Chapter 9

Accounting for Receivables

QUESTIONS

1. When customers use credit cards, the selling companies can avoid having to directly

evaluate the credit standing of their customers. They also avoid the risk of bad debts and

2. Revenues and expenses usually are not matched under the direct write-off method because

3. The accounting constraint of materiality suggests that the requirements of accounting

4. Creditors prefer notes receivable to accounts receivable because the notes can be more

5. Writing off a bad debt against the Allowance account does not reduce the estimated

realizable value of a company’s accounts receivable because the write-off reduces the

6. The adjusted balances of Bad Debts Expense and Allowance for Doubtful Accounts are

virtually never equal because the expense amount reflects only the events of the current

7. Polaris lists its accounts receivable as “Trade receivables, net” on its balance sheet. Polaris

8. Artic Cat uses the allowance method to account for doubtful accounts as evidenced by the

9. KTM’s lists its accounts receivable as “Accounts receivable— trade to third parties”,

10. Piaggio titles its accounts receivable as “Trade receivables.” Piaggio reports its accounts

QUICK STUDIES

Quick Study 9-1 (15 minutes)

1.

Cash …………………………………………………………………….

19,000

Credit Card Expense* …………………………………………...

1,000

Sales ……………………………………………………………….

20,000

To record credit card sales less fees.

*$20,000 x 5%

Cost of Goods Sold ……………………………………………...

15,000

Merchandise Inventory …………………………………….

15,000

To record cost of sales.

2.

Accounts Receivable—Credit Card Cos. ………………..

4,800

Credit Card Expense* …………………………………………...

200

Sales ……………………………………………………………….

5,000

To record credit card sales less fees.

*$5,000 x 4%

Cost of Goods Sold ……………………………………………...

3,000

Merchandise Inventory …………………………………….

3,000

To record cost of sales.

5 days later

Cash …………………………………………………………………….

4,800

Accounts Receivable—Credit Card Cos. …………..

4,800

To record cash receipts.

Quick Study 9-2 (15 minutes)

1.

Jan. 31

Allowance for Doubtful Accounts ……………………...

800

Accounts Receivable—C. Green …………………..

800

To write off account.

2.

Mar. 9

Accounts Receivable—C. Green* ……………………....

300

Allowance for Doubtful Accounts ………………...

300

To reinstate a written off account.

*If there is a strong belief that the remaining $500 will be

collected soon, then the full $800 balance can be reinstated.

9

Cash ………………………………………………………………...

300

Accounts Receivable—C. Green …………………..

300

To record payment on a receivable.

Quick Study 9-3 (15 minutes)

1.

Dec. 31

Bad Debts Expense …………………………………………

885

Allowance for Doubtful Accounts…………….…

885

To record estimate of uncollectibles.

Desired balance in allowance = $99,000 x 1.5%= $1,485 cr.

Adjustment required = $1,485 – $600 cr. = $885

2.

Desired balance in allowance = $1,485 (part 1)

Adjustment required = $1,485 cr. + $300 dr. = $1,785

Quick Study 9-4 (15 minutes)

Dec. 31

Bad Debts Expense …………………………………………

1,400

Allowance for Doubtful Accounts…………….…

1,400

To record estimate of uncollectibles

($280,000 x 0.5%).

Quick Study 9-5 (15 minutes)

1. Maturity date is October 31, which is computed as follows:

Days in August ………………………………………………………. 31

Minus the date of the note ………………………………………. 2

2.

Aug. 2 Notes Receivable—R. Albany …………………….. 6,000

Quick Study 9-6 (10 minutes)

Oct. 31 Cash ………………………………………………………….. 6,180

Notes Receivable—R. Albany ……………….. 6,000

Quick Study 9-7 (15 minutes)

Dec. 31 Interest Receivable …………………………………….. 50

Maturity date

Jan. 15 Cash ………………………………………………………….. 10,075

Interest Receivable ………………………………. 50

Quick Study 9-8 (10 minutes)

May 1

Cash ……………………………………………………………..

121,875

Factoring Fee Expense* ………………………………...

3,125

Accounts Receivable ………………………………..

125,000

To record sale of receivable.

*($125,000 x 0.025)

Quick Study 9-9 (10 minutes)

Oct. 1

Bad Debts Expense ………………………………………….….

50,000

Accounts Receivable—P. Moore …………………….

50,000

To write off an account.

Quick Study 9-10 (10 minutes)

Oct. 30

Accounts Receivable—P.Moore ……………………….….

50,000

Bad Debts Expense …………………………………….….

50,000

To reinstate an account previously written off.

Oct. 30

Cash ………………………………………………………………..….

50,000

Accounts Receivable— P. Moore ………………..….

50,000

To record cash received on account.

Quick Study 9-11 (10 minutes)

Accounts receivable turnover =

Interpretation: An accounts receivable turnover of 5.9 implies that the

company’s average accounts receivable balance is converted into cash

Quick Study 9-12 (10 minutes)

a. Both U.S. GAAP and IFRS have similar asset criteria that apply to

recognition of receivables. Further, receivables that arise from revenue–

generating activities are subject to broadly similar criteria for U.S. GAAP

b. Both U.S. GAAP and IFRS require receivables to be reported net of

estimated uncollectibles. Further, both systems require that the expense

Net sales

Average accounts receivable

EXERCISES

Exercise 9-1 (25 minutes)

Part 1

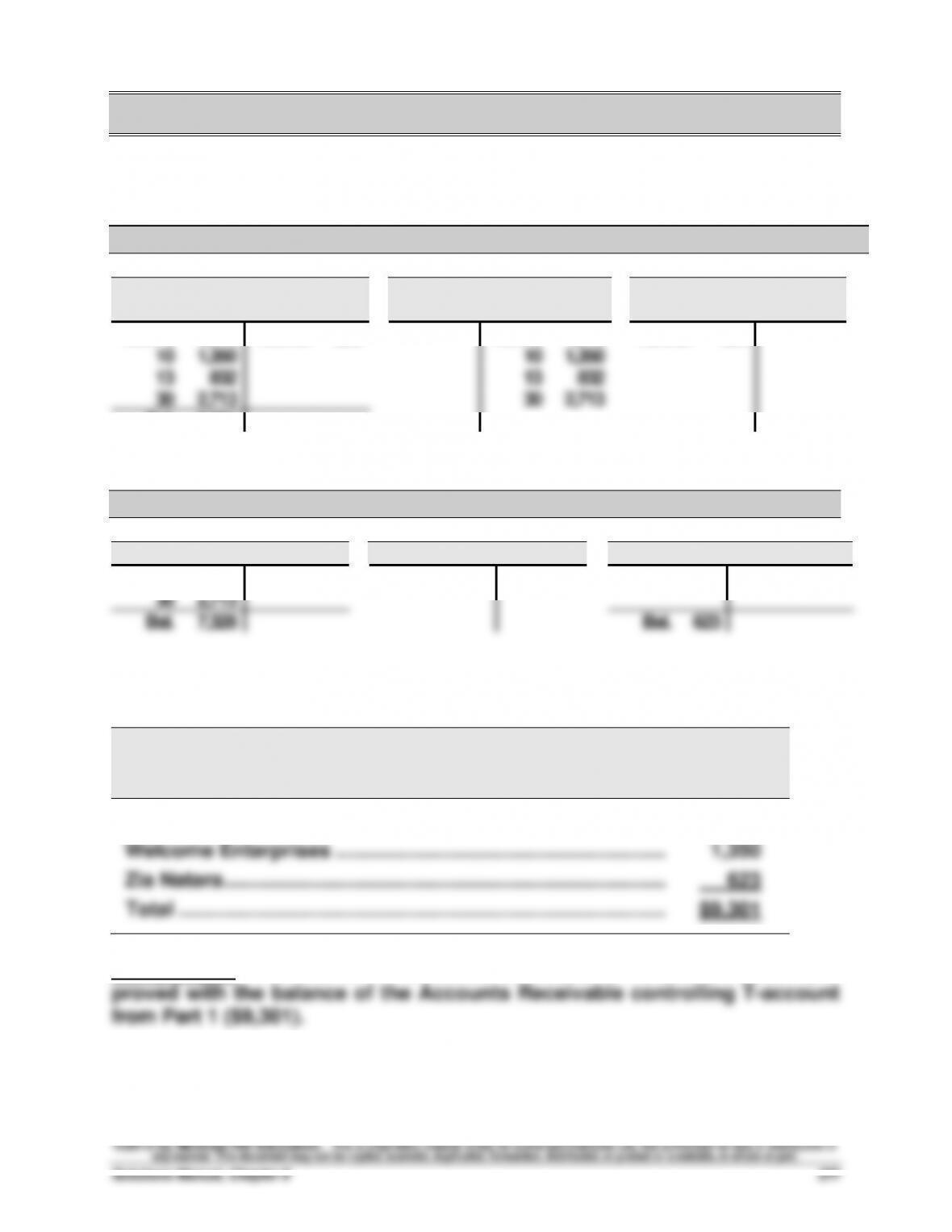

GENERAL LEDGER

Accounts Receivable

Sales

Sales Returns and

Allowances

Nov. 5

4,615

Nov. 21

209

Nov. 5

4,615

Nov. 21

209

10

1,350

10

1,350

13

832

13

832

30

2,713

30

2,713

Bal.

9,301

ACCOUNTS RECEIVABLE LEDGER

Ski Shop

Welcome Enterprises

Zia Natara

Nov. 5

4,615

Nov. 10

1,350

Nov. 13

832

Nov. 21

209

30

2,713

Bal.

7,328

Bal.

623

Part 2

Morales Company

Schedule of Accounts Receivable

November 30, 2013

Ski Shop ………………………………………………………………………

$7,328

Welcome Enterprises …………………………………………………..

1,350

Zia Natara …………………………………………………………………….

623

Total …………………………………………………………………………….

$9,301

Comparison: The total of the Schedule of Accounts Receivable ($9,301) is

Exercise 9-2 (20 minutes)

Apr. 8

Cash ……………………………………………………………….

8,064

Credit Card Expense* ………………………………………

336

Sales …………………………………………………………

8,400

To record credit card sales less 4% fee.

*($8,400 x .04)

8

Cost of Goods Sold …………………………………………

6,000

Merchandise Inventory ………………………………

6,000

To record cost of sales.

12

Accounts Receivable—Continental ………………….

5,460

Credit Card Expense* ………………………………………

140

Sales …………………………………………………………

5,600

To record credit card sales less 2.5% fee.

*($5,600 x .025)

12

Cost of Goods Sold …………………………………………

3,500

Merchandise Inventory ………………………………

3,500

To record cost of sales.

20

Cash ……………………………………………………………….

5,460

Accounts Receivable—Continental ……………..

5,460

To record cash received on credit sales less fees.

Exercise 9-3 (20 minutes)

March 11

Bad Debts Expense ……………………………………….……

45,000

Accounts Receivable—Lester Co. …………….……

45,000

To write off an account.

March 29

Accounts Receivable—Lester Co. ………………….……

45,000

Bad Debts Expense ………………………………….……

45,000

To reinstate an account previously written off.

March 29

Cash ……………………………………………………………..……

45,000

Accounts Receivable—Lester Co. …………….……

45,000

To record cash received on account.

Exercise 9-4 (20 minutes)

Dec. 31

Bad Debts Expense ………………………………………….….

4,875

Allowance for Doubtful Accounts………………..….

4,875

To record estimated bad debts expense

(.005 x $975,000).

Feb. 1

Allowance for Doubtful Accounts ……………………..….

580

Accounts Receivable—P. Park ……………………….

580

To write off an account.

June 5

Accounts Receivable—P. Park …………………………..

580

Allowance for Doubtful Accounts ………………..….

580

To reinstate an account.

June 5

Cash ………………………………………………………………..….

580

Accounts Receivable—P. Park ……………………….

580

To record cash received on account.

Exercise 9-5 (15 minutes)

a.

Dec. 31

Bad Debts Expense* …………………………..…………….…..

685

Allowance for Doubtful Accounts……………….…..

685

To record estimated bad debts expense.

*Unadjusted balance

= $ 415 credit

Estimated balance ($55,000 x .02)

= 1,100 credit

Required adjustment

= $ 685 credit

b.

Dec. 31

Bad Debts Expense** ………………………………………..…..

1,391

Allowance for Doubtful Accounts……………….…..

1,391

To record estimated bad debts expense.

** Unadjusted balance

= $ 291 debit

Estimated balance ($55,000 x .02)

= 1,100 credit

Required adjustment

= $1,391 credit

Exercise 9-6 (30 minutes)

a. Computation of the estimated balance of the allowance for uncollectibles:

Not due:

$396,000 x 0.01 =

$ 3,960

1 to 30:

90,000 x 0.02 =

1,800

31 to 60:

36,000 x 0.05 =

1,800

61 to 90:

18,000 x 0.07 =

1,260

Over 90:

30,000 x 0.10 =

3,000

$11,820

credit

Exercise 9-6 (Concluded)

b.

Dec. 31

Bad Debts Expense ……………………………………....

8,220

Allowance for Doubtful Accounts …………....

8,220

To record estimated bad debts.*

* Unadjusted balance …………………………..

$ 3,600 credit

Estimated balance …………………………………

11,820 credit

Required adjustment ………………………..…

$ 8,220 credit

c.

Dec. 31

Bad Debts Expense ……………………………………....

11,920

Allowance for Doubtful Accounts …………....

11,920

To record estimated bad debts.*

* Unadjusted balance …………………………..

$ 100 debit

Estimated balance …………………………………

11,820 credit

Required adjustment ………………………..…

$11,920 credit

Exercise 9-7 (25 minutes)

a. Computation of the estimated balance of the allowance for uncollectibles:

Dec. 31

Bad Debts Expense ……………………………………....

13,650

Allowance for Doubtful Accounts …………....

13,650

To record estimated bad debts.*

* Unadjusted balance ………………………

$12,000 credit

Dec. 31

Bad Debts Expense ……………………………………....

26,650

Allowance for Doubtful Accounts …………....

26,650

To record estimated bad debts.*

* Unadjusted balance ………………………

Exercise 9-8 (20 minutes)

Feb. 1

Allowance for Doubtful Accounts ……………………..….

6,800

Accounts Receivable—Oakley Co ……………….….

900

Accounts Receivable—Brookes Co …………….….

5,900

To write off specific accounts.

June 5

Accounts Receivable—Oakley …………………………..

900

Allowance for Doubtful Accounts ………………..….

900

To reinstate an account.

June 5

Cash ………………………………………………………………..….

900

Accounts Receivable—Oakley …………………….….

900

To record cash received on account.

Exercise 9-9 (25 minutes)

a. Expense is 1.5% of credit sales

Dec. 31

Bad Debts Expense ………………………………………..

4,500

Allowance for Doubtful Accounts ……………..

4,500

To record estimated bad debts

[$300,000 x .015].

b. Expense is 0.5% of total sales

Dec. 31

Bad Debts Expense ………………………………………..

6,000

Allowance for Doubtful Accounts ……………..

6,000

To record estimated bad debts

[($300,000 + $900,000) x .005].

c. Allowance is 6% of accounts receivable

Dec. 31

Bad Debts Expense ………………………………………..

12,500

Allowance for Doubtful Accounts ……………..

12,500

To record estimated bad debts.*

* Unadjusted balance ………………………………………………..

$ 5,000 debit.

Estimated balance ($125,000 x 6%) ………….……………..

7,500 credit

Required adjustment ……………………………….……………..

$12,500 credit

Exercise 9-10 (20 minutes)

July 4

Accounts Receivable ……………………………………..

7,245

Sales ……………………………………………………….

7,245

To record sales on credit.

4

Cost of Goods Sold ………………………………………………

5,000

Merchandise Inventory ……………………………………

5,000

To record cost of sales.

9

Cash ……………………………………………………………..

19,200

Factoring Fee Expense* ………………………………...

800

Accounts Receivable ………………………………..

20,000

To record sale of receivable. *($20,000 x .04)

17

Cash ……………………………………………………………..

5,859

Accounts Receivable ………………………………..

5,859

To record cash received on account.

27

Cash ……………………………………………………………..

10,000

Notes Payable …………………………………………..

10,000

To record cash from a loan.

Note to Financial Statements

Accounts receivable in the amount of $12,500 are pledged

as security for a $10,000 note payable to Main Bank.

Exercise 9-11 (15 minutes)

Nov. 1

Notes Receivable—K. White ………………………..

6,000

Accounts Receivable—K. White ……………..

6,000

To record receipt of note on account.

Dec. 31

Interest Receivable ……………………………………..

80

Interest Revenue ……………………………………

80

To record interest earned

[$6,000 x .08 x 60/360].

Apr. 30

Cash …………………………………………………………..

6,240

Notes Receivable—K. White …………………..

6,000

Interest Revenue* …………………………..………

160

Interest Receivable ………………………………..

80

To record cash received on note plus

interest earned. *[$6,000 x .08 x 120/360]

Exercise 9-12 (20 minutes)

Mar. 21

Notes Receivable—T. Jackson …………………….…

9,500

Accounts Receivable—T. Jackson ………….…

9,500

To record receipt of note on account.

Sept. 17

Accounts Receivable—T. Jackson ……………….…

9,880

Interest Revenue ………………………………………

380

Notes Receivable—T. Jackson ……………….…

9,500

To record note dishonored plus interest

earned [$9,500 x .08 x 180/360 = $380].

Dec. 31

Allowance for Doubtful Accounts ………………..…

9,880

Accounts Receivable—T. Jackson ………….…

9,880

To write off an account.

Exercise 9-13 (10 minutes)

Instructor note: The first printing of the book for the December 13 transaction

erroneously read “60-day” note, but should have read “45–day” note. This does

not impact Exercise 13, but does impact the January 27 entry for Exercise 14.

2012

Dec. 13

Notes Receivable—M. Lee………………………

9,500

Accounts Receivable—M. Lee …………..

9,500

To record receipt of note on account.

Dec. 31

Interest Receivable ………………………………..

38

Interest Revenue ………………………………

38

To record interest earned [$9,500 x .08 x 18/360].

Exercise 9-14 (15 minutes)

Instructor note: The first printing of the book for the December 13 transaction

of Exercise 13 erroneously read “60-day” note, but should have read “45–day”

note. This does not impact Exercise 13, but does impact the January 27 entry

for Exercise 14. An erroneous marginal check figure of Dr. Cash 9,627 should

correctly read Dr. Cash 9,595.

2013

Jan. 27

Cash …………………………………………………………..…

9,595

Interest Revenue* …………………………..…………

57

Interest Receivable ………………………………..…

38

Notes Receivable—M. Lee ……………………..…

9,500

To record cash received on note plus interest.

* [$9,500 x .08 x (45–18)/360 = $57]

Mar. 3

Notes Receivable—Tomas Co. …………………….…

5,000

Accounts Receivable-Tomas Co …………….…

5,000

To record receipt of note on account.

17

Notes Receivable—H. Cheng ……………………….…

2,000

Accounts Receivable—H. Cheng ………………

2,000

To record receipt of note on account.

Apr. 16

Accounts Receivable—H. Cheng ……………………

2,015

Interest Revenue ………………………………………

15

Notes Receivable—H. Cheng ………………….…

2,000

To record receivable for dishonored

note plus interest [$2,000 x .09 x 30/360].

May 1

Allowance for Doubtful Accounts ………………..…

2,015

Accounts Receivable—H. Cheng ………………

2,015

To write off account.

June 1

Cash …………………………………………………………..…

5,125

Interest Revenue ………………………………………

125

Notes Receivable—Tomas Co ………………..…

5,000

To record cash received on note with

interest [$5,000 x .10 x 90/360].

Exercise 9-15 (15 minutes)

Instructor note: The first printing of the book has the far-right-hand column

erroneously titled “2010” that should be titled “2011”.

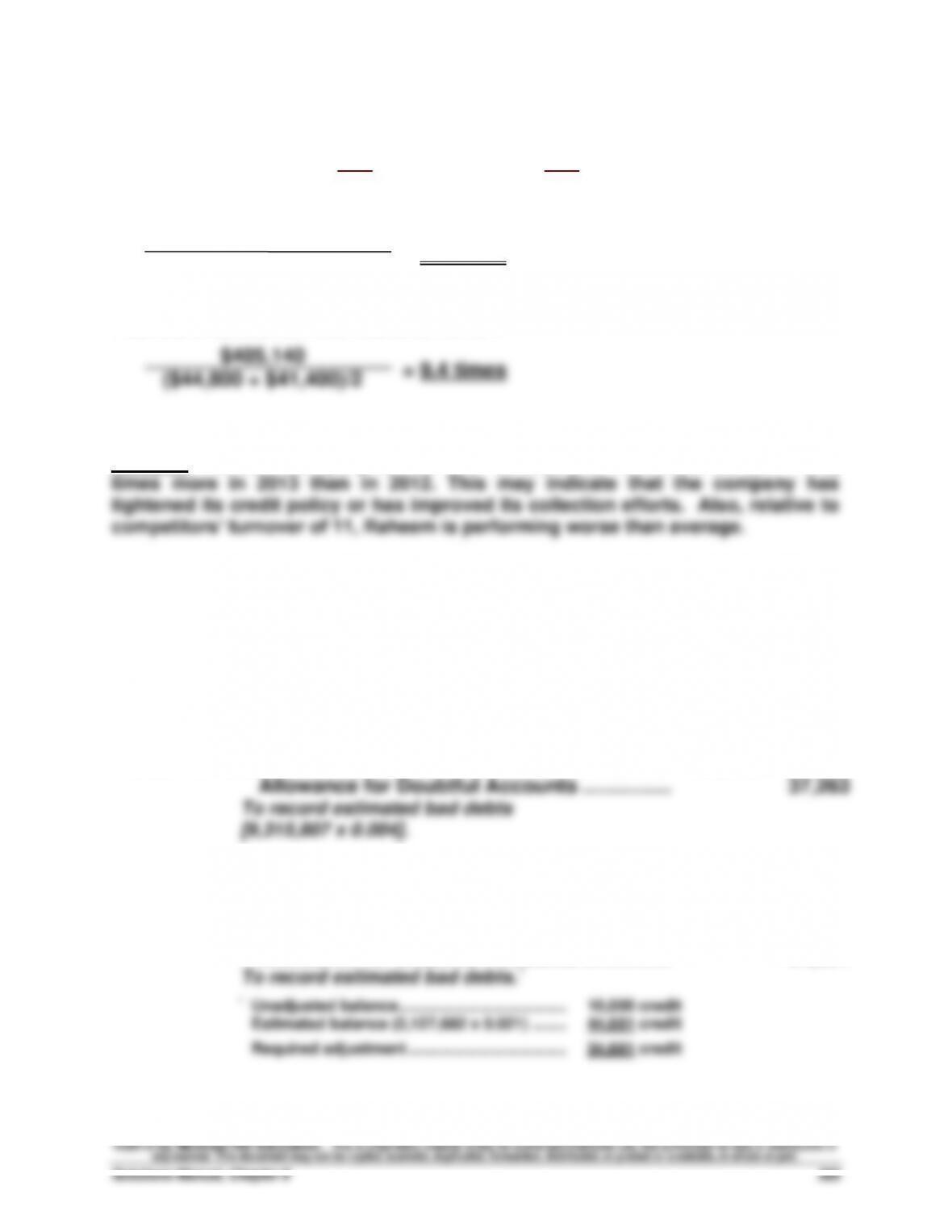

Year 2012 accounts receivable turnover:

= 8.8 times

Year 2013 accounts receivable turnover:

Analysis: Raheem Company turned over its accounts receivable 0.6 (9.4 – 8.8)

Exercise 9-16 (25 minutes)

($ in millions)

a. Expense is 0.4% of total revenues

Dec. 31

Bad Debts Expense ………………………………………..

37,263

Allowance for Doubtful Accounts ……………..

37,263

To record estimated bad debts

[9,315,807 x 0.004].

b. Allowance is 2.1% of trade receivables

Dec. 31

Bad Debts Expense ………………………………………..

34,681

Allowance for Doubtful Accounts ……………..

34,681

To record estimated bad debts.*

* Unadjusted balance ………………………………………………..

10,000 credit

Estimated balance (2,127,682 x 0.021) ……..……………..

44,681 credit

Required adjustment ……………………………….……………..

34,681 credit

$335,280

($41,400 + $34,800)/2