Problem 22-3B (Continued)

Part 4

Cash payments on product purchases (for March and April)

From purchases in

Total

% Paid

March

April

February ……………………………..….

$261,600

70%

$183,120

March …………………………………….

227,400

30

68,220

………………………………….….

70

$159,180

April ……………………………………….

230,400

30

_______

69,120

Total paid ……………………………….

$251,340

$228,300

Part 5

CONNICK COMPANY

Cash Budget

March and April

March

April

Beginning cash balance ………………………………………..………..

$ 50,000

$ 58,070

Cash receipts from customers ………………………………………..

431,530

425,150

Total available cash ……………………………………………………….

481,530

483,220

Cash disbursements

Payments on purchases ……………………………………..………..

251,340

228,300

Selling and administrative expenses …………………………..

160,000

160,000

Interest expense* ………………………………………………..……..

120

0

Total disbursements …………………………………………..………..

411,460

388,300

Preliminary cash balance ………………………………………………..

$ 70,070

$ 94,920

Additional loan ……………………………………………………....

Repayment of loan ………………………………………………..……..

(12,000)

________

Ending cash balance …………………………………………….………..

$ 58,070

$ 94,920

Ending loan balance ……………………………………………..………..

$ 0

$ 0

*Interest expense: March = $12,000 x 12% /12 = $120

Part 6

Analysis Component: Information about the supply of cash in the near future

would be helpful to the management of Connick Company. A good cash

Fundamental Accounting Principles, 21st Edition

1324

Problem 22-4B (50 minutes)

Part 1

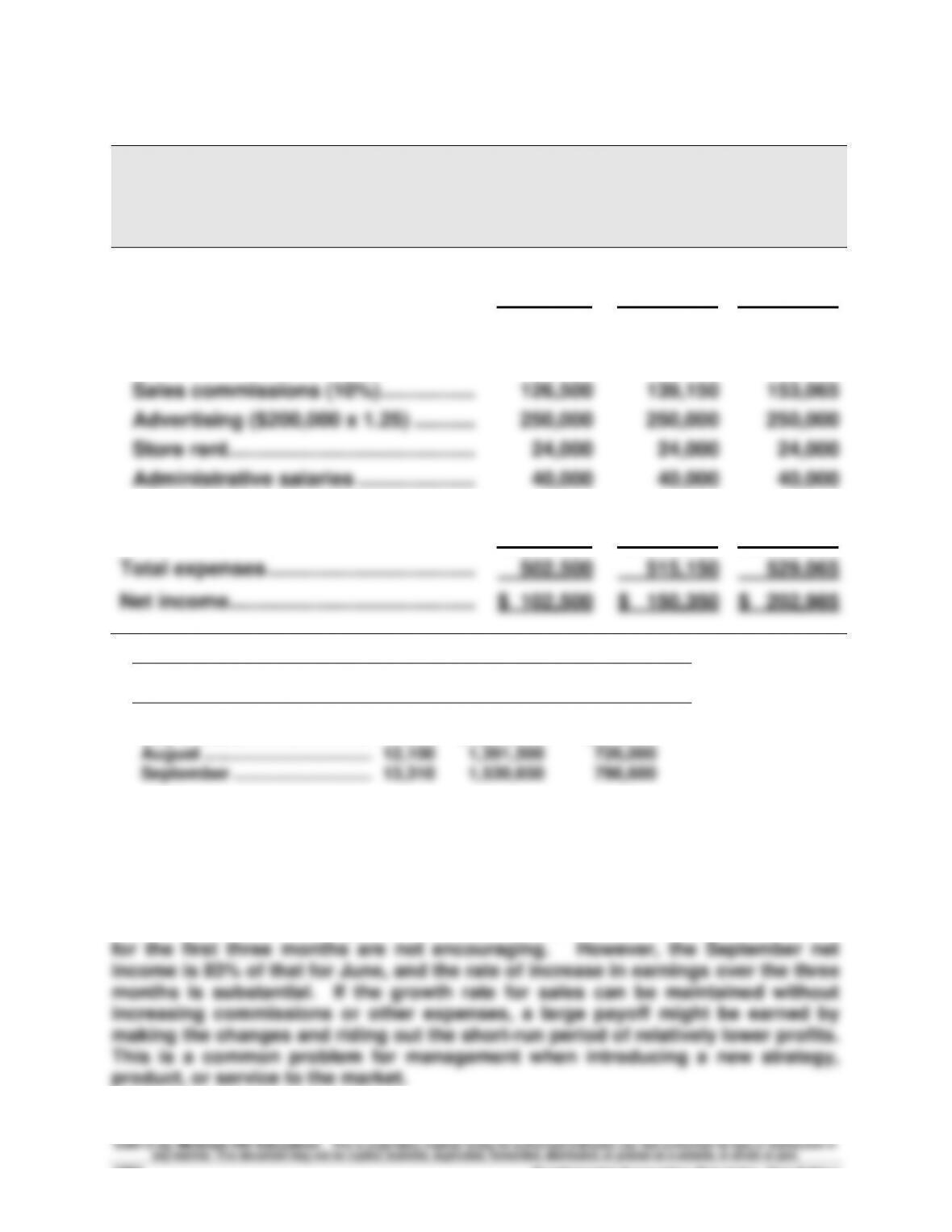

COMP-MEDIA

Budgeted Income Statement

For Months of July, August, and September, 2013

July

August

September

Sales* …………………………………………….…..

$1,265,000

$1,391,500

$1,530,650

Cost of goods sold* ………………………..…

660,000

726,000

798,600

Gross profit ………………………………………..

605,000

665,500

732,050

Expenses

Sales commissions (10%) ……………..…..

126,500

139,150

153,065

Advertising ($200,000 x 1.25) ………..…..

250,000

250,000

250,000

Store rent ……………………………………..…..

24,000

24,000

24,000

Administrative salaries ……………………..

40,000

40,000

40,000

Depreciation ……………………………………..

50,000

50,000

50,000

Other ………………………………………………..

12,000

12,000

12,000

Total expenses ……………………………….…..

502,500

515,150

529,065

Net income ……………………………………..…..

$ 102,500

$ 150,350

$ 202,985

* Volume for the next three months increases by 10% per month

Sales

Cost of Goods

Units

(@ $115)

Sold (@ $60)

June ($1,300,000/$130) …………………………

10,000

July ………………………………….…………………

11,000

$1,265,000

$660,000

August ……………………………..…………………

12,100

1,391,500

726,000

September ………………………..…

13,310

1,530,650

798,600

Part 2: Analysis Component

The plan for increasing sales volume by reducing the price and increasing

advertising would cause the company to generate less net income in each of the

three months of the next quarter than was earned in June. The expected results

Problem 22-5B (130 minutes)

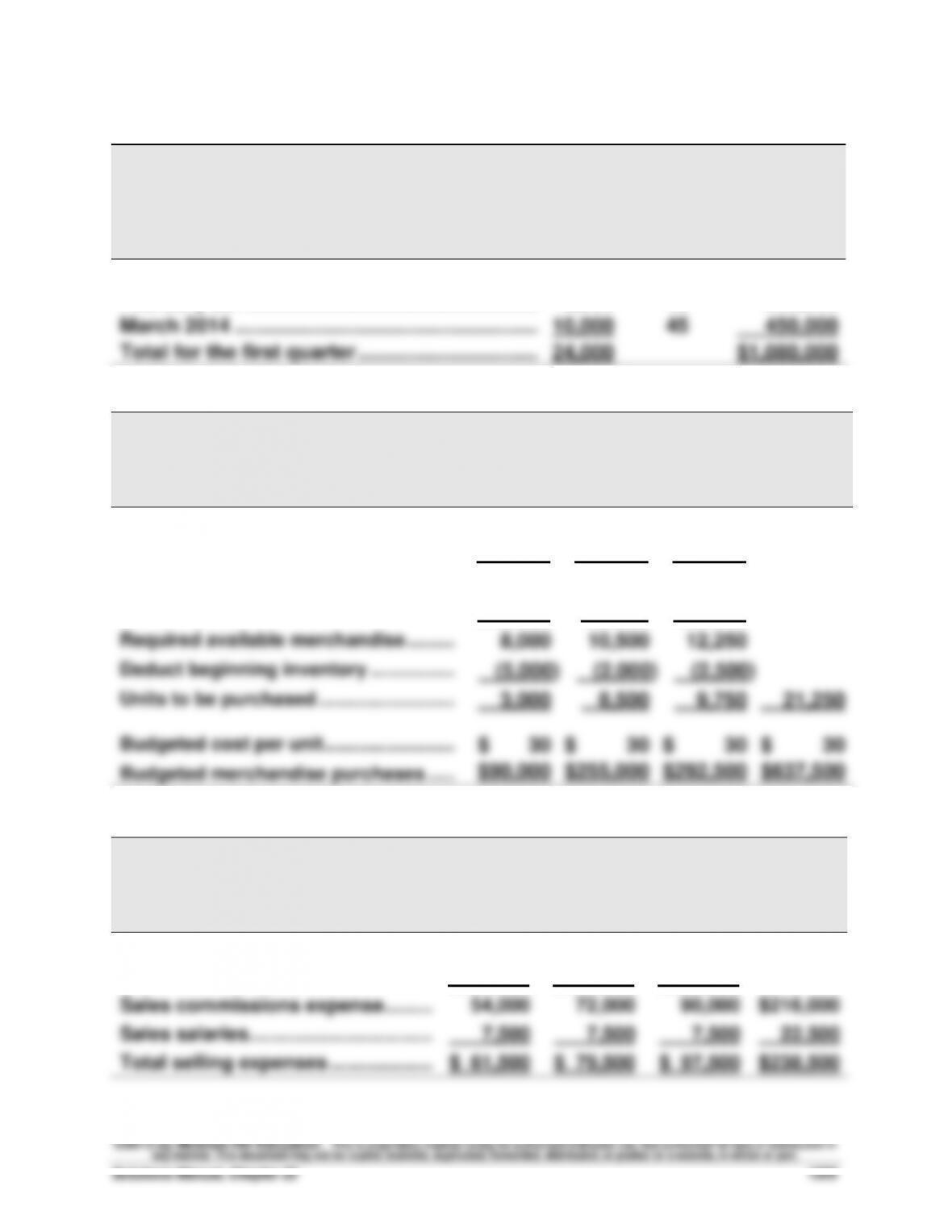

Part 1

ISLE CORPORATION

Sales Budgets

January, February, and March 2014

Budgeted

Units

Budgeted

Unit Price

Budgeted

Total Dollars

January 2014 …………………………………………….…

6,000

$45

$ 270,000

February 2014………………………………………………

8,000

45

360,000

March 2014 ……………………………………………….…

10,000

45

450,000

Total for the first quarter ………………………………

24,000

$1,080,000

Part 2

ISLE CORPORATION

Merchandise Purchases Budgets

January, February, and March 2014

January

February

March

Total

Next month’s budgeted sales …………...

8,000

10,000

9,000

Ratio of inventory to future sales ……...

x 25%

x 25%

x 25%

Budgeted ending inventory ……………...

2,000

2,500

2,250

Add budgeted sales ………………………….

6,000

8,000

10,000

Required available merchandise ……….

8,000

10,500

12,250

Deduct beginning inventory ……………..

(5,000)

(2,000)

(2,500)

Units to be purchased ……………………...

3,000

8,500

9,750

21,250

Budgeted cost per unit ……………………..

$ 30

$ 30

$ 30

$ 30

Budgeted merchandise purchases …...

$90,000

$255,000

$292,500

$637,500

Part 3

ISLE CORPORATION

Selling Expense Budgets

January, February, and March 2014

January

February

March

Total

Budgeted sales …………………………..

$270,000

$360,000

$450,000

Sales commission percent ………….…..

x 20%

x 20%

x 20%

Sales commissions expense ……….…..

54,000

72,000

90,000

$216,000

Sales salaries……………………………..…..

7,500

7,500

7,500

22,500

Total selling expenses ………………..…..

$ 61,500

$ 79,500

$ 97,500

$238,500

Fundamental Accounting Principles, 21st Edition

1326

Problem 22-5B (Continued)

Part 4

ISLE CORPORATION

General and Administrative Expense Budgets

January, February, and March 2014

January

February

March

Total

Salaries …………………………..…………………..

$12,000

$12,000

$12,000

$36,000

Maintenance …………………………..…….……..

3,000

3,000

3,000

9,000

Depreciation* ………………………………..……..

6,375

7,375

7,675

21,425

Total expenses ……………………………..……..

$21,375

$22,375

$22,675

$66,425

* Depreciation expense calculations

Annual

Amount

January

February

March

Total

Equipment owned

on 12/31/2013 ………………..

$67,500

$5,625

$5,625

$5,625

$16,875

Purchased in January ……..

9,000

750

750

750

2,250

Purchased in February …….

12,000

1,000

1,000

2,000

Purchased in March …………

3,600

______

______

300

300

Total …………………………..…..

$6,375

$7,375

$7,675

$21,425

Part 5

ISLE CORPORATION

Capital Expenditures Budgets

January, February, and March 2014

January

February

March

Equipment purchases ……………………………..……

$72,000

$96,000

$ 28,800

Land purchase …………………………..…………………

_______

_______

150,000

Total ……………………………………………………….

$72,000

$96,000

$178,800

Problem 22-5B (Continued)

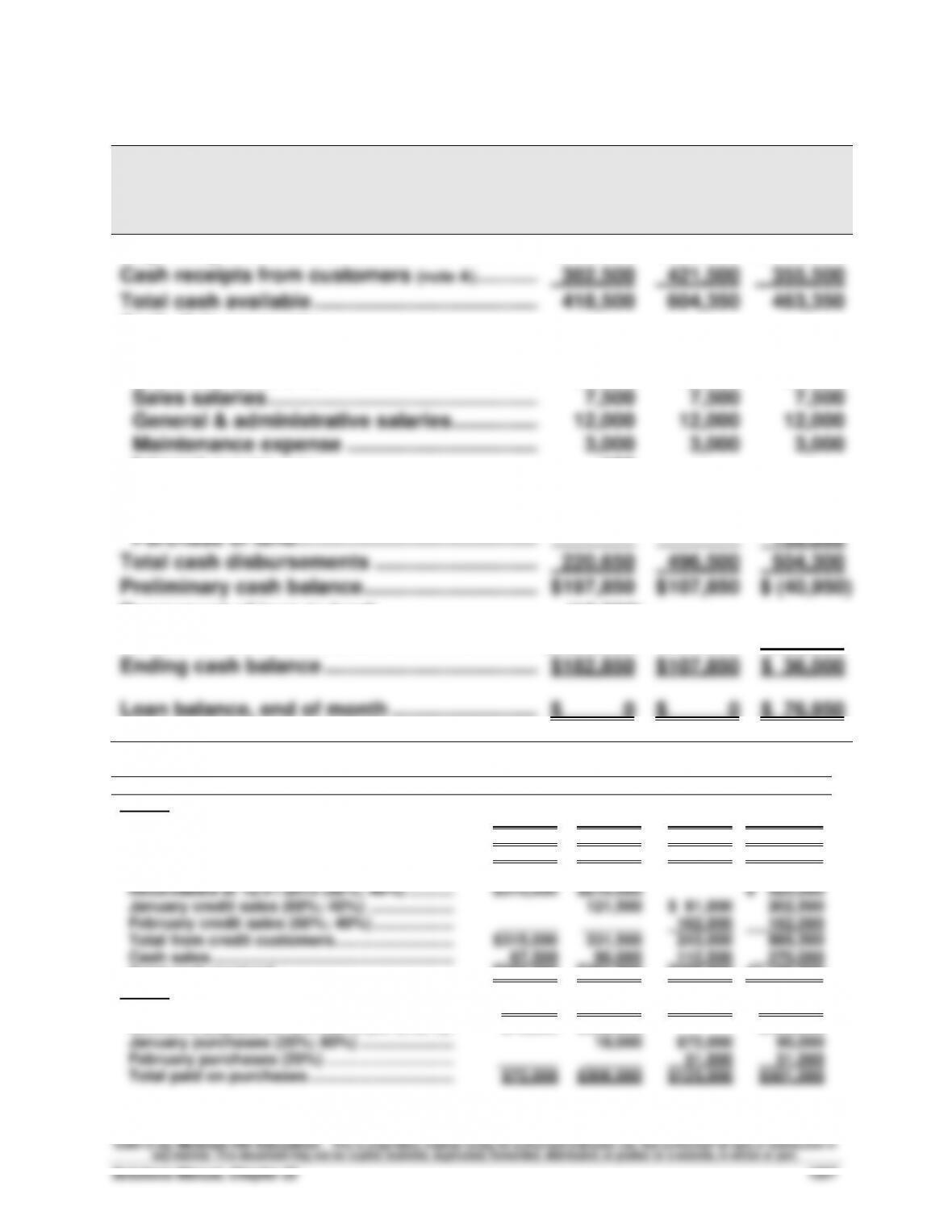

Part 6

ISLE CORPORATION

Cash Budgets

January, February, and March 2014

January

February

March

Beginning cash balance …………………………….….

$ 36,000

$182,850

$ 107,850

Cash receipts from customers (note A)…………….

382,500

421,500

355,500

Total cash available …………………………………..….

418,500

604,350

463,350

Cash disbursements

Payments for merchandise (note B) ……………….

72,000

306,000

123,000

Sales commissions …………………………………….

54,000

72,000

90,000

Sales salaries ………………………………………….….

7,500

7,500

7,500

General & administrative salaries …………….….

12,000

12,000

12,000

Maintenance expense ……………………………..….

3,000

3,000

3,000

Interest ($15,000 x 1%) ………………………………….….

150

Taxes payable …………………………………………….

90,000

Purchases of equipment …………………………..

72,000

96,000

28,800

Purchase of land ……………………………………..….

________

________

150,000

Total cash disbursements …………………………..

220,650

496,500

504,300

Preliminary cash balance …………………………..

$197,850

$107,850

$ (40,950)

Repayment of loan to bank ………………………..…

(15,000)

Additional loan from bank …………………………..

________

________

76,950

Ending cash balance …………………………………….

$182,850

$107,850

$ 36,000

Loan balance, end of month ………………………….

$ 0

$ 0

$ 76,950

Supporting calculations

January

February

March

Total

Note A: Cash receipts from customers

Total sales …………………………..…………………….

$270,000

$360,000

$450,000

$1,080,000

Cash sales (25%) ……………………………………….

$ 67,500

$ 90,000

$112,500

$ 270,000

Credit sales (75%) ……………………………………..

$202,500

$270,000

$337,500

$ 810,000

Cash collections

Receivables at 12/31/2013 (60%; 40%) ………..

$315,000

$210,000

$ 525,000

January credit sales (60%; 40%) ………………..

121,500

$ 81,000

202,500

February credit sales (60%; 40%) ……………….

_______

_______

162,000

162,000

Total from credit customers ……………………….

$315,000

331,500

243,000

889,500

Cash sales…………………………………………………

67,500

90,000

112,500

270,000

Total cash received ……………………………………

$382,500

$421,500

$355,500

$1,159,500

Note B: Cash payments for merchandise

Credit purchases ……………………………………….

$90,000

$255,000

$292,500

$637,500

Accounts payable at 12/31/2013 (20%; 80%) .

$72,000

$288,000

$360,000

January purchases (20%; 80%) ………………….

18,000

$72,000

90,000

February purchases (20%) …………………………

_______

_______

51,000

51,000

Total paid on purchases …………………………….

$72,000

$306,000

$123,000

$501,000

Fundamental Accounting Principles, 21st Edition

1328

Problem 22-5B (Continued)

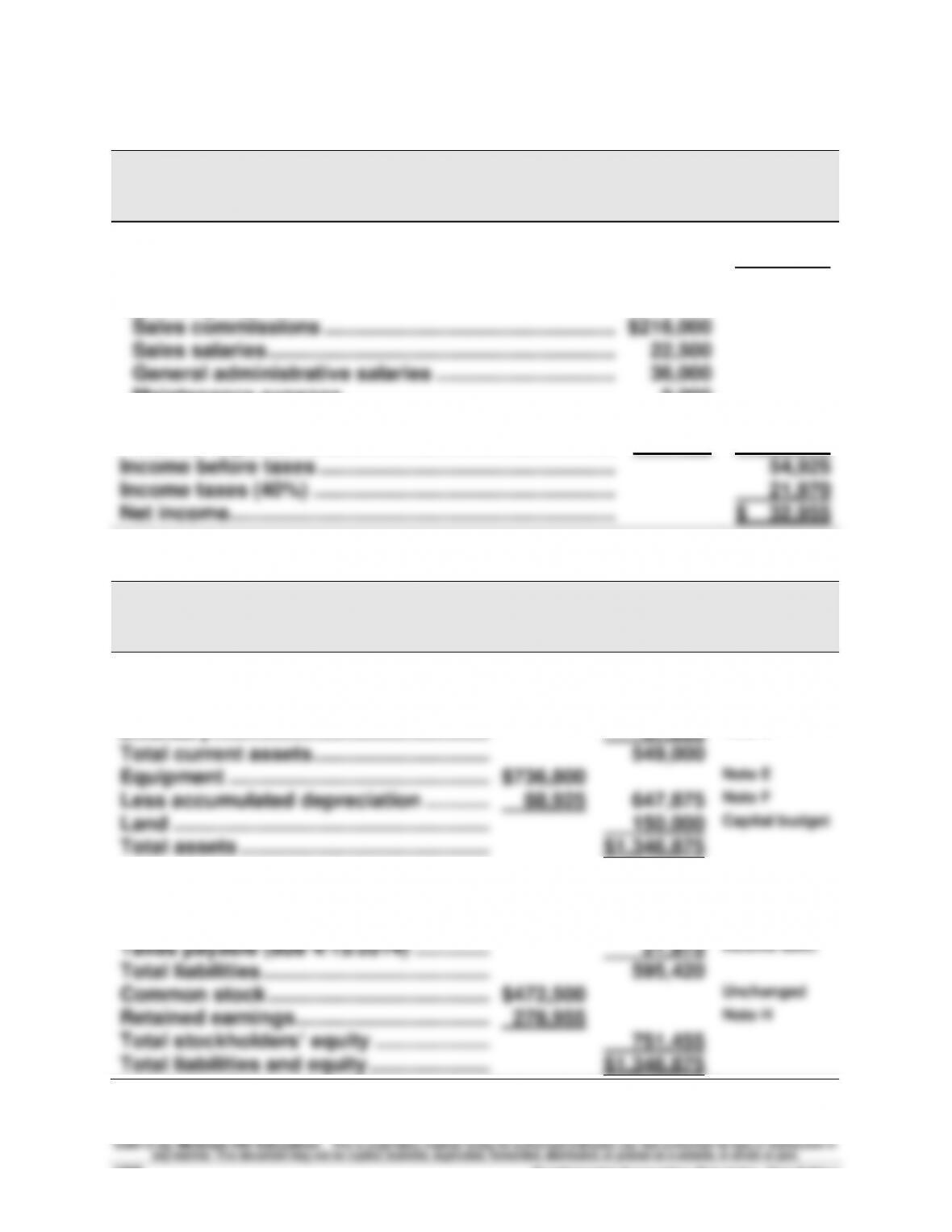

Part 7

ISLE CORPORATION

Budgeted Income Statement

For Three Months Ended March 31, 2014

Sales ……………………………………………………………………..

$1,080,000

Cost of goods sold (24,000 units @ $30) ………………...

720,000

Gross profit ……………………………………………………….….

360,000

Operating expenses

Sales commissions ……………………………………………..

$216,000

Sales salaries ……………………………………………………...

22,500

General administrative salaries …………………………..

36,000

Maintenance expense ………………………………………….

9,000

Depreciation expense ………………………………………….

21,425

Interest expense ………………………………………………….

150

305,075

Income before taxes ……………………………………………...

54,925

Income taxes (40%) ……………………………………………….

21,970

Net income …………………………………………………………….

$ 32,955

Part 8

ISLE CORPORATION

Budgeted Balance Sheet

March 31, 2014

ASSETS

Cash …………………………..…………………….…

$ 36,000

Cash budget

Accounts receivable …………………………..

445,500

Note C

Inventory …………………………………………..…

67,500

Note D

Total current assets …………………………..

549,000

Equipment ………………………………………..…

$736,800

Note E

Less accumulated depreciation ……………

88,925

647,875

Note F

Land ……………………………………………………

150,000

Capital budget

Total assets …………………………..………….…

$1,346,875

LIABILITIES AND EQUITY

Accounts payable ……………………………..…

$ 496,500

Note G

Bank loan payable …………………………….…

76,950

Cash budget

Taxes payable (due 4/15/2014) …………..…

21,970

Income stmt.

Total liabilities …………………………………..…

595,420

Common stock ………………………………….…

$472,500

Unchanged

Retained earnings ……………………………..…

278,955

Note H

Total stockholders’ equity ……………………

751,455

Total liabilities and equity ………………….…

$1,346,875

Problem 22-5B (Concluded)

Supporting Footnotes

Note C

Beginning receivables ……………………………………………………….

$ 525,000

Credit sales ………………………………………………………………………..

810,000

Less collections …………………………………………………………….…..

(889,500)

Ending receivables ……………………………………………………………..

$ 445,500

Note D

Beginning inventory ……………………………………………………….

$ 150,000

Purchases ……………………………………………………………………..…..

637,500

Less cost of goods sold ……………………………………………………..

(720,000)

Ending inventory* …………………………………………………………..…..

$ 67,500

*Also equals 2,250 units @ $30 = $67,500

Note E

Beginning equipment ……………………………………………………....

$ 540,000

Purchased in January …………………………………………………….…

72,000

Purchased in February……………………………………………………….

96,000

Purchased in March ……………………………………………………….

28,800

Total ……………………………………………………………………………..…..

$ 736,800

Note F

Beginning accumulated depreciation …………………………………..

$ 67,500

Depreciation expense …………………………………………………….…

21,425

Total ……………………………………………………………………………..…..

$ 88,925

Note G

Beginning accounts payable …………………………………………..…..

$ 360,000

Purchases ……………………………………………………………………..…..

637,500

Payments …………………………..………………………………………….…..

(501,000)

Ending accounts payable ……………………………………………….…..

$ 496,500

Note H

Beginning retained earnings …………………………………………..…..

$ 246,000

Net income …………………………..………………………………………..…..

32,955

Total ……………………………………………………………………………..…..

$ 278,955

Fundamental Accounting Principles, 21st Edition

1330

Problem 22-6B (30 minutes)

Part 1

NSA COMPANY

Production Budget (in units)

Second Quarter

Budgeted ending inventory (bats) ………………………………………….…….

6,000

Add budgeted sales ……………………………………………………………….…….

250,000

Required units of available production …………………………………..…….

256,000

Deduct beginning inventory (bats) ……………………………………………….

(8,000)

Units to be manufactured ……………………………………………………….

248,000

Part 2

NSA COMPANY

Direct Materials Budget (in lbs, except where noted)

Second Quarter

Materials (aluminum) needed for production (248,000 x 3) …………

744,000

Add budgeted ending inventory (aluminum) …………………………..

12,000

Total materials (aluminum) requirements ……………………………….…

756,000

Deduct beginning inventory (aluminum) ……………………………………

(15,000)

Units of materials (aluminum) to be purchased …………………………

741,000

Materials cost per pound ……………………………………………………….

$4

Total cost of materials purchases (741,000 x $4) …………………….…

$2,964,000

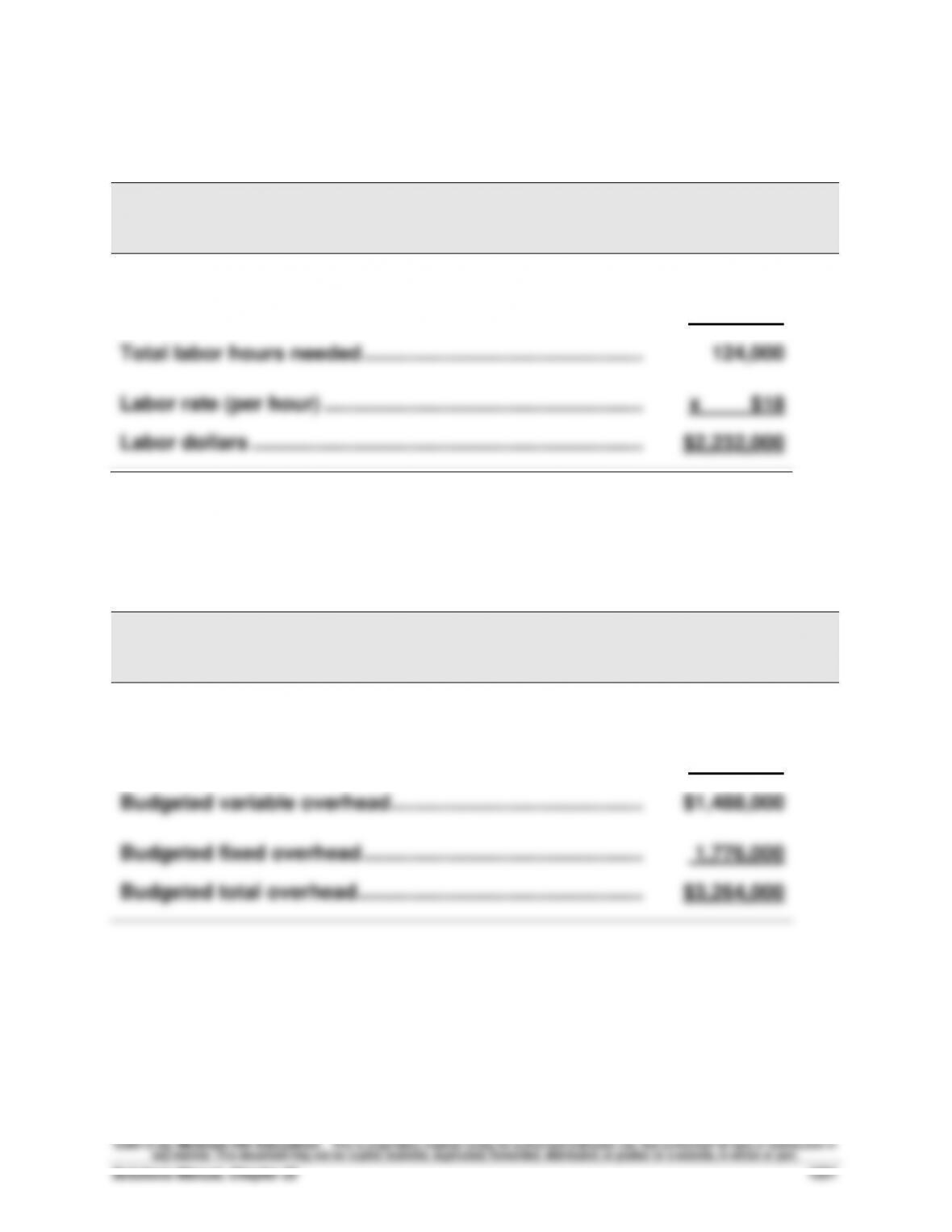

Problem 22-6B (concluded)

Part 3

NSA COMPANY

Direct Labor Budget

Second Quarter

Units to be produced ………………………………………………………

248,000

Labor requirements per unit (hours) …………………………..

x 0.50

Total labor hours needed …………………………………………..……

124,000

Labor rate (per hour) ………………………………………………………

x $18

Labor dollars ……………………………………………………….…………

$2,232,000

Part 4

NSA COMPANY

Factory Overhead Budget

Second Quarter

Total labor hours needed …………………………………………..……

124,000

Variable overhead rate per direct labor hour ……………………

x $12

Budgeted variable overhead ……………………………………………

$1,488,000

Budgeted fixed overhead …………………………………………..……

1,776,000

Budgeted total overhead …………………………………………………

$3,264,000

Fundamental Accounting Principles, 21st Edition

1332

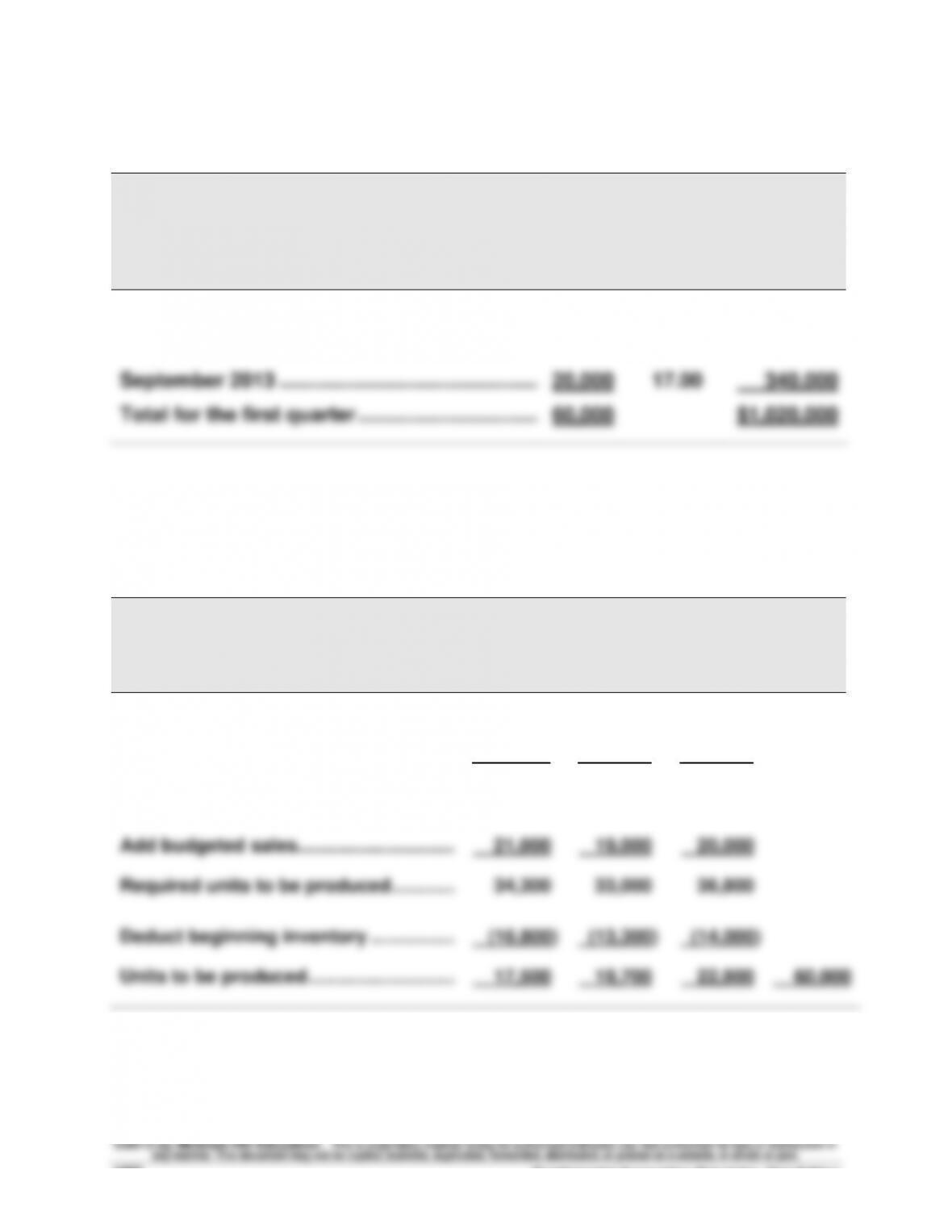

Problem 22-7B (130 minutes)

Part 1

NABAR MANUFACTURING

Sales Budgets

July, August, and September 2013

Budgeted

Units

Budgeted

Unit Price

Budgeted

Total Dollars

July 2013 …………………………………………………..….

21,000

$17.00

$ 357,000

August 2013 ………………………………………………….

19,000

17.00

323,000

September 2013 …………………………..……………….

20,000

17.00

340,000

Total for the first quarter ……………………………….

60,000

$1,020,000

Part 2

NABAR MANUFACTURING

Production Budget

July, August, and September 2013

July

August

Sept.

Total

Next month’s budgeted sales …………...

19,000

20,000

24,000

Ratio of inventory to future sales ……...

x 70%

x 70%

x 70%

Budgeted ending inventory ……………...

13,300

14,000

16,800

Add budgeted sales ………………………….

21,000

19,000

20,000

Required units to be produced ………….

34,300

33,000

36,800

Deduct beginning inventory ……………..

(16,800)

(13,300)

(14,000)

Units to be produced ………………………..

17,500

19,700

22,800

60,000

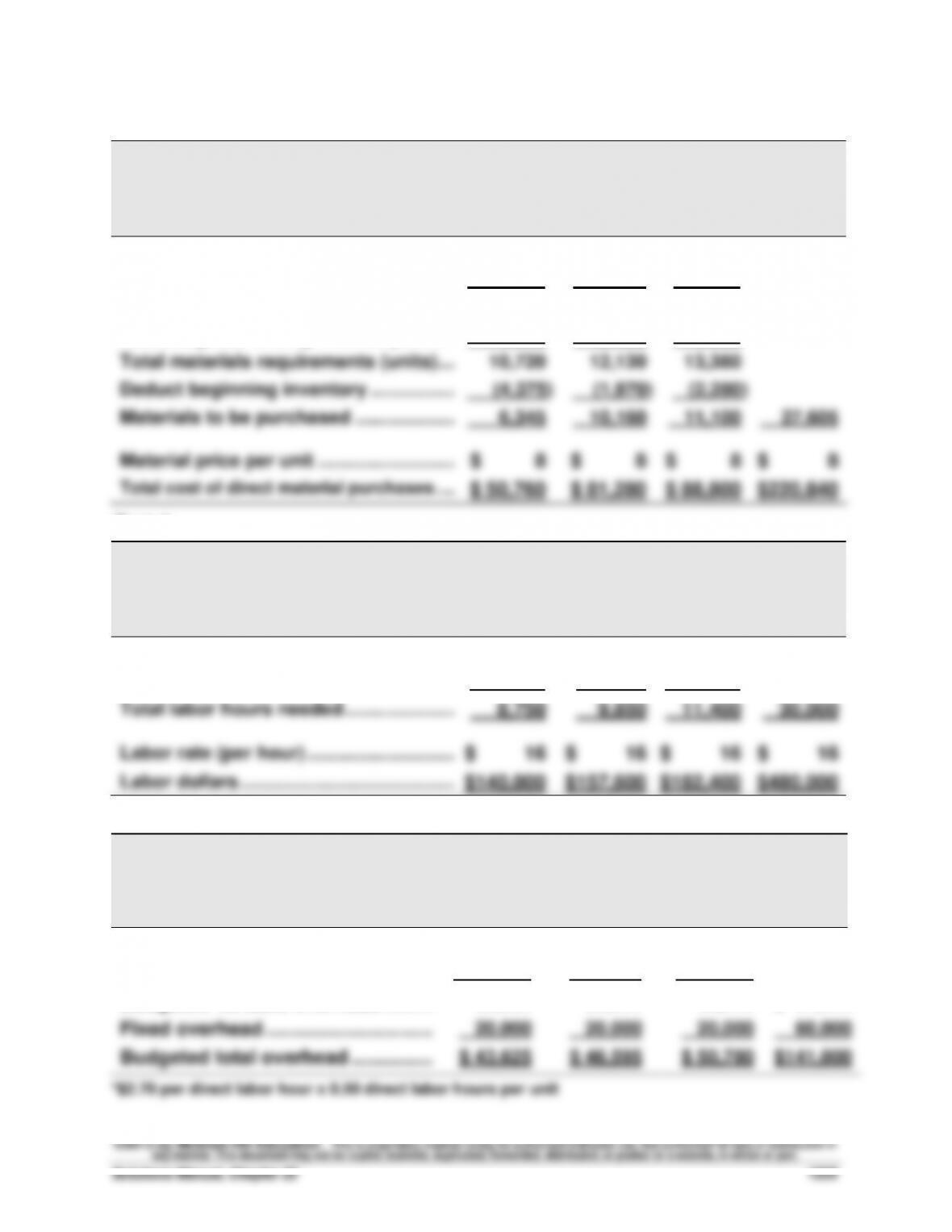

Problem 22-7B (continued)

Part 3

NABAR MANUFACTURING

Raw Materials Budget

July, August, and September 2013

July

August

Sept.

Total

Production budget (units) ………………...

17,500

19,700

22,800

Materials requirement per unit ………….

x 0.50

x 0.50

x 0.50

Materials needed for production ……….

8,750

9,850

11,400

Add budgeted ending inventory ………..

1,970

2,280

1,980

Total materials requirements (units) ….

10,720

12,130

13,380

Deduct beginning inventory ……………..

(4,375)

(1,970)

(2,280)

Materials to be purchased ………………..

6,345

10,160

11,100

27,605

Material price per unit ……………………...

$ 8

$ 8

$ 8

$ 8

Total cost of direct material purchases …..

$ 50,760

$ 81,280

$ 88,800

$220,840

Part 4

NABAR MANUFACTURING

Direct Labor Budget

July, August, and September 2013

July

August

Sept.

Total

Budgeted production (units) …………….

17,500

19,700

22,800

Labor requirements per unit (hours) ….

x 0.50

x 0.50

x 0.50

Total labor hours needed ………………….

8,750

9,850

11,400

30,000

Labor rate (per hour) ………………………..

$ 16

$ 16

$ 16

$ 16

Labor dollars …………………………………...

$140,000

$157,600

$182,400

$480,000

Part 5

NABAR MANUFACTURING

Factory Overhead Budget

July, August, and September 2013

July

August

Sept.

Total

Budgeted production (units) ……….…..

17,500

19,700

22,800

Variable factory overhead rate* …..…..

x $1.35

x $1.35

x $1.35

Budgeted variable overhead ……….…..

23,625

26,595

30,780

$ 81,000

Fixed overhead …………………………..

20,000

20,000

20,000

60,000

Budgeted total overhead …………….…..

$ 43,625

$ 46,595

$ 50,780

$141,000

*$2.70 per direct labor hour x 0.50 direct labor hours per unit