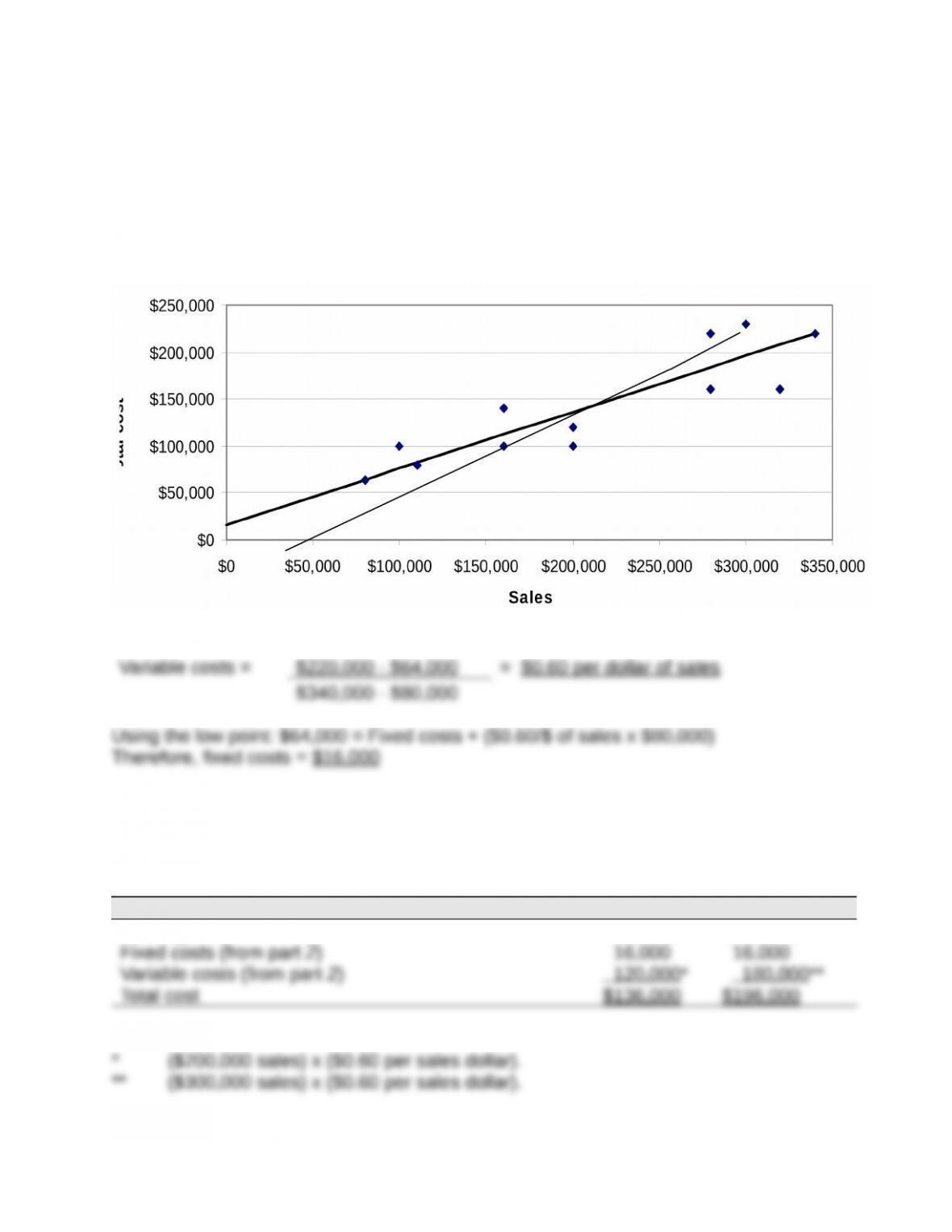

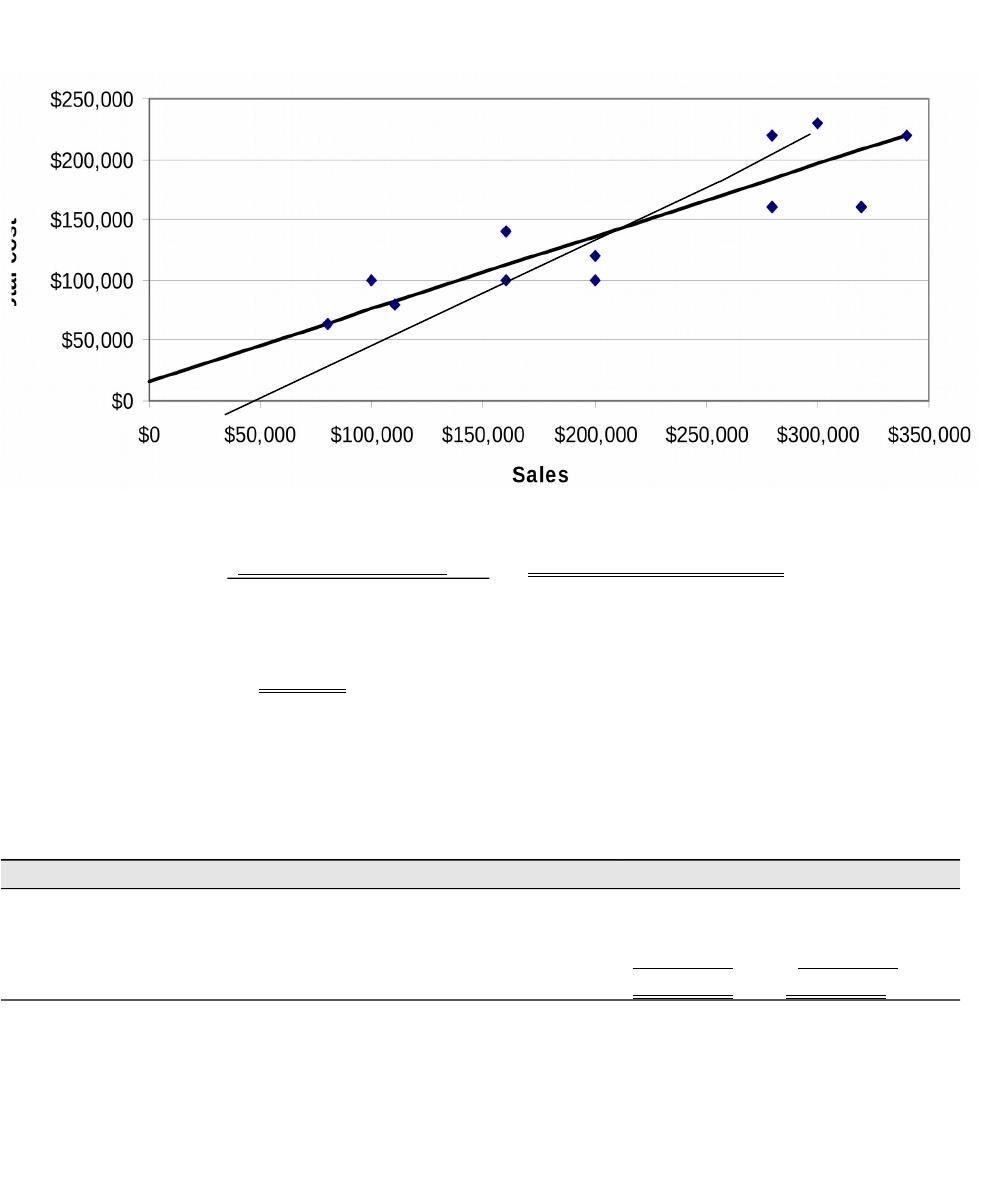

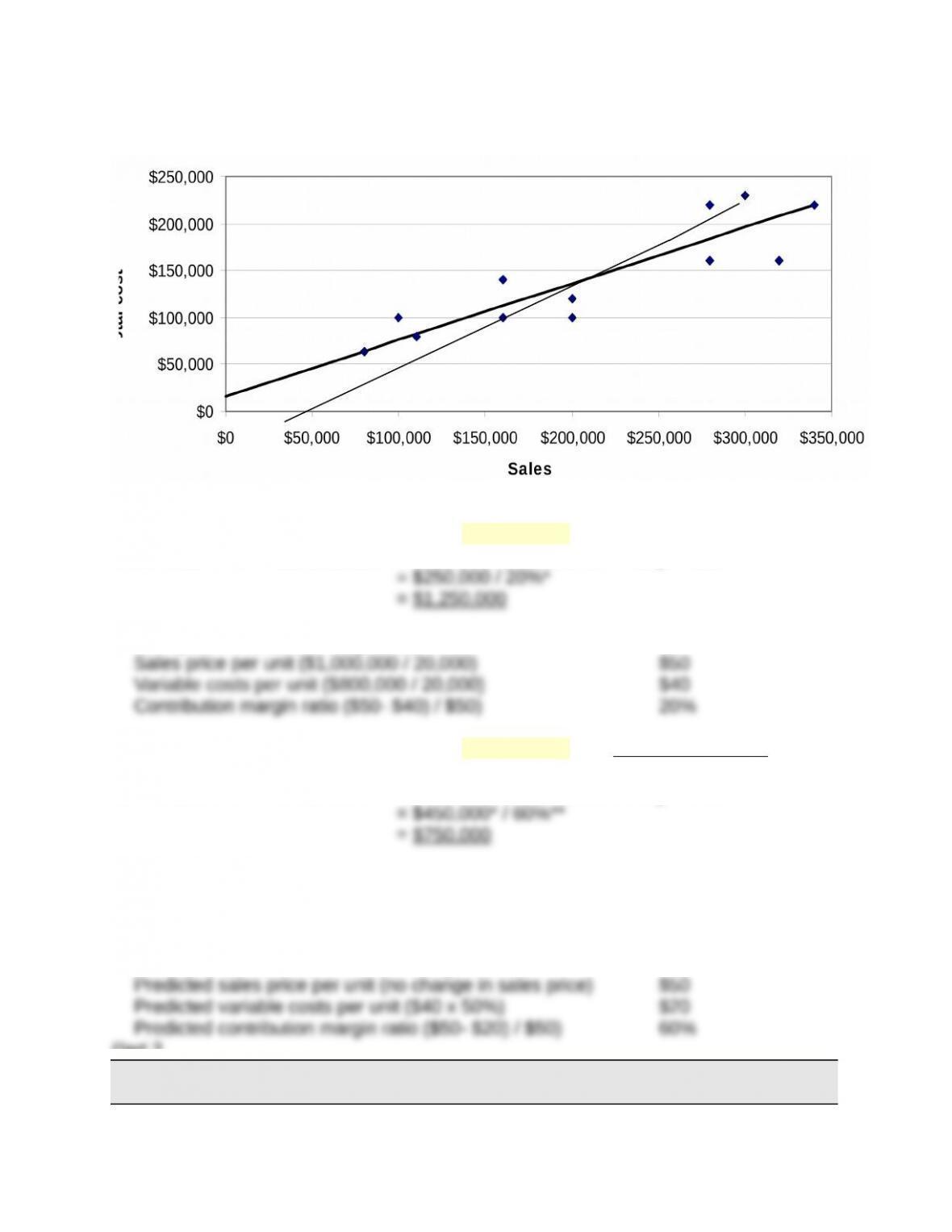

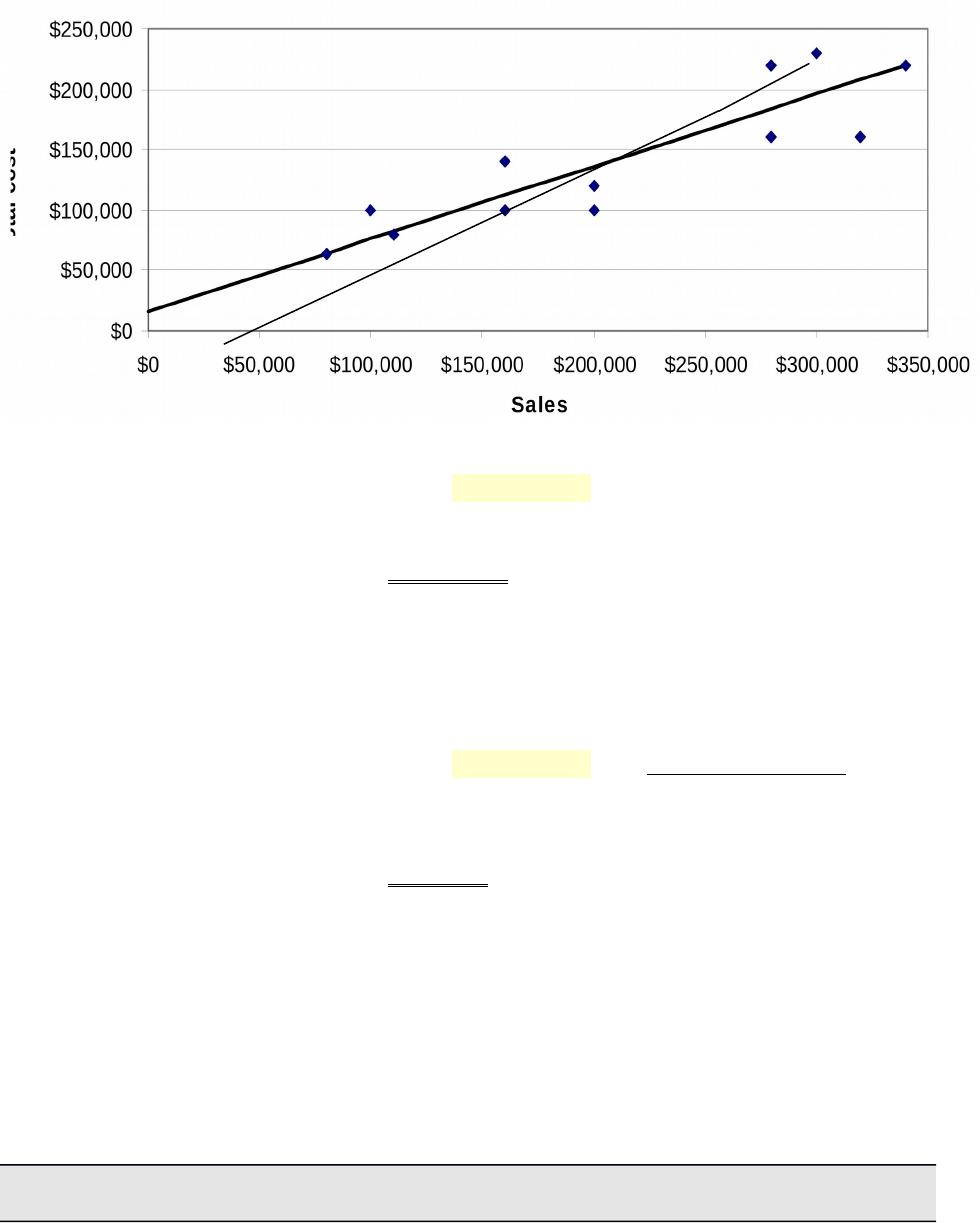

Parts 1 and 2

The scatter diagram and its estimated line of cost behavior appear below.

Part 2 – Calculation of variable and fixed costs

Part 3

The estimates in Part 2 can be used to predict the total costs that will be incurred at

sales levels of $200,000 and $300,000.

Predictions

Sales (given) $200,000 $300,000

Alden Co.

Alden Co.

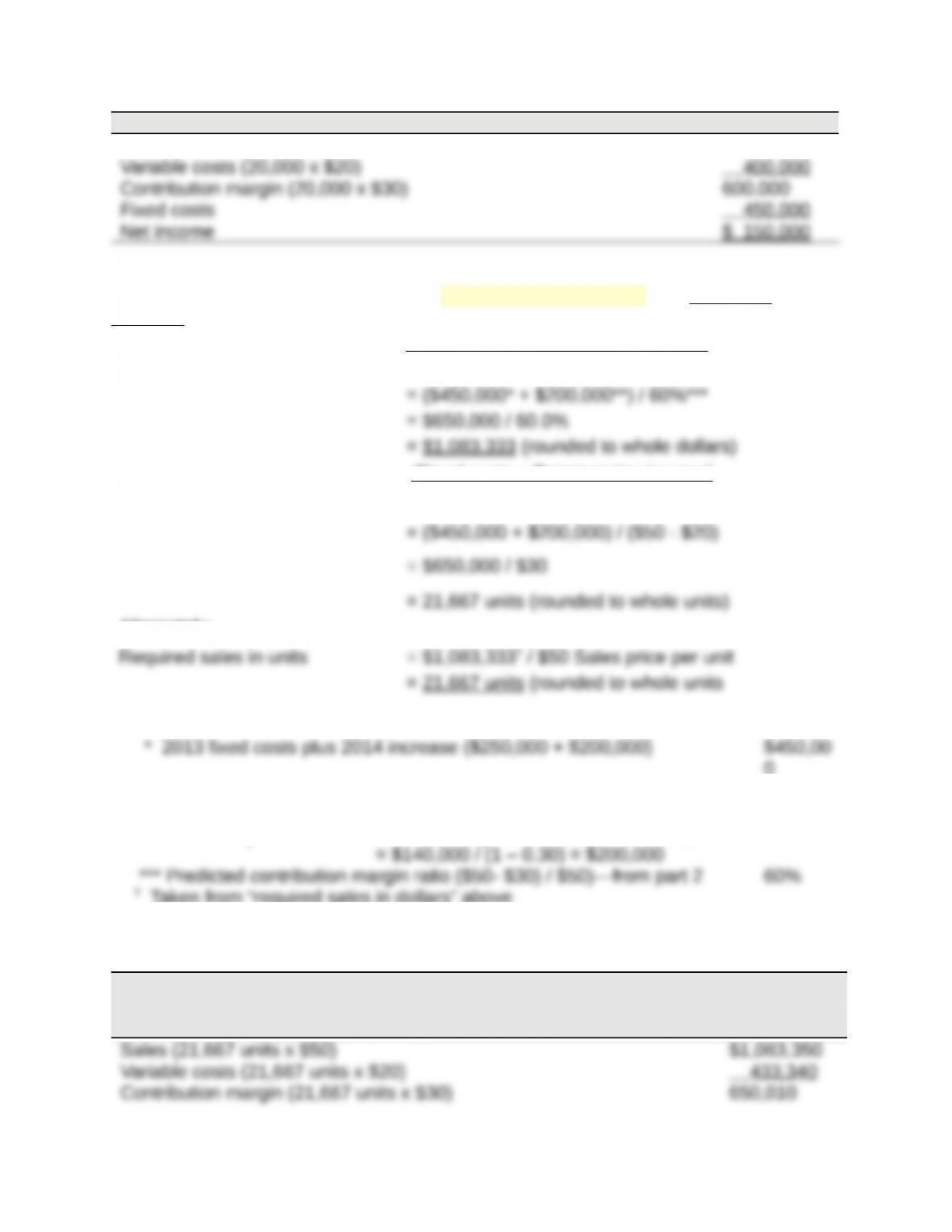

Title: Problem 21-4A

QA_Ori:

Part 1 Instructor note: Use the equation in Exhibit 21.12

2013 break-even in sales dollars = Fixed costs / Contribution margin ratio

*To compute contribution margin ratio

Part 2 Instructor note: Use the equation in Exhibit 21.12 with predicted numbers

2014 break-even in sales dollars = Fixed costs / Contribution margin ratio

*To compute predicted fixed costs

2013 fixed costs plus 2014 increase ($250,000 + $200,000) $450,00

0

**To compute predicted contribution margin ratio

Part 3

ASTRO COMPANY

Forecasted Contribution Margin Income Statement

For Year Ended December 31, 2014

Sales (20,000 x $50) $1,000,000

Part 4 Instructor note: Use equations in Exhibits 21.22 and 21.23 with predicted

numbers

Required sales in dollars = (Fixed costs + Target pretax income)

Contribution margin ratio

(Fixed costs + Target pretax income)

Required sales in units = Contribution margin per unit

Alternately:

0

** Target after-tax income (given) $140,00

0

Pretax target income = After-tax target income / (1 – Tax rate)

† Taken from “required sales in dollars” above

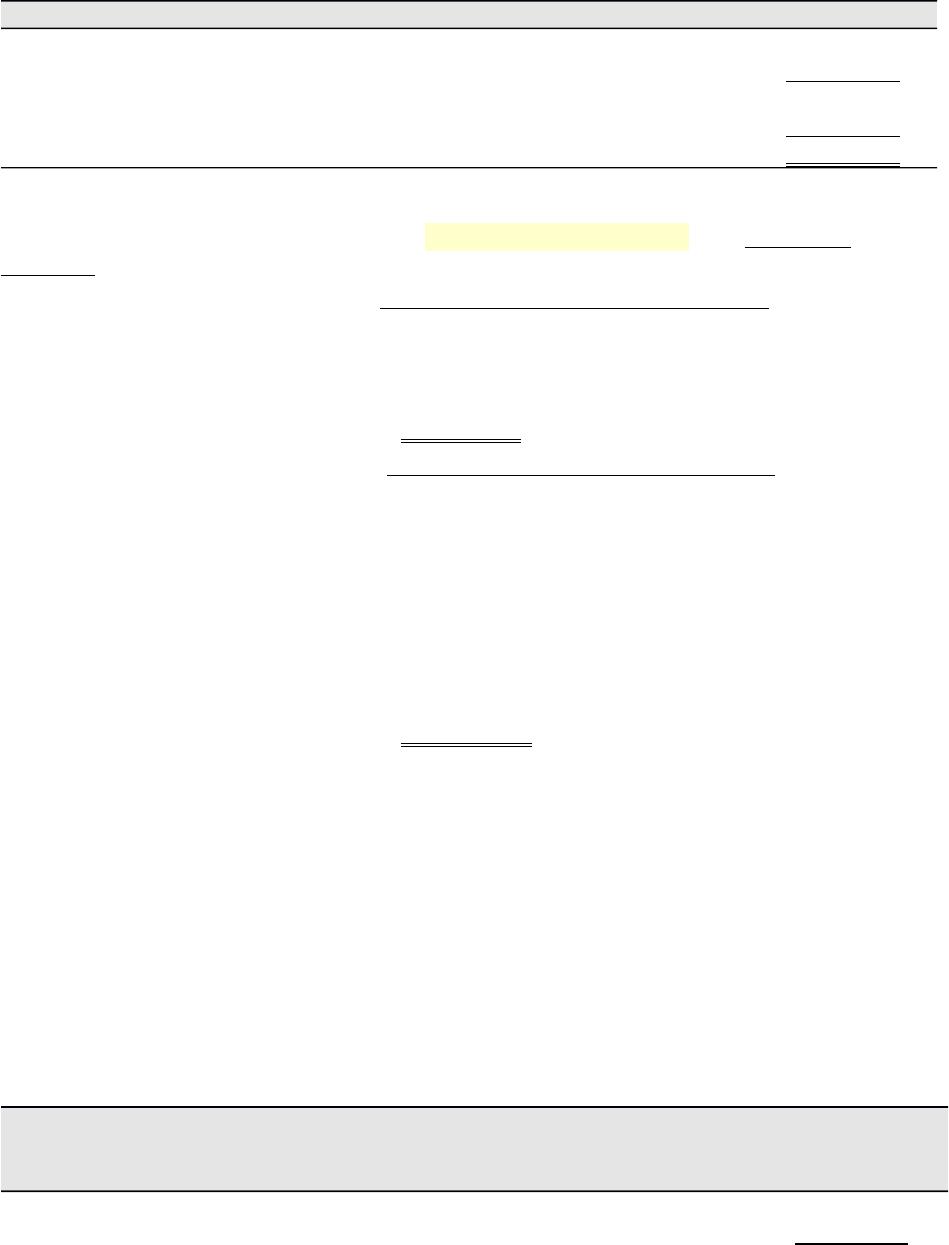

Part 5

ASTRO COMPANY

Forecasted Contribution Margin Income Statement

For Year Ended December 31, 2014

*Slightly greater than the targeted $140,000 income due to rounding of units.

Title: Problem 21-5A

QA_Ori:

Part 1 Instructor note: Use the equation in Exhibit 21.12

Break-even in dollar sales = Fixed costs / Contribution margin ratio

Product T: Break-even in dollar sales

Product O: Break-even in dollar sales

*To compute contribution margin ratio

Sales price per unit

Product T ($2,000,000 / 50,000)

Product O ($2,000,000 / 50,000)

__T__

$40

__O_

_

Part 2

Forecasted contribution margin income statements for each product assuming sales

declines to 30,000 units with no change in unit sales price

VANNA CO.

Forecasted Contribution Margin Income Statement

Product T Product O

Sales* $1,200,000 $1,200,000

Unit sales price and variable costs are computed in Part 1 and used in these

computations:

units x $5.

Part 3 Forecasted contribution margin income statements for each product assuming

sales increase to 60,000 units with no change in unit sales price

VANNA CO.

Forecasted Contribution Margin Income Statement

Product T Product O

Sales* $2,400,000 $2,400,000

Unit sales price and variable costs are computed in Part 1 and used in these

computations:

Part 4

If sales were to greatly decrease, Product O would suffer the greater loss because it

would lose more contribution margin per unit than Product T ($35 for O versus $8 for T).

Part 5

Factors that could cause Product T to have lower fixed costs might include:

Labor arrangement that pays workers for units produced.

A salary structure that is not based on production or sales.

Product O’s assets that are owned or obtained under a lease agreement based on time,

and not on asset usage.

Title: Problem 21-6A

QA_Ori:

Part 1 Instructor note: Use the equation in Exhibit 21.12

Break-even in dollar sales = Fixed costs / Contribution margin ratio

Plan 1: Break-even in dollar sales

Plan 2: Break-even in dollar sales

*To compute contribution margin ratio

Sales price per unit

Plan 1 (no change)

Plan 2 [$25.00 x (1 + 20%)]

Plan 1

$25.00

Plan 2

$30.00

Total variable costs per unit (both Plans 1 and 2)

Part 2

BERTRAND CO.

Forecasted Contribution Margin Income Statement

Plan 1 Plan 2

Sales* $1,000,000 $1,080,000

Variable costs** 300,000 270,000

Unit sales price and variable costs are computed in Part 1 and used in these

computations:

** Plan 1 variable costs = 40,000 units x $7.50; Plan 2 variable costs = 36,000 units x

$7.50.

Title: Problem 21-7A

QA_Ori:

Part 1 BREAK–EVEN ANALYSIS ASSUMING USE OF SAME MATERIALS

Step 1: Compute break-even in composite units—Use equation in Exhibit 21.27

Break-even in composite units = Fixed costs/Contribution margin per composite unit

*To compute the contribution margin per composite unit

Unit Sales Price Unit Variable Costs

5 units of Red

@ $20 per unit

@ $12 per unit

$100

$ 60

Thus:

Step 2: Compute break-even in individual product unit sales

Step 3: Compute break-even in individual product dollar sales

Crossfoot Step 3 total with that from formula ($235 rounding difference):

Break-even in dollar sales = Fixed costs / Contribution margin ratio

Part 2 BREAK–EVEN ANALYSIS ASSUMING USE OF NEW MATERIALS

Step 1: Compute break-even in composite units—Use equation in Exhibit 21.27

Break-even in composite units = Fixed costs/Contribution margin per composite unit

*To compute the contribution margin per composite unit

Unit Sales Price Unit Variable Costs

5 units of Red

@ $20 per unit

@ ($12 – $6) per unit

$100

$ 30

Thus:

Step 2: Compute break-even in individual product unit sales

Unit sales of Red at break-even: 1,364 x 5 = 6,820 units

Step 3: Compute break-even in individual product dollar sales

Dollar sales of Red at break-even: 6,820 units x $20 = $136,400

Crossfoot Step 3 total with that from formula ($139 rounding difference):

Break-even in dollar sales = Fixed costs / Contribution margin ratio

Part 3

When a business invests in fixed assets, as in this case, there is an increase in its risk

Title: Problem 21-1B

QA_Ori:

Parts 1 and 2

Gilmore Company

Contribution Margin Income Statement

For Year Ended December 31, 2013

(12,000 units) Per unit % of sales

Sales ($18 x 12,000) $216,000 $18.00

0

100.00

%

Variable costs

Plastic for CD sets $ 1,500 $0.12

5

The contribution margin per unit is $14.625, and the contribution margin ratio is 81.25%.

Part 3 Analysis Component

Contribution margin shows how much of total sales are available to cover fixed costs

Title: Problem 21-2B

QA_Ori:

Part 1

(a) Instructor note: Use the equation in

Exhibit 21.11

= Fixed costs / Contribution margin

per unit

(b) Instructor note: Use the equation in

Exhibit 21.12

= Fixed costs / Contribution margin

ratio

Break-even in dollar sales

Part 2

Part 3

HIP-HOP CO.

Contribution Margin Income Statement (at Break-Even) — Keyboards

Sales (300 x $350) $105,000

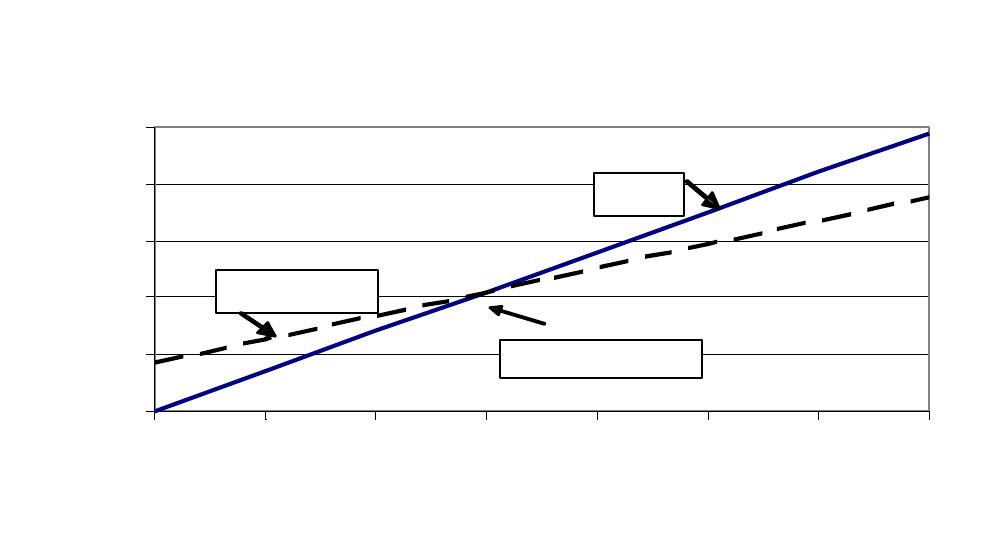

Hip-Hop Company CVP chart

$ 0

$50,000

$100,000

$150,000

$200,000

$250,000

0 100 200 300 400 500 600 700

Units

Sales

Total Costs

Breakeven point