Title: Problem 6-4A

QA_Ori:

1. Calculate cost of goods available for sale and units available for sale

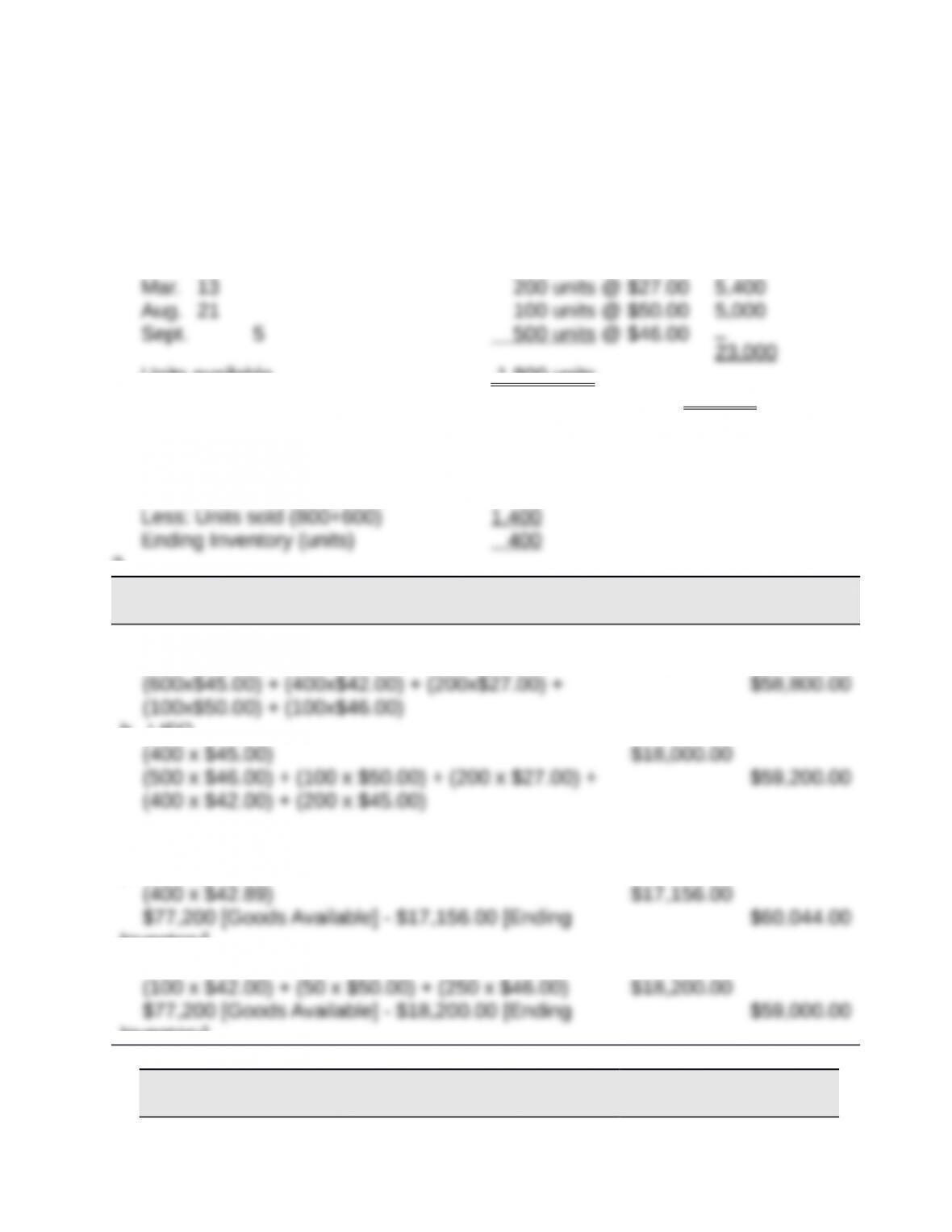

Beginning inventory 600 units @ $45.00 $27,00

0

Feb. 10 400 units @ $42.00 16,800

Units available 1,800 units

Cost of goods available for sale $77,200

2. Units in ending inventory

Units available (from part 1) 1,800

3.

Periodic Inventory

Ending

Inventory

Cost of

Goods Sold

a. FIFO

(400 x $46.00) $18,400.00

(100x$50.00) + (100x$46.00)

b. LIFO

(400 x $42.00) + (200 x $45.00)

c. Weighted average ($77,200/1,800 = $42.89

[rounded])

Inventory]

d. Specific identification

Inventory]

4.

Specific

Identifi-c Weighted

FIFO LIFO ation Average

Sales (1,400 x $75) $105,00

0

$105,00

0

$105,00

0

$105,000

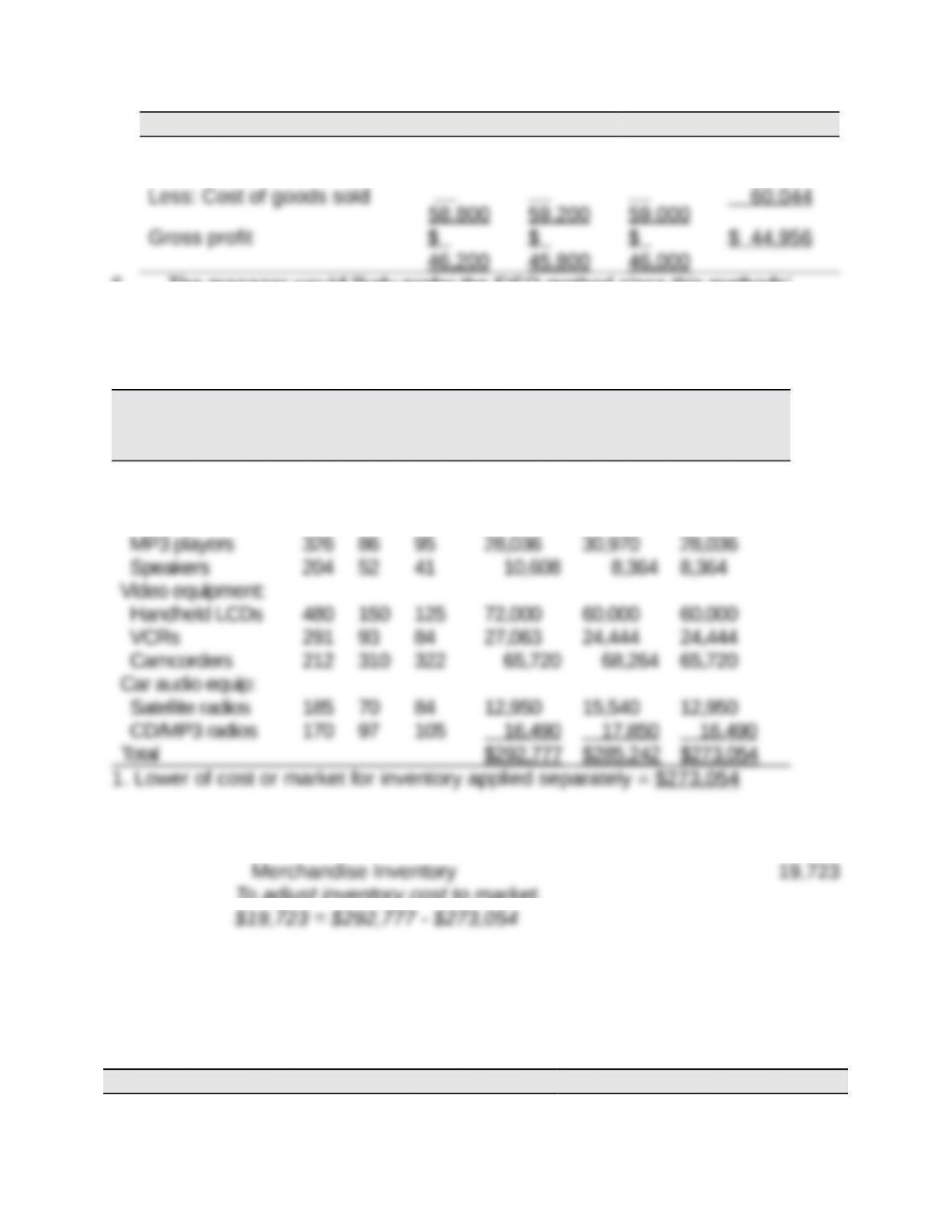

5. The manager would likely prefer the FIFO method since this methods’

gross profit is the largest at $46,200. This would give the manager the highest

bonus based on gross profit.

Title: Problem 6-5A

QA_Ori:

Per Unit Total Total LCM

Applied

to Items

Inventory Items Unit

s

Cos

t

Marke

tCost Market

Audio equipment:

Receivers 345 $ 90 $ 98 $ 31,050 $ 33,810 $ 31,050

CD players 260 111 100 28,860 26,000 26,000

2.

Dec 31 Cost of Goods Sold 19,723

To adjust inventory cost to market.

Title: Problem 6-6A

QA_Ori:

Part 1

(a)

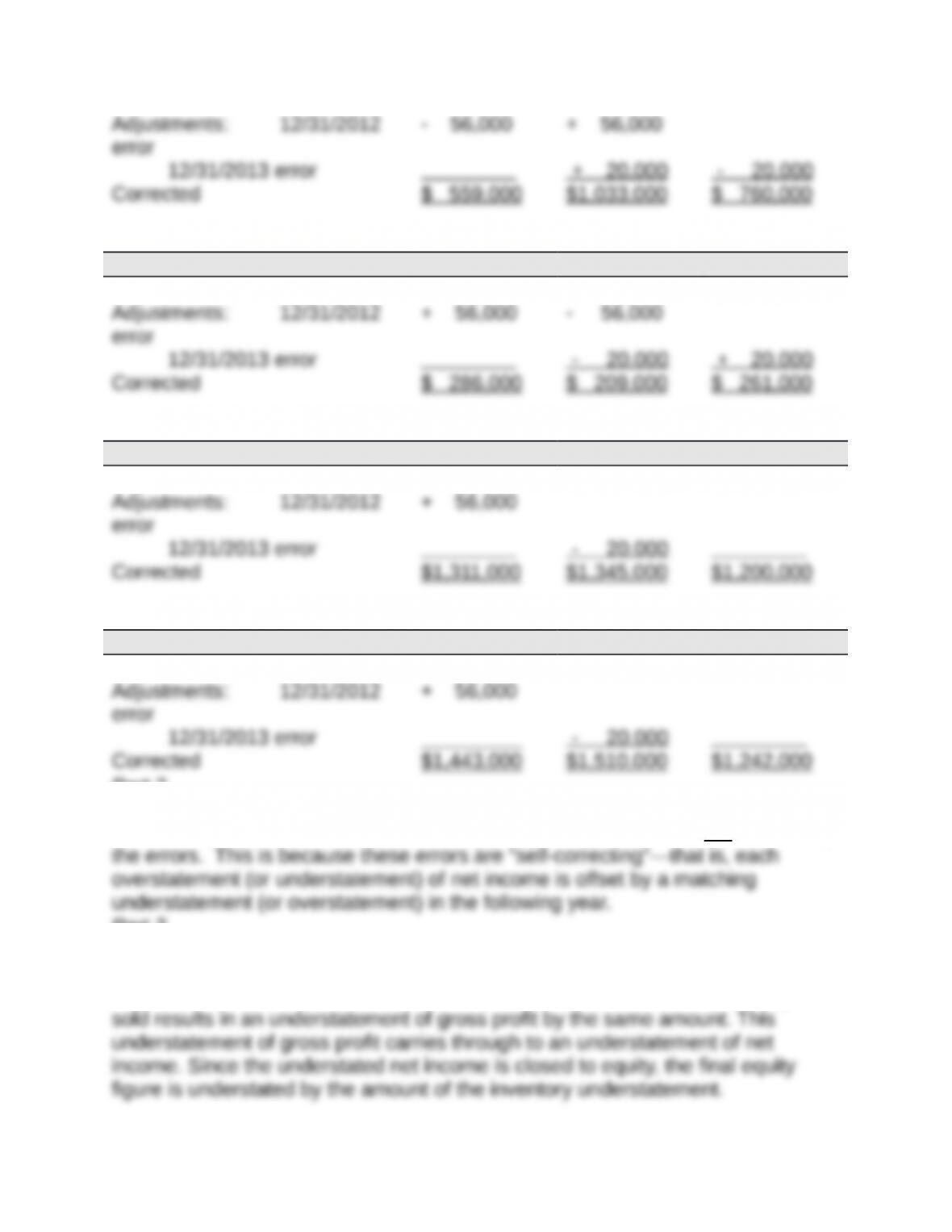

Cost of goods sold 2012 2013 2014

Reported $ 615,000 $ 957,000 $ 780,000

(b)

Net income 2012 2013 2014

Reported $ 230,000 $ 285,000 $ 241,000

(c)

Total current assets 2012 2013 2014

Reported $1,255,000 $1,365,000 $1,200,000

(d)

Equity 2012 2013 2014

Reported $1,387,000 $1,530,000 $1,242,000

Part 2

Total net income for the combined three-year period ($756,000) is not affected by

Part 3

The understatement of inventory by $56,000 results in an overstatement of cost

of goods sold by that same amount. The $56,000 overstatement of cost of goods

Title: Problem 6-7AA

QA_Ori:

Part 1

Number and total cost of units available for

sale

23,000 units in beginning inventory @ $15 $345,000

30,000 units purchased @ $18 540,000

Part 2

a. FIFO periodic

Total cost of 150,000 units available for sale $3,150,000

Less ending inventory on a FIFO basis

b. LIFO periodic

Total cost of 150,000 units available for sale $3,150,000

c. Weighted average periodic

Total cost of 150,000 units available

$3,150,000

Title: Problem 6-8AA

QA_Ori:

Part 1

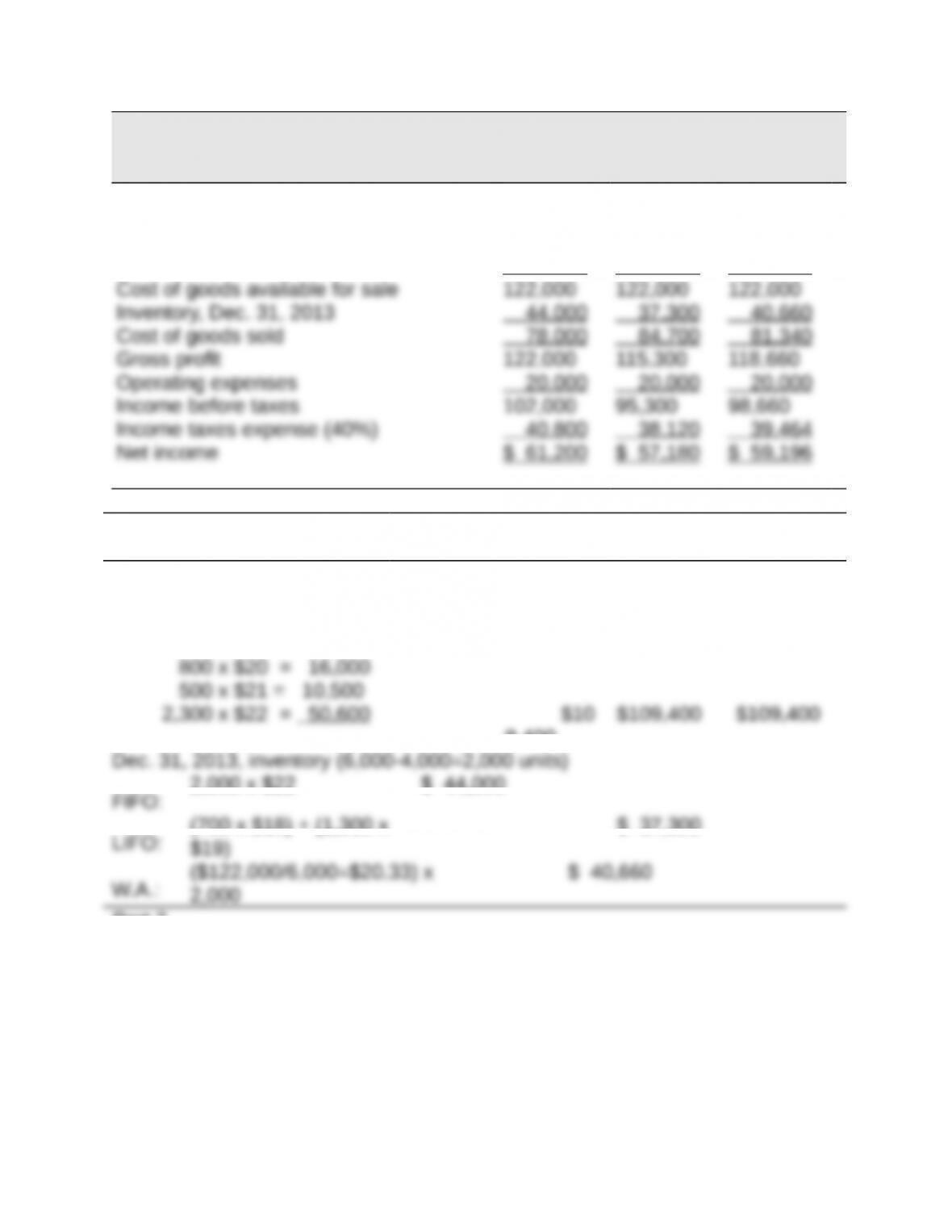

QP CORP.

Income Statements Comparing FIFO, LIFO, and Weighted Average

For Year Ended December 31, 2013

FIFO LIFO

Weighted

Average

Sales $200,000 $200,000 $200,000

Cost of goods sold

Inventory, Dec. 31, 2012 12,600 12,600 12,600

Cost of purchases 109,400 109,400 109,400

Supporting calculations FIFO LIFO

Weighted

Average

Dec. 31, 2012, inventory (700 x $18). $

12,600

$

12,600

$ 12,600

Purchases

1,700 x $19 = $32,300

$ 37,300

Part 2

If QP Corp. had been experiencing declining costs in the acquisition of inventory,

we would observe the opposite results in our comparisons. Specifically, LIFO

would have resulted in a higher ending inventory, lower cost of goods sold, higher

gross profit, and higher net income. FIFO would have resulted in a lower ending

inventory, higher cost of goods sold, lower gross profit, and lower net income.

Part 3

Advantages

LIFO: Given the cost trends in the Title: Problem, the advantage of using LIFO is

Disadvantages

LIFO: Given the cost trends in the Title: Problem, the disadvantage of using LIFO

Title: Problem 6-9AA

QA_Ori:

Part 1

ALASKA COMPANY

Estimated Inventory

December 31

At Cost At Retail

Goods available for sale

Beginning inventory $ 469,010 $ 928,950

Cost of goods purchased 3,376,050 6,381,050

Part 2

ALASKA COMPANY

Inventory Shortage

December 31

At Cost At Retail

Estimated inventory (from part 1) $ 924,182 $ 1,757,000

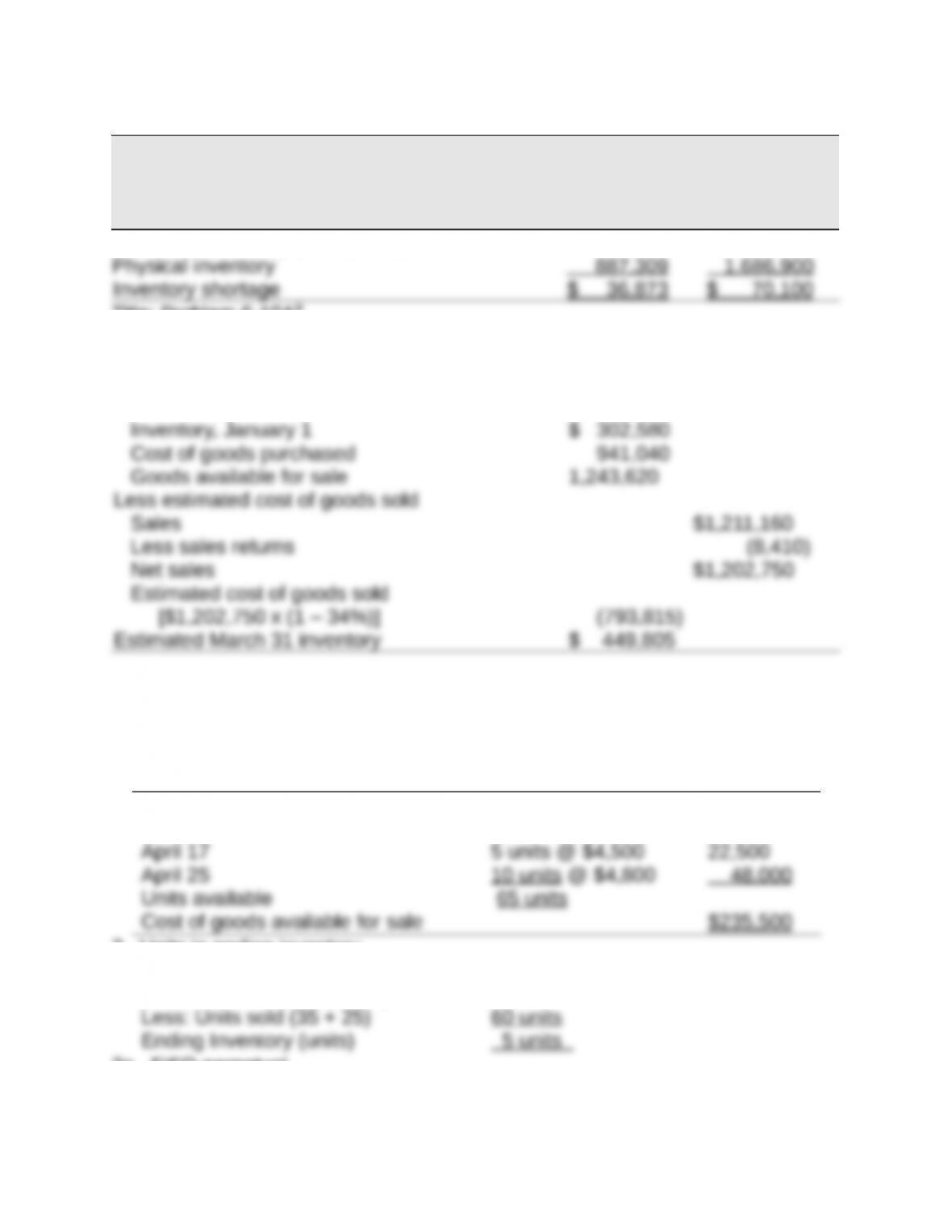

Title: Problem 6-10AB

QA_Ori:

WAYWARD COMPANY

Estimated Inventory at March 31

Goods available for sale

Title: Problem 6-1B

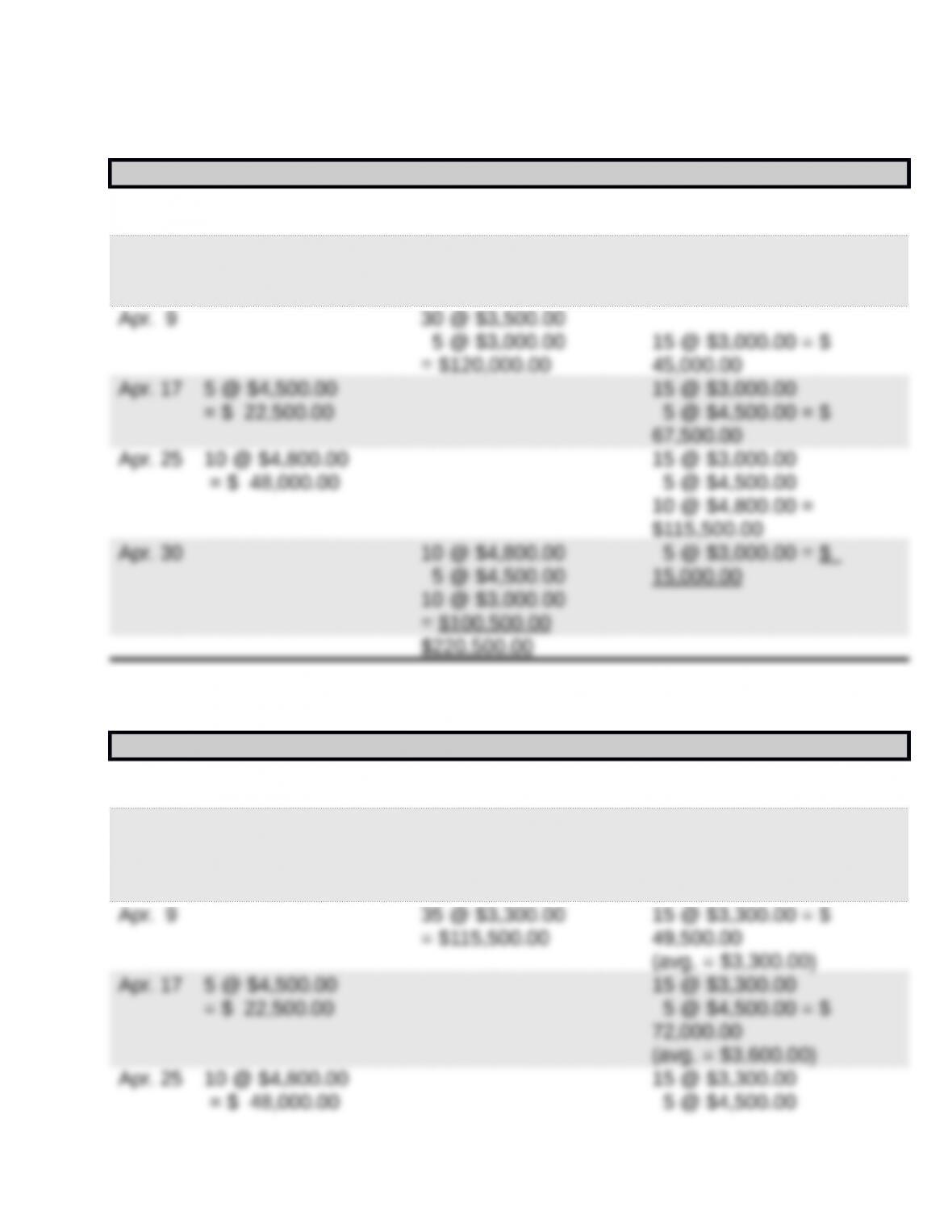

QA_Ori:

1. Compute cost of goods available for sale and units available for sale

Beginning inventory 20 units @ $3,000 $ 60,000

April 6 30 units @ $3,500 105,000

2. Units in ending inventory

Units available (from part 1) 65 units

3a. FIFO perpetual

Date Goods Purchased Cost of Goods Sold Inventory Balance

Apr. 1 20 @ $3,000.00 = $

60,000.00

Apr. 6 30 @ $3,500.00

= $105,000.00

20 @ $3,000.00

30 @ $3,500.00 =

$165,000.00

Apr. 9 20 @ $3,000.00

15 @ $3,500.00

= $112,500.00

15 @ $3,500.00 = $

52,500.00

3b. LIFO perpetual

Date Goods Purchased Cost of Goods Sold Inventory Balance

Apr. 1 20 @ $3,000.00 = $

60,000.00

Apr. 6 30 @ $3,500.00

= $105,000.00

20 @ $3,000.00

30 @ $3,500.00 =

$165,000.00

3c. Weighted Average perpetual

Date Goods Purchased Cost of Goods Sold Inventory Balance

Apr. 1 20 @ $3,000.00 = $

60,000.00

Apr. 6 30 @ $3,500.00

= $105,000.00

20 @ $3,000.00

30 @ $3,500.00 =

$165,000.00

(avg. = $3,300.00)

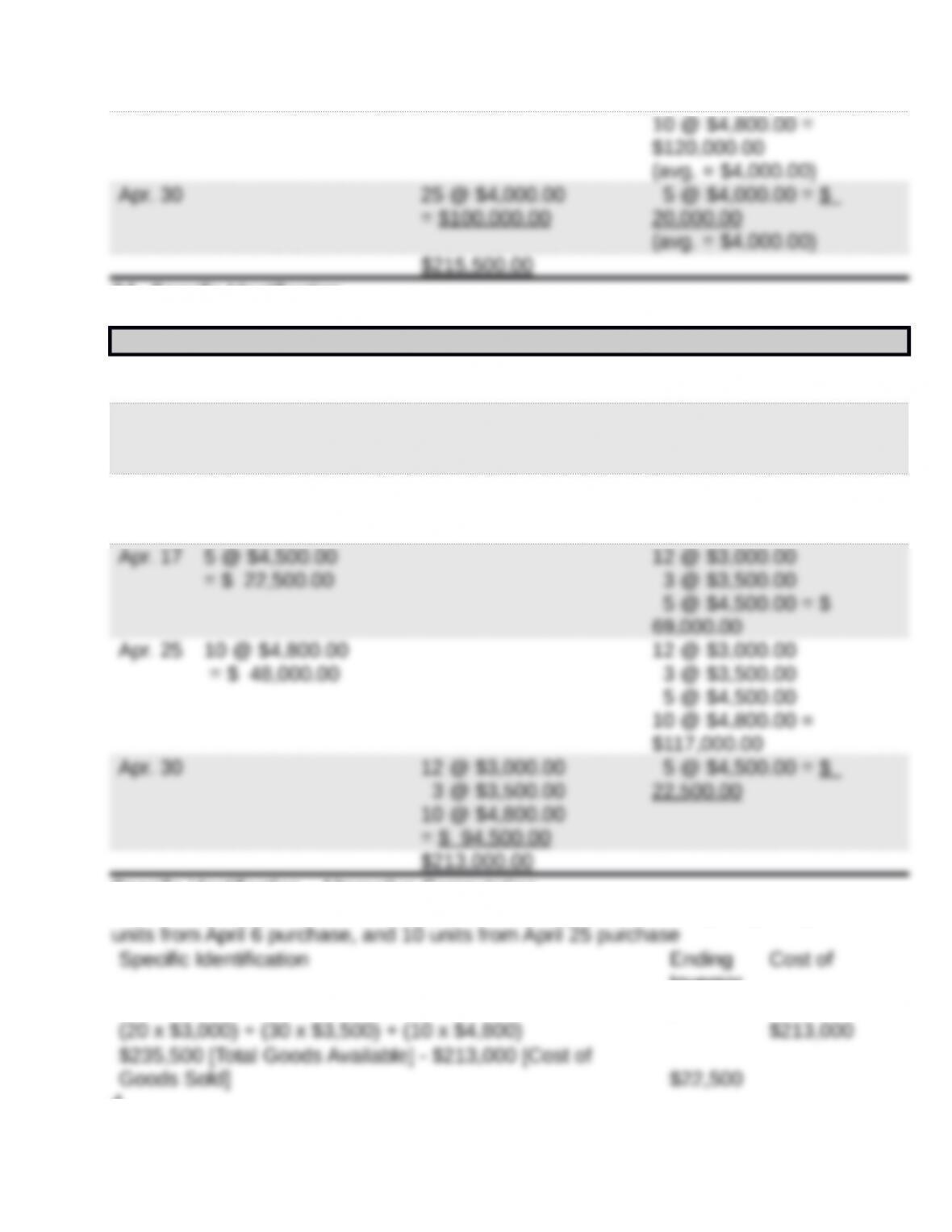

3d. Specific Identification

Date Goods Purchased Cost of Goods Sold Inventory Balance

Apr. 1 20 @ $3,000.00 = $

60,000.00

Apr. 6 30 @ $3,500.00

= $105,000.00

20 @ $3,000.00

30 @ $3,500.00 =

$165,000.00

Apr. 9 8 @ $3,000.00

27 @ $3,500.00

= $118,500.00

12 @ $3,000.00

3 @ $3,500.00 = $

46,500.00

Specific identification—Alternative Computation

Cost of goods sold—20 [8+12] units from beginning inventory, 30 [27+3]

Inventor

y Goods Sold

4.

FIFO LIFO

Weighted

Average

Specific

Identifi-cat

ion

Sales* $770,000 $770,000 $770,000 $770,000