24-1

CHAPTER 24

PERFORMANCE MEASUREMENT AND

RESPONSIBILITY ACCOUNTING

Related Assignment Materials

Student Learning Objectives

Discussion

Questions

Quick

Studies*

Exercises*

Problems*

Beyond the

Numbers

Conceptual objectives:

C1. Distinguish between direct and

indirect expenses and identify

bases for allocating indirect

expenses to departments

1,2,3,4,5,

6,7,8,9,11,

15,16

24-1, 24-2,

24-3

24-1, 24-8

C2. Appendix 24A—Explain transfer

pricing and methods to set

transfer prices.

12

24-11, 24-12

24-11

C3. Appendix 24B—Describe

allocation of joint costs across

products.

13,14

24-13

24-12, 24-13

24-4

Analytical objectives:

A1. Analyze investment centers

using return on total assets and

residual income.

24-5, 24-6,

24-15

24-7, 24-8

A2. Analyze investment centers

using profit margin and

investment turnover

24-7, 24-8

24-9, 24-14

24-2

A3. Analyze investment centers

using the balance scorecard

24-9, 24-10

24-10

A4. Compute cycle time and cycle

efficiency, and explain their

importance to production

management.

17,18, 19,

20

24-5

Procedural objectives:

P1. Prepare a responsibility report

for a cost center

24-2

24-3

24-6, 24-8

P2. Allocate indirect expenses to

departments

24-14

24-1, 24-4,

24-5, 24-6

24-1

24-4, 24-5

P3. Prepare departmental income

statements and contribution

reports

10

24-3

24-3

24-2

24-3, 24-7,

24-9

*See additional information on next page that pertains to these quick studies, exercises and

problems.

Additional Information on Related Assignment Material

Connect (Available on the instructor’s course-specific website) repeats all numerical Quick Studies, all

Exercises and Problems Set A. Connect provides new numbers each time the Quick Study, Exercise or

Problem is worked. It allows instructors to monitor, promote, and assess student learning. It can be used

in practice, homework, or exam mode.

Corresponding problems in set B also relate to learning objectives identified in grid on previous page.

Problems 24-1A and 24-2A can be completed using Excel. The Serial Problem for Success Systems

starts in this chapter and continues throughout many chapters of the text. It is most readily solved

manually if you use the working papers that accompany text.

Synopsis of Chapter Revisions

▪ United By Blue: NEW opener with new entrepreneurial assignment

▪ Was Chapter 21 in prior edition

▪ Moved section on two-stage allocation and activity-based costing methods to (new)

Appendix C

▪ Revised discussion linking direct and indirect expenses to controllable and

uncontrollable costs

▪ Highlighted 4-step process to prepare departmental income statements

▪ Moved discussion and illustration of profit margin and investment turnover to main body

of chapter

▪ Added discussion on cycle time and cycle efficiency

▪ New exhibit on how to prepare departmental performance reports

▪ Edited discussion of example on preparing departmental performance reports

▪ New discussion on issues in computing return on (assets) investment and residual

Chapter Outline

I. Responsibility Accounting⎯A responsibility accounting system can be

set up to control costs and expenses and to evaluate managers’

performance by assigning costs and expenses to the managers

responsible for controlling them.

A. Motivation for Departmentalization

1. divide large and complex companies into subunits (or divisions)

when too large.

2. Divisions are organized into separate departments.

3. Each department placed under direction of a manager.

departments.

a. Operating departments perform the organization’s main

functions. Examples: production and selling departments.

b. Service departments provide support to an organization’s

operating departments. Examples: payroll, human resources

B. Departmental Evaluation

1. Prepared for internal managers to help control operations,

appraise performance, allocate resources, and plan strategy.

2. More companies are emphasizing customer satisfaction as main

responsibility of each operating department.

b. Cost center⎯incurs cost or expenses without directly

generating revenues (e.g. manufacturing department and

service department).

c. Investment center⎯incurs costs, generates revenues and is

responsible for effectively using center assets.

4. Basis for evaluating performance:

a. Profit center: ability to generate more revenue than

Notes

24-4

Chapter Outline

II. Responsibility Accounting for Cost Centers

A. Controllable versus Uncontrollable Costs

1. A manager’s performance is evaluated using responsibility

reports that describe the department’s activities in terms of

3. A cost is uncontrollable if it is not within the manager’s control

4. Distinguishing between controllable and uncontrollable costs

analysis.

5. All costs are controllable at some level of management if the

time period is sufficiently long;

6. Good judgment is required when identifying controllable costs.

B. Responsibility Accounting System

responsibility for costs and expenses under their control.

2. Responsibility accounting budgets identify costs and expenses

under the manager’s control; typically based on flexible

budgeting approach shown in Chapter 23

3. Responsibility accounting performance reports (See Exhibit

24.2):

a. Accumulate and report costs for which a manager is

responsible and their budgeted amounts.

budget often results in corrective actions.

c. Used by upper management to evaluate effectiveness of

lower-level managers in controlling costs.

4. Recognizes that control over costs and expenses belongs to

A. The responsibility report focuses on how well each department

controlled costs and generated revenues.

B. The departmental income statement is a common way to report

profit center performance.

C. When computing department profits, challenges involve allocating

expenses across operating departments

Notes

2. Indirect Expenses are typically considered uncontrollable costs:

a. Incurred for joint benefit of more than one department; can’t

be readily traced to just one department.

b. Allocated across departments benefiting from them.

c. Ideally allocated using a cause-effect relation or, if cause-

effect relation cannot be identified, allocated on a basis

approximating the benefit received by each department.

E. Allocation of Indirect Expenses⎯no standard rule identifies the best

basis; judgment required.

1. Wages and salaries:

a. Direct expense of the department if time spent entirely in

one department; otherwise indirect.

b. Basis for allocating when indirect:

3. Advertising⎯Departmental portion of total sales, or by

newspaper space or TV/radio time devoted to products of each

department.

5. Utilities⎯portion of floor space occupied by departments (if

used uniformly); otherwise more complicated.

F. Departmental Income Statements

1. Departmental income statements are prepared after all expenses

have been assigned to the departments.

allocated to the operating departments.

24-6

Chapter Outline

2. Four Steps for allocating costs and preparing departmental

income statements.

a. Step one – accumulate revenues and direct expenses for

each service and selling department.

i. Cost centers do not generate revenues

ii. Direct expenses include wages, salaries, and other

expenses that a department incurs but does not share

with any other department.

b. Step two – allocate indirect expenses across all service and

operating departments

i. Can include items such as depreciation, rent, advertising

and other expenses than can’ not be assigned to a

department.

ii. The indirect expenses are recorded in company accounts

and an allocation based is identified to allocate the costs

to the departments on a departmental expense allocation

spreadsheet

expenses are a large portion of total expenses.

2. Evaluate using departmental contributions to overhead⎯a report

of the amount of sales less direct expenses (indirect expenses are

Notes

24-7

Chapter Outline

IV. Evaluating Investment Center Performance

A. Financial Performance Evaluation Measures

1. Assesses how well center manager has utilized center’s

productive assets to generate income.

computed as:

Investment center net income

Investment center average invested assets

4. Investment center residual income is computed as:

*target net income : Hurdle rate x average invested assets

hurdle rate: typically the cost to obtain financing

5. Using residual income encourages managers to accept all

1. Evaluating performance solely on financial measures has

limitations.

centers of different size.

c. Return on investment and residual income can encourage

managers to focus too heavily on short-term financial goals.

b. Internal process: which of our operations are critical?

c. Innovation and learning: how can we improve?

d. Financial: what do our owners think of us?

e. Exhibit 24.21 lists common performance measures.

Notes

V. Appendix 24A – Transfer Pricing

A. The price used to record transfers between divisions in the same

company is called a transfer price.

1. If there is no excess capacity, the internal supplier will not

accept a transfer price less than the market price. This is called

market based transfer pricing.

2. If there is excess capacity, the internal supplier should accept a

price between the cost to manufacturer the part and the market

price. This is called cost based transfer pricing

3. Other issues to consider in determining transfer prices include:

a. Market price may not exist

b. Cost controls

c. Division managers’ negotiation

d. Nonfinancial factors to consider include: quality control,

reduced lead times and impact on employee morale.

products at the same time; similar to indirect expense in that it’s

shared across more than one cost object.

2. Allocated to different products produced from it when total cost

of each product must be estimated (e.g., preparation of GAAP

financial statements).

3. Allocation bases

Notes

24-9

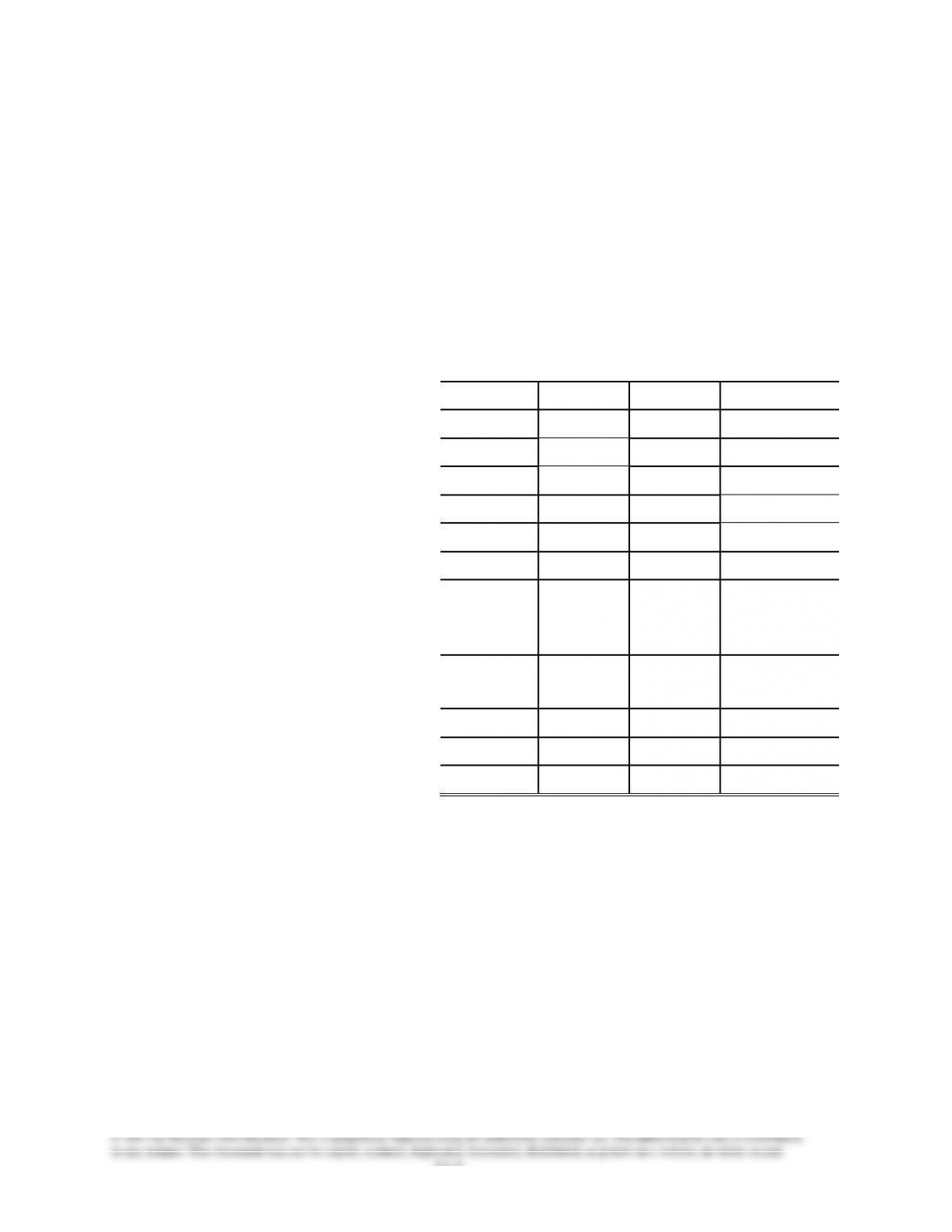

Alternate Demo Problem Chapter Twenty-Four

Jack and Susan Roberts own a farm that produces potatoes. Based on a

review of the income statement shown below, Jack remarked that they

should have fed the No. 3 potatoes to the pigs; then they would have

avoided the loss from the sale of the those potatoes.

JACK AND SUSAN ROBERTS

Income from the Production and Sale of Potatoes

For Year Ended December 31, 20xx

Results by Grade

No. 1

No. 2

No. 3

Combined

Sales by grades:

No. 1, 300,000 lbs. $0.045 per lb.

$13,500

No. 2, 500,000 lbs. $0.04 per lb.

$20,000

No. 3, 200,000 lbs. $0.03 per lb.

$6,000

Combined

$39,500

Costs:

Land preparation, seed,

planting,

cultivating @ $0.01422 per lb.

4,266

7,110

2,844

14,220

Harvesting, sorting, grading

@ $0.01185 per lb.

3,555

5,925

2,370

11,850

Marketing @ $0.00415 per lb.

1,245

2,075

830

4,150

Total costs

9,066

15,110

6,044

30,220

Net income (or loss)

$4,434

$4,890

($44)

$9,280

Jack and Susan divided their costs among the grades on a per pound

basis, because their records do not show cost per grade. However, their

records did show that $4,020 of the $4,150 of marketing costs represented

the cost of placing the No. 1 and No. 2 potatoes in bags and hauling them

to the warehouse of the produce buyer. Bagging and hauling costs were

the same for both grades. The remaining $130 represented the cost of

loading the No. 3 potatoes into the trucks of the potato starch factory that

bought these potatoes in bulk and picked them up at the farm.

Required:

Prepare an income statement that will better show the results of producing

and marketing the each of the grades of potatoes.

24–10

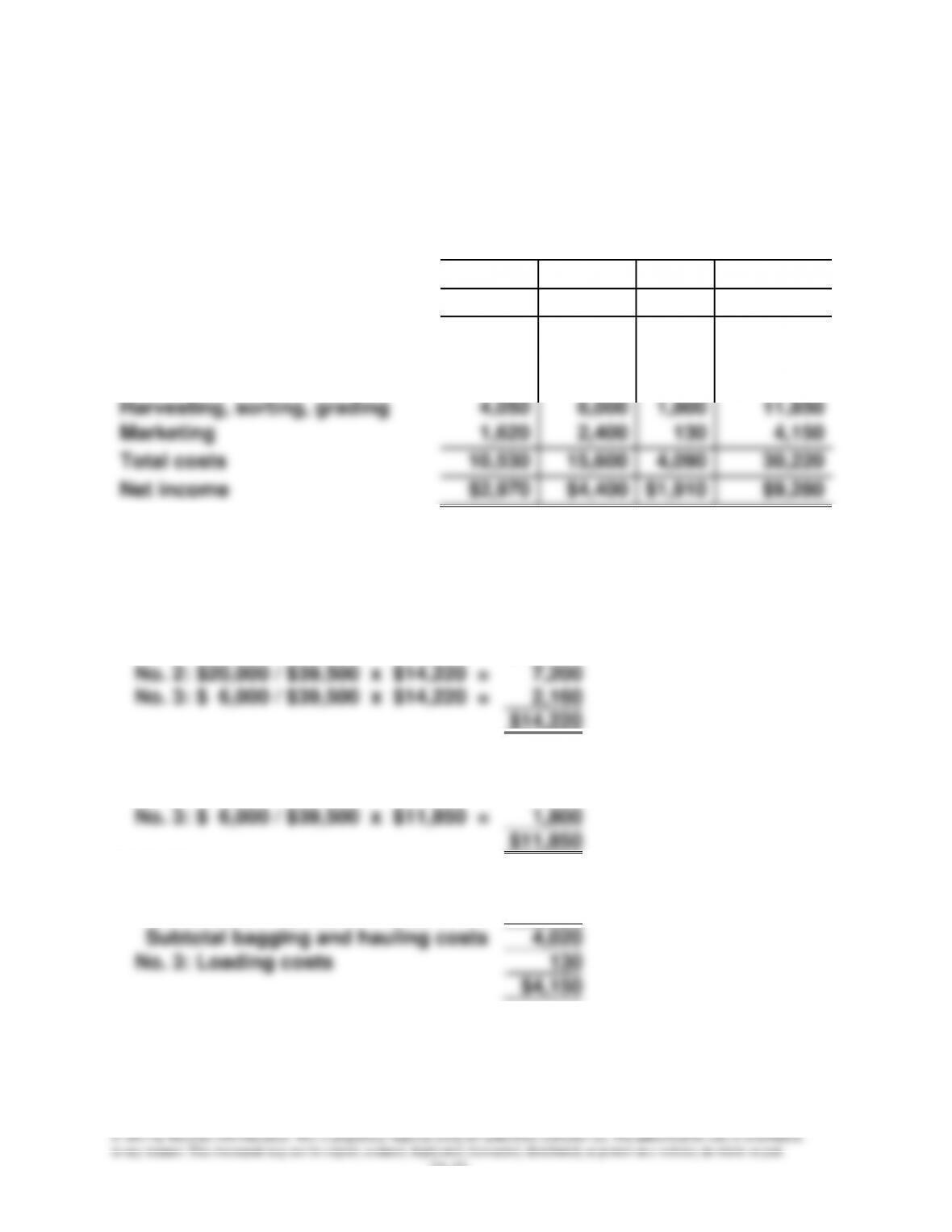

Solution: Alternate Demo Problem Chapter Twenty-Four

JACK AND SUSAN ROBERTS

Income from the Production and Sale of Potatoes

For Year Ended December 31, 20xx

Results by Grade

No. 1

No. 2

No. 3

Combined

Revenue from sales:

$13,500

$20,000

$6,000

$39,500

Costs:

Land preparation, seed,

planting, cultivating

4,860

7,200

2,160

14,220

Harvesting, sorting, grading

4,050

6,000

1,800

11,850

Marketing

1,620

2,400

130

4,150

Total costs

10,530

15,600

4,090

30,220

Net income

$2,970

$4,400

$1,910

$9,280

COST ALLOCATIONS

Land preparation, seed, planting, and

cultivating:

No. 1: $13,500 / $39,500 x $14,220 =

No. 2: $20,000 / $39,500 x $14,220 =

No. 3: $ 6,000 / $39,500 x $14,220 =

$ 4,860

7,200

2,160

$14,220

Harvesting, sorting, and grading:

No. 1: $13,500 / $39,500 x $11,850 =

No. 2: $20,000 / $39,500 x $11,850 =

No. 3: $ 6,000 / $39,500 x $11,850 =

$ 4,050

6,000

1,800

$11,850

Marketing:

No. 1: $13,500 / $33,500 x $4,020 =

No. 2: $20,000 / $33,500 x $4,020 =

$1,620

2,400

Subtotal bagging and hauling costs

4,020

No. 3: Loading costs

130

$4,150