Chapter 4

Completing the Accounting Cycle

QUESTIONS

1. The four-step closing entry process is: (i) close the revenue (and gain) accounts to

the Income Summary account, (ii) close the expense (and loss) accounts to the

2. Closing entries affect temporary accounts: revenues, expenses, withdrawals, and

income summary. Specifically, closing entries at the end of an accounting period

3. (i) Closing entries prepare the temporary accounts—revenue and expense (and gain

4. The Income Summary account is used to summarize the period’s revenues and

expenses. As a result, it temporarily has a balance equal to the net income (or net

5. Yes, an error would have occurred because a post-closing trial balance should only

6. A work sheet can be used to collect and organize data for preparing (i) adjusting

7. The adjustments in the Adjustments columns of a work sheet are identified by

letters to link the debits with the credits to ensure that the entries are complete and

8. A company’s operating cycle is the normal time between paying cash for

9. Assets on a typical classified balance sheet include current assets and noncurrent

assets—where noncurrent assets usually include long-term investments, plant

10. Unearned revenue is reported as a liability—usually a current liability.

11. Plant assets (also called property, plant and equipment or long-lived assets) are

tangible long-lived assets used to produce or sell goods or services.

12.A Reversing entries simplify subsequent entries for accrued expenses and accrued

13.A The following reversing entry could be made as of the first day of the next

accounting period, after the post-closing trial balance is completed and financial

QUICK STUDIES

Quick Study 4-1 (10 minutes)

1. Permanent accounts report on activities related to one or more future

accounting periods, and they carry their ending balances into the next

period.

4. Temporary accounts accumulate data related to one accounting period.

Quick Study 4-2 (5 minutes)

1. (e) Analyzing transactions and events.

2. (h) Journalizing transactions and events.

Quick Study 4-3 (10 minutes)

1. B

2. F

Quick Study 4-4 (5 minutes)

Current assets

Cash …………………………………………………...

$ 7,000

Accounts receivable …………………………..

18,000

Office supplies …………………………………....

2,800

Prepaid insurance ……………………………....

3,560

Total current assets …………………………..

$31,360

Current liabilities

Accounts payable ………………………………..

$11,000

Unearned services revenue ………………....

3,000

Total current liabilities ………………………...

$14,000

Current ratio = $31,360 / $14,000 = 2.24

Quick Study 4-5 (5 minutes)

a.

5

d.

3

b.

4

e.

2

c.

1

Quick Study 4-6 (5 minutes)

a.

BS

d.

IS

b.

BS

e.

BS

c.

BS

f.

IS

Quick Study 4-7 (20 minutes)

CLAUDELL COMPANY

Work Sheet

Unadjusted

Trial Balance

Adjustments

Adjusted

Trial Balance

Income

Statement

Balance Sheet

Account Title

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Prepaid Rent …………………...

1,000

(a)

200

800

800

Services Revenue …………..

55,600

(b)

900

56,500

56,500

Wages expense ……………...

5,000

(c)

700

5,700

5,700

Accounts Receivable ……..

(b)

900

900

900

Wages Payable ……………….

(c)

700

700

700

Rent Expense ………………….

(a)

200

200

200

Quick Study 4-8 (10 minutes)

Computation of B. Warton, Capital for the Dec. 31, 2013, balance sheet

B. Warton, Capital (beginning) …………………….

$ 72,000

Add net income ($181,000 – $122,000) ………….

59,000

131,000

Less withdrawals ………………………………….…….

(39,000)

B. Warton, Capital (ending) …………………..…….

$ 92,000

Quick Study 4-9 (15 minutes)

Dec. 31 Services Revenue ………………………………….. 13,000

Income Summary ……………………………. 13,000

To close the revenue account.

31 D.Mai, Capital …………………………..……………. 800

D. Mai, Withdrawals ……………………….. 800

To close the withdrawals account.

Quick Study 4-10 (5 minutes)

The only account from QS 4-9 that would appear in post-closing trial balance

is D. Mai, Capital.

Quick Study 4-11A (10 minutes)

2013

Jan. 1 Management Fees Earned ………………………. 12,000

Accounts Receivable ……………………… 12,000

To reverse accrued revenue.

Quick Study 4-12 (10 minutes)

a. The closing process is identical under U.S. GAAP and IFRS.

EXERCISES

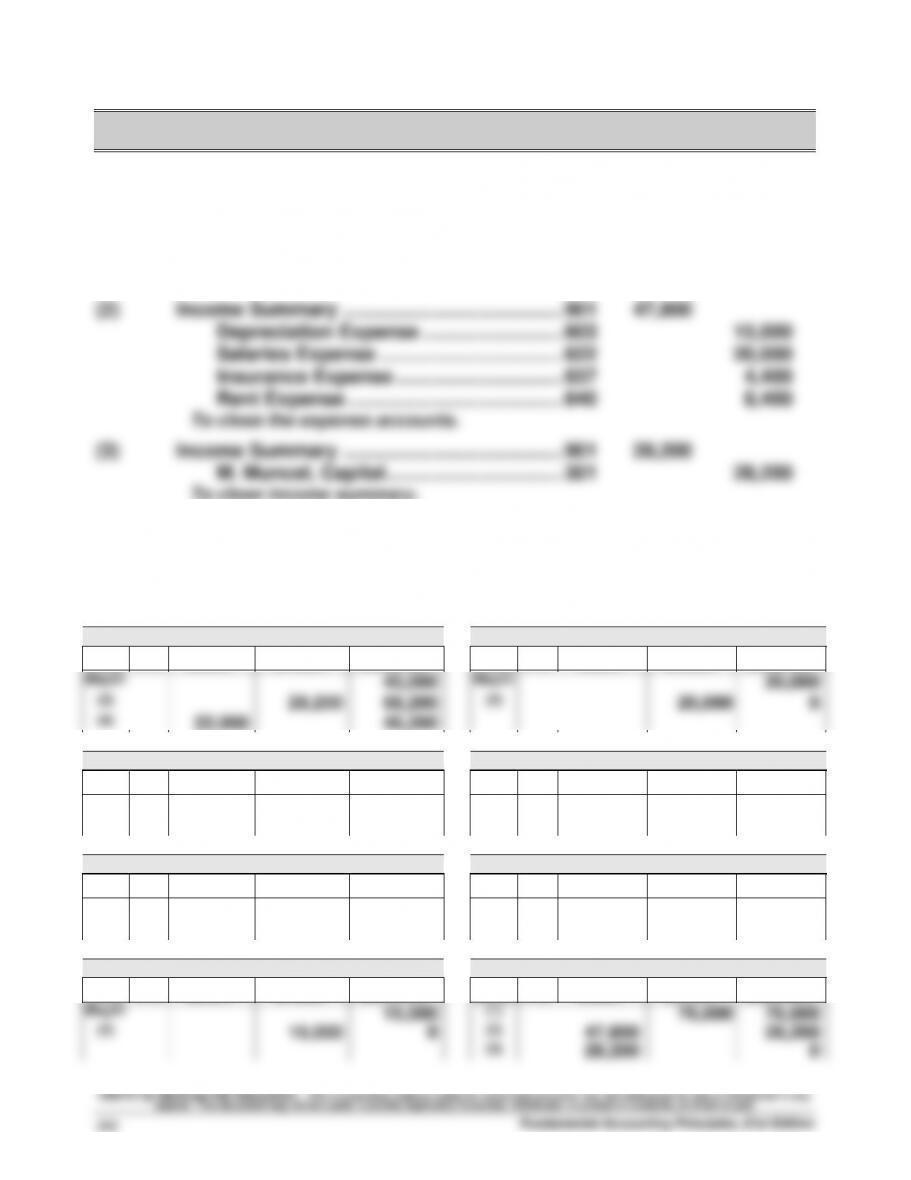

Exercise 4-1 (35 minutes)

Closing entries

(1) Services Revenue ………………………………….. 401 76,000

Income Summary ……………………………. 901 76,000

To close the revenue account.

To close income summary.

(4) M. Muncel, Capital …………………………………. 301 22,000

M. Muncel, Withdrawals ………………….. 302 22,000

To close the withdrawals account.

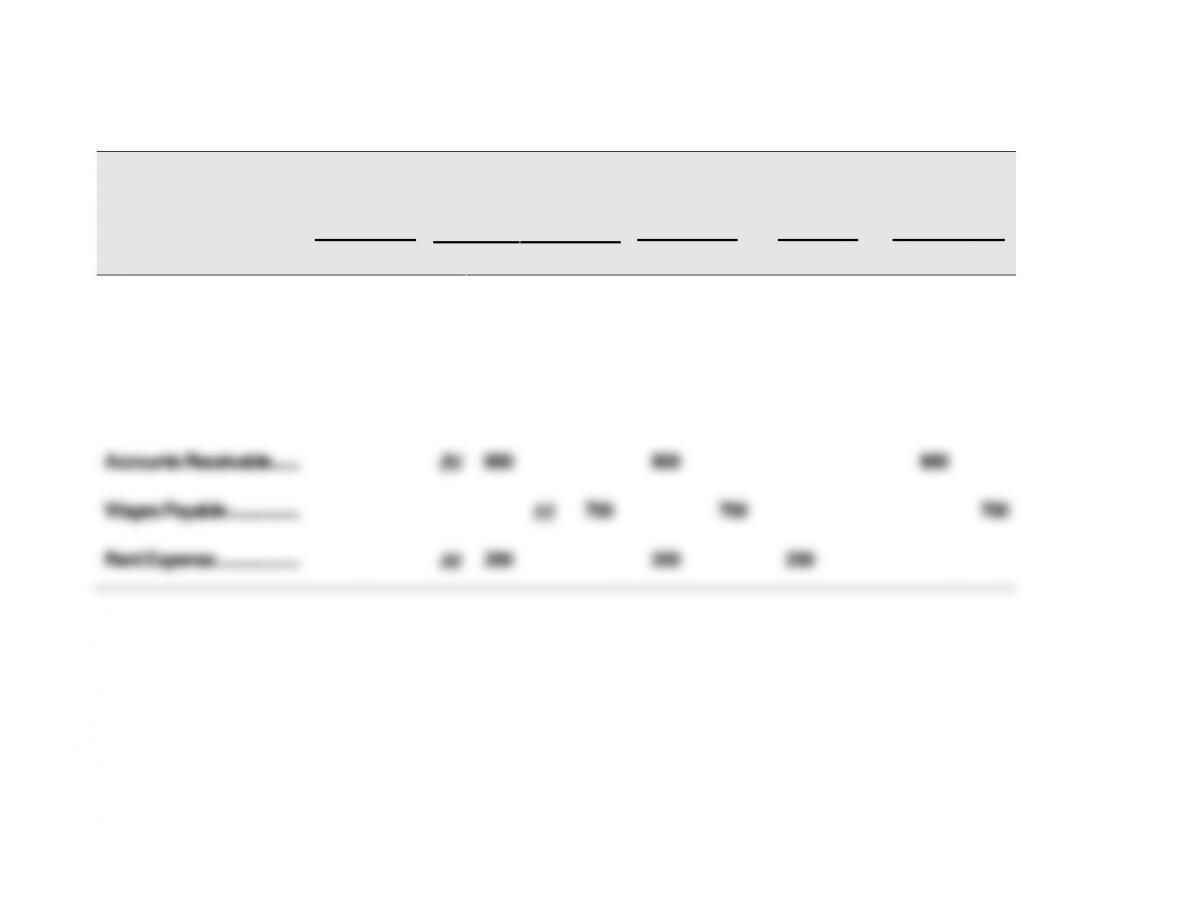

Posted ledger accounts

M. Muncel, Capital No. 301

Salaries Expense No. 622

Date

PR

Debit

Credit

Balance

Date

PR

Debit

Credit

Balance

May31

40,000

May31

20,000

(3)

28,200

68,200

(2)

20,000

0

(4)

22,000

46,200

M. Muncel, Withdrawals No. 302

Insurance Expense No. 637

Date

PR

Debit

Credit

Balance

Date

PR

Debit

Credit

Balance

May31

22,000

May31

4,400

(4)

22,000

0

(2)

4,400

0

Services Revenue No. 401

Rent Expense No. 640

Date

PR

Debit

Credit

Balance

Date

PR

Debit

Credit

Balance

May31

76,000

May31

8,400

(1)

76,000

0

(2)

8,400

0

Depreciation Expense No. 603

Income Summary No. 901

Date

PR

Debit

Credit

Balance

Date

PR

Debit

Credit

Balance

May31

15,000

(1)

76,000

76,000

(2)

15,000

0

(2)

47,800

28,200

(3)

28,200

0

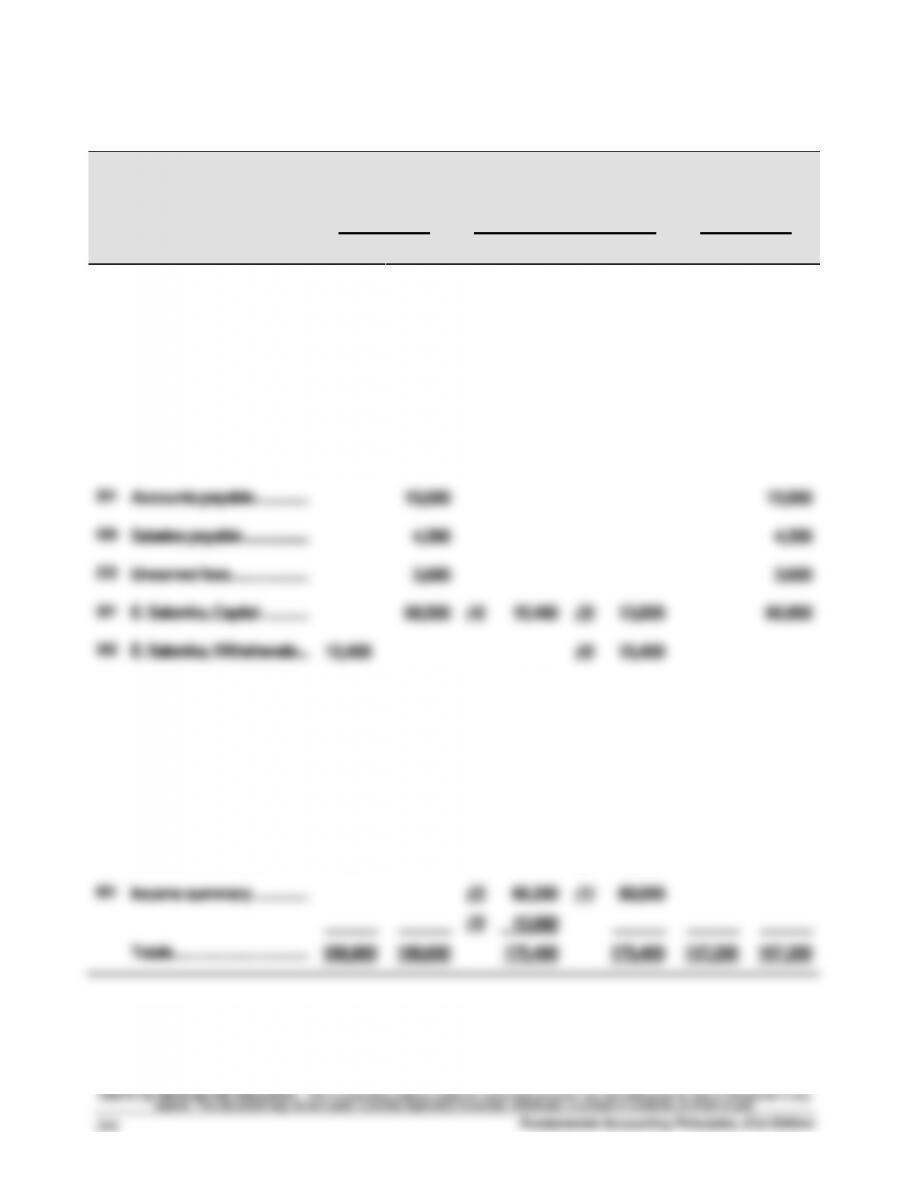

Exercise 4-2 (30 minutes)

1.

2013

Dec. 31 Services Revenue ………………………………….. 404 44,000

Income Summary ……………………………. 901 44,000

To close the revenue account.

31 Income Summary ………………………………….. 901 33,100

31 Income Summary ………………………………….. 901 10,900

T. Cruz, Capital ……………………………….. 301 10,900

To close income summary.

2.

CRUZ COMPANY

Post-Closing Trial Balance

December 31, 2013

Debit Credit

Cash ………………………………………………………. $19,000

Supplies ………………………………………………… 13,000

Prepaid insurance ………………………………….. 3,000

*$47,600 + $10,900 – $7,000 = $51,500

Exercise 4-3 (40 minutes)

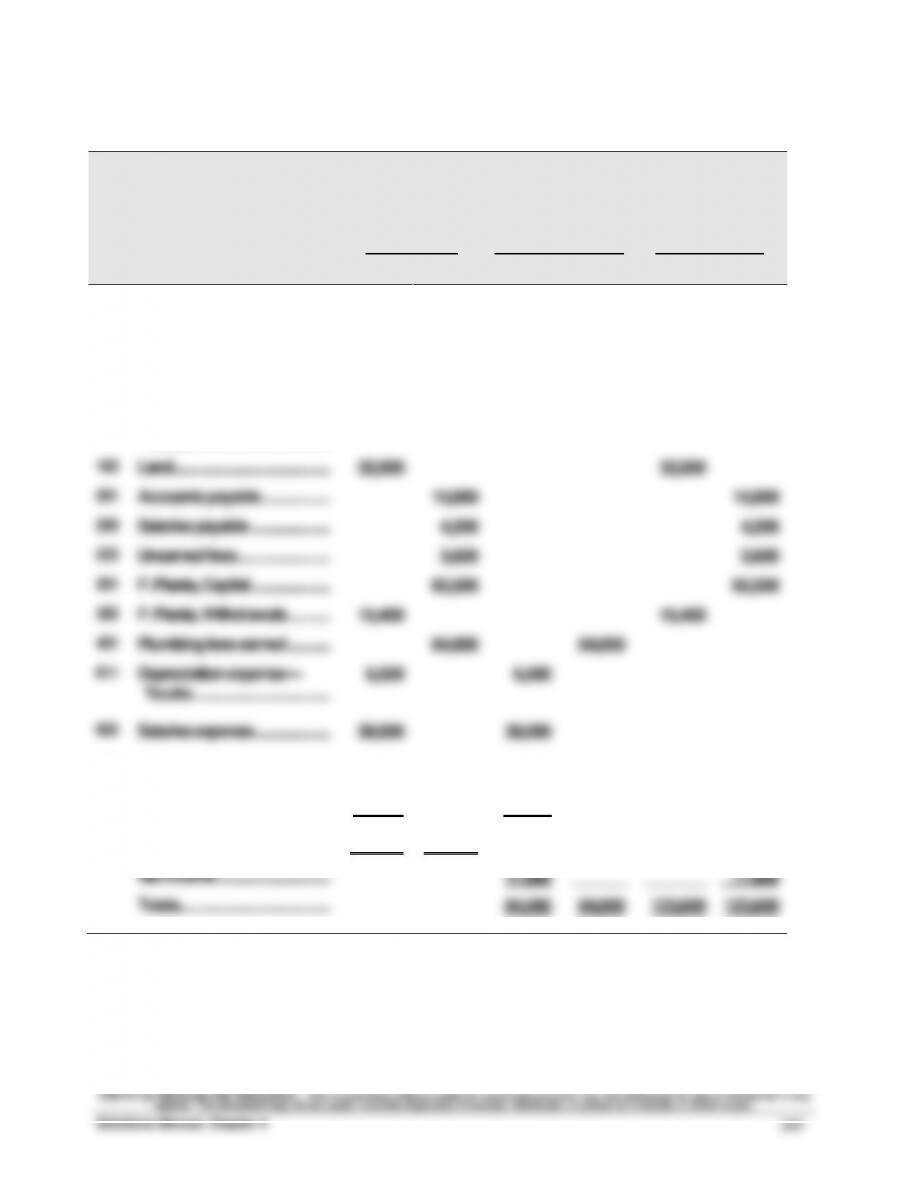

Salonika Marketing Company

Work Sheet

Adjusted

Trial Balance

Closing Entry Information

Post–Closing

Trial Balance

No.

Account Title

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

101

Cash …………………………………..

9,200

9,200

106

Accounts receivable ………..

25,000

25,000

153

Equipment …………………………

42,000

42,000

154

Accumulated depre–

ciation—Equipment ……….

17,500

17,500

193

Franchise …………………………..

31,000

31,000

201

Accounts payable …………….

15,000

15,000

209

Salaries payable ……………….

4,200

4,200

233

Unearned fees …………………..

3,600

3,600

301

E. Salonika, Capital …………..

68,500

(4)

15,400

(3)

13,800

66,900

302

E. Salonika, Withdrawals …

15,400

(4)

15,400

401

Marketing fees earned ……..

80,000

(1)

80,000

611

Depreciation expense—

Equipment. ………………………

12,000

(2)

12,000

622

Salaries expense ………………

32,500

(2)

32,500

640

Rent expense ……………………

13,000

(2)

13,000

677

Miscellaneous expense …..

8,700

(2)

8,700

901

Income summary …………….

(2)

66,200

(1)

80,000

______

______

(3)

13,800

______

______

______

Totals ………………………………….

188,800

188,800

175,400

175,400

107,200

107,200

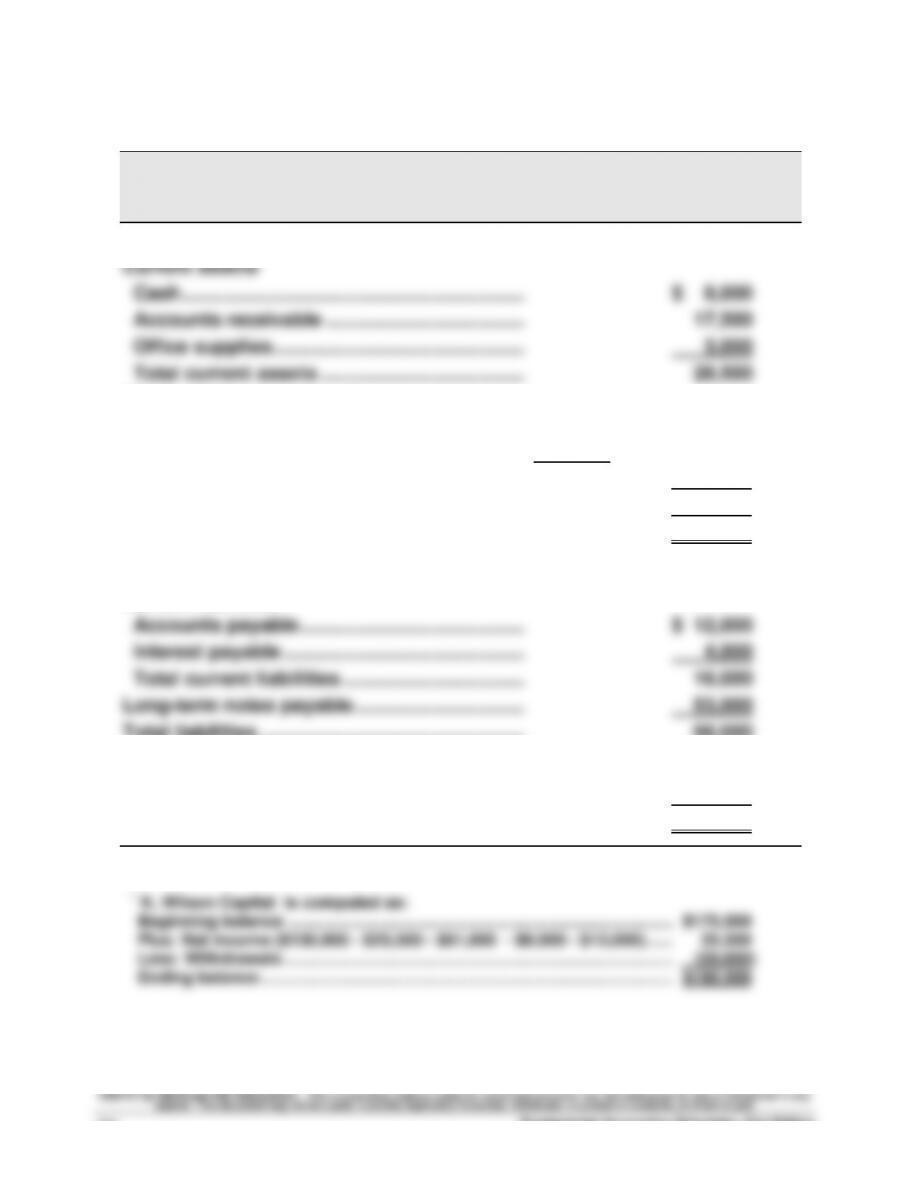

Exercise 4-4 (20 minutes)

WILSON TRUCKING COMPANY

Income Statement

For Year Ended December 31, 2013

Trucking fees earned ………………………………………… $130,000

Expenses

Depreciation expense—Trucks ……………………… $23,500

Salaries expense ………………………………………….. 61,000

WILSON TRUCKING COMPANY

Statement of Owner’s Equity

For Year Ended December 31, 2013

K. Wilson, Capital, December 31, 2012 ………………. $175,000

Exercise 4-5 (20 minutes)

WILSON TRUCKING COMPANY

Balance Sheet

December 31, 2013

Assets

Plant assets

Trucks ……………………………………………………. $172,000

Accumulated depreciation-Trucks ………….. (36,000) 136,000

Land ………………………………………………………. 85,000

Total plant assets …………………………………… 221,000

Total assets ……………………………………………… $249,500

Liabilities

Current liabilities

Total liabilities …………………………………………. 69,000

Equity

K. Wilson, Capital* ……………………………………. 180,500

Total liabilities and equity ………………………… $249,500

*From Exercise 4-4

Exercise 4-6 (15 minutes)

Current assets:

Cash ……………………………………………………………………… $ 8,000

Current liabilities:

Accounts payable ………………………………………………….. $12,000

Interpretation: Wilson Trucking Company’s current ratio of 1.78 exceeds the

industry average of 1.5. This implies the company is in a slightly better

$16,000

Current liabilities

Exercise 4-7 (15 minutes)

Current

Assets

Current

Liabilities

Current

Ratio

Case 1

$ 79,040

/

$ 32,000

=

2.47

Case 2

104,880

/

76,000

=

1.38

Case 3

45,080

/

49,000

=

0.92

Case 4

85,680

/

81,600

=

1.05

Case 5

61,000

/

100,000

=

0.61

Analysis: Company 1 is in the strongest liquidity position. It has about $2.47

of current assets for each $1 of current liabilities. The only potential concern

Exercise 4-8 (15 minutes)

1.

B

5.

D

9.

C

13.

C

2.

C

6.

B

10.

D

14.

C

3.

C

7.

D

11.

C

15.

A

4.

A

8.

A

12.

A

16.

D

Exercise 4-9 (20 minutes)

Planta Company

Work Sheet

Adjusted

Trial Balance

Income Statement

Balance Sheet &

Statement of

Owner’s Equity

No.

Account

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

101

Cash ………………………………………

7,000

7,000

106

Accounts receivable ……………

27,200

27,200

153

Trucks ……………………………………

42,000

42,000

154

Accumulated depreciation—

Trucks …………………………………….

17,500

17,500

183

Land …………………………..…………..

32,000

32,000

201

Accounts payable ………………..

15,000

15,000

209

Salaries payable …………………..

4,200

4,200

233

Unearned fees ………………………

3,600

3,600

301

F. Planta, Capital …………………..

65,500

65,500

302

F. Planta, Withdrawals …………

15,400

15,400

401

Plumbing fees earned …………

84,000

84,000

611

Depreciation expense—

Trucks ………………………………….

6,500

6,500

622

Salaries expense ………………….

38,000

38,000

640

Rent expense ……………………….

13,000

13,000

677

Miscellaneous expense ………

8,700

______

8,700

______

_______

______

Totals ……………………………………..

189,800

189,800

66,200

84,000

123,600

105,800

Net income …………………………...

17,800

______

_______

17,800

Totals ……………………………………..

84,000

84,000

123,600

123,600