Title: Exercise 13-7

QA_Ori:

1.

Feb.

5

Retained Earnings* 480,000

Common Stock Dividend Distributable** 120,000

Paid-In Capital in Excess of Par Value,

Feb. 28 Common Stock Dividend Distributable 120,000

2.

Before After

Total stockholders’ equity $1,575,000 $1,575,000

3.

February 5 February 28

Market value per share $ 40 $ 33.40

Note: The total market value of the investor’s holdings is approximately the same for

Title: Exercise 13-8

QA_Ori:

Non-Cumulative

Preferred Common

2013 ($20,000 paid)

2015 ($200,000 paid)

2016 ($350,000 paid)

Preferred* $ 30,000

* The holders of the noncumulative preferred stock are entitled to no more than $30,000

of dividends in any one year (7.5% x $5 x 80,000 shares).

Title: Exercise 13-9

QA_Ori:

Cumulative

Preferred Common

2013 ($20,000 paid)

arrears.)

2014 ($28,000 paid)

Preferredarrears from 2013 $ 10,000

2015 ($200,000 paid)

Preferredarrears from 2014 $ 12,000

2016 ($350,000 paid)

* The holders of the cumulative preferred stock are entitled to no more than

Title: Exercise 13-10

QA_Ori:

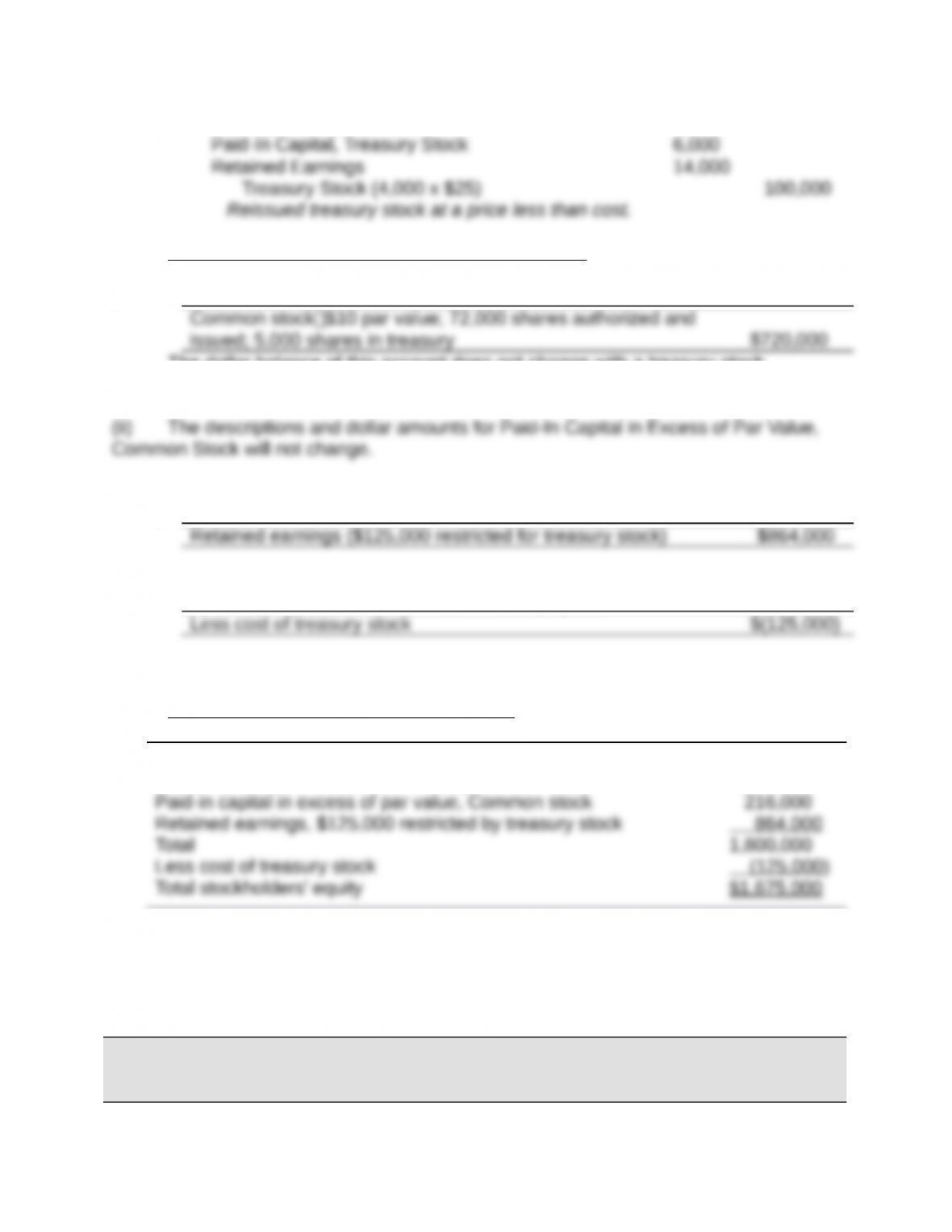

1. (a)

Oct. 11 Treasury Stock (5,000 x $25) 125,000

(b)

Nov. 1 Cash (1,000 x $31) 31,000

(c)

Nov. 25 Cash (4,000 x $20) 80,000

2. Changes to the equity section include the following

(i) The common stock account description line will change. After the treasury stock

purchase, it should read:

The dollar balance of this account does not change with a treasury stock

purchase.

(iii) The retained earnings dollar balance will not change but its description should

change to read:

(iv) After the purchase, a deduction for the cost of treasury stock is reported

immediately before the total line for stockholders’ equity as:

(v) Total stockholders’ equity will change from $1,800,000 to $1,675,000.

Revised equity section appears as follows

Common stock$10 par value; 72,000 shares authorized

and issued; 5,000 shares in treasury $ 720,000

Title: Exercise 13-11

QA_Ori:

Amos Company

Statement of Retained Earnings

For Year Ended December 31, 2013

Retained earnings, December 31, 2012, as previously reported $1,375,000

Prior period adjustment

Title: Exercise 13-12

QA_Ori:

1. Net income $2,700,000

2. Net income available to common stockholders $2,311,980

Title: Exercise 13-13

QA_Ori:

1. Net income $960,000

2. Net income available to common stockholders $840,000

Title: Exercise 13-14

QA_Ori:

Stock

Market Value

per Share

Divided

by

Earnings per

Share

Price-Earnings

Ratio

1 $176.40 $12.00 = 14.7

Analysis: Stocks with PE ratios less than about 5 to 8 are likely viewed as potentially

Title: Exercise 13-15

QA_Ori:

Dividend yield

1. $16.06 / $220.00 = 7.3%

Analysis: The yield of 1.2% on stock #4 is sufficiently low that it probably would be

classified as a growth stock, and not an income stock. Note that classification involves

expectations (not necessarily realizations).

Title: Exercise 13-16

QA_Ori:

1.

Total stockholders’ equity $1,585,000

Less equity applicable to preferred shares

2. QA_Ori:

Total stockholders’ equity $1,585,000

Less equity applicable to preferred shares

Title: Exercise 13-17

QA_Ori:

1. Share capital Common stock

2. Cash 615

Share Capital (at Par Value) 484

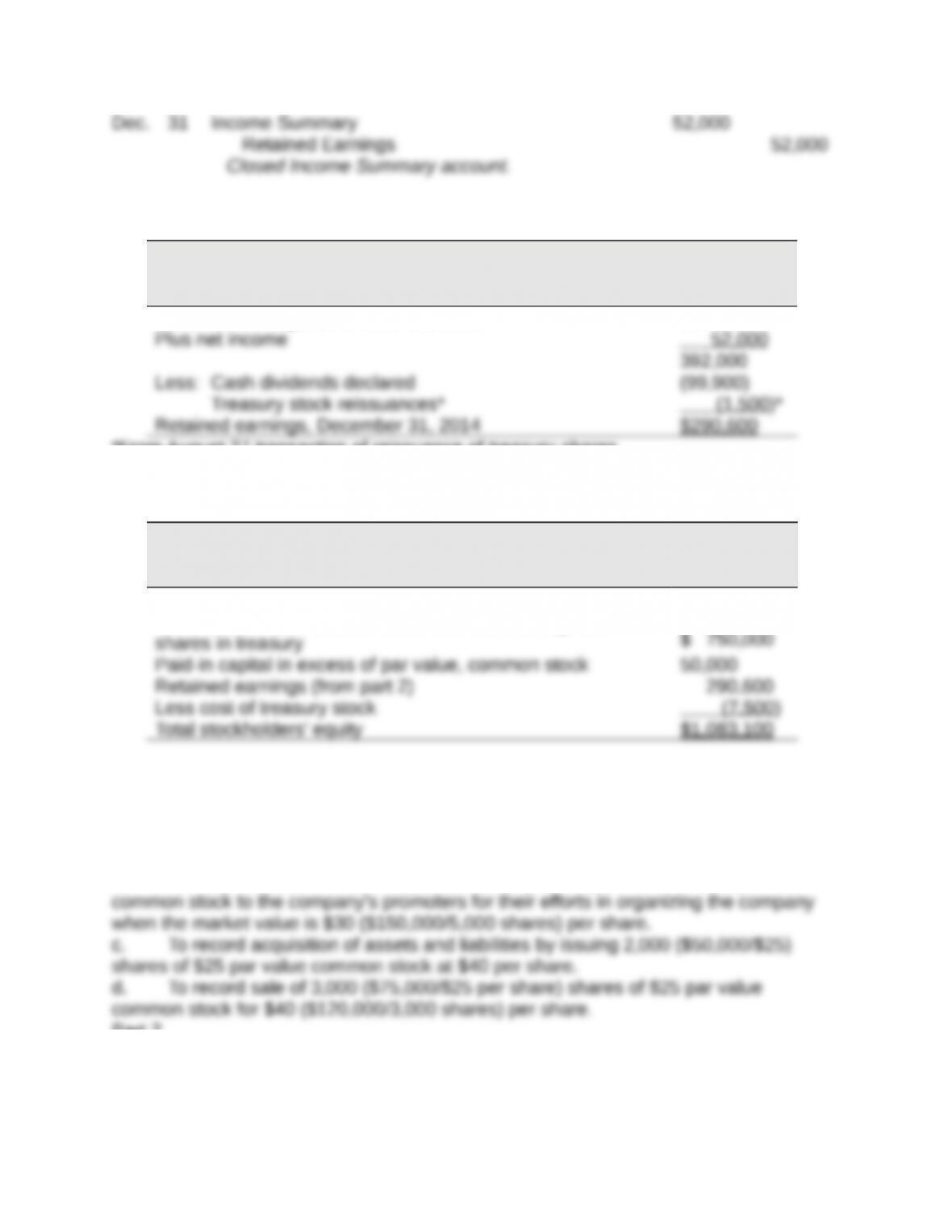

Title: Exercise 13-18

QA_Ori:

Part 1

Jan. 2 Treasury Stock, Common 75,000

Cash 75,000

Purchased treasury stock (3,000 x $25).

Part 2

QA_Ori:

ALEXANDER CORPORATION

Statement of Retained Earnings

For Year Ended December 31, 2014

Retained earnings, December 31, 2013 $340,000

*From August 27 transaction of reissuance of treasury shares.

Part 3

QA_Ori:

ALEXANDER CORPORATION

Stockholders’ Equity Section of the Balance Sheet

December 31, 2014

Common stock$25 par value, 50,000 shares

authorized, 30,000 shares issued and outstanding; 300

Title: Problem 13-1A

QA_Ori:

Part 1

a. To record sale of 10,000 ($250,000/$25 per share) shares of $25 par value

common stock for $30 ($300,000/10,000 shares) per share.

b. To record issuance of 5,000 ($125,000/$25 per share) shares of $25 par value

Part 2

Number of outstanding shares

Issued in (a) 10,000

Issued in (b) 5,000

Part 3

Minimum legal capital = Outstanding shares x Par value per share

Part 4

Total paid-in capital from common stockholders

From transaction (a) $300,000

Part 5

Book value per common share

Title: Problem 13-2A

QA_Ori:

Part 1

Jan. 1 Treasury Stock, Common 80,000

Jan. 5 Retained Earnings 72,000

Feb. 28 Common Dividend Payable 72,000

July 6 Cash* 36,000

Treasury Stock, Common** 30,000

Aug. 22 Cash* 42,500

Sept. 5 Retained Earnings 80,000

Oct. 28 Common Dividend Payable 80,000

Dec. 31 Income Summary 388,000

Part 2

KOHLER CORPORATION

Statement of Retained Earnings

For Year Ended December 31, 2014

Retained earnings, December 31, 2013 $270,000

Plus net income 388,000

Part 3

KOHLER CORPORATION

Stockholders’ Equity Section of the Balance Sheet

December 31, 2014

Common stock$10 par value, 100,000 shares