Title: Question 1

QA_Ori: Under the circumstances described, the death, bankruptcy, or legal inability of

a partner to execute a contract ends a partnership. In addition, if a partnership is

Title: Question 2

QA_Ori: Mutual agency means that each partner is an agent of the partnership and can

Title: Question 3

QA_Ori: All partners in a general partnership have unlimited liability. A limited

Title: Question 4

QA_Ori: Yes, partners can limit the right of a partner. Such an agreement is

Title: Question 5

QA_Ori: No, he does not have this right. A partnership is a voluntary association

Title: Question 6

QA_Ori: If partners agree on the method of sharing incomes, but say nothing of

Title: Question 7

Title: Question 8

QA_Ori: Unlimited liability means that the creditors of a partnership have the right to

Title: Question 9

QA_Ori: George’s claim is not valid unless the previously agreed upon method of

Title: Question 10

QA_Ori: No. Kay is still liable to her former partners for her share of the losses.

Title: Question 11

QA_Ori: At all times in the accounting history of a partnership (or any

organization), assets must equal liabilities plus equity. When the assets are converted

Title: Question 12

Title: Quick Study 12-1

QA_Ori:

a. The partnership will need to pay because it is a merchandising firm. That is, if

b. A public accounting firm is not in the merchandising business. Consequently,

Title: Quick Study 12-2

QA_Ori:

Stolton Bright Total

Net income 52,000

Salary allowances

Stolton $15,000

Title: Quick Study 12-3

QA_Ori: If Blake is allocated a $100,000 salary allowance and there remains $4,000 to

Title: Quick Study 12-4

QA_Ori: Since Carley is a limited partner, she is not personally liable for any unpaid

Title: Quick Study 12-5

QA_Ori:

Choi, Capital 10,000

Title: Quick Study 12-6

QA_Ori:

Cash 40,000

Title: Quick Study 12-7

QA_Ori:

1.

Field Brown Snow Total

Initial investments $131,250 $165,000 $153,750 $450,000

2. a)

May 31 Cash 3,750

3. a)

May 31 Brown, Capital 1,875

Snow, Capital 1,875

Title: Quick Study 12-8

QA_Ori:

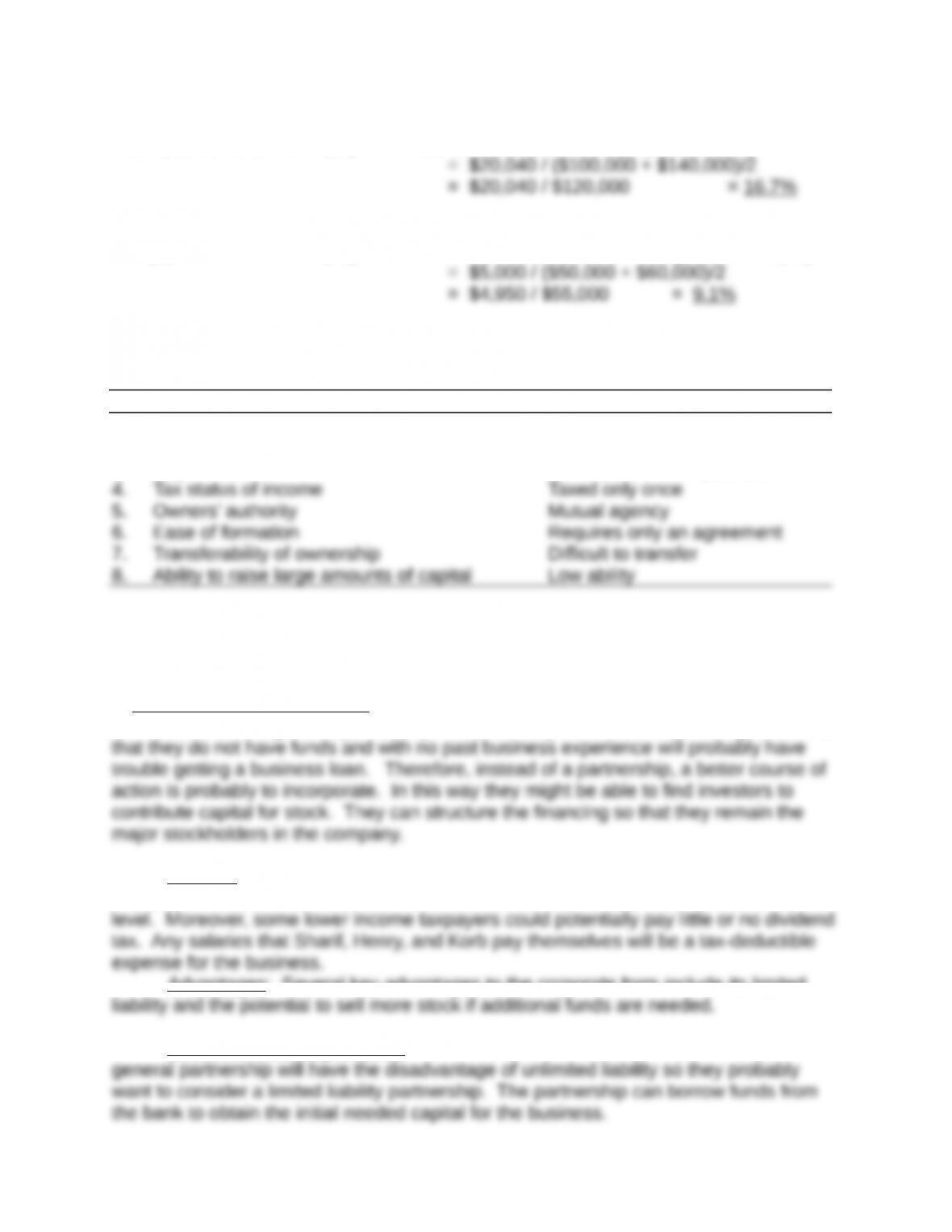

Total partnership return on equity = Net Income/Average equity

Howe partner return on equity = Partner net income/Average partner equity

Duley partner return on equity = Partner net income/Average partner equity

Title: Exercise 12-1

QA_Ori:

Characteristic General Partnerships

1. Life Limited

2. Owners’ liability Unlimited

3. Legal status Not separate from partners

Title: Exercise 12-2

QA_Ori:

a. Recommended Organization: Sharif, Henry, and Korb might first consider organizing

their business as a general partnership. However, a problem for these new graduates is

Taxation: As a corporation, any income will be subject to corporate income tax.

Any dividends paid to the stockholders will also normally be taxed, but at a much lower

Advantages: Several key advantages to the corporate form include its limited

b. Recommended Organization: The two doctors should form a partnership. A

Taxation: The owners will pay individual taxes on income earned by the partnership but

Advantages: The advantages of the partnership are ease of formation and owner

authority.

c. Recommended Organization: Munson should consider setting up a limited

Taxation: All partners will pay individual taxes on income distributed to them, but

Title: Exercise 12-3

QA_Ori:

1a. 2013

Mar. 1 Cash 82,500

Land 60,000

1b. 2013

1c. 2013

Dec. 31 Eckert, Capital 34,000

Kelley, Capital 20,000

Dec. 31 Income Summary 90,000

2.

Capital account balances

Eckert

Kelley

Initial investment

*Supporting calculations

Eckert

Kelley

Total

Net income

Total salary allowance

Total interest allowances

Eckert

Kelley

Total allocated equally

Balance of income

_______

_______

$ 0

Shares of the partners

Title: Exercise 12-4

1. QA_Ori:

Jan. 1 Cash 17,500

Equipment 82,500

2.

Jan. 1 Cash 31,250

A. Barber, Capital 31,250

To record initial capital investment of Barber.

Title: Exercise 12-5

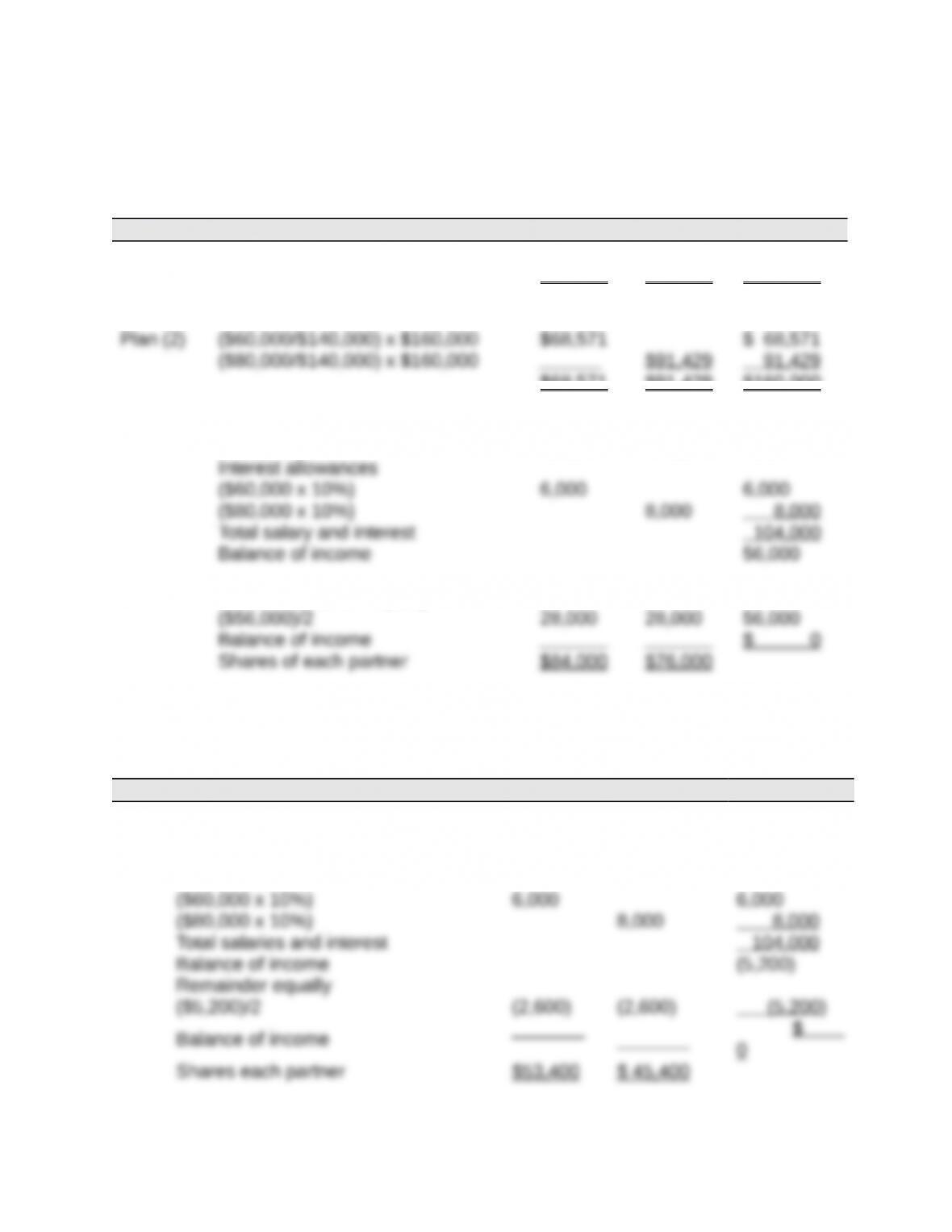

QA_Ori:

Kramer Knox Total

Plan (1) $160,000 x 1/2 $80,000 $80,000 $160,000

$68,571 $91,429 $160,000

Plan (3) Net income $160,000

Salary allowances $50,000 $40,000 90,000

Balance allocated equally

Title: Exercise 12-6

QA_Ori:

Kramer Knox Total

1. Net income $ 98,800

Salary allowances $50,000 $ 40,000 90,000

Interest allowances

2. Net income $ (16,800)

Salary allowances $50,000 $ 40,000 90,000

Interest allowances

Title: Exercise 12-7

QA_Ori:

1.

Nov. 1 Cash 90,000

Madison, Capital 90,000

2.

Nov. 1 Cash 120,000

Madison, Capital 94,500

3.

Nov. 1 Cash 80,000

Main, Capital 6,800

Supporting computations

Title: Exercise 12-8

QA_Ori:

1.

Jan. 31 Tulip, Capital 60,000

Cash 60,000

To record retirement of Tulip.

2.

3.

Jan. 31 Tulip, Capital 60,000

Hunter, Capital* 18,750

Title: Exercise 12-9

QA_Ori:

Sept. 30 Mandy, Capital 100,000

Title: Exercise 12-10

QA_Ori:

a. Loss from selling assets

* Alternative computation

b. Loss allocation

QA_Ori:

Turner Roth Lowe Total

Capital balances before loss

liquidation $ 2,500 $ 14,000 $ 31,500 $ 48,000

Allocation of loss

c. Liability to be paid

Each partner should pay the amount of the debit (deficit) balance in his or her own

capital account.