Problem 20-8B (Concluded)

Part 4

MEMORANDUM

TO:

FROM:

DATE:

RE: Percentage of Completion Error Analysis

If the units in ending inventory are 75% complete instead of 25% with respect

to labor, the number of equivalent units in ending inventory with respect to

Regarding financial statements, this error causes an overstatement of cost of

goods sold and an understatement of net income on the income statement for

Fundamental Accounting Principles, 21st Edition

1194

Problem 20-9B (80 minutes)

Part 1

BELDA CO.

Process Cost Summary – FIFO Method

For Month Ended March 31

Costs Charged to Production

Costs of beginning goods in process

Direct materials…………………………………………………….…

$ 16,800

Direct labor …………………………………………………………..….

27,920

Factory overhead………………………………………………….….

69,800

$ 114,520

Costs incurred this period

Direct materials…………………………………………………….…

223,200

Direct labor …………………………………………………………..….

352,560

Factory overhead………………………………………………….….

881,400

1,457,160

Total costs to account for ………………………………………….

$1,571,680

Unit cost information

Units to account for

Units accounted for

Beginning goods in process ……….

10,000

Completed & transferred out ……

220,000

Units started this period ……….…….

250,000

Ending goods in process ………

40,000

Total units to account for ……..…….

260,000

Total units accounted for ………

260,000

Equivalent units of production

Direct

Materials

Direct

Labor

Factory

Overhead

Units to complete beginning goods in process

Direct materials (10,000 x 25%) ………….

2,500 EUP

Direct labor (10,000 x 40%) ………………..

4,000 EUP

Factory overhead (10,000 x 40%) ……….

4,000 EUP

Units started and completed ……………….

210,000 EUP

210,000 EUP

210,000 EUP

Units of ending goods in process

Direct materials (40,000 x 50%) ………….

20,000 EUP

Direct labor (40,000 x 30%) ………………..

12,000 EUP

Factory overhead (40,000 x 30%) ……….

__________

___________

12,000 EUP

Equivalent units of production…………….

232,500 EUP

226,000 EUP

226,000 EUP

[Continued on next page]

Problem 20-9B (Continued)

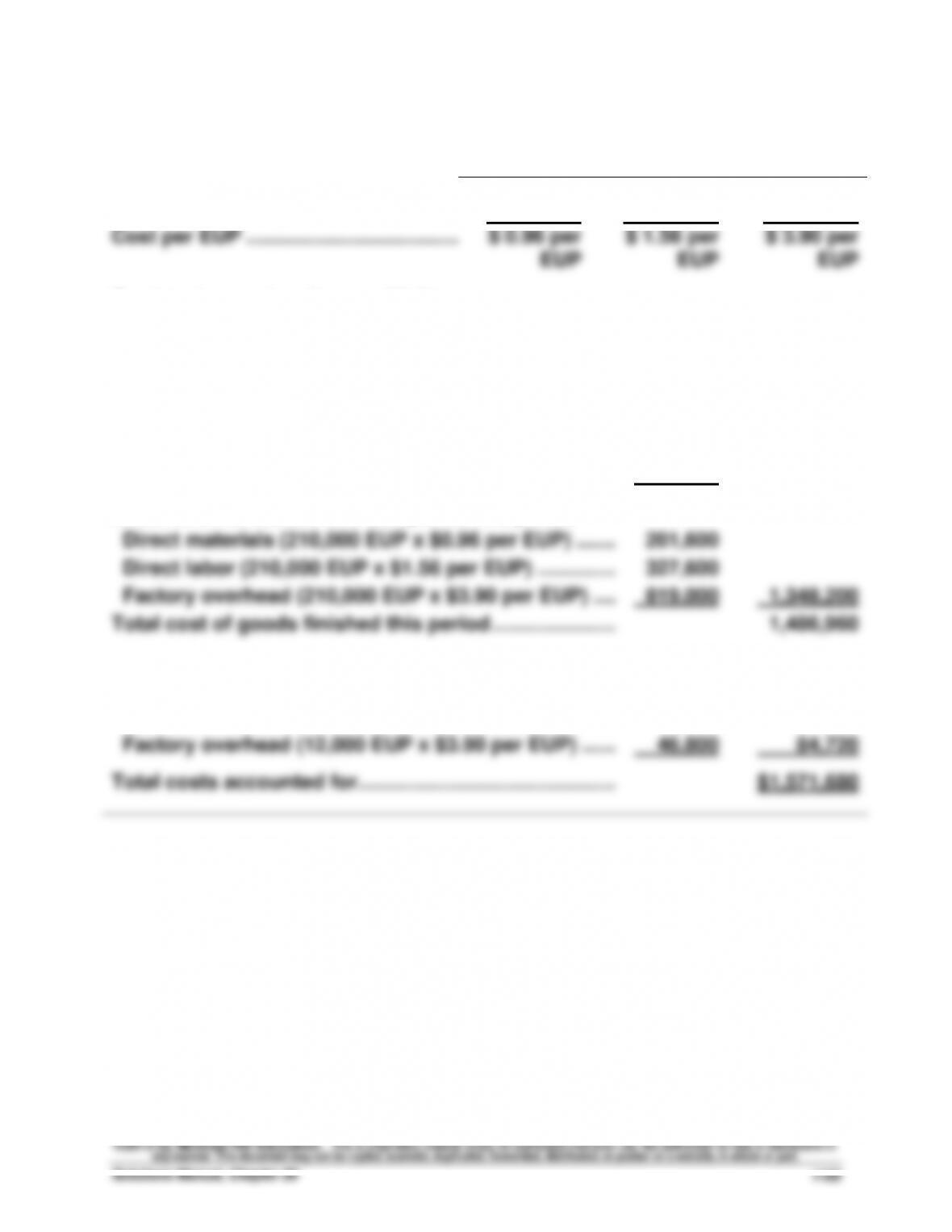

Cost per EUP

Direct

Materials

Direct Labor

Factory

Overhead

Costs incurred this period ……………...

$ 223,200

$ 352,560

$ 881,400

÷ EUP …………………………………………….

÷ 232,500

÷ 226,000

÷ 226,000

Cost per EUP ………………………………...

$ 0.96 per

EUP

$ 1.56 per

EUP

$ 3.90 per

EUP

Cost assignment and reconciliation

Costs transferred out

Cost of beginning goods in process ……………………….….

$ 114,520

Cost to complete beginning goods in process

Direct materials (2,500 EUP x $0.96 per EUP) ………..……….

$ 2,400

Direct labor (4,000 EUP x $1.56 per EUP) ……………………….

6,240

Factory overhead (4,000 EUP x $3.90 per EUP) ……..……….

15,600

24,240

Costs of units started and completed this period

Direct materials (210,000 EUP x $0.96 per EUP) …….……….

201,600

Direct labor (210,000 EUP x $1.56 per EUP) …………..……….

327,600

Factory overhead (210,000 EUP x $3.90 per EUP) ….……….

819,000

1,348,200

Total cost of goods finished this period ………………….……….

1,486,960

Costs of ending goods in process

Direct materials (20,000 EUP x $0.96 per EUP) ……………….

19,200

Direct labor (12,000 EUP x $1.56 per EUP) …………….……….

18,720

Factory overhead (12,000 EUP x $3.90 per EUP) …………….

46,800

84,720

Total costs accounted for ……………………………………….……….

$1,571,680

Part 2

Mar. 31

Finished Goods Inventory …………………………..

1,486,960

Goods in Process Inventory ………………….……….

1,486,960

Transfer of goods to finished inventory.

Problem 20-9B (Concluded)

If equivalent units of production for the production department’s ending

inventory for March are overstated, then total equivalent units of

SERIAL PROBLEM — SP 20

1. Features of job order and process costing follow.

Job order costing

Process costing

• Custom orders

• Repetitive operations

• Heterogeneous products

• Homogeneous products

• Low production volume

• High production volume

• High product flexibility

• Low product flexibility

• Low to medium standardization

• High standardization

2. Given the size of her company, and the types of products she sells,

Adria should probably stay with job order costing. The furniture she

Fundamental Accounting Principles, 21st Edition

1198

COMPREHENSIVE PROBLEM

Comprehensive Problem, Major League Bat Company (110 minutes)

[Instructor note: General Ledger accounts are shown in Part 4.]

Part 1 (Using either weighted-average or FIFO)

July Journal Entries

a.

Raw Materials Inventory ………………………………………..

125,000

Cash ………………………………………………………………..

125,000

Purchased raw materials for cash.

b.

Goods in Process Inventory …………………………………..

52,440

Factory Overhead …………………………………………..……..

10,000

Raw Materials Inventory …………………………….……..

62,440

To record use of raw materials.

c.

Factory Payroll ……………………………………………………..

227,250

Cash ………………………………………………………..……..

227,250

Paid factory payroll with cash.

d.

Goods in Process Inventory …………………………………..

202,250

Factory Overhead …………………………………………..……..

25,000

Factory Payroll ………………………………………………..

227,250

To record direct and indirect labor.

e.

Factory Overhead …………………………………………..……..

80,000

Cash ………………………………………………………..……..

80,000

Paid other overhead with cash.

f.

Goods in Process Inventory …………………………………..

101,125

Factory Overhead ……………………………………..……..

101,125

Allocated overhead at 50% of direct labor.

Comprehensive Problem (Continued)

Part 2 (Using weighted-average)

MAJOR LEAGUE BAT CO.

Process Cost Summary (Weighted Average)

For Month Ended July 31

Costs Charged to Production

Costs of beginning goods in process

Direct materials…………………………………………………..…..

$ 2,660

Direct labor ………………………………………………………………

3,650

Factory overhead………………………………………………..……

1,825

$ 8,135

Costs incurred this period

Direct materials…………………………………………………..…..

52,440

Direct labor ………………………………………………………………

202,250

Factory overhead………………………………………………..……

101,125

355,815

Total costs to account for …………………………………….……

$363,950

Unit cost information

Units to account for

Units accounted for

Beginning goods in process …………………………..

5,000

Complete & transferred out …..…….

11,000

Units started this period ……….………………….

14,000

Ending goods in process …………….

8,000

Total units to account for ……..……………………

19,000

Total units accounted for …………….

19,000

Equivalent units of production

Direct

Materials

Direct

Labor

Factory

Overhead

Units completed & transferred out ………….…

11,000 EUP

11,000 EUP

11,000 EUP

Units of ending goods in process

Direct materials (8,000 x 100%) ……………..…

8,000 EUP

Direct labor (8,000 x 40%) ……………………..…

3,200 EUP

Factory overhead (8,000 x 40%) …………….…

__________

__________

3,200 EUP

Equivalent units of production

19,000 EUP

14,200 EUP

14,200 EUP

Cost per EUP

Direct

Materials

Direct

Labor

Factory

Overhead

Cost of beginning goods in process ……….…

$ 2,660

$ 3,650

$ 1,825

Costs incurred this period …………………………

52,440

202,250

101,125

Total costs …………………………………………….…

$55,100

$205,900

$102,950

÷ EUP …………………………………………………….…

19,000 EUP

14,200 EUP

14,200 EUP

Cost per EUP ……………………………………………

$2.90 per

EUP

$14.50 per

EUP

$7.25 per

EUP

[Continued on next page]

Fundamental Accounting Principles, 21st Edition

1200

Comprehensive Problem (Continued)

(Using weighted-average)

Cost assignment and reconciliation

Costs transferred out

Direct materials (11,000 EUP x $2.90 per EUP) ……………….

$ 31,900

Direct labor (11,000 EUP x $14.50 per EUP) ……………..…….

159,500

Factory overhead (11,000 EUP x $7.25 per EUP) …………….

79,750

$271,150

Costs of ending goods in process

Direct materials (8,000 EUP x $2.90 per EUP) …………..…….

23,200

Direct labor (3,200 EUP x $14.50 per EUP) ……………….…….

46,400

Factory overhead (3,200 EUP x $7.25 per EUP) ………..…….

23,200

92,800

Total costs accounted for ………………………………………….…….

$363,950

Part 3 — Journal entries (Using weighted-average)

g.

Finished Goods Inventory …………………………..

271,150

Goods in Process Inventory …………………..………

271,150

Transferred goods to Finished Goods.

h.

Cash …………………………………………………………..…………

625,000

Sales …………………………..…………………………..

625,000

Sold finished goods for cash.

Cost of Goods Sold …………………………………….…………

265,700

Finished Goods Inventory …………………………..

265,700

Transferred cost from finished goods

to cost of goods sold.

Comprehensive Problem (Continued)

Part 4 (Using weighted-average)

General ledger accounts

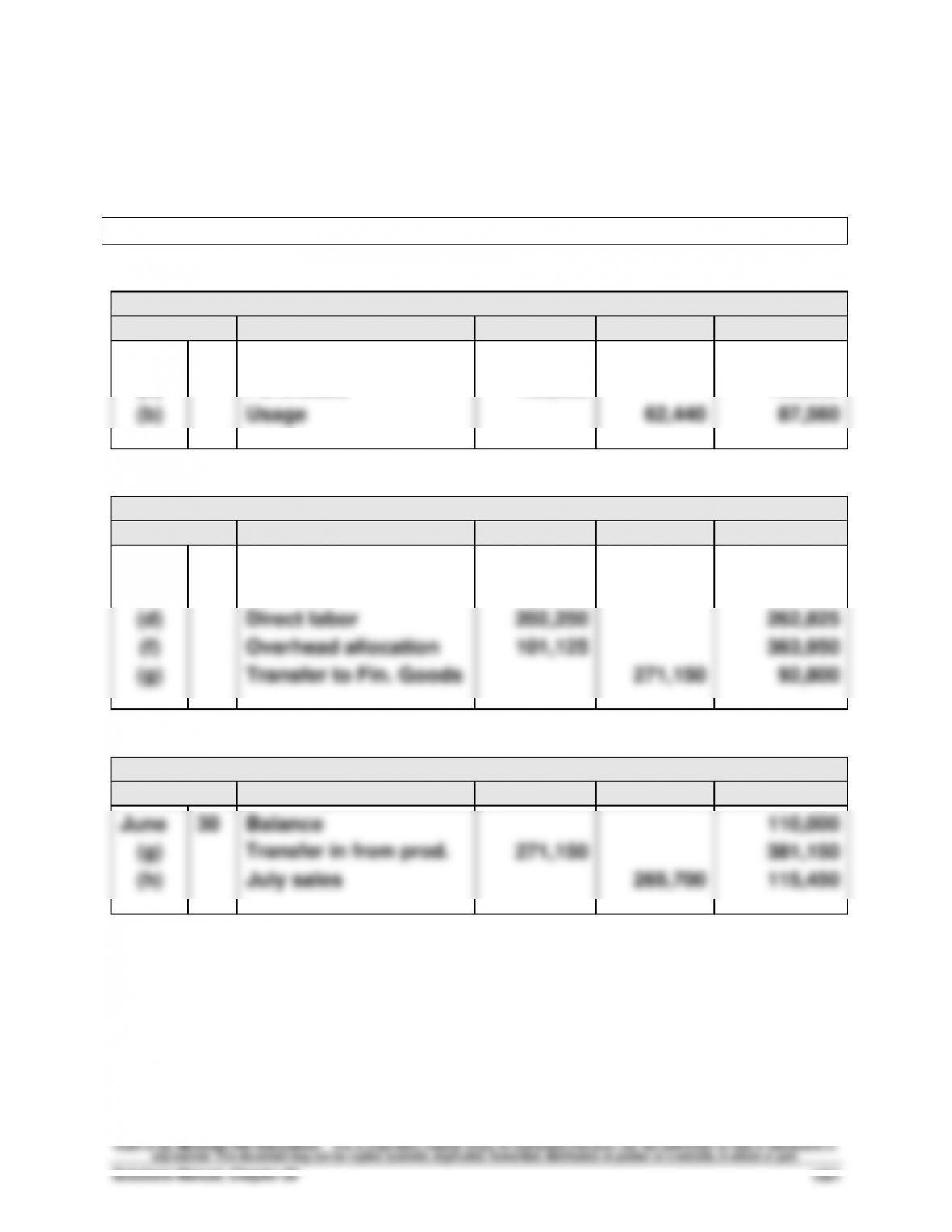

Raw Materials Inventory

Acct. No. 132

Date

Explanation

Debit

Credit

Balance

June

30

Balance

25,000

(a)

Purchases

125,000

150,000

(b)

Usage

62,440

87,560

Goods in Process Inventory

Acct. No. 133

Date

Explanation

Debit

Credit

Balance

June

30

Balance

8,135

(b)

Direct materials

52,440

60,575

(d)

Direct labor

202,250

262,825

(f)

Overhead allocation

101,125

363,950

(g)

Transfer to Fin. Goods

271,150

92,800

Finished Goods Inventory

Acct. No. 135

Date

Explanation

Debit

Credit

Balance

June

30

Balance

110,000

(g)

Transfer in from prod.

271,150

381,150

(h)

July sales

265,700

115,450

Fundamental Accounting Principles, 21st Edition

1202

Comprehensive Problem (Concluded)

Part 4 (Using weighted-average)

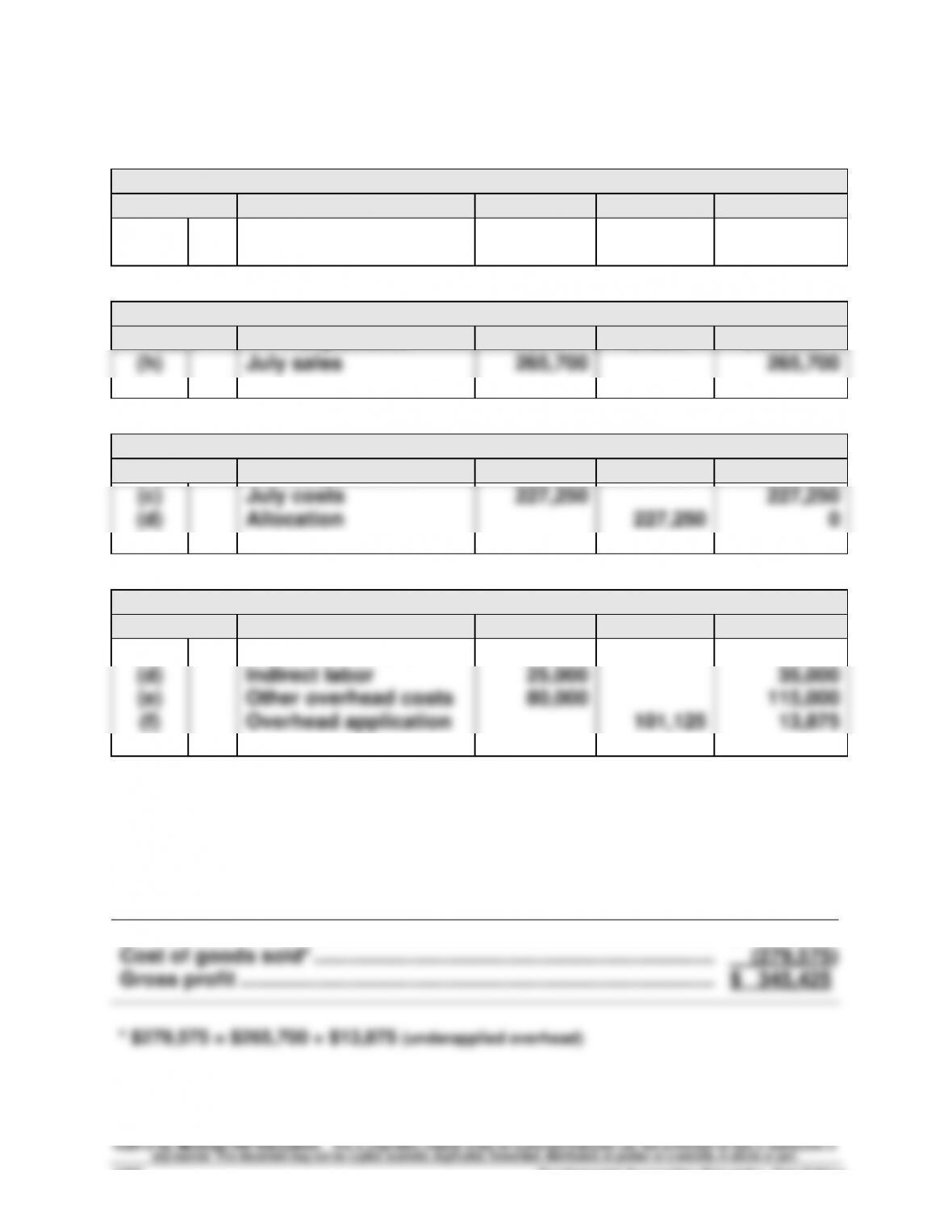

Sales

Acct. No. 413

Date

Explanation

Debit

Credit

Balance

(h)

July sales

625,000

625,000

Cost of Goods Sold

Acct. No. 502

Date

Explanation

Debit

Credit

Balance

(h)

July sales

265,700

265,700

Factory Payroll

Acct. No. 530

Date

Explanation

Debit

Credit

Balance

(c)

July costs

227,250

227,250

(d)

Allocation

227,250

0

Factory Overhead

Acct. No. 540

Date

Explanation

Debit

Credit

Balance

(b)

Indirect materials

10,000

10,000

(d)

Indirect labor

25,000

35,000

(e)

Other overhead costs

80,000

115,000

(f)

Overhead application

101,125

13,875

Part 5 (Using weighted-average)

Computation of gross profit for July

Sales …………………………………………………………………………………….…

$ 625,000

Cost of goods sold* …………………………………………………………………

(279,575)

Gross profit ………………………………………………………………………….…

$ 345,425

* $279,575 = $265,700 + $13,875 (underapplied overhead)

Comprehensive Problem (Continued)

Part 2 (Using FIFO)

MAJOR LEAGUE BAT CO.

Process Cost Summary (FIFO)

For Month Ended July 31

Costs Charged to Production

Costs of beginning goods in process

Direct materials…………………………………………………..…..

$ 2,660

Direct labor ………………………………………………………………

3,650

Factory overhead………………………………………………..……

1,825

$ 8,135

Costs incurred this period

Direct materials…………………………………………………..…..

52,440

Direct labor ………………………………………………………………

202,250

Factory overhead………………………………………………..……

101,125

355,815

Total costs to account for …………………………………….……

$363,950

Unit cost information

Units to account for

Units accounted for

Beginning goods in process …………………………..

5,000

Complete & transferred out …..…….

11,000

Units started this period ……….………………….

14,000

Ending goods in process …………….

8,000

Total units to account for ……..……………………

19,000

Total units accounted for …………….

19,000

Equivalent units of production

Direct

Materials

Direct

Labor

Factory

Overhead

Units to complete beginning goods in process

Direct materials (5,000 x 25%) ……………

0 EUP

Direct labor (5,000 x 25%) ………………….

1,250 EUP

Factory overhead (5,000 x 25%) …………

1,250 EUP

Units started and completed ……………….

6,000 EUP

6,000 EUP

6,000 EUP

Units of ending goods in process

Direct materials (8,000 x 100%) ………….

8,000 EUP

Direct labor (8,000 x 40%) ………………….

3,200 EUP

Factory overhead (8,000 x 40%) …………

_________

_________

3,200 EUP

Equivalent units of production…………….

14,000 EUP

10,450 EUP

10,450 EUP

[Continued on next page]