9-1

CHAPTER 9

ACCOUNTING FOR RECEIVABLES

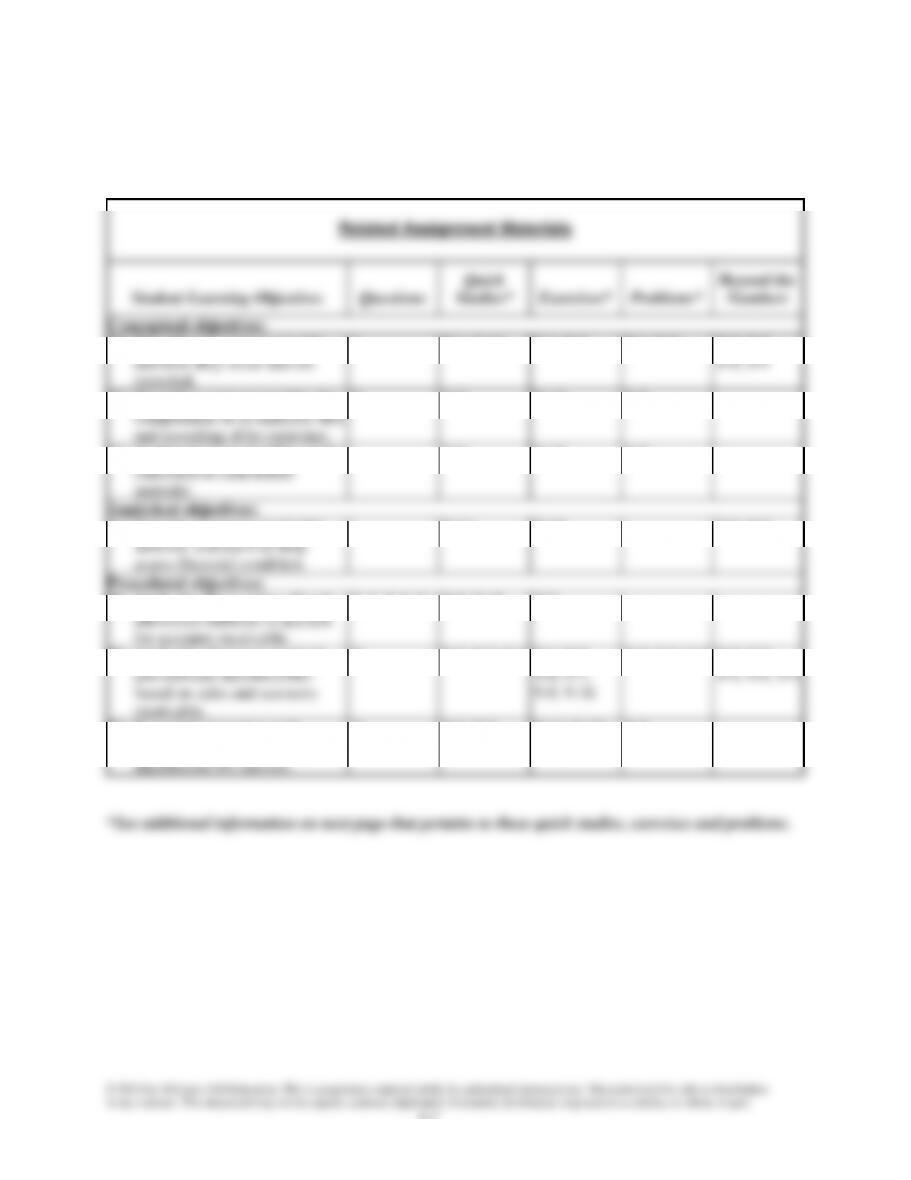

Related Assignment Materials

Student Learning Objectives

Questions

Quick

Studies*

Exercises*

Problems*

Beyond the

Numbers

Conceptual objectives:

C1. Describe accounts receivable

and how they occur and are

recorded.

1

9-1, 9-12

9-1, 9-2

9-1, 9-2

9-5, 9-7,

9-8, 9-9

C2. Describe a note receivable, the

computation of its maturity date

and recording of its existence.

9

9-5

9-13

9-5

C3. Explain how receivables can be

converted to cash before

maturity.

9-8

9-10

9-5

Analytical objectives:

A1 Compute accounts receivable

turnover and use it to help

assess financial condition.

9-11

9-15

9-1, 9-2

Procedural objectives:

P1. Apply the direct write-off and

allowance methods to account

for accounts receivable.

2, 3, 5, 6, 8

9-9, 9-10

9-3

P2. Apply the allowance method

and estimate uncollectibles

based on sales and accounts

receivable.

7

9-2, 9-3, 9-4

9-4, 9-5,

9-6, 9-7,

9-8, 9-16

9-2, 9-3, 9-4

9-2, 9-3,

9-4, 9-6, 9-9

P3. Record the honoring and

dishonoring of a note and

adjustments for interest.

4

9-6, 9-7

9-11, 9-12,

9-14

9-5

Additional Information on Related Assignment Material

The Serial Problem for Success Systems continues in this chapter. Problem 9-1A, 9-5A and the Serial

Problem can be completed with Sage 50 Software.

Connect (Available on the instructor’s course-specific website) repeats all numerical Quick Studies, all

Exercises and Problems Set A. Connect provides new numbers each time the Quick Study, Exercise or

Problem is worked. It allows instructors to monitor, promote, and assess student learning. It can be used

in practice, homework, or exam mode

commonly called bad debts. Two methods are used to account for

uncollectible accounts:

Chapter Outline

Notes

I. Accounts Receivable—Amounts due from customers for credit sales.

They occur when a customer uses credit cards issued by third parties

and when a company gives credit directly to customers.

A. Recognizing Accounts Receivable:

1. Sales on credit—Increase (debit) Accounts Receivable for the

full amount of the sale and increase (credit) Sales.

a. The General Ledger continues to keep a single (total)

accounts receivable.

b. A supplementary record, called the Accounts Receivable

(subsidiary) Ledger, maintains a separate account

receivable for each customer.

c. A Schedule of Accounts Receivable shows that the sum of

the individual accounts in the subsidiary ledger equals the

debit balance of the Accounts Receivable account in the

general ledger.

2. Credit card sales (Examples: Visa, MasterCard, American

Express).

a. Advantages: (1) eliminates the company’s need to

evaluate each customer’s credit standing (2) avoids

seller’s risk (3) seller receives cash sooner than when they

grant credit directly (4) more credit options potentially

increase sales.

b. Credit card sales (when cash is received immediately upon

deposit of sales receipt) results in debit to Cash for the

amount of sale less the credit card company charge, debit

to Credit Card Expense for this fee and credit to Sales for

full invoice amount.

c. Credit card sales ((when cash receipt is received some

time after deposit of sales receipt) results in debit to

Accounts Receivable for the amount to be collected, and a

debit to Credit Card expense for the amount of the fee and

credit to Sales for full invoice. Later, when payment is

received, debit Cash and credit Accounts Receivable.

B. Installment Sales and Receivables

Amounts owed by customers from credit sales where payment is

required in periodic amounts over an extended time period.

1. Customer is usually charged interest.

2. Should be classified as current assets even if credit period

exceeds year if the company regularly offers customers such

terms.

Chapter Outline

Notes

1. Direct Write-off Method

Records the loss from an uncollectible account receivable

when it is determined to be uncollectible.

a. To write off uncollectible and recognize loss: debit Bad

Debt Expense, credit Accounts Receivable.

b. If a written off account is later collected, this results in a

reversal of the write-off (see above) and a normal

collection of account entry.

c. This method violates the matching (expense recognition)

principle since it frequently results in expense being

charged in a period after that of the credit sale.

d. Materiality constraint states that an amount can be

ignored if its effect on the financial statements is

unimportant to users’ decisions. This constraint permits

use of direct write-off when bad debts expenses are very

small in relation to other financial statement items such as

sales and net income.

2. Allowance Method

Matches the estimated loss from uncollectibles against the

sales they helped produce.

a. At the end of each accounting period, bad debts expense is

estimated and recorded in an adjusting entry.

b. To record estimate of bad debt expense, Debit Bad Debt

Expense, credit a contra-asset account called Allowance

for Doubtful Accounts.

c. Advantages of method:

i. Satisfies the matching principle because expense is

charged in the period of the corresponding sale.

ii. Reports accounts receivable on balance sheet at the

estimated amount of cash to be collected.

d. To write-off an uncollectible: debit Allowance for

Doubtful Accounts, credit Accounts Receivable.

e. Writing off an uncollectible does not change the estimated

amount of cash to be collected (realizable value of

accounts receivable).

f. If a written off account is later recovered (collected) , this

results of a reversal of the write off (see d above) and a

normal collection of account entry.

Chapter Outline

Notes

D. Estimating Bad Debts Expense—two methods:

1. Percent of Sales Method (uses income statement relations to

estimate)—bad debts expense is computed as a percentage of

sales for the period.

a. Sales figure chosen as base is usually credit sales but it

can be total or net sales if cash sales are small.

b. The estimate is used in the adjusting entry. Note that the

resulting reported allowance account balance is rarely

equal the reported expense because the allowance account

was not likely to be zero prior to adjustment.

2. Percent of Accounts Receivable Method (uses balance sheet

relations to estimate)—desired credit balance in Allowance for

Doubtful Accounts is computed:

a. As a percentage of outstanding receivables (simplified

approach) or

b. By aging accounts receivable.

a. The amount in the adjustment is calculated by determining

the amount necessary to bring allowance account to a

credit balance equivalent to the estimated uncollectibles.

II. Notes Receivable— Promissory note that is a written promise to pay a

specified amount of money (principal) either on demand or on a

definite future date. Most notes are interest bearing. Promissory notes

are notes payable to the maker (person promising to pay) and notes

receivable to the payee (person to be paid).

A. Computations for Notes

1. Maturity date is the date the note must be repaid.

2. Amount to be repaid is principal plus interest (maturity value).

3. The period of the note is the time from the note’s date to its

maturity date.

4. Formula for computing annual interest:

Annual Time of note

Principal of x rate of x expressed in = Interest

note interest fraction of year

B. Recognizing Notes Receivable—debit Notes Receivable for

principal or face amount of note. Credit will vary; depends on

reason note is received. Note that interest is not recorded until

earned.

C. Valuing and Settling Notes

1. Recording an honored note—debit Cash for maturity value

(face and interest), credit Note Receivable for face amount and

credit Interest Revenue for the interest amount.

9-6

Chapter Outline

Notes

2. Recording a dishonored note—debit Accounts Receivable for

maturity value, credit Note Receivable for face amount and

credit Interest Revenue for the interest amount. If account

receivable remains uncollected, it will be written-off.

3. Recording End-of-Period Interest Adjustment—record

accrued interest by debiting Interest Receivable and crediting

Interest Revenue.

4. Collection entry if some interest was accrued requires a debit

to Cash for full amount received, credits to Interest Receivable

(amount previously accrued), Interest Revenue (amount

earned since accrual date) and Notes Receivable (face amount

of note).

III. Disposing of Receivables—Companies can convert receivables to

cash before they are due. Reasons for this include the need for cash or

a desire to not be involved in collection activities.

A. Selling Receivables

1. Buyer, called a factor, charges the seller a factoring fee and

then collects the receivables as they come due.

2. Entry: debit Cash (amount received), and Factoring Fee

Expense (amount charged) and credit Accounts Receivable

(amount sold).

B. Pledging Receivables

1. Company borrows money by pledging its receivables as

security.

2. Borrower retains ownership of the receivables.

3. If borrower defaults, the lender has right to be paid from

receipts on accounts receivable when collected.

4. The pledge should be disclosed in financial statement

footnotes.

5. The loan is recorded as a debit to Cash and a credit to Notes

Payable.

Chapter Outline

Notes

V. Decision Analysis—Accounts Receivable Turnover

A. Measures both the quality (likeliness of collecting) and liquidity

(speed of collection) of accounts receivable,

B. Indicates how often, on average, receivables are received and

collected during the period.

C. Calculated by dividing net sales by average accounts receivable.

IV. Decision Analysis—Accounts Receivable Turnover

D. Measures both the quality (likeliness of collecting) and liquidity

(speed of collection) of accounts receivable,

E. Indicates how often, on average, receivables are received and

collected during the period.

F. Calculated by dividing net sales by average accounts receivable.

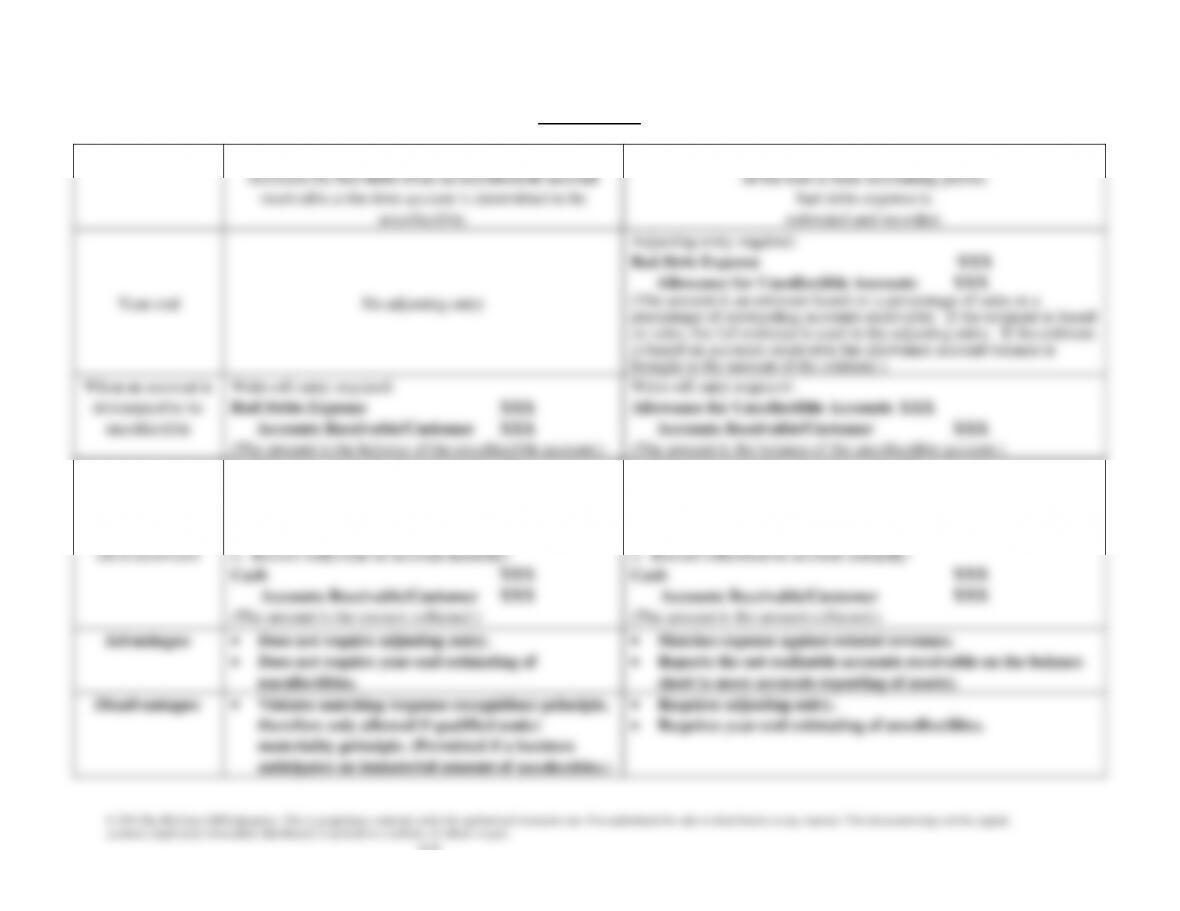

VISUAL # 9-1

METHODS OF ACCOUNTING FOR BAD DEBTS

DIRECT WRITE-OFF METHOD

Accounts for bad debts from an uncollectible account

receivable at the time account is determined to be

uncollectible.

ALLOWANCE METHOD

At the end of each accounting period,

bad debts expense is

estimated and recorded.

Year-end

No adjusting entry

Adjusting entry required:

Bad Debt Expense XXX

Allowance for Uncollectible Accounts XXX

(The amount is an estimate based on a percentage of sales or a

percentage of outstanding accounts receivable. If the estimate is based

on sales, the full estimate is used in the adjusting entry. If the estimate

is based on accounts receivable the allowance account balance is

brought to the amount of the estimate.)

When an account is

determined to be

uncollectible

Write-off entry required:

Bad Debts Expense XXX

Accounts Receivable/Customer XXX

(The amount is the balance of the uncollectible account.)

Write-off entry required:

Allowance for Uncollectible Accounts XXX

Accounts Receivable/Customer XXX

(The amount is the balance of the uncollectible account.)

When an account

previously written

off is recovered

1. Reinstate account by reversing write-off:

Accounts Receivable/Customer XXX

Bad Debts Expense XXX

(The amount is the account balance that was written off.)

2. Record collection on account normally:

Cash XXX

Accounts Receivable/Customer XXX

(The amount is the amount collected.)

1. Reinstate account by reversing write-off:

Accounts Receivable/Customer XXX

Allowance for Uncollectible Accounts XXX

(The amount is the account balance that was written off.)

2. Record collection on account normally:

Cash XXX

Accounts Receivable/Customer XXX

(The amount is the amount collected.)

Advantages:

• Does not require adjusting entry.

• Does not require year-end estimating of

uncollectibles.

• Matches expense against related revenues.

• Reports the net realizable accounts receivable on the balance

sheet (a more accurate reporting of assets).

Disadvantages:

• Violates matching (expense recognition) principle,

therefore only allowed if qualified under

materiality principle. (Permitted if a business

anticipates an immaterial amount of uncollectibles.)

• Requires adjusting entry.

• Requires year-end estimating of uncollectibles.

9-9

VISUAL #9-2

PROMISSORY NOTE

(6) $2,000.00 April 15, 2011 (1)

9-10

Alternate Demonstration Problem

Chapter Nine

At the end of the year, the M. I. Wright Company showed the following

selected account balances:

Sales (all on credit) ………………………………………………………………….$300,000

Accounts Receivable ………………………………………………………………. 800,000

Allowance for Doubtful Accounts …………………………………………….. 38,000

Required:

1. Assume the company estimates that 1% of all credit sales will not be

collected.

a. Prepare the proper journal entry to recognize the expense

involved.

b. Present the balances in Accounts Receivable and Allowance for

Doubtful Accounts as they would appear on the balance sheet.

Also show the net r ealizable Accounts Receivable.

2. Assume the company estimates that 5% of its accounts receivable

will never be collected.

a. Prepare the proper journal entry to recognize the expense

involved.

b. Present the balances in Accounts Receivable and Allowance for

Doubtful Accounts as they would appear on the balance sheet.

Also show the net realizable Accounts Receivable.

3. Under assumptions 1 and 2 above, give the proper journal entries for

the following events.

June 3 John Shifty, who owes us $500, informs us that

he is broke and cannot pay. We believe him.

Nov. 9 We learned that John Shifty has won the lottery and

is willing to pay off all his old debts.

9-11

Solution: Alternate Demonstration Problem

Chapter Nine

1a. Bad Debts Expense …………………………………… 3,000

Allowance for Doubtful Accounts ………….. 3,000

($ 300,000 X 1 %)

Estimated Realizable A/R …………………………..$759,000

2a. Bad Debts Expense …………………………………… 2,000

Allowance for Doubtful Accounts ………….. 2,000

($ 800,000 X 5 % less $38,000)

3. Both assumptions 1 and 2 above represent the allowance method of

accounting for uncollectibles. The only difference is in the approach

June 3 Allowance for Doubtful Accounts …………. 500

Accounts Receivable, John Shifty……. 500

Note: There would be a closing entry for the Bad Debts Expense

since it is an expense account just like any other expense account.