Fundamental Accounting Principles, 21st Edition

1430

Exercise 24-6 (20 minutes)

Allocation of annual wages between the two departments

Hours Worked*

% of Total

Cost

Jewelry Dept ……………………….….

57

75%

$22,500

Totals …………………………………………

76

100%

$30,000

*Computation of hours worked in the two selling departments

Jewelry department

Selling …………………………………………………..

51

Arranging and stocking …………………..……..

6

57 hours

Hosiery department

Selling …………………………………………………..

12

Arranging and stocking …………………..……..

7

Total hours ………………………………………..……..

Instructor note: This analysis ignores idle time because neither department

Exercise 24-7 (15 minutes)

1.

Location

Net Income

Average Assets

Return on

Investment (Assets)

Location A …………..………

$160,000

$1,000,000

16%

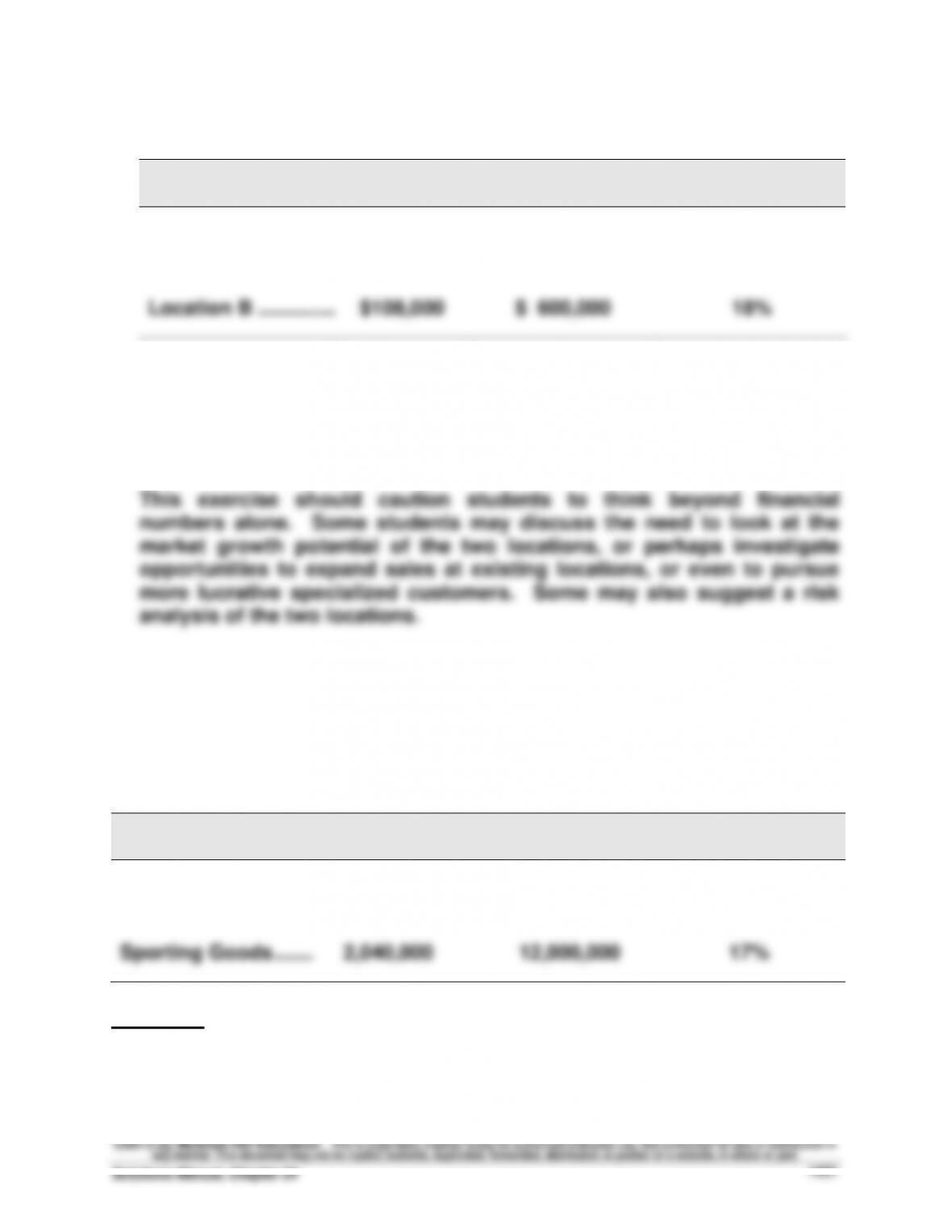

2. The recommendation is to pursue Location B because its return on

investment (assets) is 18%, compared to 16% at Location A. Moreover,

given the normal return of 18% for this chain, only Location B meets this

hurdle.

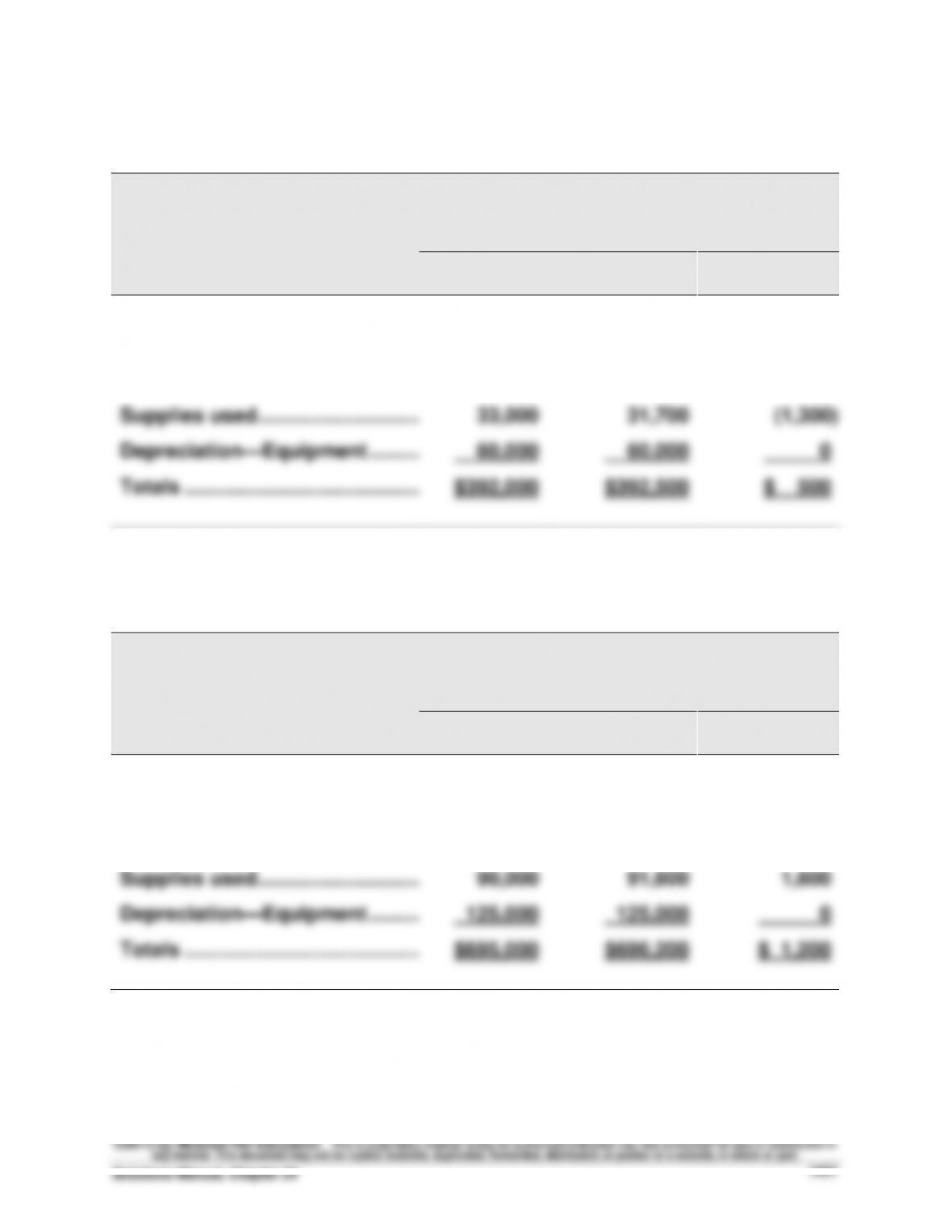

Exercise 24-8 (20 minutes)

(1)

Investment Center

Net Income

Average Assets

Return on

Investment (Assets)

Electronics …………….….

$2,880,000

$16,000,000

18%

17%

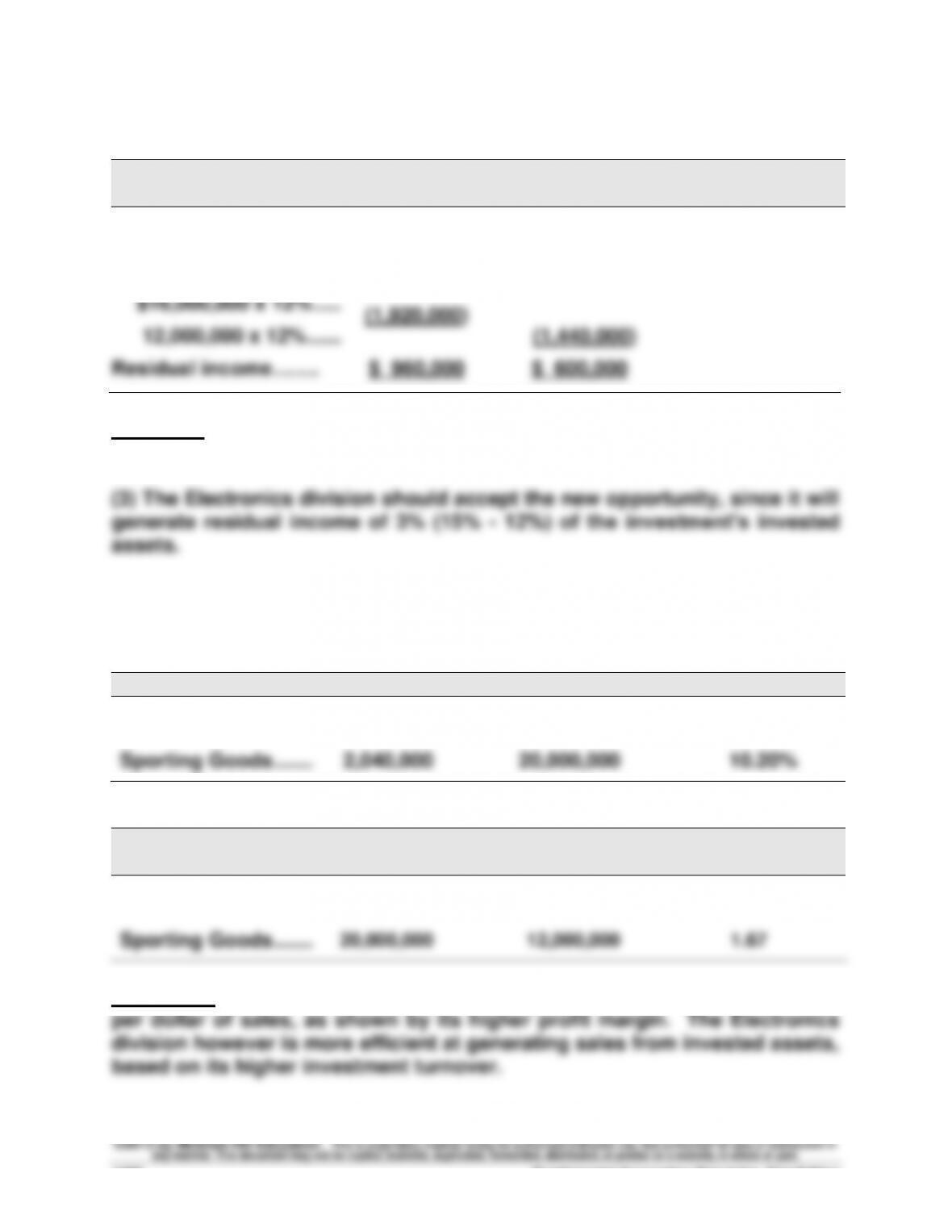

Comment: The Electronics division is the superior investment center on

the basis of the investment center return on investment (assets).

Fundamental Accounting Principles, 21st Edition

1432

Exercise 24-8 (continued)

(2)

Investment Center

Electronics

Sporting

Goods

Net income ………………..

$2,880,000

$2,040,000

Target net income

Comment: The Electronics division is the superior investment center on

the basis of investment center residual income.

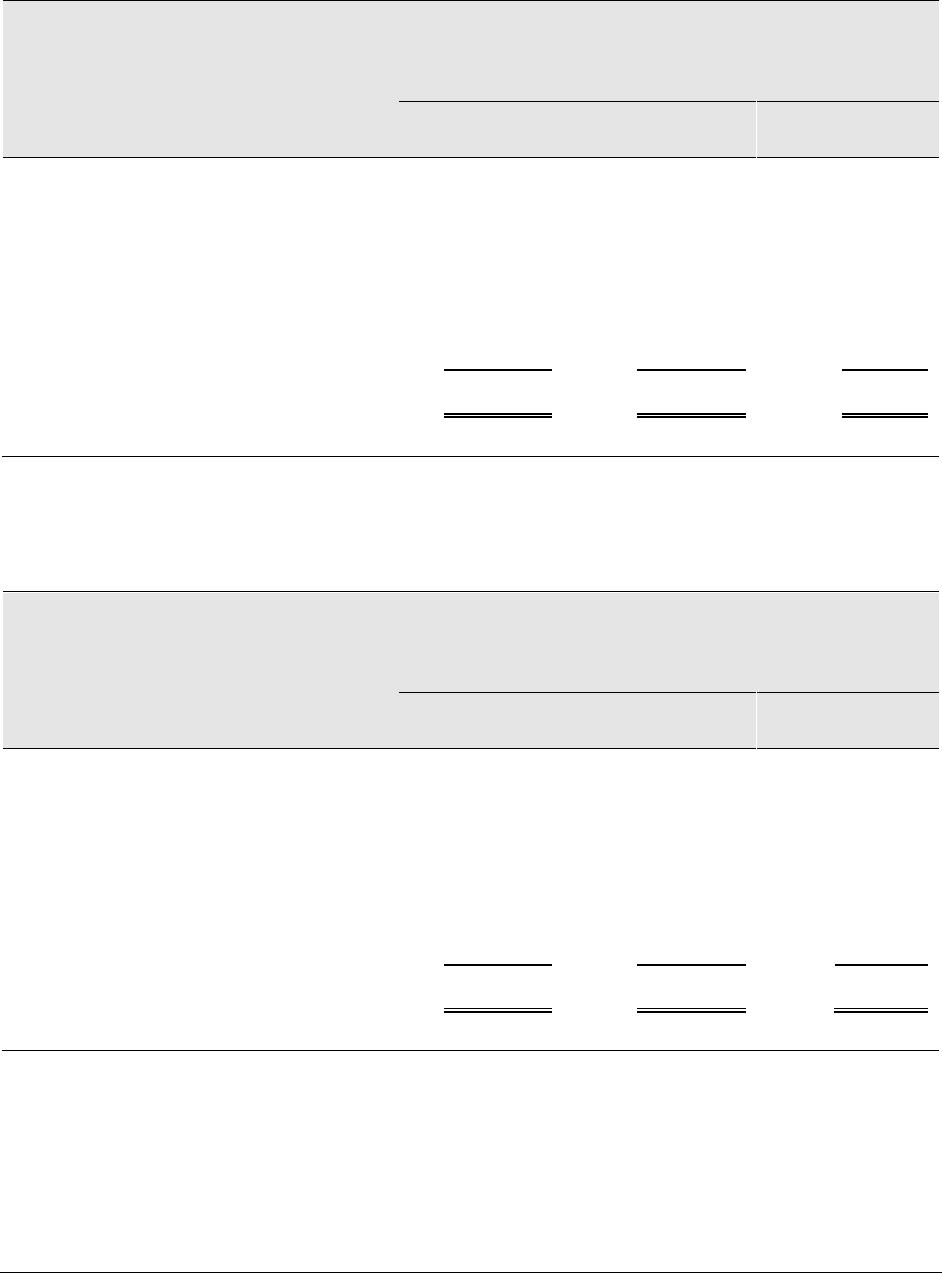

Exercise 24-9 (15 minutes)

Investment Center

Net Income

Sales

Profit Margin

Electronics …………….….

$2,880,000

$40,000,000

7.20%

Investment Center

Sales

Average Assets

Investment

Turnover

Electronics …………….….

$40,000,000

$ 16,000,000

2.50

1.67

Comments: The Sporting goods division generates the most net income

Exercise 24-10 (20 minutes)

1. F 8. P

Exercise 24-11A (15 minutes)

1. If the Trailer division is currently operating at full capacity, its manager

2. If the Trailer division is currently producing 20,000 trailers and the

Assembly division will order 15,000 more trailers, the Trailer division will

3. The Trailer division would prefer a transfer price of $140 per trailer,

since it provides a $60 ($140 – $80) contribution margin per trailer. At a

transfer price of $80 the Trailer division reports a contribution margin of $0

Fundamental Accounting Principles, 21st Edition

1434

Exercise 24-12B (20 minutes)

Preliminary calculations

Land cost ……………………………………………………………..…….

$4,000,000

Improvements ……………………………………………………….

Total cost of lots …………………………………………………..…..

$7,500,000

Lots

Quantity

Price

Total

Canyon …………………………………..

450

$ 55,000

$24,750,000

Hilltop ………………………………..…..

150

Total market value ……………..…..

$41,250,000

Allocated cost—value basis of allocation: $7,500,000

Market

% of

Allocated

Average

Value

Total

Cost

Lot Cost

Canyon section ………...

$24,750,000

60%

$4,500,000

$10,000

$3,000,000

$20,000

Exercise 24-13B (25 minutes)

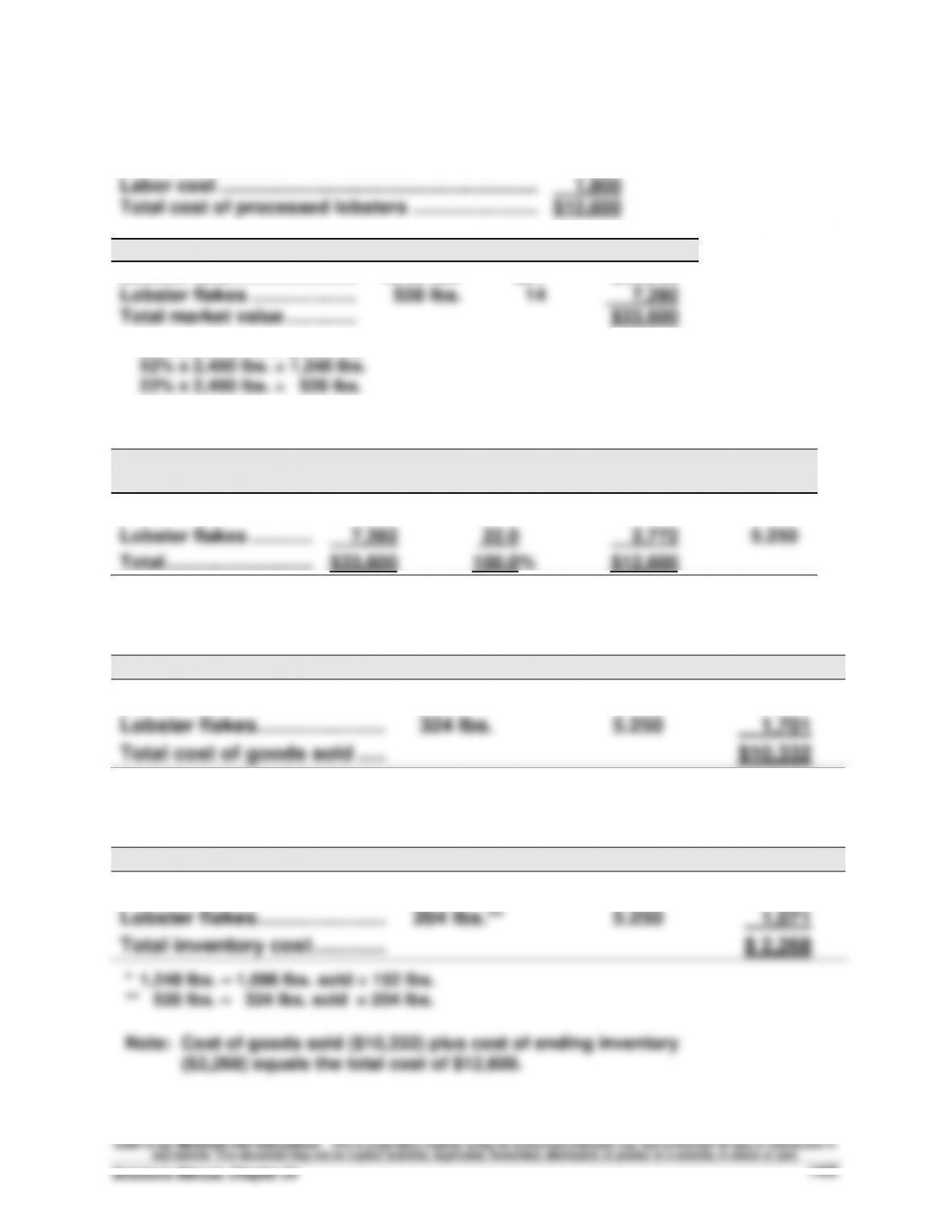

Preliminary calculations

Lobster cost (2,400 lbs. x $4.50) ……………………….

$10,800

Labor cost ……………………………………………………...

Total cost of processed lobsters ……………………..

$12,600

Parts

Quantity*

Price

Total

Lobster tails ……………………..

1,248 lbs.

$21

$26,208

Lobster flakes …………………..

Total market value …………....

$33,600

* Quantities are computed as:

Allocated cost—value basis allocation: $12,600

Market

% of

Allocated

Cost

Parts

Value

Total

Cost

per lb.

Lobster tails …………….….

$26,208

78.0%

$9,828

$7.875

Lobster flakes ………….….

(1) Cost of goods sold

Parts

Quantity (given)

Cost

Total

Lobster tails ……………………....

1,096 lbs.

$7.875

$ 8,631

Lobster flakes…………………....

(2) Cost of ending inventory

Parts

Quantity

Cost

Total

Lobster tails ……………………....

152 lbs.*

$7.875

$ 1,197

Lobster flakes…………………....

Fundamental Accounting Principles, 21st Edition

1436

Exercise 24-14 (20 minutes)

(1) Profit margin = Income/Sales

Investment Center

Income*

Sales*

Profit margin

Professional products ……….

€ 552

€2,717

20.32%

Consumer products …………..

1,765

9,530

18.52%

*In € millions

(2) Investment turnover = Sales/Average invested assets

Investment Center

Sales*

Avg. assets*

Investment

turnover

Professional products ……….

€2,717

€2,570

1.06

4,507

3,855

1.17

*In € millions. Avg. assets = Beginning assets plus ending assets, divided by two.

Note: Profit margin and investment turnover amounts are rounded to two decimal places.

PROBLEM SET A

Problem 24-1A (60 minutes)

Part 1

These costs are assigned to the two departments as follows

Department

Square Footage

Rate

Total

Linder’s Dept. ……………

1,000

$8.25

$ 8,250

Part 2

Market rates are used to allocate occupancy costs for depreciation,

interest, and taxes. Heating, lighting, and maintenance costs are allocated

to the departments on both floors at the average rate per square foot.

These costs are separately assigned to each class as follows:

Total

Costs

Value-Based

Costs

Usage–Based

Costs

Depreciation—Building ………….……

$18,000

$18,000

Interest—Building mortgage ….……

27,000

27,000

Taxes—Building and land ……………

9,000

9,000

3,000

Fundamental Accounting Principles, 21st Edition

1438

Problem 24-1A (Continued)

Value-based costs are allocated to departments in two steps

(i) Compute market value of each floor

Floor

Square

Footage

Value per

Sq. Ft.

Total

First floor ………………..…………

4,000

$30

$120,000

4,000

Total market value …..…………

(ii) Allocate $54,000 to each floor based on its percent of market value

Floor

Market

Value

% of

Total

Allocated

Cost

Cost per

Sq. Ft.

First floor ………………..…………

$120,000

60%

$32,400

$8.10

Totals ……………………..……

$200,000

$54,000

We can then compute total allocation rates for the floors

Floor

Value

Usage

Total

First floor …………………………..

$8.10

$1.50

$9.60

$6.90

These rates are applied to allocate occupancy costs to departments

Department

Square

Footage

Rate

Total

Linder’s Department …………………...

1,000

$9.60

$ 9,600

Part 3

A second-floor manager would prefer allocation based on market value. This is a

reasonable and logical approach to allocation of occupancy costs. The current

Problem 24-2A (70 minutes)

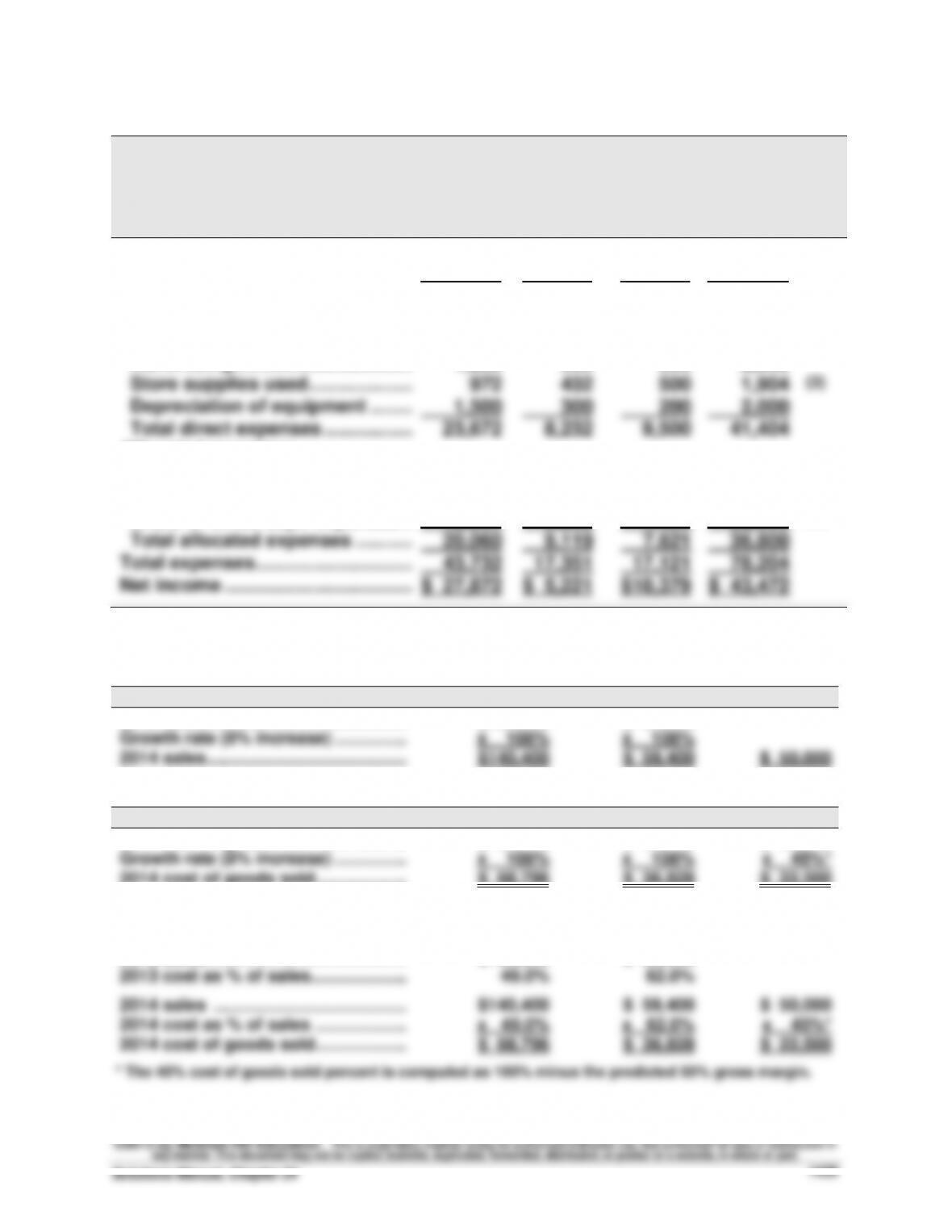

Williams Company

Forecasted Departmental Income Statements

For Year Ended December 31, 2014

Clock

Mirror

Paintings

Combined

Sales …………………………..…………...

$140,400

$59,400

$50,000

$249,800

(1)

Cost of goods sold …………………...

68,796

36,828

22,500

128,124

(2)

Gross profit ……………………………...

71,604

22,572

27,500

121,676

Direct expenses

Sales salaries ………………………….

20,000

7,000

8,000

35,000

Advertising ……………………………..

1,200

500

800

2,500

Store supplies used ………………...

432

500

1,904

(3)

Depreciation of equipment ……...

1,500

300

200

2,000

Total direct expenses ……………...

23,672

8,232

9,500

41,404

Allocated expenses

Rent expense ………………………….

5,616

2,835

2,349

10,800

(4)

Utilities expense ……………………..

2,080

1,048

872

4,000

(4)

Share of office dept. expenses ...

12,364

5,236

4,400

22,000

(5)

Total allocated expenses ………...

20,060

9,119

7,621

36,800

Total expenses ………………………….

43,732

17,351

17,121

78,204

Net income ……………………………….

$ 27,872

$ 5,221

$10,379

$ 43,472

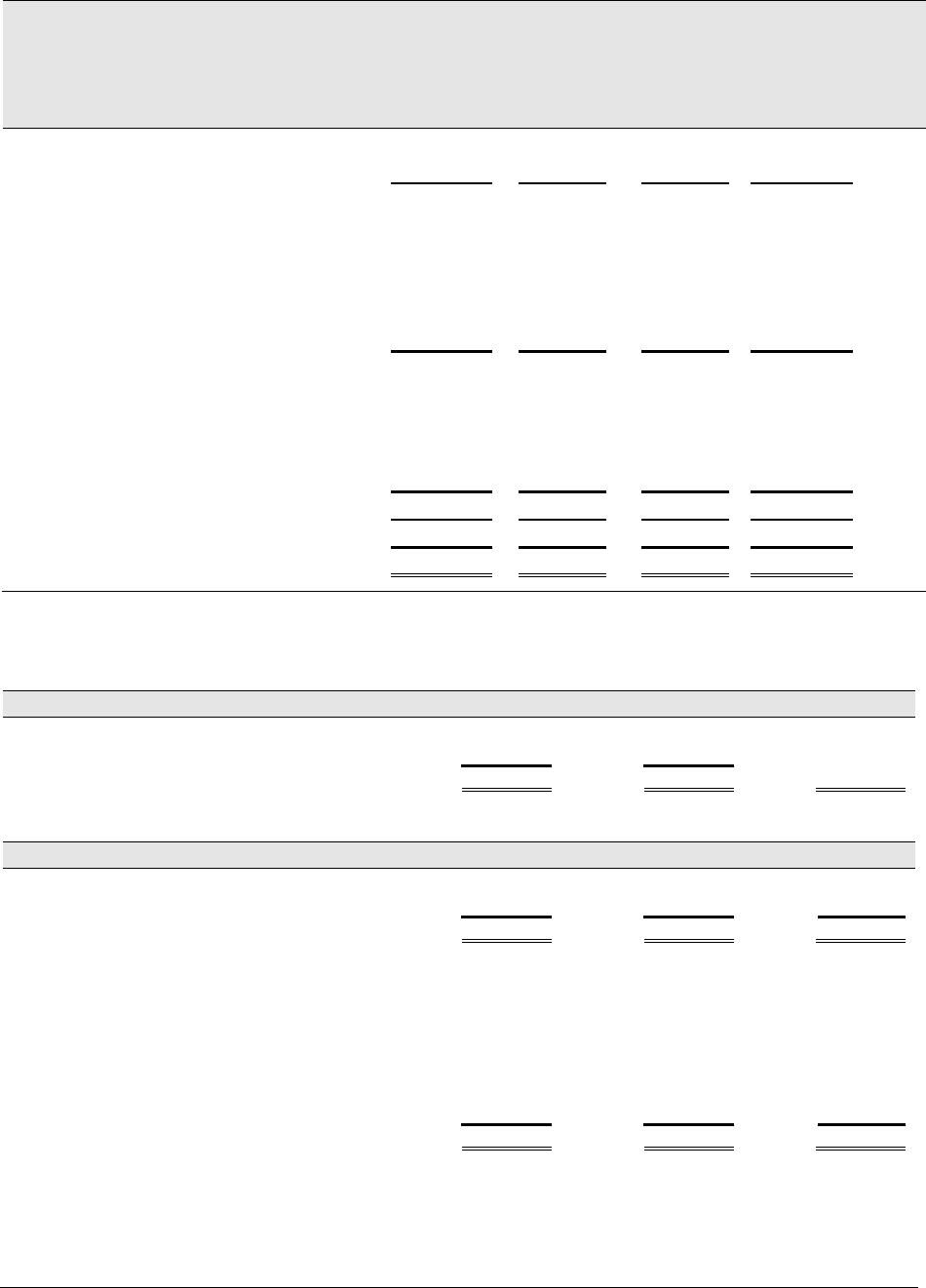

Supporting Computations—coded (1) through (5) in statement above

Note 1 (Sales)

Clock

Mirror

Paintings

2013 sales …………………………………..

$130,000

$ 55,000

2014 sales …………………………………..

$140,400

$ 59,400

$ 50,000

Note 2 (Cost of Goods Sold)

Clock

Mirror

Paintings

2013 cost of goods sold ……………….

$ 63,700

$ 34,100

$ 50,000

2014 cost of goods sold ……………….

$ 68,796

$ 36,828

$ 22,500

ALTERNATIVELY

2013 cost of goods sold ……………….

$ 63,700

$ 34,100

2013 sales …………………………………..

$130,000

$ 55,000

2014 sales ………………………………….

$140,400

$ 59,400

$ 50,000

2014 cost of goods sold ……………….

$ 68,796

$ 36,828

$ 22,500

Fundamental Accounting Principles, 21st Edition

1440

Problem 24-2A (Continued)

Note 3 (Store Supplies Used)

Clock

Mirror

Paintings

2013 store supplies used …………..……

$ 900

$ 400

Growth rate (8% increase) ………….……

x 108%

2014 store supplies …………………..……

$ 972

$ 432

$ 500

Note 4 (Rent and Utilities)

Clock

Mirror

Paintings

2013 rent …………………………………..……

$ 7,020

$ 3,780

One-fifth from clock to paintings

(1,404)

$ 1,404

One-fourth from mirror to

paintings

______

(945)

945

2014 allocation of $10,800 rent …………

$ 5,616

$ 2,835

$ 2,349

Percent of total * ……………………….….

2014 allocation of $4,000

$ 2,080

$ 1,048

$ 872

† Adjusted to eliminate rounding difference.

Note 5 (Office Department Expenses)

Clock

Mirror

Paintings

2014 sales ………………………………………

$140,400

$ 59,400

$ 50,000

Percent of total sales * ……………….……

56.2%

23.8%

20.0%

$ 12,364

$ 5,236

$ 4,400

Problem 24-3A (50 minutes)

Part 1

Responsibility Accounting Performance Report

Dept. Manager, Camper Department

For the Year

Budgeted

Actual

Over (Under)

Amount

Amount

Budget

Controllable Costs

Raw materials ………………………..…

$195,000

$194,200

$ (800)

Employee wages …………………………

104,000

106,600

2,600

Supplies used ………………………..…

b.

Responsibility Accounting Performance Report

Dept. Manager, Trailer Department

For the Year

Budgeted

Actual

Over (Under)

Amount

Amount

Budget

Controllable Costs

Raw materials ………………………..…

$275,000

$273,200

$(1,800)

Employee wages ………………………..

205,000

206,400

1,400

Supplies used ………………………..…

1,600

Fundamental Accounting Principles, 21st Edition

1442

Problem 24-3A (Continued)

c.

Responsibility Accounting Performance Report

Plant Manager, Indiana Plant

For the Year

Budgeted

Actual

Over (Under)

Amount

Amount

Budget

Controllable Costs

Dept. manager salaries ………….…

$ 95,000

$ 97,500

$ 2,500

Utilities ………………………………….…

9,000

8,300

(700)

Building rent …………………………..

15,000

14,000

(1,000)

32,500

30,100

(2,400)

Camper department ……………….…

Part 2

The plant manager did a better job of controlling costs and meeting the

budget. She came in under budget for the plant even though she paid the

Problem 24-4AB (60 minutes)

Part 1

Allocations of joint costs on the basis of sales values

Tree pruning and care: $405,000

Grade

Sales

Value

Percent

of Total

Allocated

Cost

No. 1 ……………….…………

$450,000

48.0%

$194,400

No. 2 ……………….…………

300,000

32.0

129,600

$937,500

$405,000

Picking, sorting, and grading: $202,500

Grade

Sales

Value

Percent

of Total

Allocated

Cost

No. 1 ……………….…………

$450,000

48.0%

$ 97,200

No. 2 ……………….…………

300,000

32.0

64,800

Delivery: $30,000 to Grade Nos. 1 & 2

Grade

Sales

Value

Percent

of Total

Allocated

Cost

No. 1 ……………….…………

$450,000

60.0%

$18,000

No. 2 ……………….…………

300,000

40.0

12,000

$750,000

$67,500

Fundamental Accounting Principles, 21st Edition

1444

Problem 24-4AB (Continued)

Part 2

GEORGIA ORCHARDS

Income Statement

For Year Ended December 31, 2013

No. 1

No. 2

No. 3

Combined

Sales (by grade)

No. 1: 300,000 lbs. @ $1.50 …….…..

$450,000

No. 2: 300,000 lbs. @ $1.00 …….…..

$300,000

No. 3: 750,000 lbs. @ $0.25 …….…..

$187,500

Total sales …………………………….…..

$937,500

Costs

Tree pruning and care ………………..

194,400

129,600

81,000

405,000

Delivery ……………………………………..

Net income (loss) …………………….…..

$140,400

$ 93,600

$ 28,500

$262,500

Part 3

Delivery costs include both crating and hauling costs. Georgia is able to

identify the portion of the cost directly related to the No. 3 peaches,

presumably because the No. 3s are going to a different destination than the