Fundamental Accounting Principles, 21st Edition

1148

Exercise 20-14 (Concluded)

(1)

Beginning goods in process

$ 17,250

Direct materials

$ ?

Direct labor

47,250

Factory overhead

51,300

Total costs added

?

Total costs in process

$242,400

$17,250 + [Total costs added] = $242,400

Therefore, Total costs added = $225,150

$225,150 = Direct materials + $47,250 + $51,300

Therefore, Direct materials = $126,600

Exercise 20-15 (30 minutes)

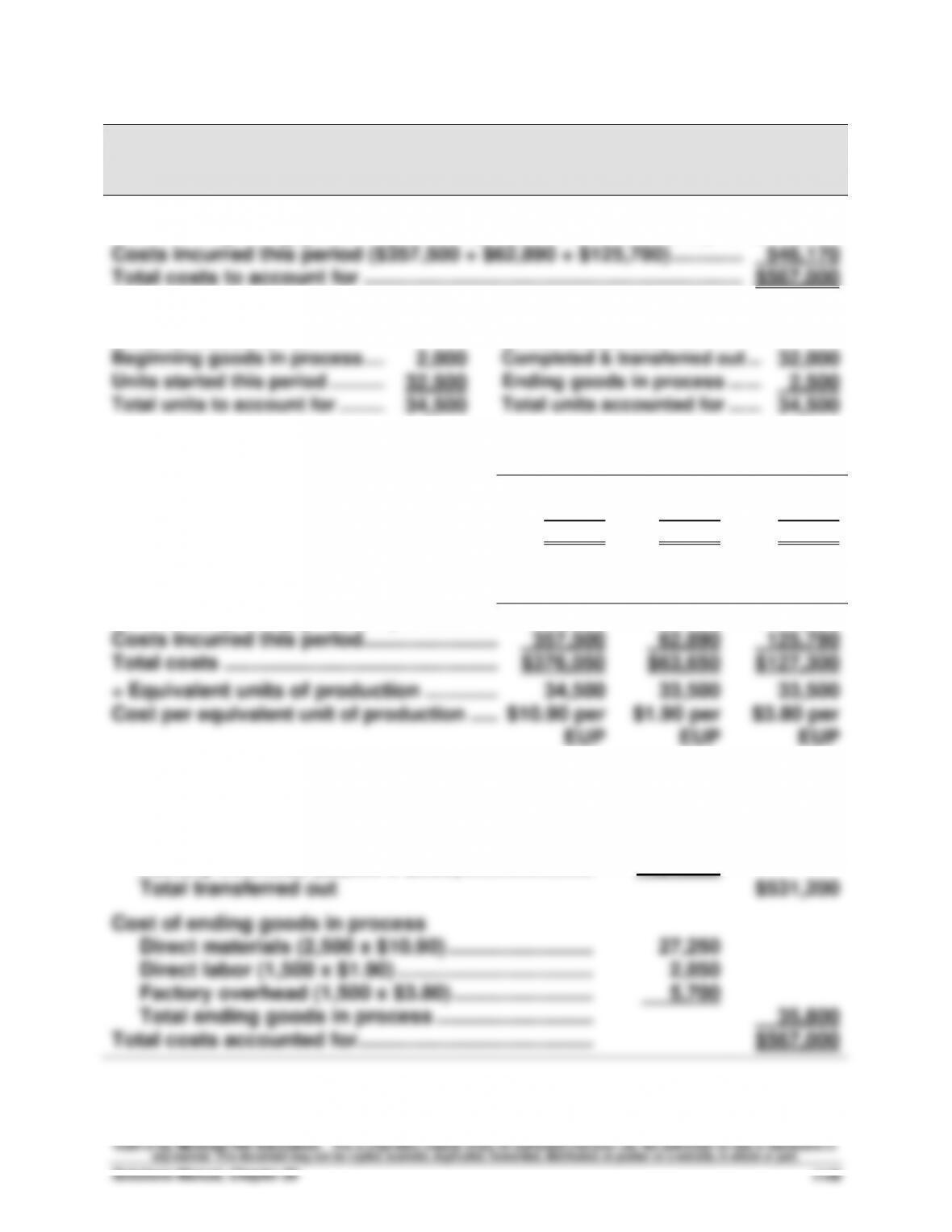

ASHAD COMPANY

Process Cost Summary – Weighted Average Method

For Month Ended July 31

Costs Charged to Production

Costs of beginning goods in process ($18,550 + $760 + $1,520) …..…….

$ 20,830

Costs incurred this period ($357,500 + $62,890 + $125,780) ………….…….

546,170

Total costs to account for …………………………………………………………..…….

$567,000

Unit Cost Information

Units to Account For

Units Accounted For

Beginning goods in process …..…………

2,000

Completed & transferred out ….……………………….

32,000

Units started this period ……………………

32,500

Ending goods in process ……..……………………

2,500

Total units to account for ……….…………

34,500

Total units accounted for ……..……………………

34,500

Equivalent Units of Production (EUP)

Direct

Materials

Direct

Labor

Factory

Overhead

Units completed and transferred out ……..

32,000

32,000

32,000

Units of ending goods in process ………....

2,500

1,500

1,500

Equivalent units of production ……………...

34,500

33,500

33,500

Cost per EUP

Direct

Materials

Direct

Labor

Factory

Overhead

Costs of beginning goods in process …....

$ 18,550

$ 760

$ 1,520

Costs incurred this period ……………………..

357,500

62,890

125,780

Total costs …………………………………………...

$376,050

$63,650

$127,300

÷ Equivalent units of production …………...

34,500

33,500

33,500

Cost per equivalent unit of production …....

$10.90 per

EUP

$1.90 per

EUP

$3.80 per

EUP

Cost Assignment and Reconciliation

Costs transferred out

Direct materials (32,000 x $10.90) …………………….…….

$348,800

Direct labor (32,000 x $1.90) …………………………….………….

60,800

Factory overhead (32,000 x $3.80) …………………………..

121,600

Total transferred out

$531,200

Cost of ending goods in process

Direct materials (2,500 x $10.90) …………………………..

27,250

Direct labor (1,500 x $1.90) ………………………………………….

2,850

Factory overhead (1,500 x $3.80) ……………………..……

5,700

Total ending goods in process ………………………..…

35,800

Total costs accounted for …………………………………….………….

$567,000

Fundamental Accounting Principles, 21st Edition

1150

Exercise 20-16 (40 minutes)

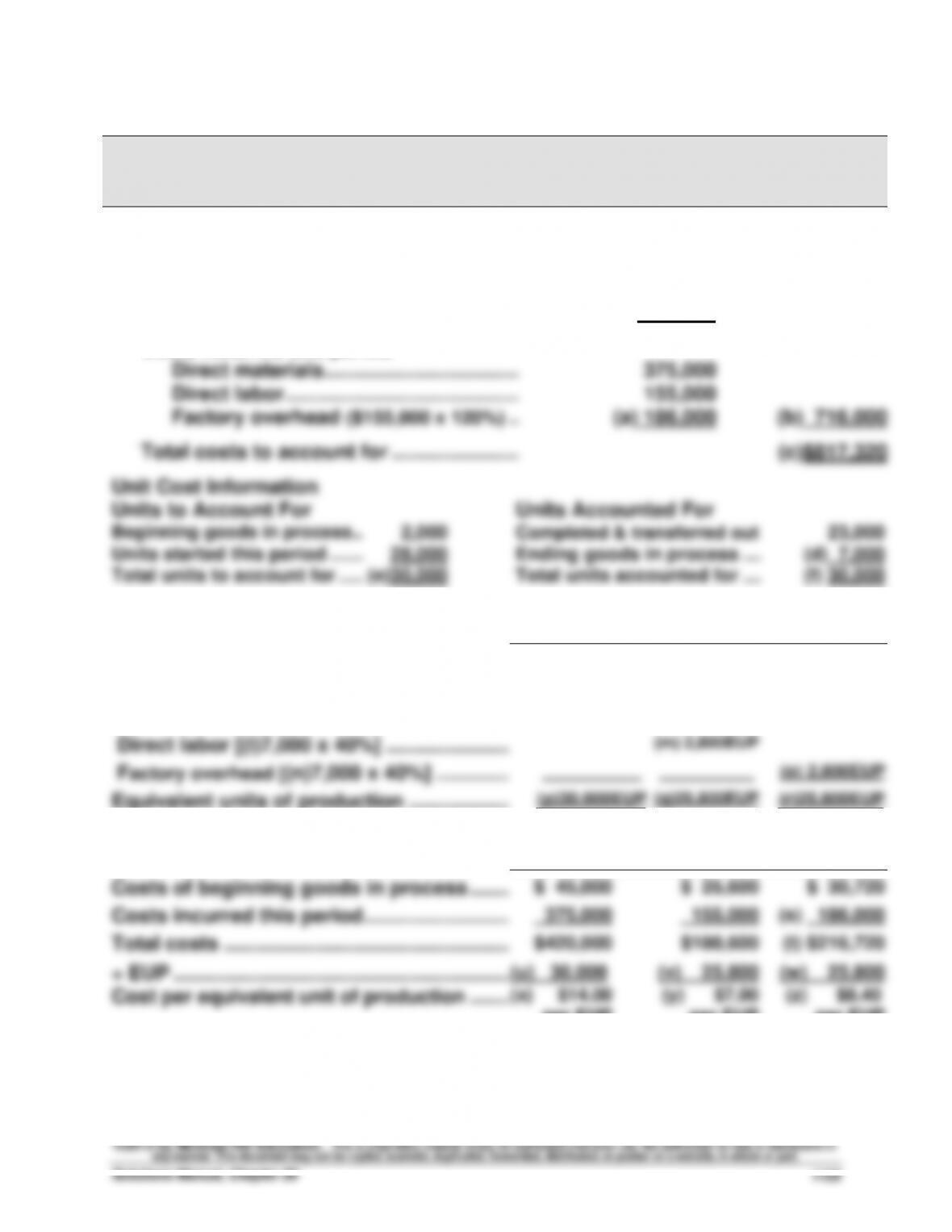

ASHAD COMPANY

Process Cost Summary – FIFO Method

For Month Ended July 31

Costs Charged to Production

Costs of beginning goods in process

Direct materials ………………………………………………….……

$ 18,550

Direct labor ………………………………………………………..…….

760

Factory overhead ……………………………………………….…….

1,520

$ 20,830

Costs incurred this period

Direct materials ………………………………………………….……

357,500

Direct labor ………………………………………………………..…….

62,890

Factory overhead ……………………………………………….…….

125,780

546,170

Total costs to account for …………………………………….…….

$567,000

Unit cost information

Units to account for

Units accounted for

Beginning goods in process …………………………..

2,000

Completed & transferred out ….…….

32,000

Units started this period ……….………………….

32,500

Ending goods in process …………….

2,500

Total units to account for ……..……………………

34,500

Total units accounted for …………….

34,500

Equivalent units of production

Direct

Materials

Direct

Labor

Factory

Overhead

Units to complete beginning goods in process

Direct materials (2,000 x 0%) ………………..……..

0 EUP

Direct labor (2,000 x 80%) …………………….…….

1,600 EUP

Factory overhead (2,000 x 80%) …………………..

1,600 EUP

Units started and completed …………………..……..

30,000 EUP

30,000 EUP

30,000 EUP

Units of ending goods in process

Direct materials …………………………………………..

2,500 EUP

Direct labor ………………………………………….……..

1,500 EUP

Factory overhead ………………………………………..

_________

_________

1,500 EUP

Equivalent units of production ……………….……..

32,500 EUP

33,100 EUP

33,100 EUP

[Continued on next page]

Exercise 20-16 (Concluded)

Cost per EUP

Direct

Materials

Direct

Labor

Factory

Overhead

Costs incurred this period ………………

$ 357,500

$ 62,890

$125,780

EUP (from prior page) …………………….

÷ 32,500

÷ 33,100

÷ 33,100

Cost per EUP …………………………………

$11.00 per

EUP

$1.90 per

EUP

$3.80 per

EUP

Cost assignment and reconciliation

Costs transferred out

Cost of beginning goods in process …………………….

$20,830

Cost to complete beginning goods in process

Direct materials (0 EUP x $11.00 per EUP) ………….

$ 0

Direct labor (1,600 EUP x $1.90 per EUP) ……………

3,040

Factory overhead (1,600 EUP x $3.80 per EUP) …..

6,080

9,120

Costs of units started and completed this period

Direct materials (30,000 EUP x $11.00 per EUP) ….

330,000

Direct labor (30,000 EUP x $1.90 per EUP) ………….

57,000

Factory overhead (30,000 EUP x $3.80 per EUP) …

114,000

501,000

Total cost of goods finished this period ………………

530,950

Costs of ending goods in process

Direct materials (2,500 EUP x $11.00 per EUP) ……

27,500

Direct labor (1,500 EUP x $1.90 per EUP) ……………

2,850

Factory overhead (1,500 EUP x $3.80 per EUP) …..

5,700

36,050

Total costs accounted for …………………………………….

$567,000

Fundamental Accounting Principles, 21st Edition

1152

Exercise 20-17 (10 minutes)

1. Process operation. 7. Job order operation.

Note: Reasonable arguments can be made to classify #7 and #11 as being made

in a process operation, and #8 in a job order operation, in some cases.

Exercise 20-18 (10 minutes)

Exercise 20-19 (10 minutes)

A hybrid costing system contains features of both process costing and job

Exercise 20-20 (20 minutes)

1. Beginning inventory is 100% complete with respect to materials.

Ending inventory is 100% complete with respect to materials.

EUP for Materials

Goods completed (191,500 EUP x 100%) …………………………….

191,500

Ending goods in process* (29,500 EUP x 100%) …………………..

29,500

Total EUP …………………………..………………………………………………

221,000

2. Beginning inventory is 50% complete with respect to materials.

Ending inventory is 50% complete with respect to materials.

Units of

EUP for Materials

Product

Goods completed (191,500 EUP x 100%) …………………………….

191,500

Ending goods in process (29,500* EUP x 50%) …………………….

14,750

Total EUP …………………………..………………………………………………

206,250

*Ending goods in process = Beginning goods in process + Goods started – Goods completed.

= 31,500 + 189,500 – 191,500

= 29,500

Fundamental Accounting Principles, 21st Edition

1154

Exercise 20-21 (20 minutes)

1. Beginning inventory is 100% complete with respect to materials.

Ending inventory is 100% complete with respect to materials.

EUP for Materials

To complete beginning work in process (31,500 EUP x 0%) …..….

0

Units started and completed* (160,000 EUP x 100%) ……………..….

160,000

Ending goods in process** (29,500 EUP x 100%) ……………………….

29,500

Total EUP …………………………..………………………………………………..….

189,500

2. Beginning inventory is 50% complete with respect to materials.

Ending inventory is 50% complete with respect to materials.

Units of

EUP for Materials

Product

To complete beginning work in process (31,500 EUP x 50%) …….

15,750

Units started and completed* (160,000 EUP x 100%) ……………..….

160,000

Ending goods in process** (29,500 EUP x 50%) ……………………..….

14,750

Total EUP …………………………..………………………………………………..….

190,500

*Units started and completed = Units completed – Beginning goods in process

= 191,500 – 31,500

= 160,000

** Ending goods in process = Beginning goods in process + Goods started – Goods completed

= 31,500 + 189,500 – 191,500

= 29,500

Exercise 20-22 (30 minutes)

HI-TEST COMPANY

Process Cost Summary (Weighted-Average Method)

For Month Ended September 30

Costs Charged to Production

Costs of beginning work in process

Direct materials ……………………………..………………………..

$ 45,000

Direct labor ……………………………………………………….

25,600

Factory overhead …………………………..

30,720

$101,320

Costs incurred this period

Direct materials ……………………………..………………………..

375,000

Direct labor ……………………………………………………….

155,000

Factory overhead ($155,000 x 120%) ..…………………………

(a) 186,000

(b) 716,000

Total costs to account for …………………..………

(c)$817,320

Unit Cost Information

Units to Account For

Units Accounted For

Beginning goods in process ………………

2,000

Completed & transferred out .………………………….

23,000

Units started this period …….……………..

28,000

Ending goods in process …..………………………

(d) 7,000

Total units to account for …..……………..

(e)30,000

Total units accounted for …..………………………

(f) 30,000

Equivalent Units of Production (EUP)

Direct

Materials

Direct

Labor

Factory

Overhead

Units completed and transferred out ……………..

(g)23,000EUP

(h)23,000EUP

(i)23,000EUP

Units of ending goods in process …………..……..

Direct materials [(j)7,000 x 100%] …………..……..

(k) 7,000EUP

Direct labor [(l)7,000 x 40%] …………………..……..

(m) 2,800EUP

Factory overhead [(n)7,000 x 40%] …………..……..

.

.

(o) 2,800EUP

Equivalent units of production ……………….…………

(p)30,000EUP

(q)25,800EUP

(r)25,800EUP

Cost per EUP

Direct

Materials

Direct

Labor

Factory

Overhead

Costs of beginning goods in process …….

$ 45,000

$ 25,600

$ 30,720

Costs incurred this period ……………………..

375,000

155,000

(s) 186,000

Total costs ……………………………………………

$420,000

$180,600

(t) $216,720

÷ EUP ……………………………………………………

(u) 30,000

(v) 25,800

(w) 25,800

Cost per equivalent unit of production …….

(x) $14.00

per EUP

(y) $7.00

per EUP

(z) $8.40

per EUP

[Continued on next page]

Fundamental Accounting Principles, 21st Edition

1156

Exercise 20-22 (concluded)

Cost Assignment and Reconciliation

Costs transferred out

Direct materials [(aa)$14.00 x (bb)23,000] ……………….….

(cc)$322,000

Direct labor [(dd)$ 7.00 x (ee)23,000] ………………………….

(ff) 161,000

Factory overhead [(gg)$ 8.40 x (hh)23,000] ……………..….

(ii) 193,200

Total transferred out ……………………………………………….

(jj) $676,200

Cost of ending goods in process

Direct materials [(kk)$14.00 x (ll)7,000] ……………………….

(mm) 98,000

Direct labor [(nn)$ 7.00 x (oo)2,800] ………………………..…

(pp) 19,600

Factory overhead [(qq)$ 8.40 x (rr)2,800]…………………….

(ss) 23,520

Total ending goods in process ……………………………….….

(tt) 141,120

Total costs accounted for …………………………………..…..

(uu)$817,320

PROBLEM SET A

Problem 20-1A (45 minutes)

Part 1: Cost of goods transferred and cost of goods sold

Beginning goods in process inventory …………………….…….

$ 435,000

Direct materials used in production …………………………..

157,500

Direct labor used in production ……………………………….……..

780,000

Overhead applied (115% of direct labor cost) …………………..

897,000

Total production costs …………………………………………..……..

2,269,500

Less ending goods in process inventory ………………..……..

(515,000)

Transferred to finished goods inventory (a) ……………..……..

$1,754,500

Beginning finished goods inventory ……………………….….

$ 633,000

Plus goods transferred from production ………………….……..

1,754,500

Goods available for sale ………………………………………………..

2,387,500

Less ending finished goods inventory ……………………..……

(605,000)

Cost of goods sold (b) …………………………………………….……..

$1,782,500

Part 2: Summary journal entries

a.

May 31

Raw Materials Inventory …………………………….………….

250,000

Accounts Payable ………………………………..………….

250,000

Purchased raw materials.

b.

May 31

Goods in Process Inventory ……………………….….

157,500

Raw Materials Inventory ………………………..…

157,500

Used direct materials.

c.

May 31

Factory Overhead ……………………………………..………….

60,000

Raw Materials Inventory ……………………….….

60,000

Used indirect materials.

Problem 20-1A (Continued)

d.

May 31

Factory Payroll ………………………………………….………….

1,530,000

Cash ……………………………………………………….

1,530,000

Incurred payroll cost.

e.

May 31

Goods in Process Inventory ……………………….….

780,000

Factory Payroll …………………………………….………….

780,000

Used direct labor.

f.

May 31

Factory Overhead ……………………………………..………….

750,000

Factory Payroll …………………………………….………….

750,000

Used indirect labor.

g.

May 31

Factory Overhead ……………………………………..………….

87,000

Other Accounts ……………………………………………….

87,000

Incurred other overhead costs.

h.

May 31

Goods in Process Inventory ……………………….….

897,000

Factory Overhead …………………………………………….

897,000

Applied overhead at 115% of direct labor cost.

i.

May 31

Finished Goods Inventory …………………………..

1,754,500

Goods in Process Inventory ………………….……….

1,754,50

0

Transferred completed products from

production to finished goods inventory.

j.

May 31

Accounts Receivable …………………………………………….

2,500,000

Sales ……………………………………………………….

2,500,00

0

Sold finished goods.

May 31

Cost of Goods Sold …………………………………..………….

1,782,500

Finished Goods Inventory …………………………..

1,782,50

0

To record cost of goods sold for May.

Problem 20-2A (50 minutes)

Part 1

(a) and (b) Equivalent units with respect to direct materials and direct labor

Direct

Direct

Equivalent units of production (EUP)

Materials

Labor

Units completed and transferred out ……………….

700,000

700,000

Units of ending goods in process ……………………

Direct materials (180,000 x 100%) ………………

180,000

Direct labor (180,000 x 30%) ………………………

_______

54,000

Total equivalent units of production ………………..

880,000

754,000

Part 2

Cost per equivalent unit of production

Direct

Materials

Direct

Labor

Costs of beginning goods in process …………….………

$ 420,000

$ 139,000

Costs incurred this period ……………………………..………

2,220,000

3,254,000

Total costs …………………………..………………………..…

$2,640,000

$3,393,000

÷ Equivalent units of production …………………….…….

880,000 EUP

754,000 EUP

Cost per equivalent unit of production ……………………

$3.00 per EUP

$4.50 per EUP

Part 3 Assigning product costs to units

Costs transferred out

Direct materials (700,000 EUP x $3.00 per EUP) …….

$2,100,000

Direct labor (700,000 EUP x $4.50 per EUP) ……….….

3,150,000

Total costs transferred out ……………………………….….

$5,250,000

Costs of ending goods in process

Direct materials (180,000 EUP x $3.00 per EUP) …….

540,000

Direct labor (54,000 EUP x $4.50 per EUP) …………….

243,000

Total costs of ending goods in process …………….….

783,000

Total costs accounted for* ………………………………….….

$6,033,000

*This equals the sum of the total direct materials cost and the

total direct labor costs ($2,640,000 + $3,393,000 = $6,033,000).

Fundamental Accounting Principles, 21st Edition

1160

Problem 20-2A (Concluded)

Part 4

MEMORANDUM

TO:

FROM:

DATE:

RE: Percentage of Completion Error Analysis

If the units in ending inventory are 60% complete instead of 30% with

respect to labor, the number of equivalent units in ending inventory with

Regarding financial statements, this error causes an overstatement of cost

of goods sold and an understatement of net income on the income

Problem 20-3A (60 minutes)

Part 1

a.

Mar. 31

Raw Materials Inventory ……………………………..………….

250,000

Accounts Payable …………………………………………….

250,000

Raw materials purchased.

b.

Mar. 31

Goods in Process Inventory ……………………….….

168,000

Raw Materials Inventory ………………………..…

168,000

Direct materials used in production.

c.

Mar. 31

Factory Overhead ………………………………………………….

70,000

Raw Materials Inventory ………………………..…

70,000

Indirect materials used.

d.

Mar. 31

Factory Payroll …………………………………………..………….

244,850

Cash …………………………………………………….…

244,850

Factory payroll costs.

e.

Mar. 31

Goods in Process Inventory ……………………….….

199,850

Factory Payroll ……………………………………..………….

199,850

Direct labor used in production.

f.

Mar. 31

Factory Overhead ………………………………………………….

45,000

Factory Payroll ……………………………………..………….

45,000

Indirect labor used.

g.

Mar. 31

Factory Overhead ………………………………………………….

164,790

Other Accounts …………………………………….………….

164,790

Other overhead costs.

h.

Mar. 31

Goods in Process Inventory ……………………….….

279,790

Factory Overhead …………………………………………….

279,790

Application of overhead at 140%

of direct labor cost.

Problem 20-3A (Continued)

i.

Mar. 31

Finished Goods Inventory …………………………..

572,390

Goods in Process Inventory ………………….……….

572,390

Transfer goods to finished goods.

j.

Mar. 31

Cash ………………………………………………………….………….

1,200,000

Sales …………………………………………………….…

1,200,000

Sales of finished goods. (10,000 x $120)

Mar. 31

Cost of Goods Sold ……………………………………………….

592,390

Finished Goods …………………………………….………….

592,390

Cost of goods sold.

Part 2

ELLIOTT COMPANY

Process Cost Summary – Weighted Average Method

For Month Ended March 31

Costs Charged to Production

Costs of beginning goods in process

Direct materials ………………………………………………………..

$ 2,500

Direct labor ………………………………………………………………

2,650

Factory overhead ……………………………………………………..

3,710

$ 8,860

Costs incurred this period

Direct materials ………………………………………………………..

168,000

Direct labor ………………………………………………………………

199,850

Factory overhead ……………………………………………………..

279,790

647,640

Total costs to account for …………………………………………..

$656,500

Unit cost information

Units to account for

Units accounted for

Beginning goods in process …………………………..

2,000

Completed & transferred out ………….

17,000

Units started this period ………….……………….

20,000

Ending goods in process …………….

5,000

Total units to account for ………..…………………

22,000

Total units accounted for …………….

22,000

[Continued on next page]