Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Fundamental Accounting Principles, 21st Edition

908

Problem 15-5B (Concluded)

2014

Aug. 1

Cash ..........................................................................................

27,000

Dividend Revenue .............................................................

27,000

Received cash dividends (20,000 x $1.35).

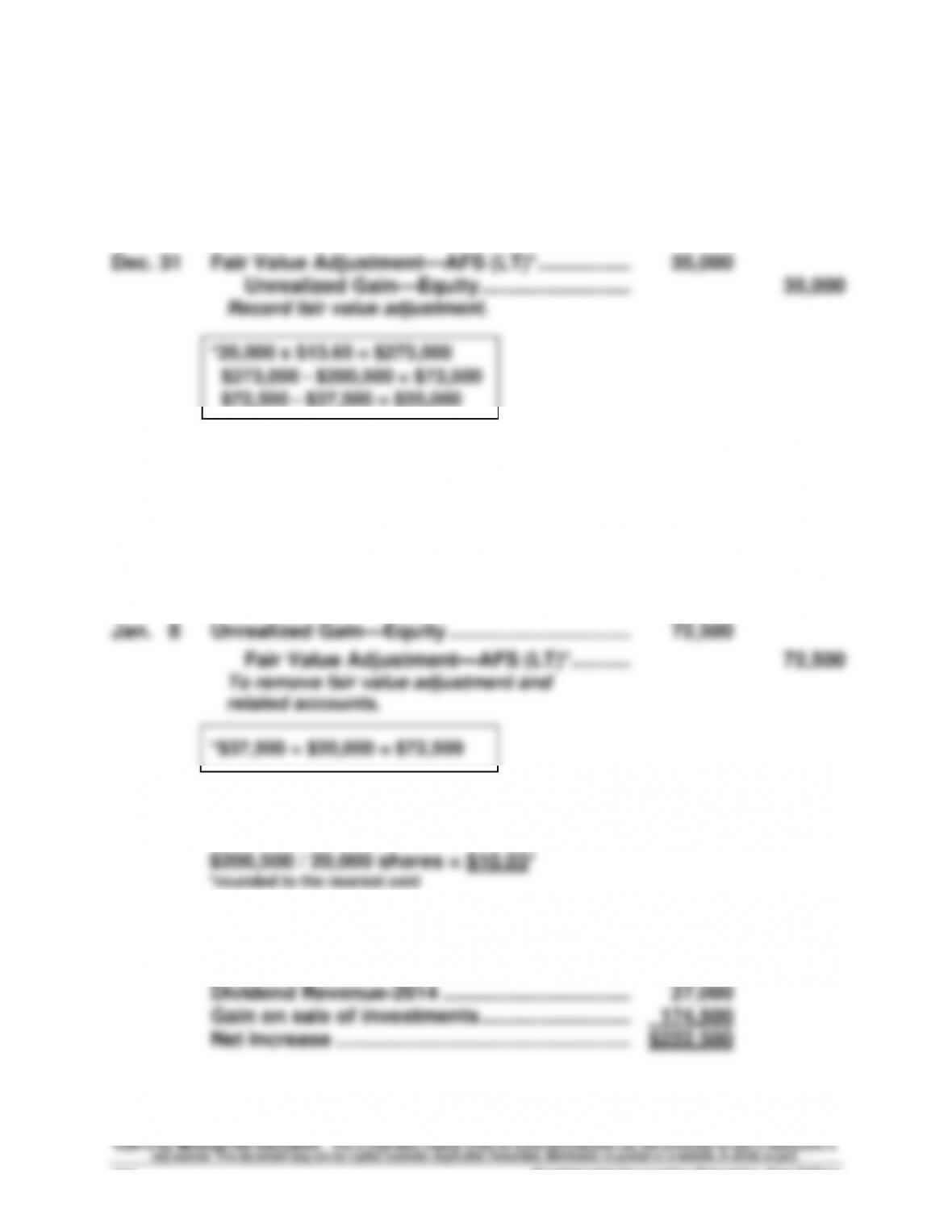

2015

Jan. 8

Cash ..........................................................................................

375,000

Long-Term Investments—AFS (Bloch) ............................

200,500

Gain on Sale of Investments ................................

174,500

Sold Bloch shares.

2. Investment cost per share, January 7, 2015

3. Change in Brinkley's equity

Dividend Revenue-2013 ......................................

$ 21,000

Problem 15-6BA (60 minutes)

Part 1

2013

May 26

Accounts Receivable—Fuji ................................

60,450

Sales ................................................................

60,450

(6,500,000 yen x $0.0093/yen)

Oct. 15

Accounts Receivable—Martinez Brothers ............................

38,556

Sales ................................................................

38,556

(378,000 pesos x $0.1020/peso)

Dec. 31

Accounts Receivable--Martinez Brothers .............................

1,512

Foreign Exchange Gain* ................................

1,512

*Original measure = (378,000 pesos x $0.1020/peso) = $38,556

*Original measure = (250,000 yuans x $0.1439/yuan) = $35,975

2014

Jan. 5

Cash* .........................................................................................

39,500

Accounts Receivable—Chi-Ying** ................................

36,250

Fundamental Accounting Principles, 21st Edition

910

Problem 15-6BA (Concluded)

Part 2

Foreign exchange gain reported on 2013 income statement

July 25 ....................................................

$ (650)

Part 3

To reduce the risk of foreign exchange gain or loss, Datamix could attempt

to negotiate foreign customer sales that are denominated in U.S. dollars.

Serial Problem — SP 15

Serial Problem, Success Systems (35 minutes)

Part 1

2014

April 16

Short-Term Investments—Trading (J&J) ..................

20,300

Cash ................................................................

20,300

Purchased Johnson & Johnson shares

[(400 x $50) + $300].

Part 2 Adjusting entry at June 30, 2014

June 30

Fair Value Adjustment—Trading* ........................

850

* Fair Value Adjustment computations

Trading securities’

portfolio

Shares

Share Price

at 6/30/2014

Fair

Value

Cost

Unrealized

Gain (Loss)

J & J ......................

400

$55

$22,000

$20,300

$1,700

Reporting in Action — BTN 15-1

1. Yes, Polaris’s financial statements are consolidated. The statements

2. Polaris’s comprehensive income for the year ended December 31, 2011,

Net income ...........................................................................................

$227,575

Foreign currency translation adjustments, net of tax benefit of $6,782 .....

2,554

4. The return on total assets for the year ended December 31, 2011,

($thousands) follows:

Comparative Analysis — BTN 15-2

1. Polaris’s return on total assets

Current Year: $227,575 / [($1,228,024 + $1,061,647) / 2] = 19.9%

Arctic Cat’s return on total assets

2. Return on total assets = Profit margin x Total asset turnover

Polaris’s component analysis of return on total assets*

Current Year

19.9% = $227,575/$2,656,949 x$2,646,949/[($1,228,024 + $1,061,647)/ 2]

19.9% = 8.6% x 2.31

One Year Prior

Arctic Cat’s component analysis of return on total assets*

Current Year

5.0% = 2.8% x 1.79

One Year Prior

Fundamental Accounting Principles, 21st Edition

914

Comparative Analysis (Concluded)

3. Current Year Analysis: Polaris has the higher return on total assets

(19.9%) compared to Arctic Cat (5.0%), the higher profit margin (8.6%

vs. 2.8% for Arctic Cat) and the higher total asset turnover (2.31 vs. 1.79

for Arctic Cat). Of the two companies, Polaris’s return on total assets is

Ethics Challenge — BTN 15-3

1. Kasey’s bonus is not contingent on the classification of available-for-

sale versus held-to-maturity. Designation of the bonds as available-for-

the past year in net income (and neither in equity).

2. Generally, Kasey must classify its debt securities as either short or long

term and as available-for-sale or held-to-maturity. Since the bonds are

5-year bonds they should be classified as long-term investments unless

3. The company’s auditors (internal and external) and/or its board of

Communicating in Practice — BTN 15-4

TO: Mary Jolee

FROM: (Your Name)

SUBJECT: Sale of Kemper Common Stock

The $6,000 loss on the sale of Kemper common stock is correctly stated.

Jolee Company owned 40% of the outstanding shares, and therefore

compared to the net proceeds to determine gain or loss.

During year 2012, the income statement showed earnings from all

investments of $126,000. This amount included $81,000 from the

investment in Kemper (Kemper’s 2012 net income of $202,500 x 40%),

Taking It to the Net — BTN 15-5

($ millions for Parts 1 through 4)

1. At June 30, 2011 (total cost-basis) .................................................... $60,804

2. Mutual funds; Commercial paper; Certificates of deposit; U.S.

3. Unrealized gains = $3,052; and Unrealized losses = $(219).

(recorded basis) is $63,637; and the cost basis is $60,804.

Teamwork in Action — BTN 15-6

There is no specific solution to this activity. The instructor should serve as

a facilitator during this learning reinforcement activity.

Entrepreneurial Decision — BTN 15-7

1.

2013

Jan. 1

Internet Rights ...................................................

106,920

Accounts Payable .......................................

106,920

Agreed to pay for Internet rights

12,000,000 yen x $0.00891/yen

2.

Mar. 31

Accounts Payable* ............................................

26,730

Loss from Currency Translation......................

60

Cash ..............................................................

26,790

Paid ¼ of total amount due

*$106,920/4 **3,000,000 yen x $0.00893/yen

*3,000,000 yen x $0.00897/yen

3. Since all of the company’s payments are to be in yen, the company can

buy yen in advance to “lock in” the payment amount.

Fundamental Accounting Principles, 21st Edition

918

Hitting the Road— BTN 15-8A

Exchange rates can be found at businesses that specialize in foreign currency

Global Decision— BTN 15-9

1. Piaggio (Euro in thousands)

Return on total assets = Net Income / Average Total Assets

Current Year: 47,053 / [(1,520,184 + 1,545,722)/2] = 3.1%

Prior Year: 42,811/ [(1,545,722 + 1,564,820)/2] = 2.8%

Current Year

3.1% = 3.1% x 0.99

One Year Prior

2. (a) Current Year Analysis: Piaggio vs Polaris vs Arctic Cat

Company

Return on total assets*

Profit margin

Total asset turnover

Polaris

19.9%

8.6%

2.31

In the current year, Polaris has the highest return on total assets

followed by a distant second, Arctic Cat, and third, Piaggio. Polaris also

Global Decision (Concluded)

2. (b) Prior Year Analysis: Piaggio vs Polaris vs Arctic Cat

Company

Return on total assets*

Profit margin

Total asset turnover

Polaris

16.1%

7.4%

2.18

In the prior year, Polaris has the highest return on total assets, with

Arctic Cat and Piaggio having a return on total assets substantially