Fundamental Accounting Principles, 21st Edition

1278

Exercise 22-2 (concluded)

Notes: concluded

(5) August beginning inventory

Total required (4 above)

355,500

Less budgeted purchases

(308,250)

August beginning inventory

47,250

(6) August Beginning Inventory = July Ending Inventory

(7) July required units

Ending inventory

47,250

Add budgeted sales

180,000

Total required in July

227,250

(8) July Beginning Inventory

Total required (7 above)

227,250

Less budgeted purchases

(200,250)

July beginning inventory

27,000

(9) Percent of Sales to be held as Ending Inventory

Ending inventory for August

September Sales

= 40,500 = 15%

270,000

This percentage is constant for the three months.

(10) October expected sales

September Ending Inventory

Required %

= 30,000 = 200,000

15%

2. Monthly ending inventory is 15% of next month’s sales (see note #9).

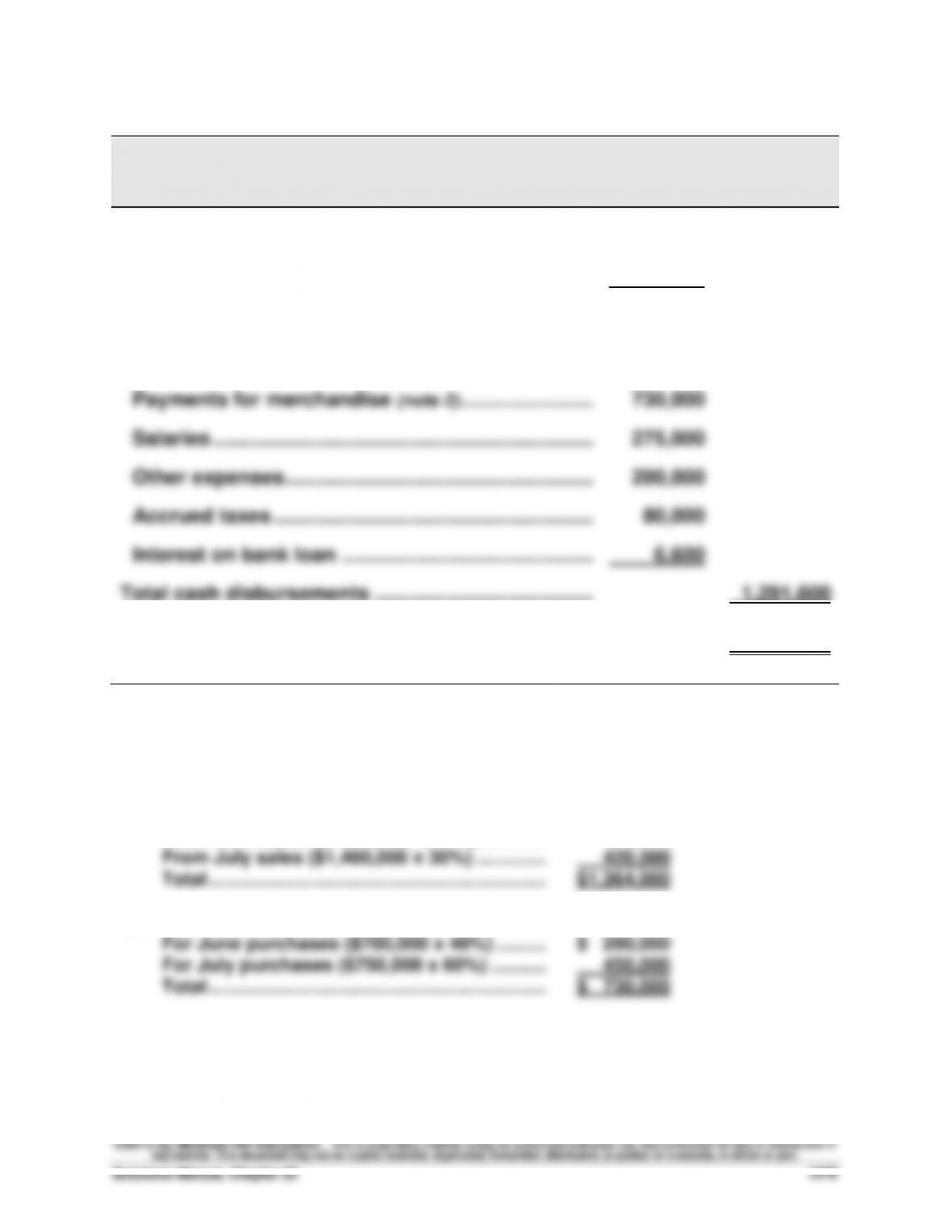

Exercise 22-3 (25 minutes)

ACCO COMPANY

Cash Budget

For Month Ended July 31

Beginning cash balance ……………………………………..….

$ 50,000

Cash receipts from sales (note 1) …………………………..

1,364,000

Total cash available ……………………………………………….

$1,414,000

Cash disbursements

Payments for merchandise (note 2) …………………….….

730,000

Salaries ……………………………………………………………….

275,000

Other expenses ………………………………………………..….

200,000

Accrued taxes ………………………………………………….….

80,000

Interest on bank loan ……………………………………….….

6,600

Total cash disbursements ………………………………….….

1,291,600

Ending cash balance ………………………………………….….

$ 122,400

Supporting calculations

(1) Cash receipts in July from sales

From May sales ($1,720,000 x 20%) …………..

$ 344,000

From June sales ($1,200,000 x 50%) ………….

600,000

From July sales ($1,400,000 x 30%) …………..

420,000

Total ………………………………………………………..

$1,364,000

(2) Cash disbursements in July for merchandise

For June purchases ($700,000 x 40%) ……….

$ 280,000

For July purchases ($750,000 x 60%) ………..

450,000

Total ………………………………………………………..

$ 730,000

Fundamental Accounting Principles, 21st Edition

1280

Exercise 22-4 (45 minutes)

ACCO COMPANY

Budgeted Income Statement

For Month Ended July 31

Sales (from Exercise 22–3) …………………………..……………...

$1,400,000

Cost of goods sold (note 1) ……………………………………...

770,000

Gross profit …………………………………………………………...

630,000

Operating expenses

Salaries expense (note 2) ……………………………………....

$285,000

Depreciation expense (from Exercise 22–3) ………………..

36,000

Other cash expenses (from Exercise 22–3) ………………...

200,000

Bank loan interest expense …………………………………..

6,600

Total expenses ……………………………………………………....

527,600

Income before taxes ……………………………………………....

102,400

Income tax expense (note 3) ……………………………………..

30,720

Net income ……………………………………………………………..

$ 71,680

Supporting calculations

(1) Cost of goods sold

Sales ……………………………………………………....

$1,400,000

Cost percent …………………………………………....

55%

Cost of goods sold …………………………………..

$ 770,000

(2) Salaries expense

Cash paid ………………………………………………...

$ 275,000

Less beginning payable …………………………..

(50,000)

Plus ending payable ………………………………...

60,000

Salaries expense ……………………………………...

$ 285,000

(3) Income tax expense

Pre-tax income ………………………………………...

$ 102,400

Tax rate …………………………………………………...

30%

Income tax expense ………………………………....

$ 30,720

Exercise 22-4 (Continued)

ACCO COMPANY

Budgeted Balance Sheet

As of July 31

ASSETS

Cash (from Exercise 22-3) ……………………………………….….

$ 122,400

Accounts receivable (note 1) ………………………………..….

1,220,000

Inventory (given) ………………………………………………….….

60,000

Total current assets ……………………………………………….

1,402,400

Equipment …………………………………………………………….

$1,600,000

Less accumulated depreciation (note 2) ……………….….

316,000

1,284,000

Total assets ……………………………………………………….

$2,686,400

LIABILITIES AND EQUITY

Liabilities

Accounts payable (note 3) ………………………………….….

$ 300,000

Salaries payable ………………………………………………….

60,000

Income taxes payable ………………………………………….

30,720

Total current liabilities ……………………………………..….

390,720

Bank loan payable ……………………………………………….

660,000

1,050,720

Stockholders’ equity

Common stock …………………………………………………….

600,000

Retained earnings (note 4) …………………………………….

1,035,680

1,635,680

Total liabilities and equity …………………………………..….

$2,686,400

Supporting calculations

(1) Accounts receivable

June sales (20% x $1,200,000) ……….………………….

$ 240,000

July sales (70% x $1,400,000)……….………………….

980,000

Total ……………………………………………..………..

$ 1,220,000

(2) Accumulated depreciation

Beginning ……………………………………..………………..

$ 280,000

Expense ………………………………………..……………..

36,000

Ending ………………………………………….……………

$ 316,000

(3) Accounts payable

Purchases …………………………………….…………………

$ 750,000

Percent unpaid…………………………………………………….

40%

Payable ……………………………………………………….

$ 300,000

(4) Retained earnings

Beginning ……………………………………..………………..

$ 964,000

Net income ……………………………………………………….

71,680

Ending ………………………………………….……………

$1,035,680

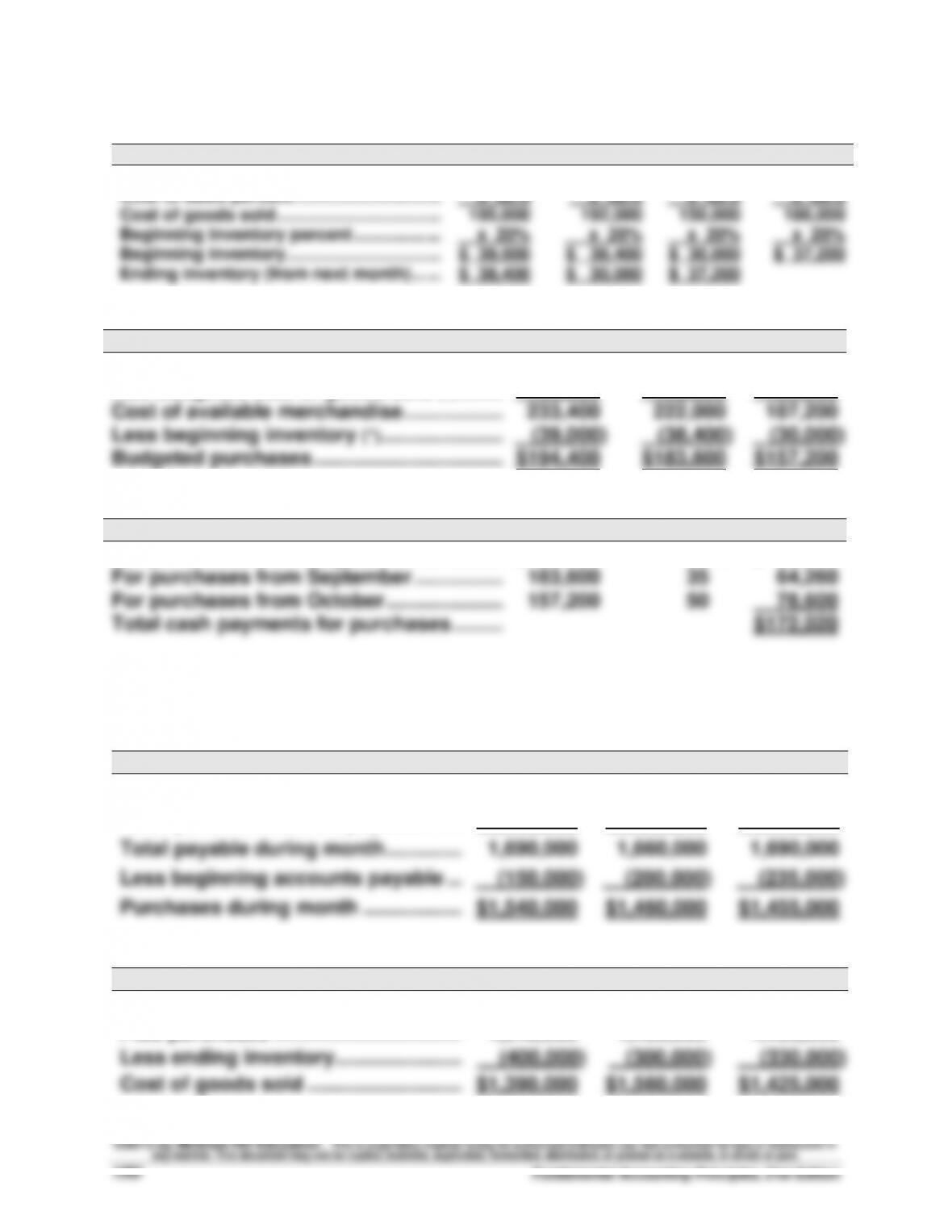

Exercise 22-5 (30 minutes)

Preliminary calculations (sales, cost of sales, beginning and ending inventory)

August

September

October

November

Sales ………………………………………………..…

$325,000

$ 320,000

$250,000

$310,000

Cost to sales percent …………………………..

x 60%

x 60%

x 60%

x 60%

Cost of goods sold …………………………….…

195,000

192,000

150,000

186,000

Beginning inventory percent …………………

x 20%

x 20%

x 20%

x 20%

Beginning inventory …………………………..

$ 39,000

$ 38,400

$ 30,000

$ 37,200

Ending inventory (from next month) ………

$ 38,400

$ 30,000

$ 37,200

Merchandise purchases budgets (* denotes from preliminary calculations)

August

September

October

Budgeted ending inventory (*) ……………….…..

$ 38,400

$ 30,000

$ 37,200

Add budgeted cost of goods sold (*) ……..…..

195,000

192,000

150,000

Cost of available merchandise …………………..

233,400

222,000

187,200

Less beginning inventory (*) ………………….…..

(39,000)

(38,400)

(30,000)

Budgeted purchases …………………………….…..

$194,400

$183,600

$157,200

Cash payments for purchases (on accounts) in October

Dollars

Percent

Paid

For purchases from August ………………….…..

$194,400

15%

$ 29,160

For purchases from September …………….…..

183,600

35

64,260

For purchases from October ……………………..

157,200

50

78,600

Total cash payments for purchases …………..

$172,020

Exercise 22-6 (25 minutes)

1. Budgeted merchandise purchases

June

July

August

Ending accounts payable ……………..……..

$ 200,000

$ 235,000

$ 195,000

Cash paid on accounts payable …….……..

1,490,000

1,425,000

1,495,000

Total payable during month …………..……..

1,690,000

1,660,000

1,690,000

Less beginning accounts payable ………..

(150,000)

(200,000)

(235,000)

Purchases during month ……………………..

$1,540,000

$1,460,000

$1,455,000

2. Budgeted cost of goods sold

June

July

August

Beginning inventory ……………………..……

$ 250,000

$ 400,000

$ 300,000

Plus purchases …………………………….……..

1,540,000

1,460,000

1,455,000

Less ending inventory …………………..……..

(400,000)

(300,000)

(330,000)

Cost of goods sold ……………………….….

$1,390,000

$1,560,000

$1,425,000

©2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Solutions Manual, Chapter 22

1283

1.

Preliminary calculations (sales, cost of sales, beginning inventory)

July

August

September

October

November

Budgeted sales ………………………….

$350,000

$290,000

$320,000

$275,000

$265,000

Cost to sales percent ……………..….

x 70%

x 70%

x 70%

x 70%

x 70%

Budgeted cost of goods sold ….….

245,000

203,000

224,000

192,500

185,500

Budgeted inventory percent ……….

x 20%

x 20%

x 20%

x 20%

x 20%

Budgeted beginning inventory …..….

$ 49,000

$ 40,600

$ 44,800

$ 38,500

$ 37,100

Budgeted merchandise purchases

July

August

September

October

Budgeted ending inventory ………..……

$ 40,600

$ 44,800

$ 38,500

$ 37,100

Budgeted cost of goods sold ……..……

245,000

203,000

224,000

192,500

Cost of available merchandise …………

285,600

247,800

262,500

229,600

Less beginning inventory …………..……

(49,000)

(40,600)

(44,800)

(38,500)

Budgeted purchases ………………….……

$236,600

$207,200

$217,700

$191,100

2.

Budgeted payments on accounts payable in September

Purchases

Percent Paid

Dollars Paid

For purchases from September ……….

$217,700

25%

$ 54,425

For purchases from August ……………..

207,200

60

124,320

For purchases from July ………………….

236,600

15

35,490

Total payments ……………………………….

$214,235

Budgeted payments on accounts payable in October

Purchases

Percent Paid

Dollars Paid

For purchases from October ……………

$191,100

25%

$ 47,775

For purchases from September ……….

217,700

60

130,620

For purchases from August ……………..

207,200

15

31,080

Total payments ……………………………….

$209,475

3.

Budgeted balance of accounts payable at the end of September

Purchases

Percent Unpaid

Dollars Unpaid

From purchases in September ………...

$217,700

75%

$163,275

From purchases in August ……………...

207,200

15

31,080

Total …………………………..…………………..

$194,355

Budgeted balance of accounts payable at the end of October

Purchases

Percent Unpaid

Dollars Unpaid

From purchases in October ……………..

$191,100

75%

$143,325

From purchases in September ………...

217,700

15

32,655

Total …………………………..…………………..

$175,980

Fundamental Accounting Principles, 21st Edition

1284

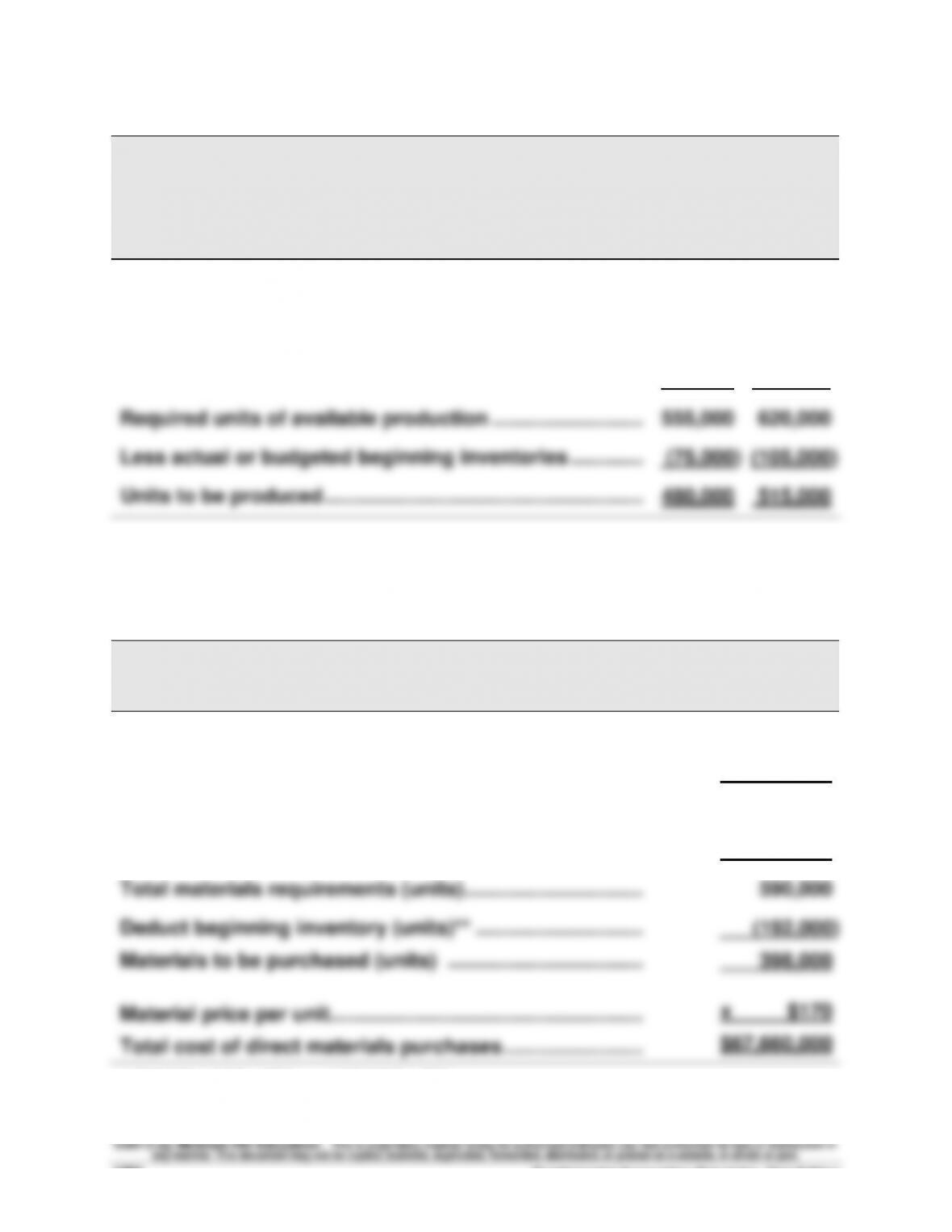

Exercise 22-8 (15 minutes)

ELECTRO COMPANY

Production Budget

Second and Third Quarters

Second

Third

Quarter

Quarter

Budgeted ending inventories

Second quarter (20% x 525,000) ……………………………….……

105,000

Third quarter (20% x 475,000) …………………………………..……

95,000

Add budgeted sales …………………………………………………..…..

450,000

525,000

Required units of available production …………………………..

555,000

620,000

Less actual or budgeted beginning inventories ………….……

(75,000)

(105,000)

Units to be produced ………………………………………………………

480,000

515,000

Exercise 22-9 (15 minutes)

ELECTRO COMPANY

Direct Materials Budget

Second Quarter

Units to be produced (from Exercise 22-8) …………………………..

480,000

Materials requirement per unit …………………………………..……

x 0.80

Materials needed for production (units) ……………………..……

384,000

Add budgeted ending inventory (units)* …………………….……

206,000

Total materials requirements (units) …………………………..

590,000

Deduct beginning inventory (units)** …………………………..

Materials to be purchased (units) ……………………………..……

Material price per unit………………………………………………..……

Total cost of direct materials purchases …………………….……

(192,000)

398,000

x $170

$67,660,000

* (515,000 x 0.80) x 50% **384,000 x 50%

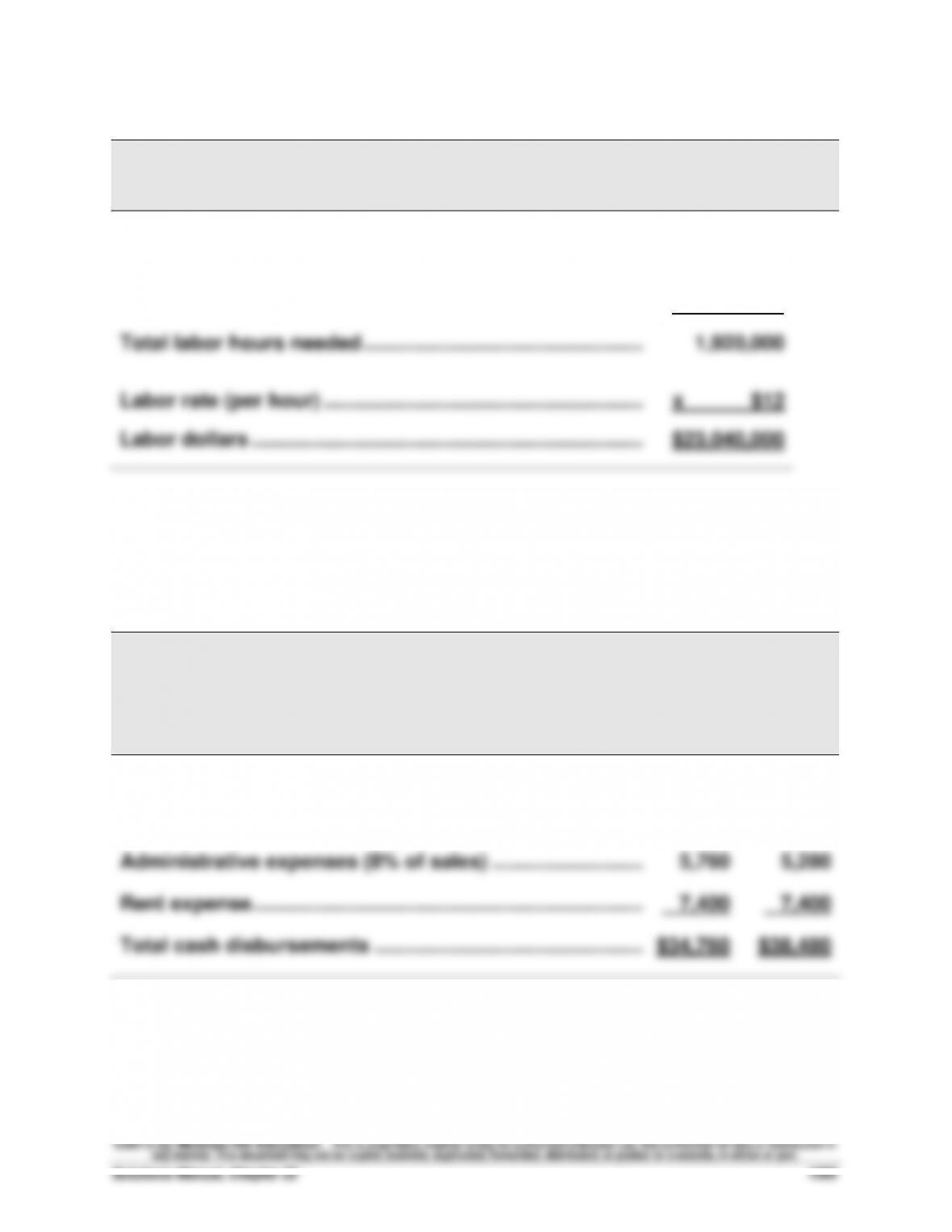

Exercise 22-10 (15 minutes)

ELECTRO COMPANY

Direct Labor Budget

Second Quarter

Units to be produced (from Exercise 22-8) …………………………..

480,000

Labor requirements per unit (hours) …………………………..

x 4

Total labor hours needed …………………………………………..……

1,920,000

Labor rate (per hour) ………………………………………………………

x $12

Labor dollars …………………………………………………………….……

$23,040,000

Exercise 22-11 (10 minutes)

HECTOR COMPANY

Budgeted Cash Disbursements

For August and September

August

Sept.

Payments for merchandise* ……………………………………………

$14,400

$19,200

Selling expenses (10% of sales) ………………………………………

7,200

6,600

Administrative expenses (8% of sales) …………………………..

5,760

5,280

Rent expense …………………………………………………………….……

7,400

7,400

Total cash disbursements ………………………………………………

$34,760

$38,480

**Equals prior month’s purchases. Note that depreciation expense is excluded since it is

a non-cash expense.

Fundamental Accounting Principles, 21st Edition

1286

Exercise 22-12 (15 minutes)

JASPER COMPANY

Cash Receipts Budget

For April, May, and June

April

May

June

Sales …………………………………………………..…

$525,000

$535,000

$560,000

Less ending accts. receivable (70%) ………

367,500

374,500

392,000

Cash receipts from

Cash sales (30% of sales) …………………..…

157,500

160,500

168,000

Collections of prior month’s receivables ……

400,000

367,500

374,500

Total cash receipts …………………………….…

$557,500

$528,000

$542,500

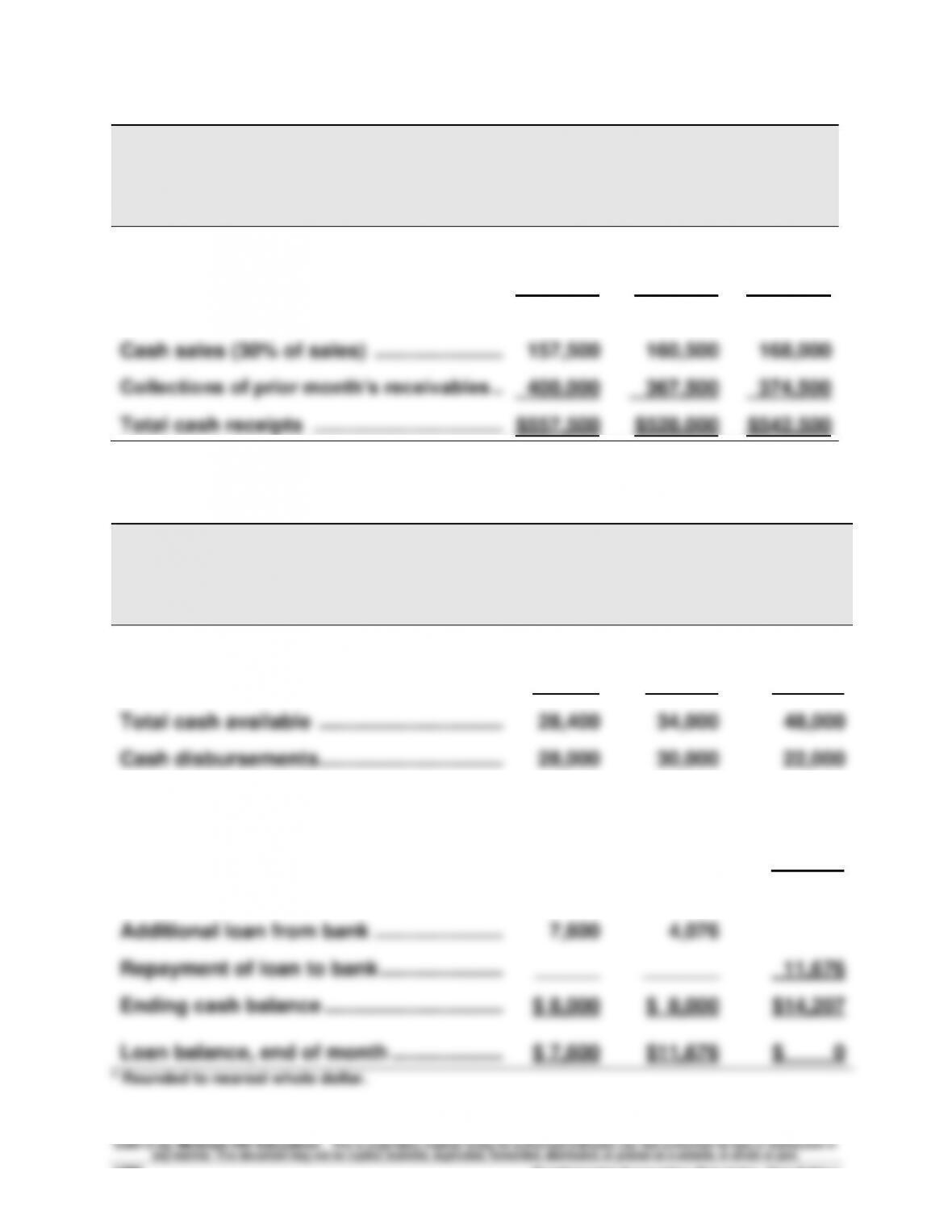

Exercise 22-13 (20 minutes)

KARIM CORP.

Cash Budget

For July, August, and September

July

August

Sept.

Beginning cash balance …………………………

$ 8,400

$ 8,000

$ 8,000

Cash receipts ……………………………………..…

20,000

26,000

40,000

Total cash available ………………………………

28,400

34,000

48,000

Cash disbursements………………………………

28,000

30,000

22,000

Interest on bank loan

August ($7,600 x 1%) ………………………..…

September ($11,676 x 1%)* ……………….…

Preliminary cash balance ………………………

______

$ 400

76

______

$ 3,924

117

$25,883

Additional loan from bank …………………..…

7,600

4,076

Repayment of loan to bank ………………….…

______

_______

11,676

Ending cash balance …………………………..

$ 8,000

$ 8,000

$14,207

Loan balance, end of month ………………..…

$ 7,600

$11,676

$ 0

* Rounded to nearest whole dollar.

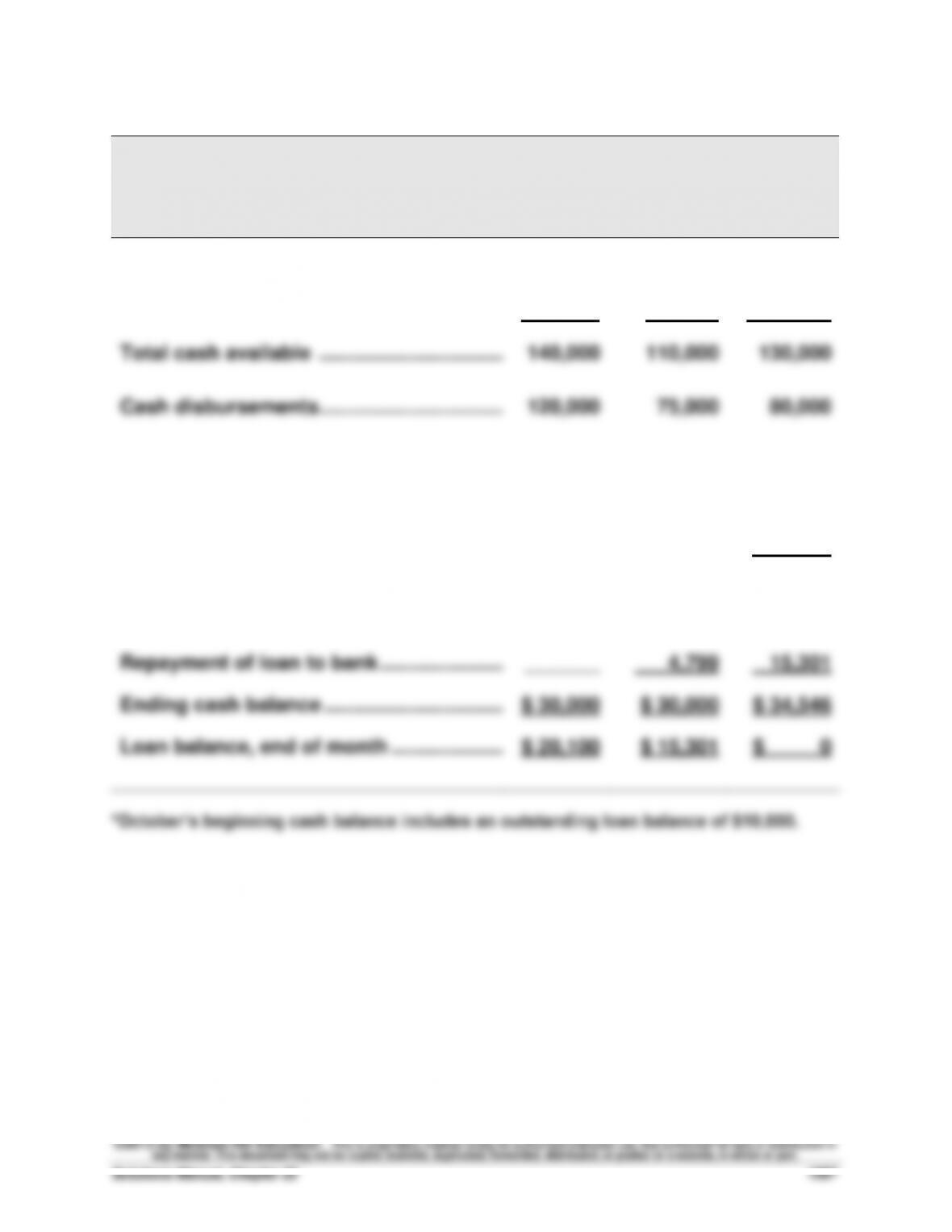

Exercise 22-14 (20 minutes)

FOYERT CORP.

Cash Budget

For October, November, and December

Oct.

Nov.

Dec.

Beginning cash balance* …………………….…

$ 30,000

$ 30,000

$ 30,000

Cash receipts ……………………………………..…

110,000

80,000

100,000

Total cash available ………………………………

140,000

110,000

130,000

Cash disbursements………………………………

120,000

75,000

80,000

Interest on bank loan

October ($10,000 x 1%) …………………….…

November ($20,100 x 1%) ………………….…

December ($15,300 x 1%) ………………….…

Preliminary cash balance ………………………

100

_______

$ 19,900

201

_______

$ 34,799

153

$ 49,847

Additional loan from bank …………………..…

10,100

Repayment of loan to bank ………………….…

_______

4,799

15,301

Ending cash balance …………………………..

$ 30,000

$ 30,000

$ 34,546

Loan balance, end of month ………………..…

$ 20,100

$ 15,301

$ 0

*October’s beginning cash balance includes an outstanding loan balance of $10,000.

Fundamental Accounting Principles, 21st Edition

1288

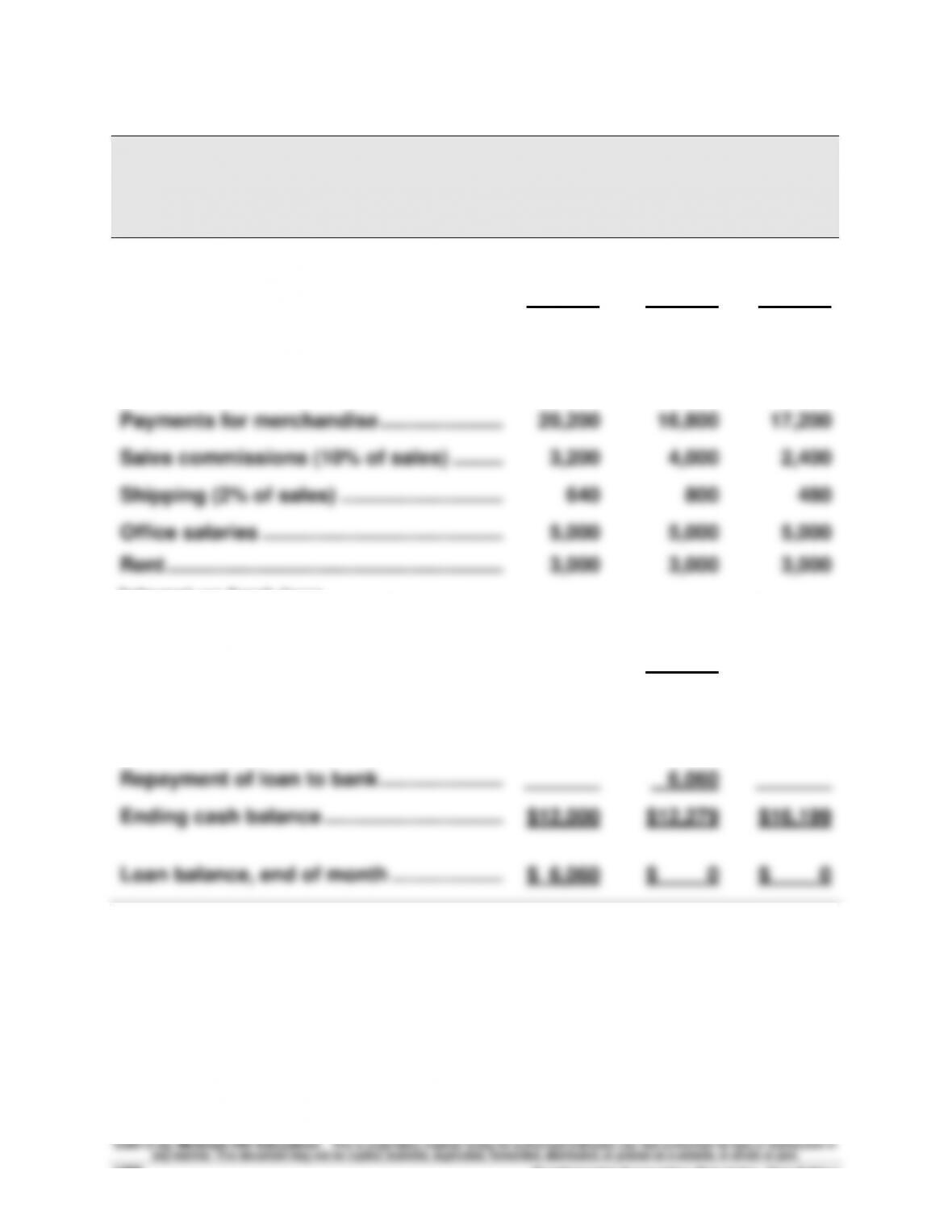

Exercise 22-15 (25 minutes)

CASTOR, INC.

Cash Budget

For April, May, and June

April

May

June

Beginning cash balance* …………………….…

$12,000

$12,000

$12,279

Cash receipts**………………………………………

28,000

36,000

32,000

Total cash available ………………………………

40,000

48,000

44,279

Cash disbursements

Payments for merchandise ………………….…

20,200

16,800

17,200

Sales commissions (10% of sales) …………

3,200

4,000

2,400

Shipping (2% of sales) ………………………..…

640

800

480

Office salaries …………………………………….…

Rent ………………………………………………………

Interest on bank loan

April ($2,000 x 1%) ………………………………

May ($6,060 x 1%) …………………………….…

Preliminary cash balance ………………………

5,000

3,000

20

______

$7,940

5,000

3,000

61

$18,339

5,000

3,000

_______

$16,199

Additional loan from bank …………………..…

4,060

Repayment of loan to bank ………………….…

_______

6,060

_______

Ending cash balance …………………………..

$12,000

$12,279

$16,199

Loan balance, end of month ………………..…

$ 6,060

$ 0

$ 0

*April’s beginning cash balance includes an outstanding loan payable of $2,000.

**Per cash receipts budget on next page

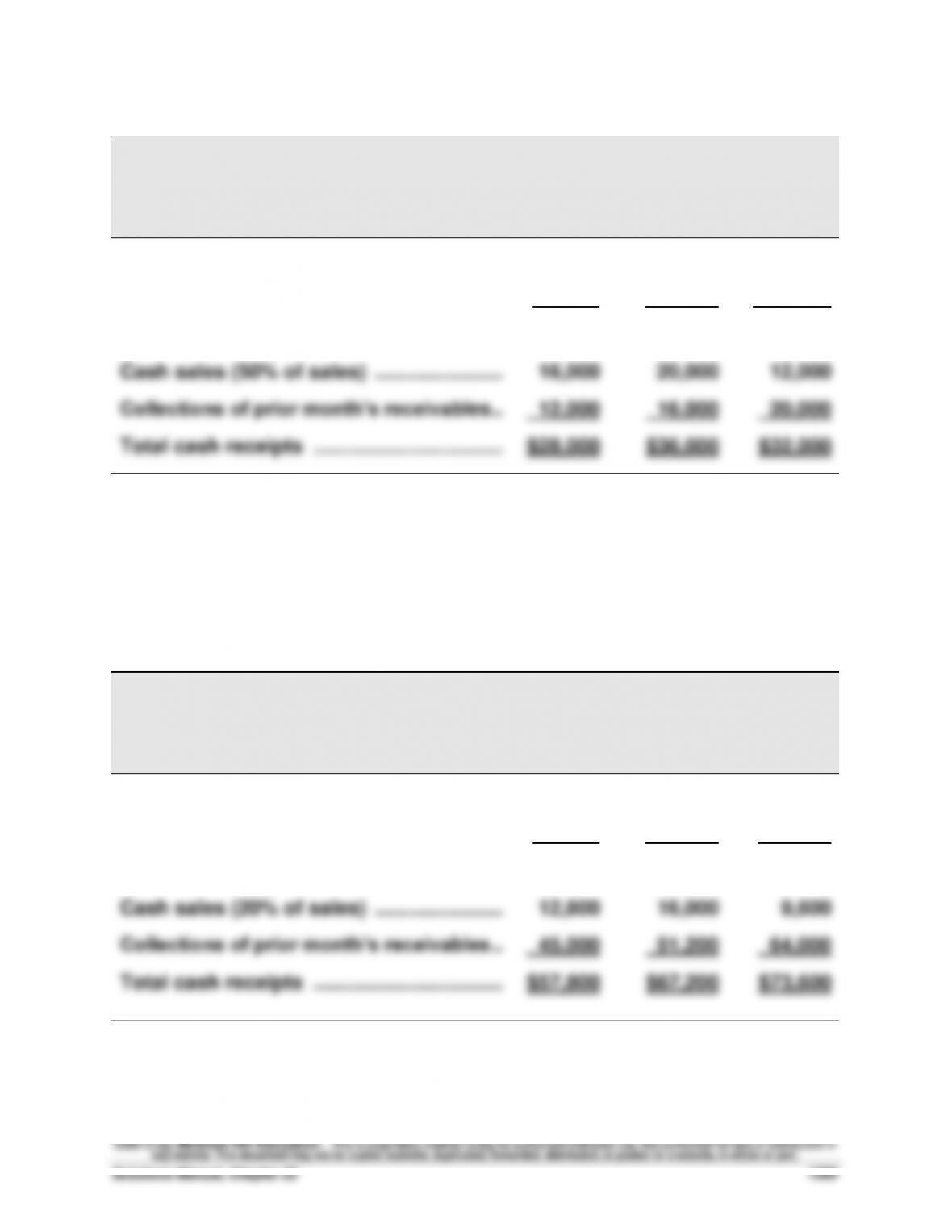

Exercise 22-15 (continued)

CASTOR, INC.

Cash Receipts Budget

For April, May, and June

April

May

June

Sales …………………………………………………..…

$32,000

$40,000

$24,000

Less ending accts. receivable (50%) ………

16,000

20,000

12,000

Cash receipts from

Cash sales (50% of sales) …………………..…

16,000

20,000

12,000

Collections of prior month’s receivables ……

12,000

16,000

20,000

Total cash receipts …………………………….…

$28,000

$36,000

$32,000

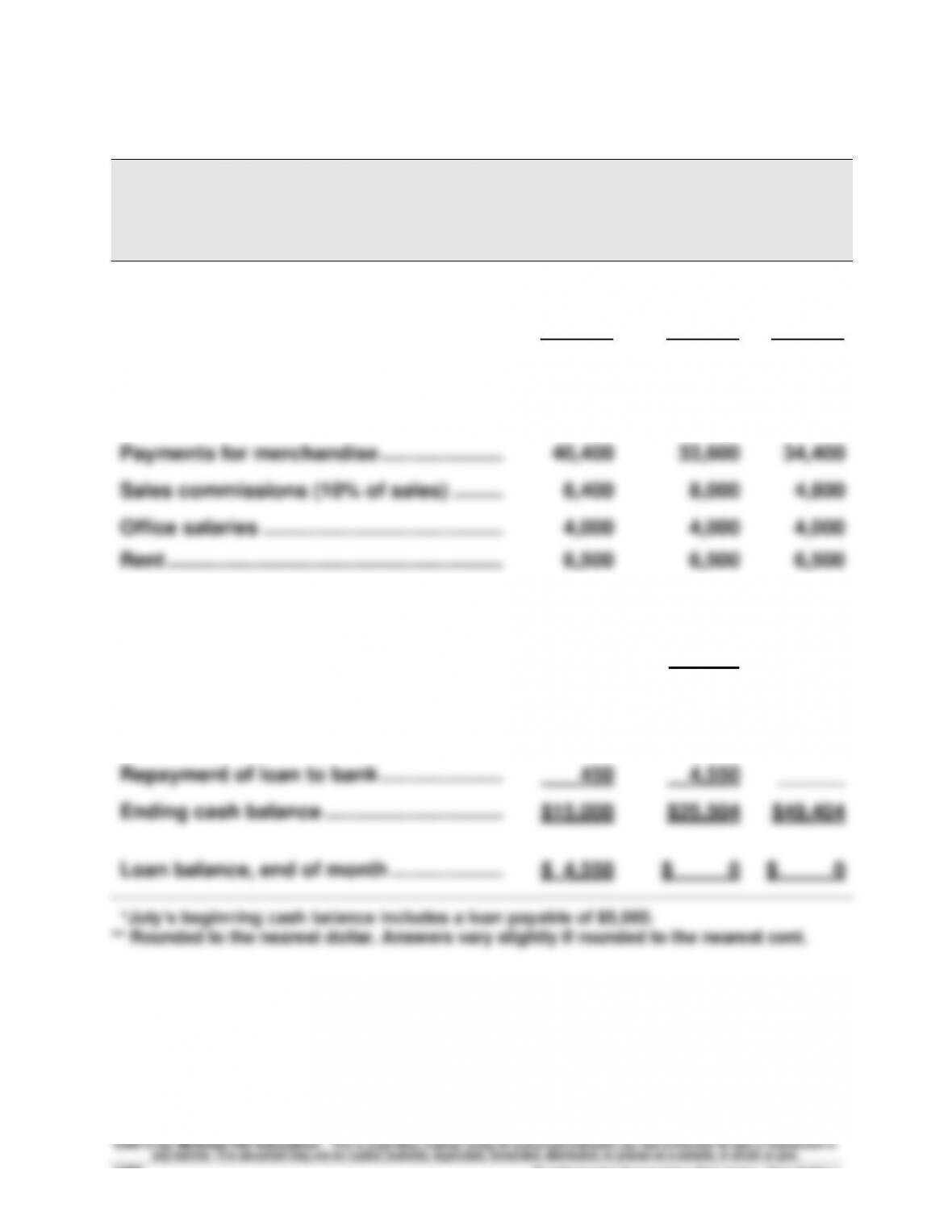

Exercise 22-16 (30 minutes)

(1)

KELSEY

Cash Receipts Budget

For July, August, and September

July

August

Sept.

Sales …………………………………………………..…

$64,000

$80,000

$48,000

Less ending accts. receivable (80%) ………

51,200

64,000

38,400

Cash receipts from

Cash sales (20% of sales) …………………..…

12,800

16,000

9,600

Collections of prior month’s receivables ……

45,000

51,200

64,000

Total cash receipts …………………………….…

$57,800

$67,200

$73,600

Fundamental Accounting Principles, 21st Edition

1290

Exercise 22-16 (continued)

(2)

KELSEY

Cash Budget

For July, August, and September

July

August

Sept.

Beginning cash balance* …………………….…

$15,000

$15,000

$25,504

Cash receipts (from part 1) ………………….…

57,800

67,200

73,600

Total cash available ………………………………

72,800

82,200

99,104

Cash disbursements

Payments for merchandise ………………….…

40,400

33,600

34,400

Sales commissions (10% of sales) …………

6,400

8,000

4,800

Office salaries …………………………………….…

Rent ………………………………………………………

Interest on bank loan**

July (5,000 x 1%) …………………………………

August ($4,550 x 1%) ………………………..…

Preliminary cash balance ………………………

4,000

6,500

50

_______

$15,450

4,000

6,500

46

$30,054

4,000

6,500

_______

$49,404

Additional loan from bank …………………..…

Repayment of loan to bank ………………….…

450

4,550

______

Ending cash balance …………………………..

$15,000

$25,504

$49,404

Loan balance, end of month ………………..…

$ 4,550

$ 0

$ 0

*July’s beginning cash balance includes a loan payable of $5,000.

** Rounded to the nearest dollar. Answers vary slightly if rounded to the nearest cent.

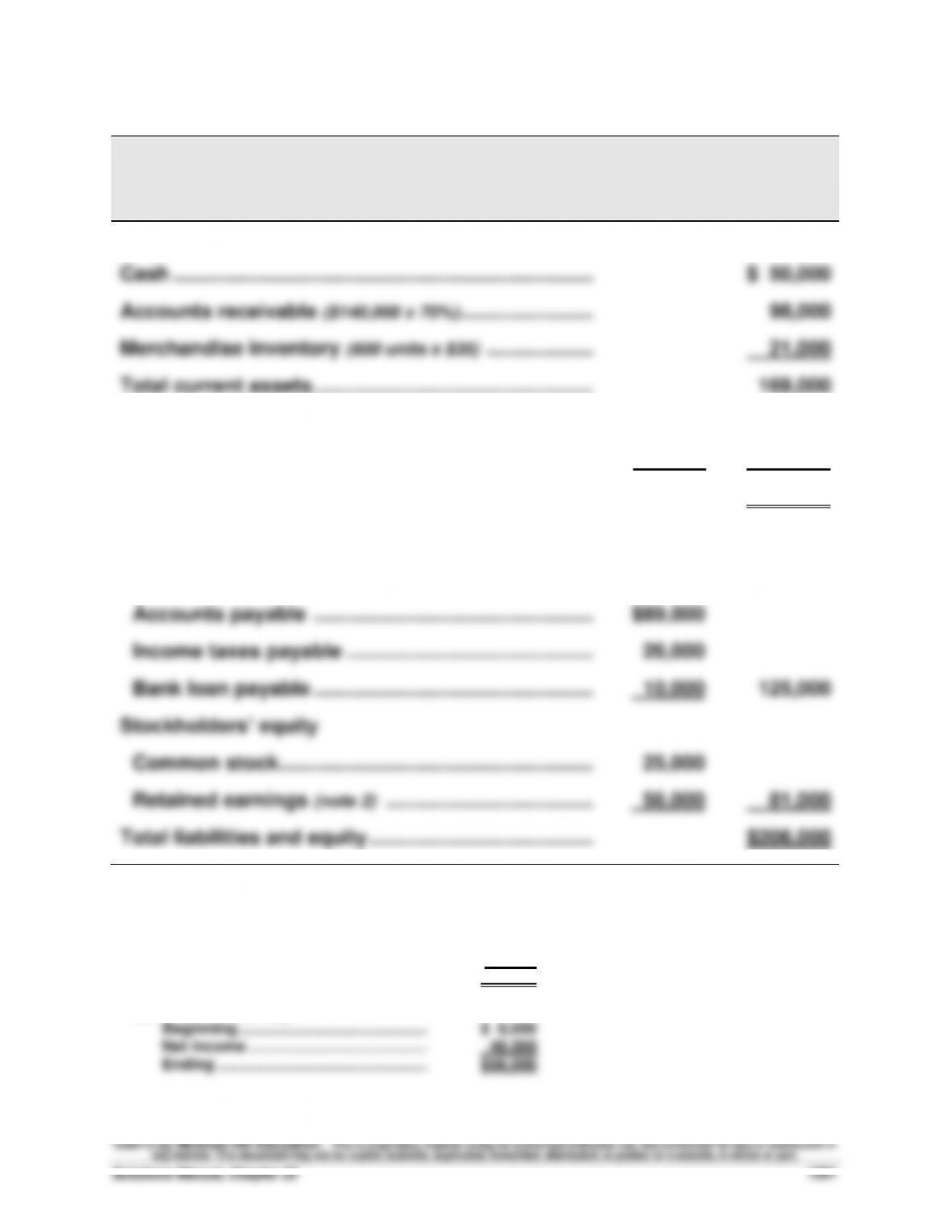

Exercise 22-17 (15 minutes)

ZETROV COMPANY

Budgeted Balance Sheet

As of March 31

ASSETS

Cash ……………………………………………………….…………….

$ 50,000

Accounts receivable ($140,000 x 70%) …………………….….

98,000

Merchandise inventory (600 units x $35) ………………..….

21,000

Total current assets ……………………………………………….

169,000

Equipment …………………………………………………………….

$84,000

Less accumulated depreciation (note 1) ………………….

47,000

37,000

Total assets ……………………………………………………….

$206,000

LIABILITIES AND EQUITY

Liabilities

Accounts payable ……………………………………………….

$89,000

Income taxes payable ………………………………………….

26,000

Bank loan payable ……………………………………………….

10,000

125,000

Stockholders’ equity

Common stock …………………………………………………….

25,000

Retained earnings (note 2) ………………………………..….

56,000

81,000

Total liabilities and equity …………………………………..….

$206,000

Supporting calculations

(1) Accumulated depreciation

Beginning ……………………………………..………………..

$46,000

Depreciation expense …………………………..

1,000

Ending ………………………………………….……………

$47,000

(2) Retained earnings

Beginning ……………………………………..………………..

$ 8,000

Net income ……………………………………………………….

48,000

Ending ………………………………………….……………

$56,000

Fundamental Accounting Principles, 21st Edition

1292

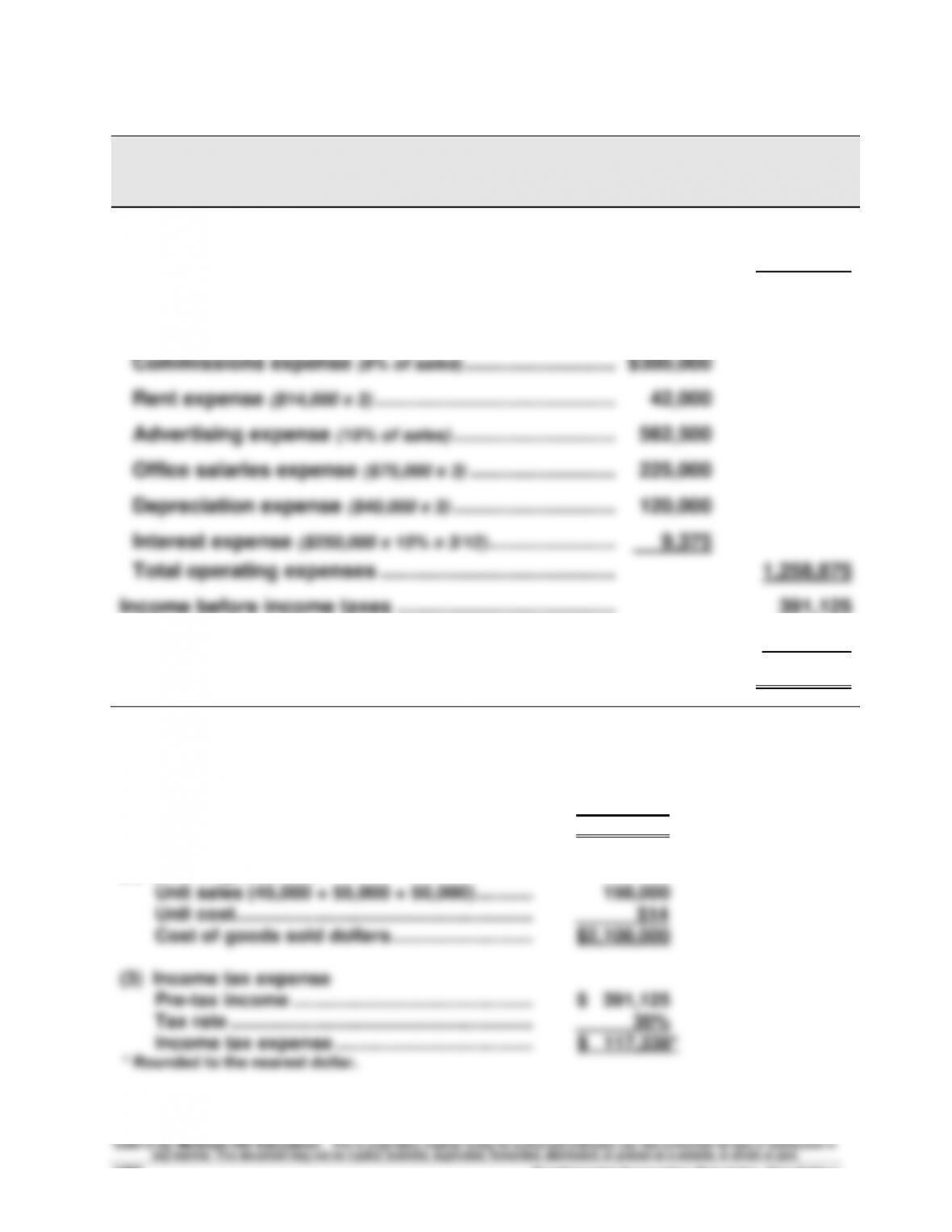

Exercise 22-18 (15 minutes)

FORTUNE, INC.

Budgeted Income Statement

For Quarter Ended March 31

Sales (note 1) …………………………………………………………...

$3,750,000

Cost of goods sold (note 2) ……………………………………...

2,100,000

Gross profit …………………………………………………………...

1,650,000

Operating expenses

Commissions expense (8% of sales) ………………………..

$300,000

Rent expense ($14,000 x 3) ……………………………………...

42,000

Advertising expense (15% of sales) ………………………....

562,500

Office salaries expense ($75,000 x 3) ……………………....

225,000

Depreciation expense ($40,000 x 3) ………………………....

120,000

Interest expense ($250,000 x 15% x 3/12) …………………....

Total operating expenses ……………………………………..

9,375

1,258,875

Income before income taxes …………………………………..

391,125

Income tax expense (note 3) ……………………………………..

117,338

Net income ……………………………………………………………..

$ 273,787

Supporting calculations

(1) Sales

Unit sales (45,000 + 55,000 + 50,000) ………....

150,000

Unit price ………………………………………………...

$25

Sales dollars …………………………………………....

$3,750,000

(2) Cost of goods sold

Unit sales (45,000 + 55,000 + 50,000) ………....

150,000

Unit cost…………………………………………………..

$14

Cost of goods sold dollars ………………………..

$2,100,000

(3) Income tax expense

Pre-tax income ………………………………………...

$ 391,125

Tax rate …………………………………………………...

30%

Income tax expense ………………………………....

$ 117,338*

* Rounded to the nearest dollar.