Chapter 6

Inventories and Cost of Sales

QUESTIONS

1. (a) FIFO: The cost of the first (earliest) items purchased in inventory flow to cost of

2. Merchandise inventory is disclosed on the balance sheet as a current asset. It is

3. Incidental costs sometimes are ignored in computing the cost of inventory because

the expense of tracking such costs on a precise basis can outweigh the benefits

5. The full-disclosure principle requires that the nature of the accounting change, the

justification for the change, and the effect of the change on net income be disclosed

in the notes or in the body of a company’s financial statements.

8. Many people make important business decisions based on period-to-period

fluctuations in a company’s financial numbers, including gross profit and net

income. As such, inventory errors—which can substantially impact gross profit, net

9. An inventory error that causes an understatement (or overstatement) for net income

in one accounting period, if not corrected, will cause an overstatement (or

10. Market usually means replacement cost of inventory when applied in the LCM.

11. The accounting constraint of conservatism guides preparers of accounting reports

12. Factors that contribute to inventory shrinkage are breakage, loss, deterioration,

decay, and theft.

15. Cost of goods available for sale equals ending inventory plus cost of sales. As of

16. Cost of goods available for sale equals ending inventory plus cost of sales. As of

17. Merchandise inventory (EUR thousands) comprises 46.5% (236,988 / 509,708) of

QUICK STUDIES

Quick Study 6-1 (10 minutes)

FIFO—Perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

1/1

320 @ $3.00

= $ 960.00

1/9

80 @ $3.20

320 @ $3.00

80 @ $3.20

= $1,216.00

1/25

100 @ $3.34

320 @ $3.00

80 @ $3.20

= $1,550.00

100 @ $3.34

1/26

320 @ $3.00 =$ 960.00

30 @ $3.20 = 96.00

50 @ $3.20

$1,056.00

100 @ $3.34

= $ 494.00

Alternate solution format

FIFO:

100

@ $3.34 =

$ 334.00

50

@ $3.20 =

160.00

150

$ 494.00

Ending inventory cost

Quick Study 6-2 (10 minutes)

LIFO—Perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

1/1

320 @ $3.00

= $ 960.00

1/9

80 @ $3.20

320 @ $3.00

80 @ $3.20

= $1,216.00

1/25

100 @ $3.34

320 @ $3.00

80 @ $3.20

= $1,550.00

100 @ $3.34

1/26

100 @ $3.34 =$ 334.00

80 @ $3.20 = 256.00

170 @ $3.00 = 510.00

150 @ $3.00

= $ 450.00

$1,100.00

Alternate solution format

LIFO:

150

@ $3.00 =

$ 450.00

Ending inventory cost

}

}

}

}

}

Quick Study 6-3 (10 minutes)

Weighted Average—Perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

1/1

320 @ $3.00

= $ 960.00

1/9

80 @ $3.20

320 @ $3.00

80 @ $3.20

= $1,216.00

(avg. cost is $3.04)

1/25

100 @ $3.34

320 @ $3.00

80 @ $3.20

= $1,550.00

100 @ $3.34

(avg. cost is $3.10)

1/26

350 @ $3.10 = $1,085.00

150 @ $3.10

= $ 465.00

Alternate solution format

Weighted average:

320

@ $3.00 =

$ 960.00

80

@ $3.20 =

256.00

100

@ $3.34 =

334.00

500

$1,550.00

Cost of goods available for sale

$1,550.00/500 = $3.10 weighted average cost per unit

150 units @ $3.10 = $ 465.00 Ending inventory cost

Quick Study 6-4A (10 minutes)

Ending Cost of

FIFO—Periodic Inventory Goods Sold

FIFO

Quick Study 6-5A (10 minutes)

Ending Cost of

LIFO—Periodic Inventory Goods Sold

LIFO

}

}

Quick Study 6-6A (10 minutes)

Ending Cost of

Weighted Average—Periodic Inventory Goods Sold

Weighted Average ($1,550/ 500 = $3.10 cost per unit)

Quick Study 6-7 (10 minutes)

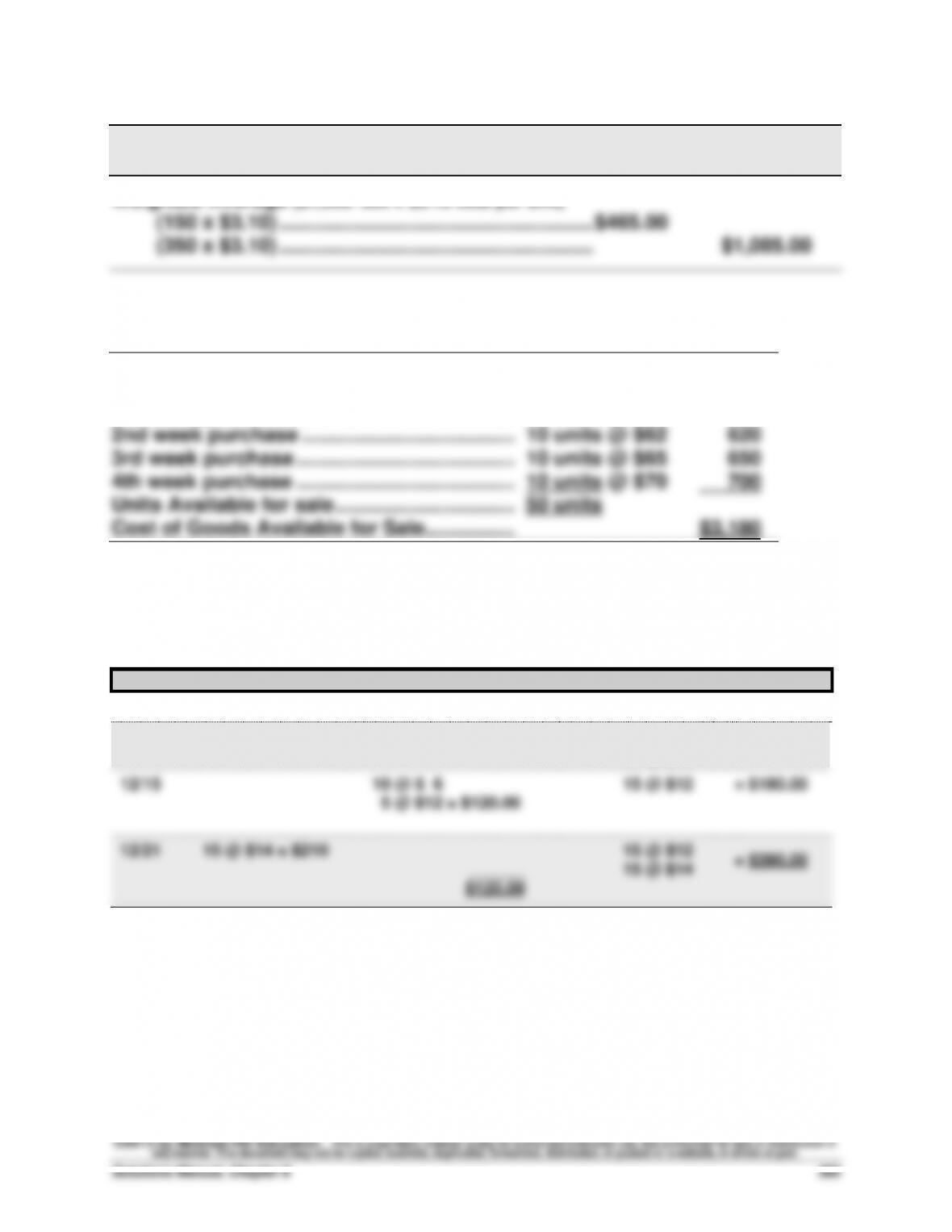

Beginning inventory ……………………………….

10 units @ $60

$ 600

Plus

1st week purchase …………………………………

10 units @ $61

610

2nd week purchase ………………………………..

10 units @ $62

620

3rd week purchase …………………………………

10 units @ $65

650

4th week purchase …………………………………

10 units @ $70

700

Units Available for sale …………………………..

50 units

Cost of Goods Available for Sale …………….

$3,180

Quick Study 6-8 (25 minutes)

FIFO—Perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

12/ 7

10 @ $ 6 = $ 60

10 @ $ 6

= $ 60.00

12/14

20 @ $12 = $240

10 @ $ 6

= $300.00

20 @ $12

12/15

10 @ $ 6

15 @ $12

= $180.00

5 @ $12 = $120.00

12/21

15 @ $14 = $210

15 @ $12

= $390.00

______

15 @ $14

$120.00

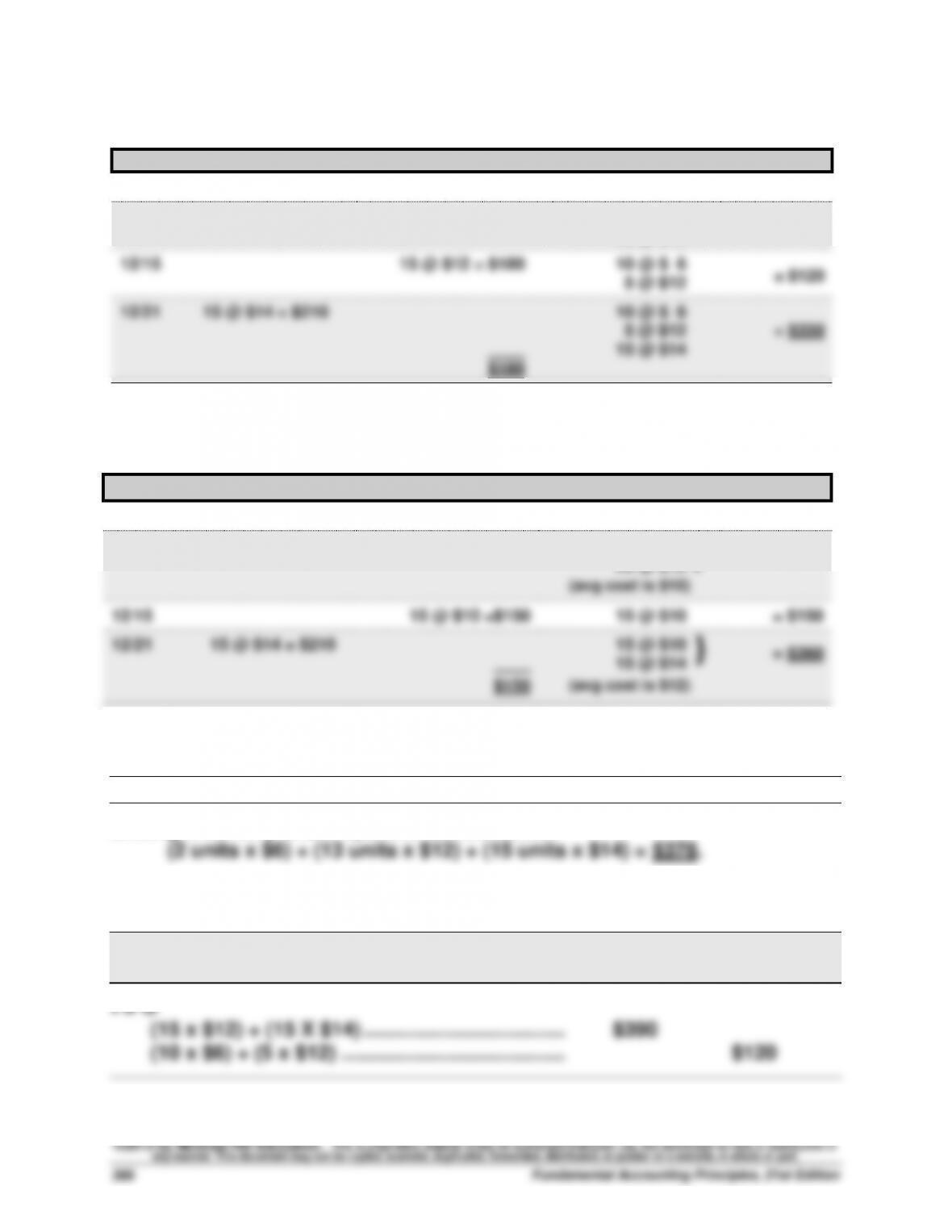

Quick Study 6-9

LIFO—Perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

12/7

10 @ $ 6 = $ 60

10 @ $ 6

= $ 60

12/14

20 @ $12 = $240

10 @ $ 6

= $300

20 @ $12

12/15

15 @ $12 = $180

10 @ $ 6

= $120

5 @ $12

12/21

15 @ $14 = $210

10 @ $ 6

5 @ $12

= $330

____

15 @ $14

$180

Quick Study 6-10

Weighted Average—Perpetual

Quick Study 6-11

Specific Identification—Perpetual

Ending inventory under specific identification:

Quick Study 6-12A (10 minutes)

Ending Cost of

FIFO—Periodic Inventory Goods Sold

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

12/7

10 @ $6 = $60

10 @ $6

= $ 60

12/14

20 @ $12 = $240

10 @ $6

= $300

20 @ $12

(avg cost is $10)

12/15

15 @ $10 =$150

15 @ $10

= $150

12/21

15 @ $14 = $210

15 @ $10

= $360

____

15 @ $14

$150

(avg cost is $12)

}

}

Quick Study 6-13A (10 minutes)

Ending Cost of

LIFO—Periodic Inventory Goods Sold

LIFO

Quick Study 6-14A (10 minutes)

Ending Cost of

Weighted Average—Periodic Inventory Goods Sold

Weighted Average ($510/ 45 = $11.33 cost per unit)*

*If unit cost is not rounded, then ending inventory is $340 and goods sold is $170.

Quick Study 6-15A (10 minutes)

Ending Cost of

Specific Identification—Periodic Inventory Goods Sold

Specific Identification

Quick Study 6-16 (10 minutes)

Quick Study 6-17 (10 minutes)

Units in ending inventory

Units stored in basement …………………………..

1,300

units

Less damaged (unsalable) units ……………….……

(20)

Plus units in transit ………………………………….……

350

Plus units on consignment …………………………..

80

Total units in ending inventory ………………………

1,710

units

Quick Study 6-18 (10 minutes)

Cost ……………………………………………………….

$14,000

Plus

Transportation-in ………………………………….……

250

Import duties ………………………………………..……

900

Insurance ……………………………………………..……

300

Inventory Cost ……………………………………..……

$15,450

The $150 advertising cost and the $1,250 cost for sales staff salaries are

Quick Study 6-19 (20 minutes)

Per Unit

Total

Total

LCM –

Items

Inventory Items

Units

Cost

Market

Cost

Market

Mountain bikes

11

$600

$550

$ 6,600

$ 6,050

$ 6,050

Skateboards

13

350

425

4,550

5,525

4,550

Gliders

26

800

700

20,800

18,200

18,200

$31,950

$29,775

$28,800

LCM applied to each product ………………………………………………

$28,800

Quick Study 6-20 (15 minutes)

a. Overstates 2013 cost of goods sold.

b. Understates 2013 gross profit.

Quick Study 6-21 (10 minutes)

Inventory turnover = Cost of goods sold/Average merchandise inventory

= $1,200,000 / [($150,000 + $180,000)/2 ] = 7.27 times

Quick Study 6-22B (15 minutes)

Goods available for sale

Inventory, January 1 …………………………………………….…………

$190,000

Cost of goods purchased (net) ……………………………..………………

352,000

Goods available for sale (at cost) …………………………..

542,000

Net sales at retail ……………………………………………………….

$685,000

Estimated cost of goods sold [$685,000 x (1 – 44%)] ……..………………

(383,600)

Estimated September 5 inventory destroyed …………..………………

$158,400

Quick Study 6-23 (10 minutes)

a. Both IFRS and U.S. GAAP provide broad and similar guidance on the

accounting for items and costs making up merchandise inventory.

b. Yes, companies reporting under IFRS can apply cost flow assumptions

c. U.S. GAAP prohibits any later increase in the recorded value of

inventory that had been written down even if that decline in value is

EXERCISES

Exercise 6-1 (10 minutes)

1. The consignor is Harris Company. The consignee is Harlow Company.

2. The title will pass at “destination” which is Harlow Company’s receiving

Exercise 6-2 (10 minutes)

Cost of inventory (estate’s contents)

Price …………………………………………………………………………….

$75,000

Transportation-in ………………………………………………………….

2,400

Insurance on shipment ………………………………………………….

300

Cleaning and refurbishing ……………………………………………..

980

Total cost of inventory …………………………………………………..

$78,680

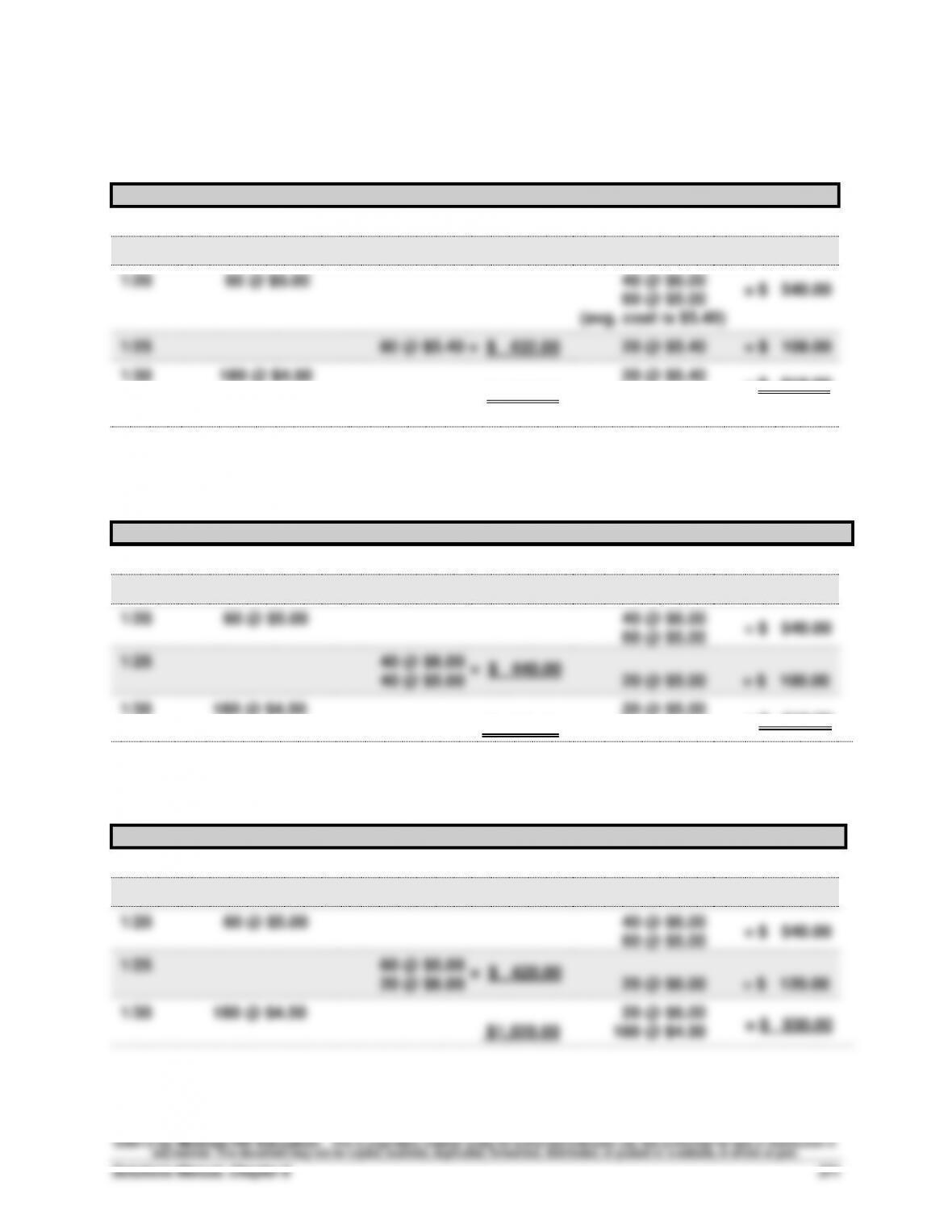

Exercise 6-3 (45 minutes)

a. Specific identification

Ending inventory—180 units from January 30, 5 units from January 20, and 15

units from beginning inventory

Ending Cost of

Specific Identification Inventory Goods Sold

Exercise 6-3 (continued)

b. Weighted Average—Perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

1/1

140 @ $6.00

= $ 840.00

1/10

100 @ $6.00 = $ 600.00

40 @ $6.00

= $ 240.00

1/20

60 @ $5.00

40 @ $6.00

= $ 540.00

60 @ $5.00

(avg. cost is $5.40)

1/25

80 @ $5.40 = $ 432.00

20 @ $5.40

= $ 108.00

1/30

180 @ $4.50

20 @ $5.40

= $ 918.00

$1,032.00

180 @ $4.50

(avg. cost is $4.59)

c. FIFO—Perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

1/1

140 @ $6.00

= $ 840.00

1/10

100 @ $6.00 = $ 600.00

40 @ $6.00

= $ 240.00

1/20

60 @ $5.00

40 @ $6.00

= $ 540.00

60 @ $5.00

1/25

40 @ $6.00

40 @ $5.00

20 @ $5.00

= $ 100.00

1/30

180 @ $4.50

20 @ $5.00

= $ 910.00

$1,040.00

180 @ $4.50

d. LIFO—Perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

1/1

140 @ $6.00

= $ 840.00

1/10

100 @ $6.00 = $ 600.00

40 @ $6.00

= $ 240.00

1/20

60 @ $5.00

40 @ $6.00

= $ 540.00

60 @ $5.00

1/25

60 @ $5.00

20 @ $6.00

20 @ $6.00

= $ 120.00

1/30

180 @ $4.50

20 @ $6.00

= $ 930.00

$1,020.00

180 @ $4.50

= $ 440.00

= $ 420.00

Exercise 6-3 (Concluded)

Alternate Solution Format for FIFO and LIFO Perpetual

Ending Cost of

Computations Inventory Goods Sold

c. FIFO

(180 x $4.50) + (20 x $5.00) ……………………………………….. $ 910.00

(100 x $6.00) + (40 x $6.00) + (40 x $5.00) ………………….. $1,040.00

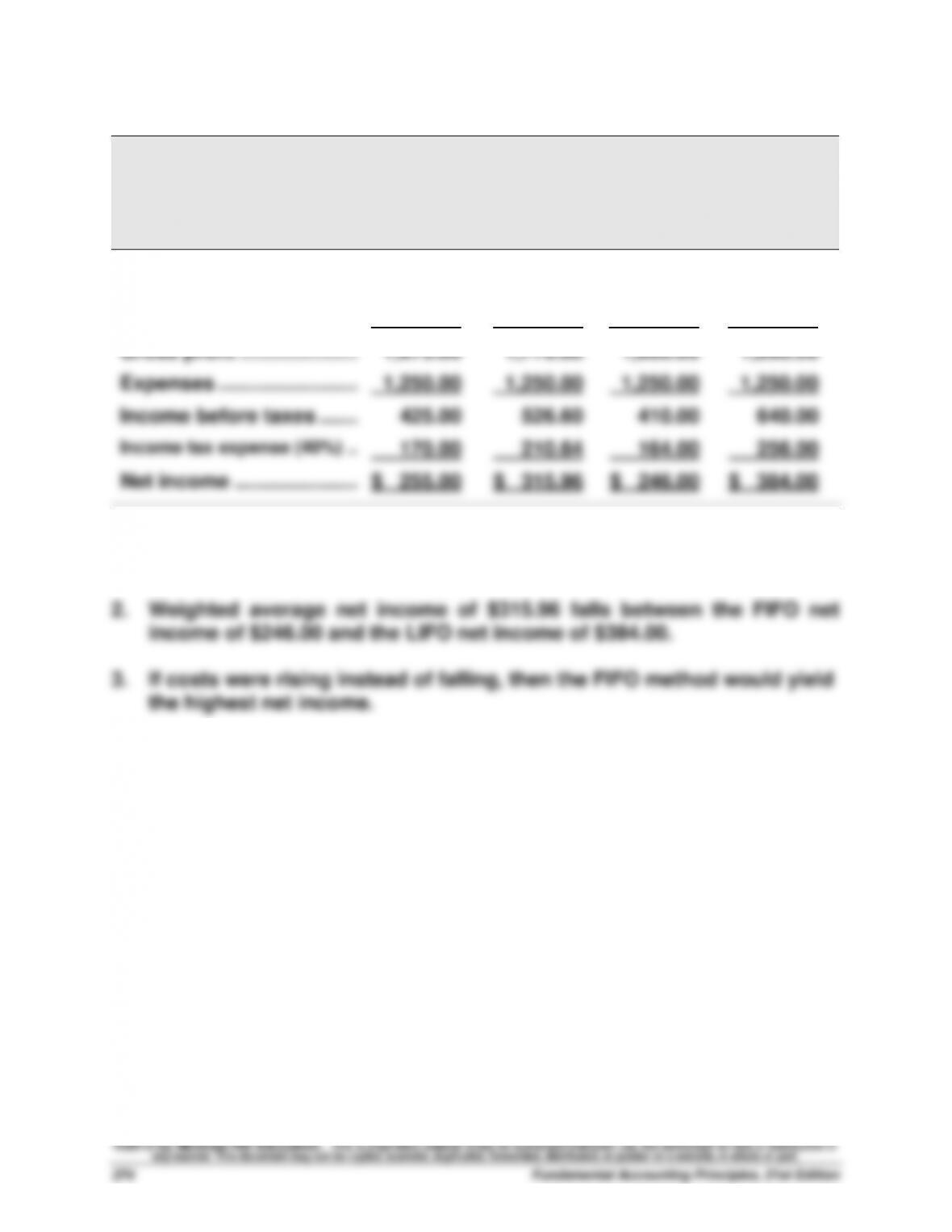

Exercise 6-4 (20 minutes)

LAKER COMPANY

Income Statements

For Month Ended January 31

Specific

Identification

Weighted

Average

FIFO

LIFO

Sales …………………………...…..

$2,700.00

$2,700.00

$2,700.00

$2,700.00

(180 units x $15 price)

Cost of goods sold …………..

1,025.00

1,032.00

1,040.00

1,020.00

Gross profit ……………………..

1,675.00

1,668.00

1,660.00

1,680.00

Expenses …………………….…..

1,250.00

1,250.00

1,250.00

1,250.00

Income before taxes …….…..

425.00

418.00

410.00

430.00

Income tax expense (40%) ..……

170.00

167.20

164.00

172.00

Net income ………………….…..

$ 255.00

$ 250.80

$ 246.00

$ 258.00

1. LIFO method results in the highest net income of $258.00.

Exercise 6-5A (35 minutes)

Ending Cost of

Periodic Inventory Computations Inventory Goods Sold

a. Specific Identification—Periodic

b. Weighted Average—Periodic

c. FIFO—Periodic

(180 x $4.50) + (20 x $5.00) …………………………….. $ 910.00

(140 x $6.00) + (40 x $5.00) …………………………….. $1,040.00

d. LIFO—Periodic

*rounded to dollars and cents

Exercise 6-6 (20 minutes)

LAKER COMPANY

Income Statements

For Month Ended January 31

Specific

Identification

Weighted

Average

FIFO

LIFO

Sales …………………………...…..

$2,700.00

$2,700.00

$2,700.00

$2,700.00

(180 units x $15 price)

Cost of goods sold …………..

1,025.00

923.40

1,040.00

810.00

Gross profit ……………………..

1,675.00

1,776.60

1,660.00

1,890.00

Expenses …………………….…..

1,250.00

1,250.00

1,250.00

1,250.00

Income before taxes …….…..

425.00

526.60

410.00

640.00

Income tax expense (40%) ..……

170.00

210.64

164.00

256.00

Net income ………………….…..

$ 255.00

$ 315.96

$ 246.00

$ 384.00

1. LIFO method results in the highest net income of $384.00.

Exercise 6-7 (20 minutes)

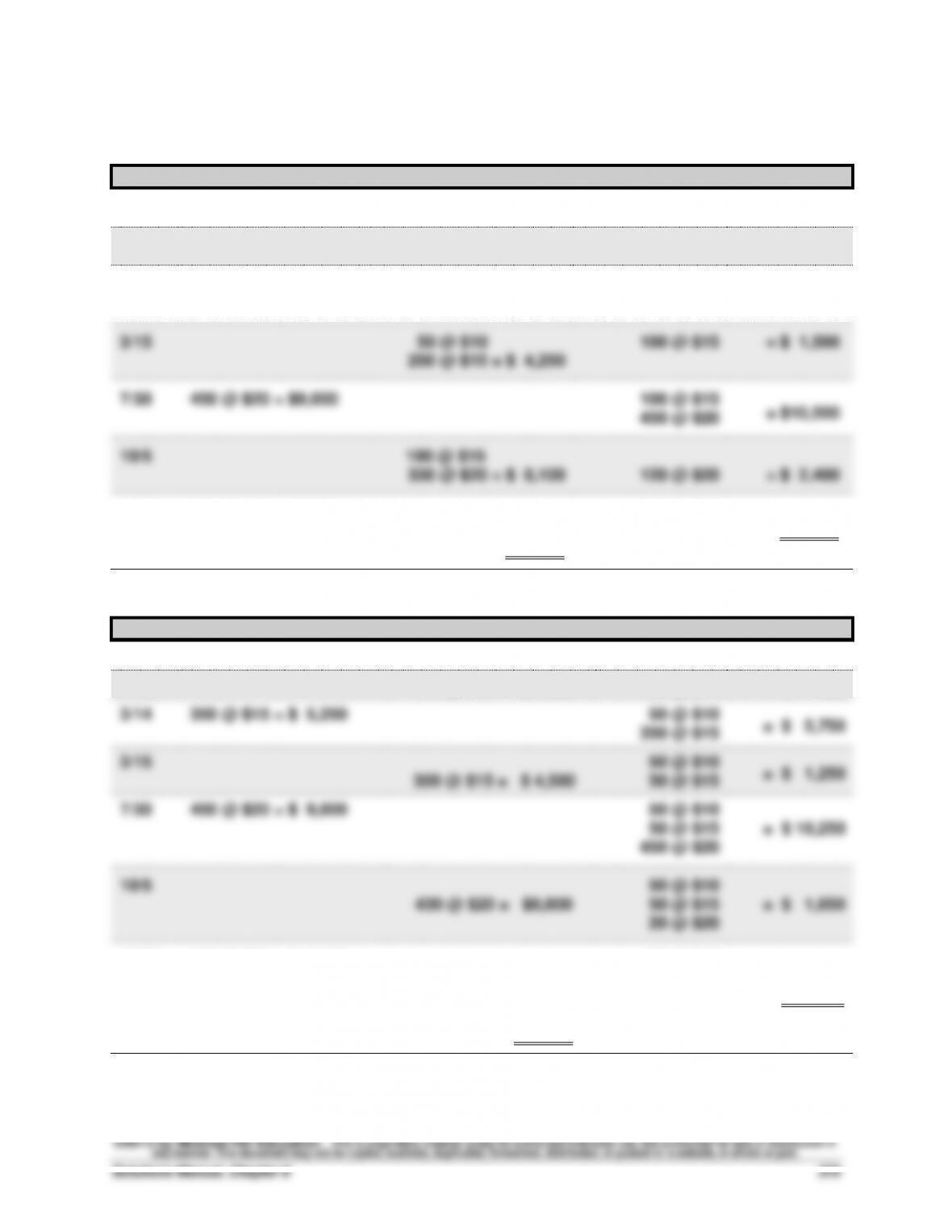

a. FIFO—Perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

1/1

200 @ $10

= $ 2,000

1/10

150 @ $10 = $ 1,500

50 @ $10

= $ 500

3/14

350 @ $15 = $5,250

50 @ $10

= $ 5,750

350 @ $15

3/15

50 @ $10

100 @ $15

= $ 1,500

250 @ $15 = $ 4,250

7/30

450 @ $20 = $9,000

100 @ $15

= $10,500

450 @ $20

10/5

100 @ $15

330 @ $20 = $ 8,100

120 @ $20

= $ 2,400

10/26

100 @ $25 = $2,500

120 @ $20

______

100 @ $25

= $ 4,900

$13,850

b. LIFO—Perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

1/1

200 @ $10

= $ 2,000

1/10

150 @ $10 = $ 1,500

50 @ $10

= $ 500

3/14

350 @ $15 = $ 5,250

50 @ $10

= $ 5,750

350 @ $15

3/15

50 @ $10

= $ 1,250

300 @ $15 = $ 4,500

50 @ $15

7/30

450 @ $20 = $ 9,000

50 @ $10

50 @ $15

= $ 10,250

450 @ $20

10/5

50 @ $10

430 @ $20 = $8,600

50 @ $15

= $ 1,650

20 @ $20

10/26

100 @ $25 = $ 2,500

50 @ $10

50 @ $15

20 @ $20

= $ 4,150

_______

100 @ $25

$14,600