Title: Problem 22-7B

QA_Ori:

Part 1

NABAR MANUFACTURING

Sales Budgets

July, August, and September 2013

Budgeted

Units

Budgeted

Unit Price

Budgeted

Total Dollars

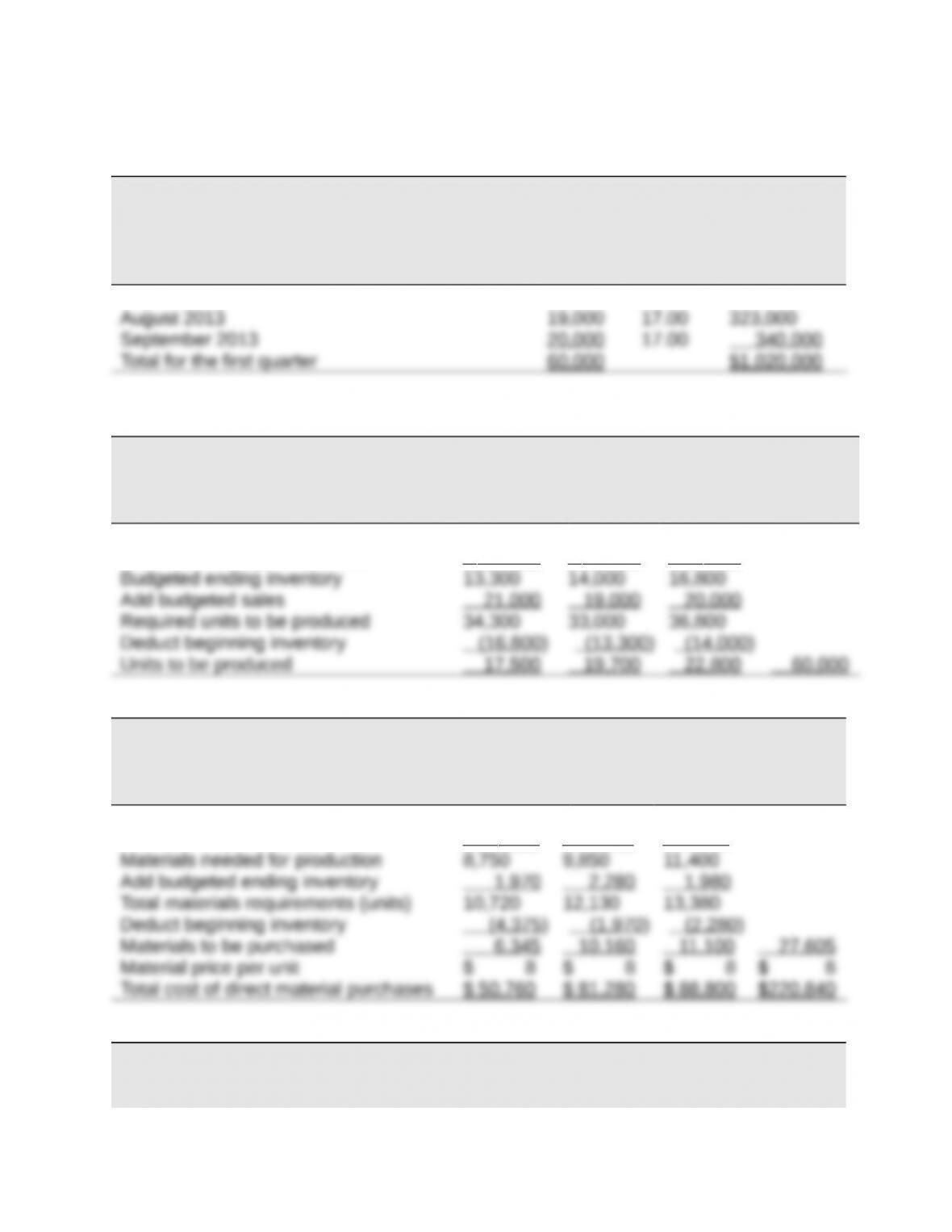

July 2013 21,000 $17.00 $ 357,000

Part 2

NABAR MANUFACTURING

Production Budget

July, August, and September 2013

July August Sept. Total

Next month’s budgeted sales 19,000 20,000 24,000

Ratio of inventory to future sales x 70% x 70% x 70%

Part 3

NABAR MANUFACTURING

Raw Materials Budget

July, August, and September 2013

July August Sept. Total

Production budget (units) 17,500 19,700 22,800

Materials requirement per unit x 0.50 x 0.50 x 0.50

Part 4

NABAR MANUFACTURING

Direct Labor Budget

July, August, and September 2013

July August Sept. Total

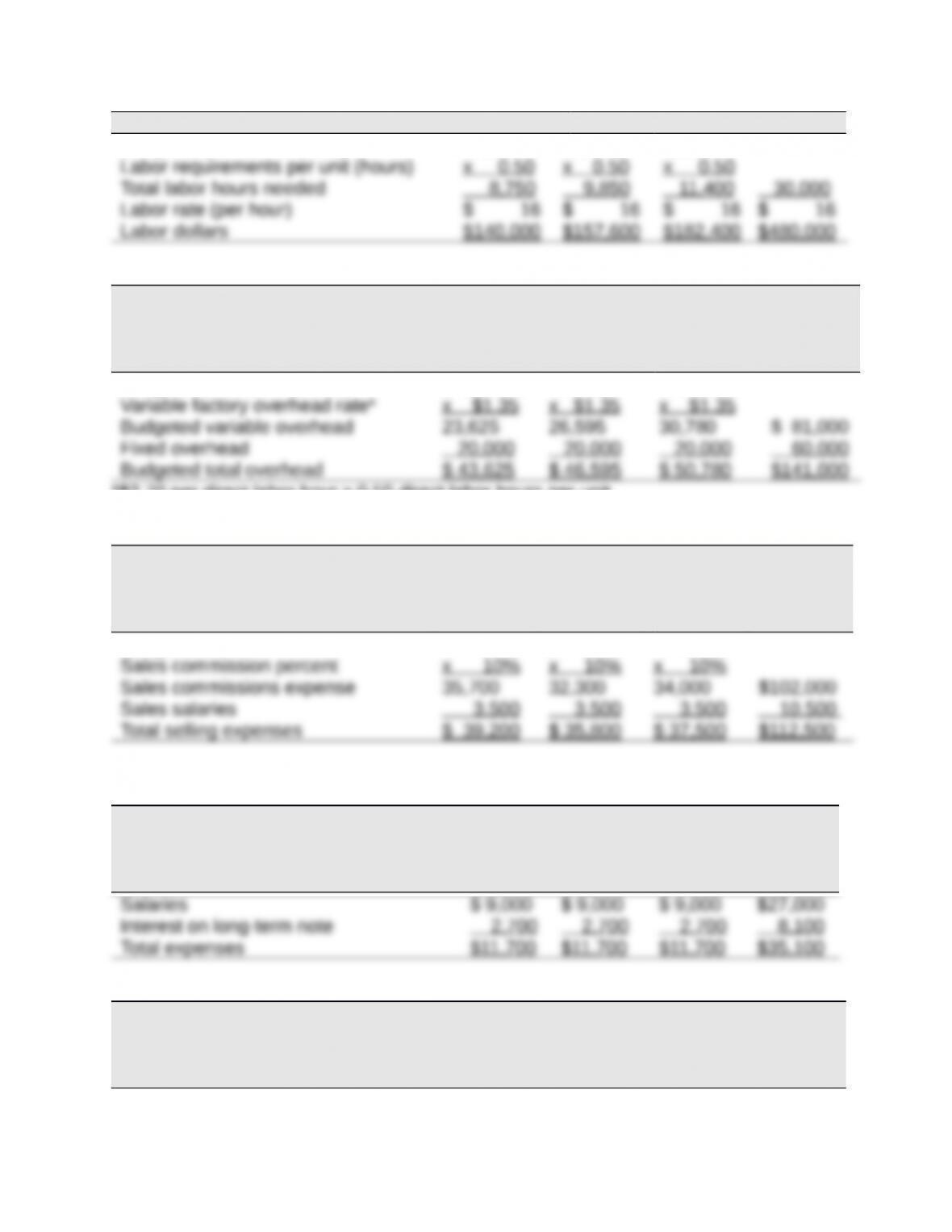

Budgeted production (units) 17,500 19,700 22,800

Part 5

NABAR MANUFACTURING

Factory Overhead Budget

July, August, and September 2013

July August Sept. Total

Budgeted production (units) 17,500 19,700 22,800

*$2.70 per direct labor hour x 0.50 direct labor hours per unit

Part 6

NABAR MANUFACTURING

Selling Expense Budgets

July, August, and September 2013

July August Sept. Total

Budgeted sales $357,000 $323,000 $340,000

Part 7

NABAR MANUFACTURING

General and Administrative Expense Budgets

July, August, and September 2013

July August Sept. Total

Part 8

NABAR MANUFACTURING

Cash Budgets

July, August, and September 2013

July August Sept.

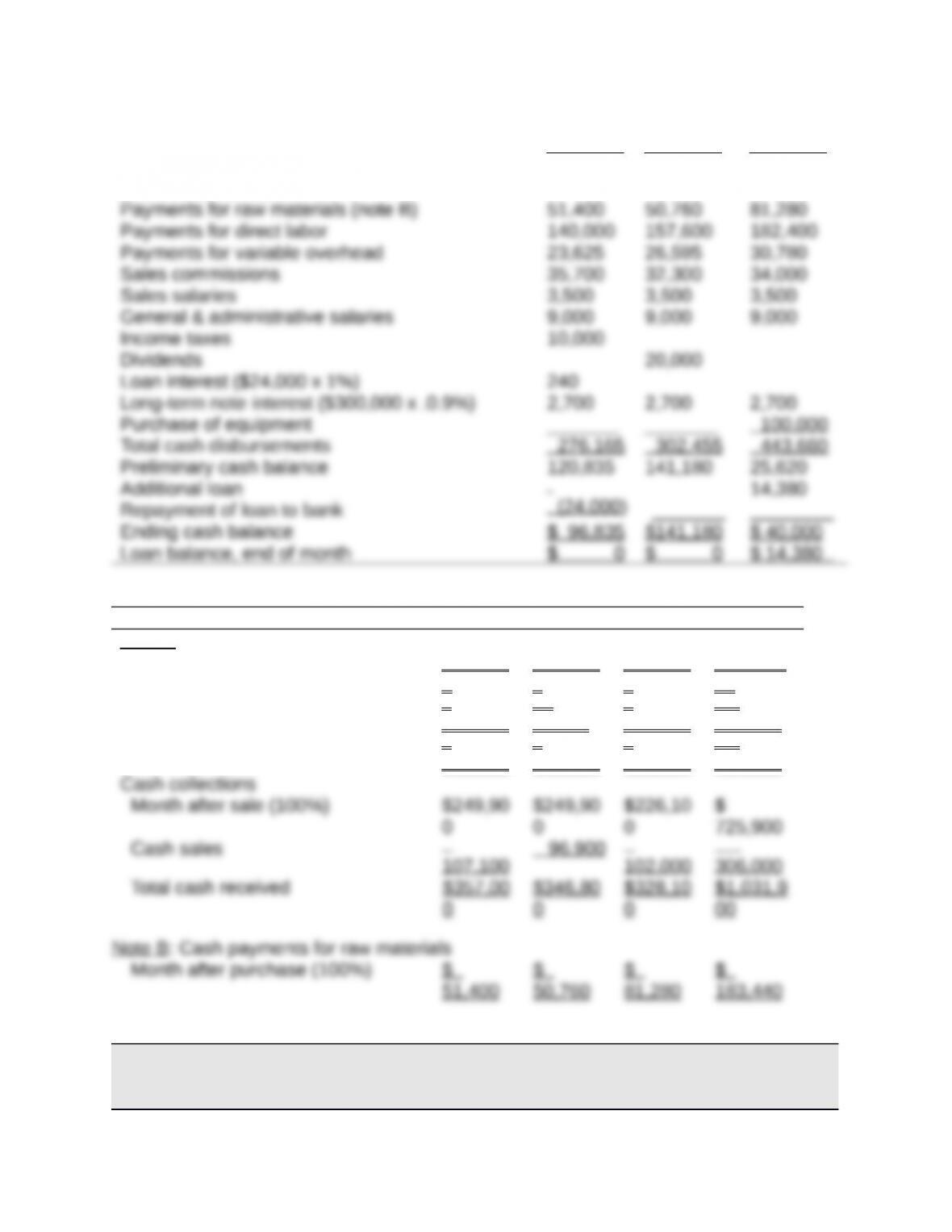

Beginning cash balance $ $ 96,835 $141,180

40,000

Cash receipts from customers (note A) 357,000 346,800 328,100

Total cash available 397,000 443,635 469,280

Cash disbursements

Supporting calculations July August Sept. Total

Note A: Cash receipts from customers

Total sales $357,00

0

$323,00

0

$340,00

0

$1,020,0

00

Cash sales (30%)

107,100

96,900

102,000

306,000

Credit sales (70%)

249,900

226,100

238,000

714,000

Part 9

NABAR MANUFACTURING

Budgeted Income Statement

For Three Months Ended September 30, 2013

Sales $1,020,000

Cost of goods sold (60,000 units @ $14.35) 861,000

Gross profit 159,000

Part — Budgeted Retained Earnings & Budgeted Balance Sheet

NABAR MANUFACTURING

Budgeted Balance Sheet

September 30, 2013

ASSETS

Cash $ 40,000 Cash budget

Accounts receivable 238,000 Note C

LIABILITIES AND EQUITY

Accounts payable $ 88,800 Note H

Supporting Footnotes

Note C

Note D

Less materials used in production**

(240,000)

Ending inventory raw materials inventory* $ 15,840

Note E

Beginning finished goods inventory $ 241,080

Note F

Note G

Note H

Note I

67,834

Title: Serial Problem, Success Systems

QA_Ori:

Part 1

SUCCESS SYSTEMS

Budgeted Income Statements

For Months of April, May, and June

April May June

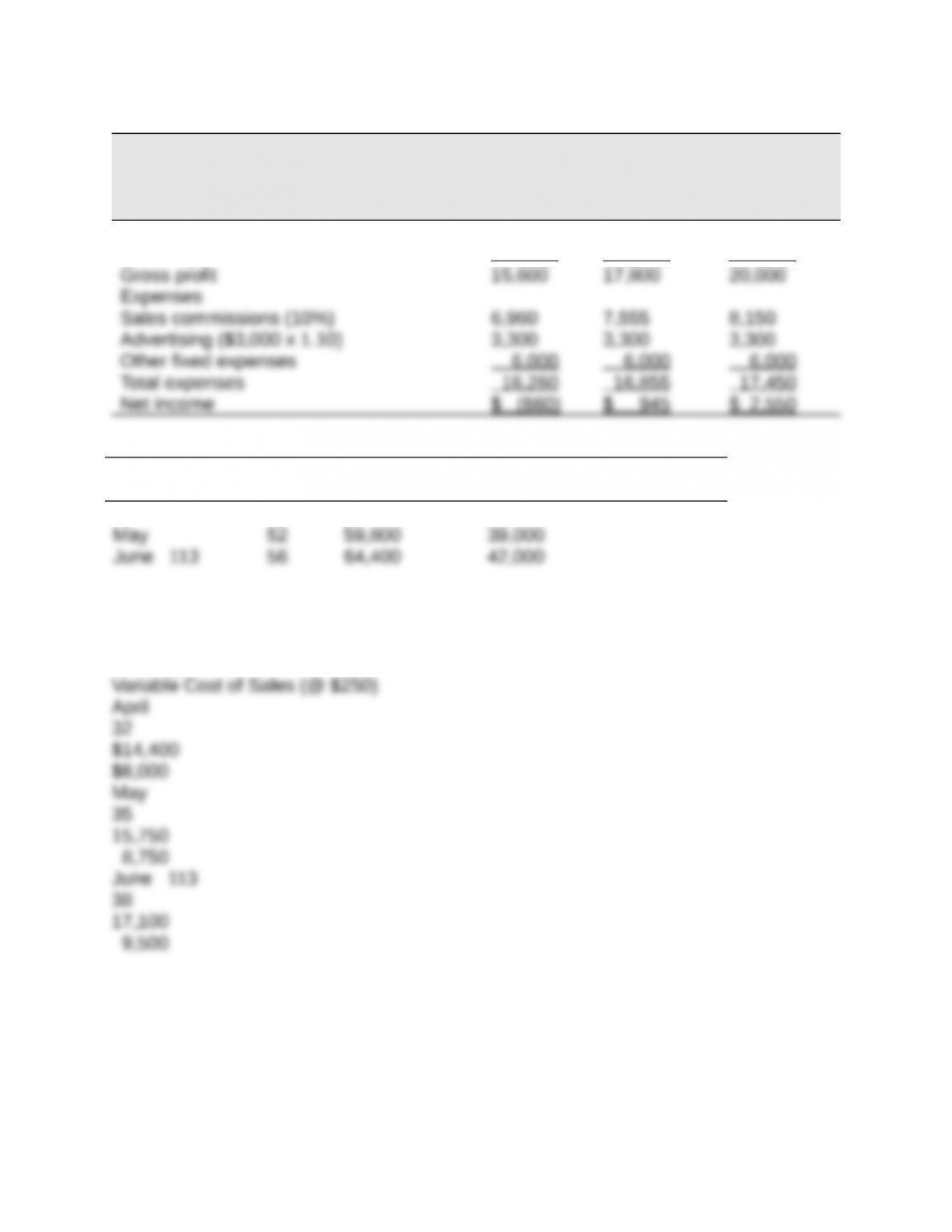

Sales* $69,600 $75,550 $81,500

Cost of goods sold** 54,000 57,750 61,500

*Results from per month volume increases for the next 3 months

Desks Units Sales (@

$1,150)

Variable Cost of Sales (@

$750)

April 48 $55,200 $36,000

Chairs

Units

Sales (@ $450)

Total Desk & Chairs

Sales

Variable Cost of Sales

April

May

June 113

**Total Cost of Sales

Variable

Fixed

Total Cost of Sales

April

May

47,750

Part 2

The plan for increasing sales volume by reducing the price and increasing advertising

would cause the company to generate a loss in the first month of the next quarter. This

result is not encouraging. However, the company would expect profits in each of the

Title: Reporting in Action 1

QA_Ori:

Title: Reporting in Action 2

QA_Ori:

a. Cash paid for acquisitions of property and equipment and reported on the statement

b. Given the assumption—that Polaris’s annual cash payments for acquisitions of

Title: Reporting in Action 3

QA_Ori:

Answers will depend on Polaris’s results obtained.

Title: Comparative Analysis 1

QA_Ori:

Computation of inventory reduction under new distribution system

Amount of ending inventory required at the 30% rule

This result implies that Arctic Cat can reduce its inventory level for the Canadian market

Title: Comparative Analysis 2

QA_Ori:

An analysis such as in part 1 along with an explanation can make clear to management

To further illustrate, assuming a 15% interest cost of resources tied up in

inventory, a company can save money by reducing its inventory level. In particular, by

Title: Ethics Challenge

QA_Ori:

Report on “Use It or Lose It” Budgeting

Instructor note: There is no widely accepted solution to this problem. The key is for the

student to think about the problem and work to at least modify the negative behavioral

consequences of this practice.

Any plan offered as a solution must better align upper management’s expectations with

department managers’ behavior. For example, upper management might only cut by

one-half the amount not spent according to budget. Another potential suggestion is to

allow department managers the option of justifying why the amount was not spent and

explain why current budget levels must be maintained.

Upper management must also keep in mind that efficient and effective allocation of

resources is necessary to provide high-quality services to customers and the public. All

spending behavior must be monitored. Without monitoring in the budgeting system,

even more money will be wasted or used inefficiently.

QA_Edit:

Title: Communicating in Practice

QA_Ori:

MEMORANDUM

TO: ____________________

FROM: ____________________

DATE: ____________________

SUBJECT: ____________________

The content of this memorandum will vary among students. The student must

The memorandum should explain why a concern with bias in the information does exist.

Specifically, if a bonus is paid when sales go over budget, then the sales staff is likely to

QA_Edit:

MEMORANDUM

TO: ____________________

FROM: ____________________

DATE: ____________________

SUBJECT: ____________________

Title: Taking It to the Net 1

QA_Ori:

The “e-budgets” Website lists a number of benefits such as accuracy, timeliness, ease

of sharing information, ease of updating, real-time comparison of actual performance vs.

estimates, and so on.

In the case of large, multi-divisional companies, coordination across and within divisions

Title: Taking It to the Net 2

QA_Ori:

As a senior manager, my biggest concern would be security, particularly when the

Title: Teamwork in Action

QA_Ori:

There is no specific solution to this assignment. The instructor should watch for proper

Title: Entrepreneurial Decision 1

QA_Ori:

Budgeting allows an organization to plan its activities better by allocating financial

Title: Entrepreneurial Decision 2

QA_Ori:

Sales forecasts and purchases budgets are particularly important in businesses like

Title: Hitting the Road 1 & 2

QA_Ori:

Instructor note: This problem is designed to (1) show that external factors are important

Climatic conditions.

Title: Global Decision 1

QA_Ori:

The infrastructure and administration expense budget is likely to be an important budget

Title: Global Decision 2

QA_Ori:

General office expenses

Top management salaries

Depreciation expense

Title: Global Decision 3

QA_Ori:

The initial responsibility usually rests with a vice president or an equivalent-level

manager. KTM is organized by divisions. Therefore, managers in each division may

have initial responsibility for the infrastructure and administration expense budget.