Problem 11-2B (60 minutes)

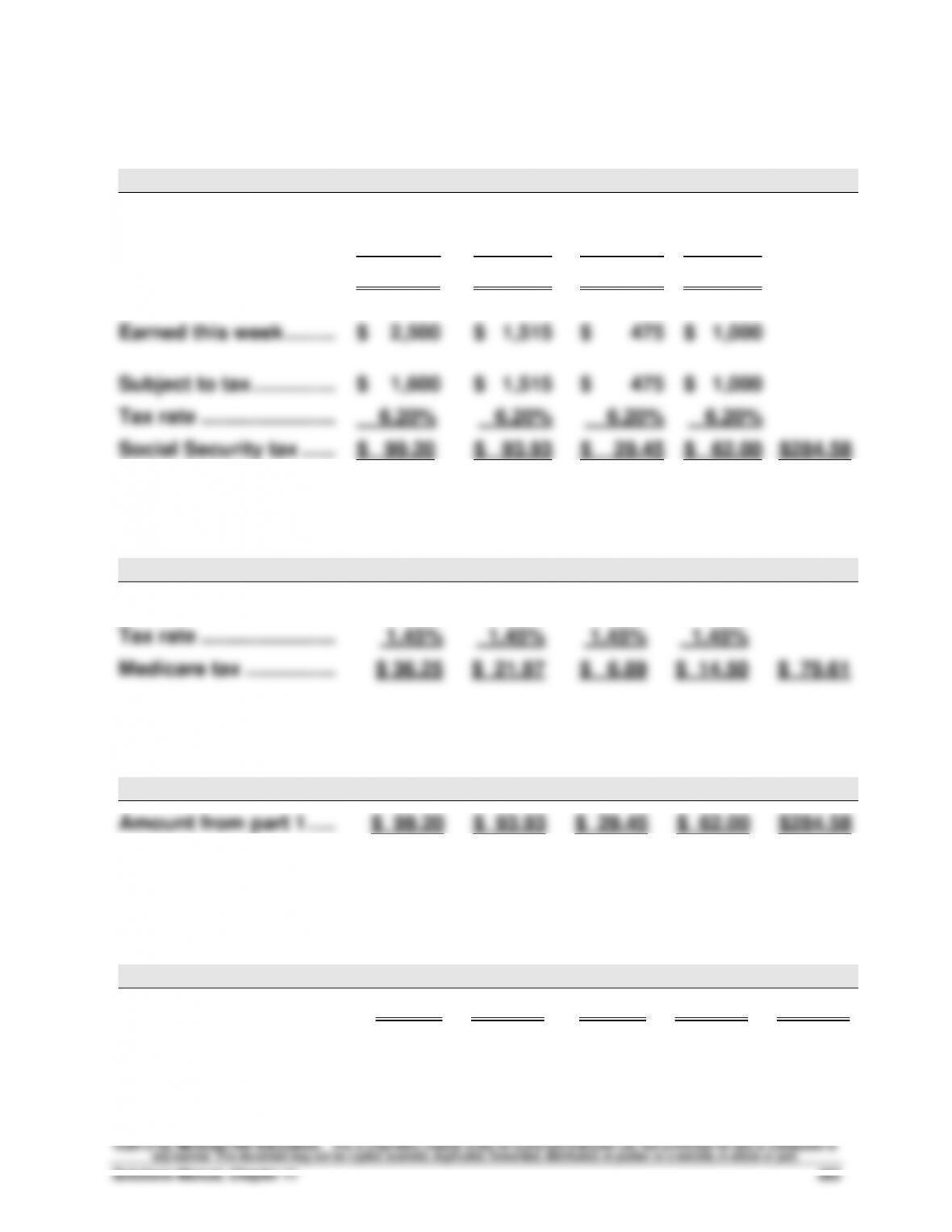

1. Each employee’s FICA withholdings for Social Security

Ahmed

Carlos

June

Marie

Total

Maximum base …………

$110,100

$110,100

$110,100

$110,100

Earned through 9/23 …

108,500

36,650

6,650

22,200

Amount subject to tax

$ 1,600

$ 73,450

$103,450

$ 87,900

Earned this week ………

$ 2,500

$ 1,515

$ 475

$ 1,000

Subject to tax ……………

$ 1,600

$ 1,515

$ 475

$ 1,000

Tax rate ……………………

6.20%

6.20%

6.20%

6.20%

Social Security tax ……

$ 99.20

$ 93.93

$ 29.45

$ 62.00

$284.58

2. Each employee’s FICA withholdings for Medicare (no limits)

Ahmed

Carlos

June

Marie

Total

Earned this week ………

$ 2,500

$ 1,515

$ 475

$ 1,000

Tax rate ……………………

1.45%

1.45%

1.45%

1.45%

Medicare tax …………….

$ 36.25

$ 21.97

$ 6.89

$ 14.50

$ 79.61

3. Employer’s FICA taxes for Social Security

Ahmed

Carlos

June

Marie

Total

Amount from part 1 …..

$ 99.20

$ 93.93

$ 29.45

$ 62.00

$284.58

4. Employer’s FICA taxes for Medicare

Ahmed

Carlos

June

Marie

Total

Amount from part 2 …..

$ 36.25

$ 21.97

$ 6.89

$ 14.50

$ 79.61

Problem 11-2B(Concluded)

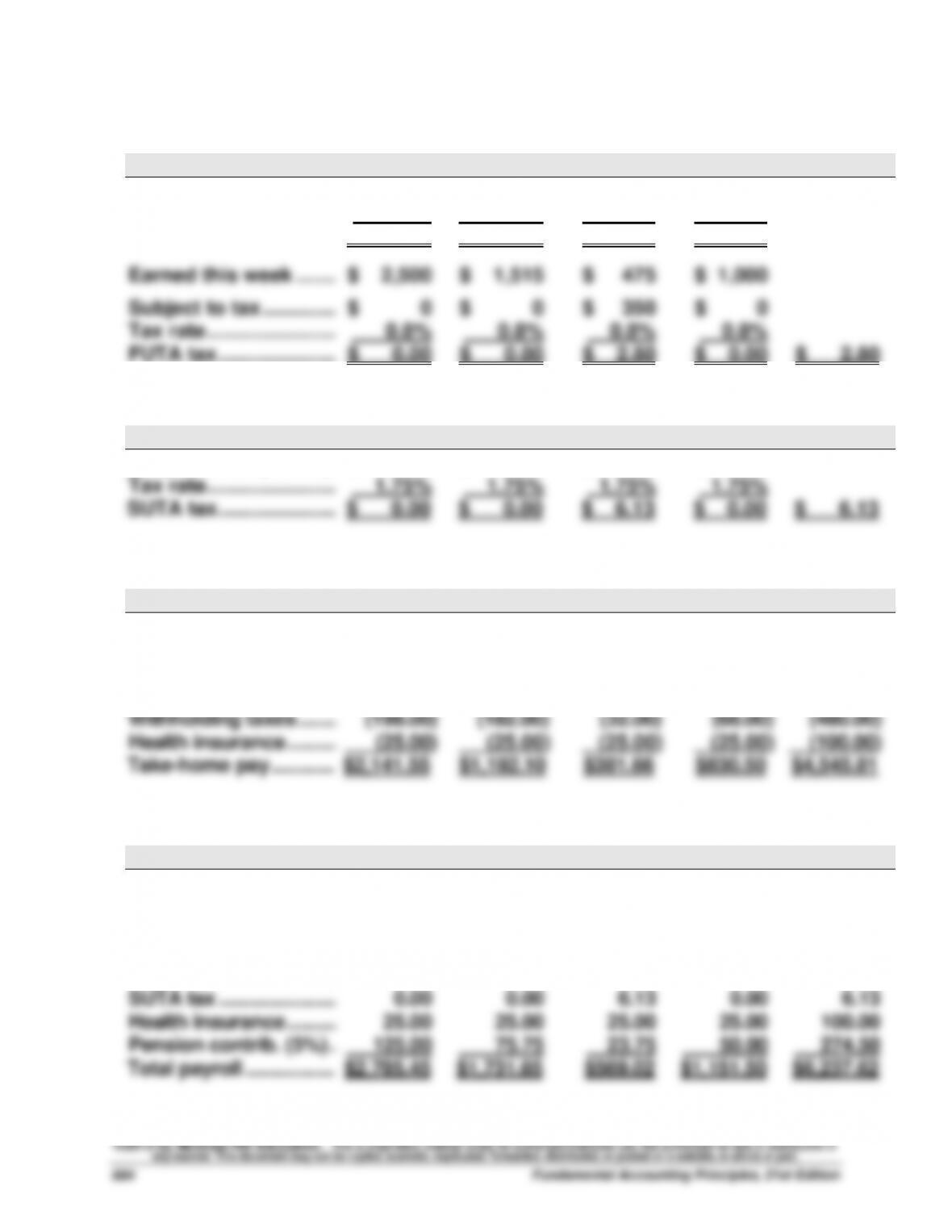

5. Employer’s FUTA taxes

Ahmed

Carlos

June

Marie

Total

Maximum base …………

$ 7,000

$ 7,000

$ 7,000

$ 7,000

Earned through 9/23 ...

108,500

36,650

6,650

22,200

Amount subject to tax .

$ 0

$ 0

$ 350

$ 0

Earned this week ……..

$ 2,500

$ 1,515

$ 475

$ 1,000

Subject to tax …………..

$ 0

$ 0

$ 350

$ 0

Tax rate ……………………

0.8%

0.8%

0.8%

0.8%

FUTA tax ………………….

$ 0.00

$ 0.00

$ 2.80

$ 0.00

$ 2.80

6. Employer’s SUTA taxes

Ahmed

Carlos

June

Marie

Total

Subject to tax (from 5) .

$ 0

$ 0

$ 350

$ 0

Tax rate ……………………

1.75%

1.75%

1.75%

1.75%

SUTA tax …………………

$ 0.00

$ 0.00

$ 6.13

$ 0.00

$ 6.13

7. Each employee’s net (take-home pay)

Ahmed

Carlos

June

Marie

Total

Gross earnings………….

$2,500.00

$1,515.00

$475.00

$1,000.00

$5,490.00

Less

FICA Social Sec. tax ….

(99.20)

(93.93)

(29.45)

(62.00)

(284.58)

FICA Medicare taxes …

(36.25)

(21.97)

(6.89)

(14.50)

(79.61)

Withholding taxes ……..

(198.00)

(182.00)

(32.00)

(68.00)

(480.00)

Health insurance ……….

(25.00)

(25.00)

(25.00)

(25.00)

(100.00)

Take-home pay ………….

$2,141.55

$1,192.10

$381.66

$830.50

$4,545.81

8. Employer’s total payroll-related expense for each employee

Ahmed

Carlos

June

Marie

Total

Gross earnings………….

$2,500.00

$1,515.00

$475.00

$1,000.00

$5,490.00

Plus

FICA Social Sec. tax ….

99.20

93.93

29.45

62.00

284.58

FICA Medicare taxes …

36.25

21.97

6.89

14.50

79.61

FUTA tax …………………..

0.00

0.00

2.80

0.00

2.80

SUTA tax …………………..

0.00

0.00

6.13

0.00

6.13

Health insurance ……….

25.00

25.00

25.00

25.00

100.00

Pension contrib. (5%) ..

125.00

75.75

23.75

50.00

274.50

Total payroll ………………

$2,785.45

$1,731.65

$569.02

$1,151.50

$6,237.62

Problem 11-3B (25 minutes)

Part 1

Jan. 8

Sales Salaries Expense …………………………………….

34,745.00

Office Salaries Expense ……………………………..…….

21,225.00

Delivery Salaries Expense…………………………..

1,030.00

FICA—Social Security Taxes Payable* …..…….

3,534.00

FICA—Medicare Taxes Payable** …………..…….

826.50

Employee Fed. Income Taxes Payable …..…….

8,625.00

Employee Med. Insurance Payable ………..…….

1,160.00

Employee Union Dues Payable ……………..…….

138.00

Salaries Payable ………………………………………….

42,716.50

To record payroll for period.

* $57,000 x 6.2% = $3,534.00

** $57,000 x 1.45% = $826.50

Part 2

Jan. 8

Payroll Taxes Expense ……………………………….…….

6,754.50

FICA—Social Security Taxes Payable ………….

3,534.00

FICA—Medicare Taxes Payable ……………..…….

826.50

State Unemployment Taxes Payable* …….…….

1,938.00

Federal Unemployment Taxes Payable** ….…….

456.00

To record employer payroll taxes.

* $57,000 x .034 = $1,938

**$57,000 x .008 = $456

Problem 11-4B (40 minutes)

1.

2013

Nov. 16

Cash ………………………………………………………………..

2,500

Sales ………………………………………………………….

2,500

Sold coffee grinders to customers.

16

Cost of Goods Sold ………………………………………….

1,200

Merchandise Inventory ……………………………….

1,200

To record cost of November 16 sale (50 x $24).

30

Warranty Expense ……………………………………………

250

Estimated Warranty Liability ……………………….

250

To record coffee grinder warranty expense

and liability at 10% of selling price.

Dec. 12

Estimated Warranty Liability …………………………….

144

Merchandise Inventory ……………………………….

144

To record cost of coffee grinder

warranty replacements (6 x $24).

18

Cash ………………………………………………………………..

10,000

Sales ………………………………………………………….

10,000

Sold coffee grinders to customers.

18

Cost of Goods Sold ………………………………………….

4,800

Merchandise Inventory ……………………………….

4,800

To record cost of December 18 sale (200 x $24).

28

Estimated Warranty Liability …………………………….

408

Merchandise Inventory ……………………………….

408

To record cost of coffee grinder

warranty replacements (17 x $24).

31

Warranty Expense ……………………………………………

1,000

Estimated Warranty Liability ……………………….

1,000

To record coffee grinder warranty expense

and liability at 10% of selling price.

Problem 11-4B (Concluded)

2014

Jan. 7

Cash ………………………………………………………………..

2,000

Sales ………………………………………………………….

2,000

Sold coffee grinders to customers.

7

Cost of Goods Sold ………………………………………….

960

Merchandise Inventory ……………………………….

960

To record cost of January 7 sale (40 x $24).

21

Estimated Warranty Liability …………………………….

864

Merchandise Inventory ……………………………….

864

To record cost of coffee grinder

warranty replacements (36 x $24).

31

Warranty Expense ……………………………………………

200

Estimated Warranty Liability ……………………….

200

To record coffee grinder warranty expense

and liability at 10% of selling price.

2. Warranty expense for November 2013 and December 2013

Sales

Percent

Warranty Expense

November …………………...

$ 2,500

10%

$ 250

December …………………….

10,000

10

1,000

Total …………………………..

$12,500

$1,250

3. Warranty expense for January 2014

Sales in January………………………..

$2,000

Warranty percent ……………………...

10%

Warranty expense ……………………...

$ 200

4. Balance of the estimated liability as of December 31, 2013

Warranty expense for November ……………………………..

$ 250

credit

Warranty expense for December……………………………...

1,000

credit

Cost of replacing items in December (23 x $24) ………..

(552)

debit

Estimated Warranty Liability balance ……………………….

$ 698

credit

5. Balance of the estimated liability as of January 31, 2014

Beginning balance …………………………………………………..

$ 698

credit

Warranty expense for January ………………………………...

200

credit

Cost of replacing items in January (36 x $24) …………..

(864)

debit

Estimated Warranty Liability balance ……………………….

$ 34

credit

Problem 11-5B (60 minutes)

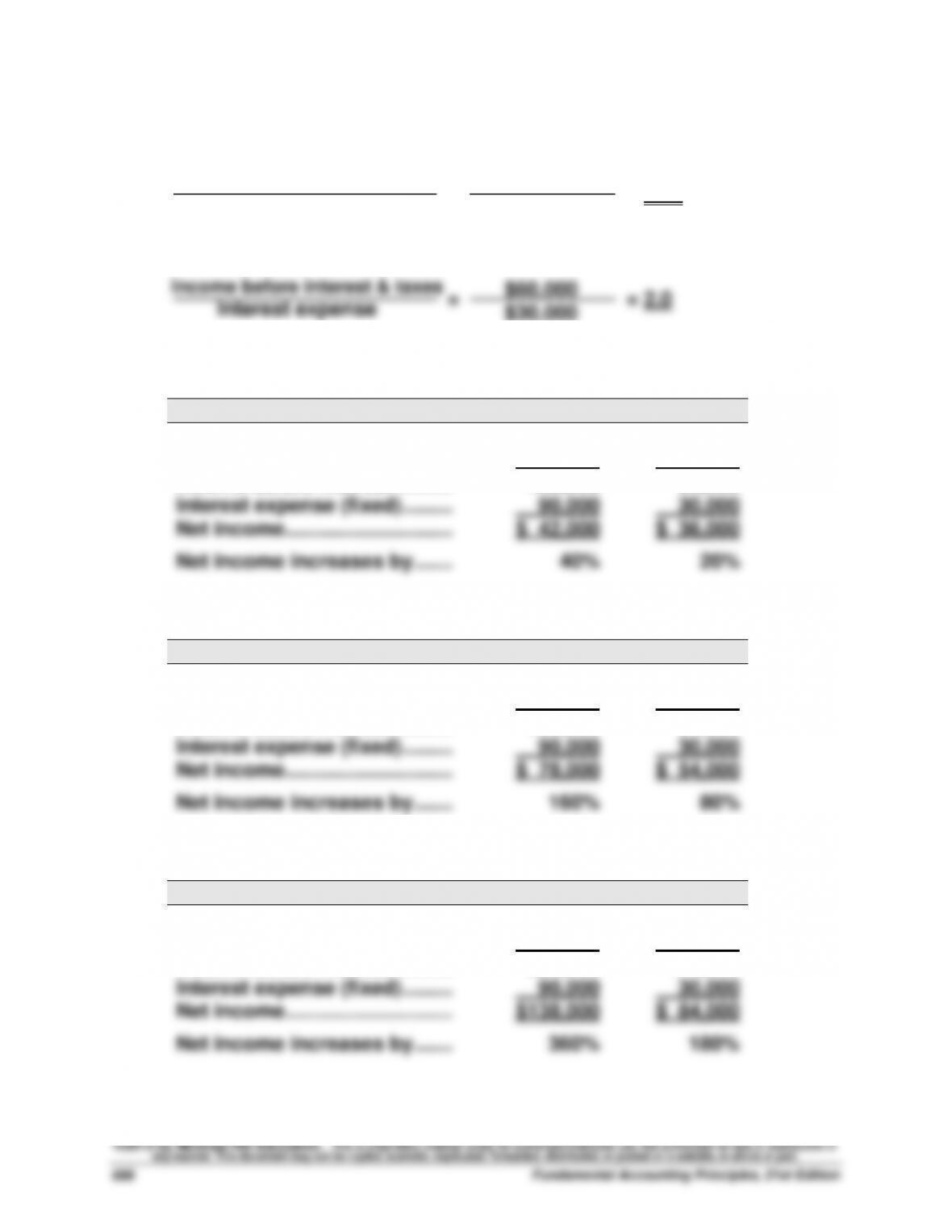

1. Ellis Company

= = 1.33

2. Seidel Company

3. Sales increase by 10% (multiply prior sales by 1.10)

Ellis Co.

Seidel Co.

Sales ………………………………….

$264,000

$264,000

Variable expenses ……………..

132,000

198,000

Income before interest ……….

132,000

66,000

Interest expense (fixed) ………

90,000

30,000

Net income …………………………

$ 42,000

$ 36,000

Net income increases by …….

40%

20%

4. Sales increase by 40% (multiply prior sales by 1.40)

Ellis Co.

Seidel Co.

Sales ………………………………….

$336,000

$336,000

Variable expenses ……………..

168,000

252,000

Income before interest ……….

168,000

84,000

Interest expense (fixed) ………

90,000

30,000

Net income …………………………

$ 78,000

$ 54,000

Net income increases by …….

160%

80%

5. Sales increase by 90% (multiply prior sales by 1.90)

Ellis Co.

Seidel Co.

Sales ………………………………….

$456,000

$456,000

Variable expenses ……………..

228,000

342,000

Income before interest ……….

228,000

114,000

Interest expense (fixed) ………

90,000

30,000

Net income …………………………

$138,000

$ 84,000

Net income increases by …….

360%

180%

Income before interest & taxes

Interest expense

Interest expense

$120,000

$90,000

$30,000

Problem 11-5B (Concluded)

6. Sales decrease by 20% (multiply prior sales by 0.80)

Ellis Co.

Seidel Co.

Sales ………………………………….

$192,000

$192,000

Variable expenses ……………..

96,000

144,000

Income before interest ……….

96,000

48,000

Interest expense (fixed) ………

90,000

30,000

Net income …………………………

$ 6,000

$ 18,000

Net income decreases by ……

–80%

–40%

7. Sales decrease by 50% (multiply prior sales by 0.50)

Ellis Co.

Seidel Co.

Sales ………………………………….

$120,000

$120,000

Variable expenses ……………..

60,000

90,000

Income before interest ……….

60,000

30,000

Interest expense (fixed) ………

90,000

30,000

Net income …………………………

$(30,000)

$ 0

Net income decreases by ……

–200%

–100%

8. Sales decrease by 80% (multiply prior sales by 0.20)

Ellis Co.

Seidel Co.

Sales ………………………………….

$ 48,000

$ 48,000

Variable expenses ……………..

24,000

36,000

Income before interest ……….

24,000

12,000

Interest expense (fixed) ………

90,000

30,000

Net income …………………………

$(66,000)

$(18,000)

Net income decreases by ……

–320%

–160%

9. The higher fixed cost strategy (having more fixed interest expense) of

Ellis Co. accentuates the effects of increases and decreases in sales.

That is, increases in sales produce greater increases in net income and

Fundamental Accounting Principles, 21st Edition

690

Problem 11-6BA (50 minutes)

June 15

FICA—Social Security Taxes Payable ……………….

992

FICA—Medicare Taxes Payable …………………….….

232

Employee Fed. Income Taxes Payable …………..….

1,050

Cash ……………………………………………………….

2,274

To record payment of FICA and

federal income taxes.

30

Office Salaries Expense ………………………………..….

3,800

Shop Salaries Expense …………………………………….

4,200

FICA—Social Security Taxes Payable ………….

496

FICA—Medicare Taxes Payable ……………….….

116

Employee Fed. Income Taxes Payable ……..….

1,050

Salaries Payable ……………………………………..….

6,338

To record payroll period.

30

Salaries Payable …………………………………………..….

6,338

Cash ……………………………………………………….

6,338

To record payment of payroll.*

*Check numbers may be entered in the Payroll Register.

30

Payroll Taxes Expense* …………………………………….

612

FICA⎯Social Security Taxes Payable ………….

496

FICA⎯Medicare Taxes Payable ……………….….

116

To record employer payroll taxes.

*Amount earned through 5/31 = 5 x $1,600 = $8,000

Subject to SUTA/FUTA in June = $0

SUTA = $0

FUTA = $0

FICA⎯Social Security Taxes = $496 (same as employees)

FICA⎯Medicare Taxes = $116 (same as employees)

Problem 11-6BA (Concluded)

July 15

FICA⎯Social Security Taxes Payable ……………….

992

FICA⎯Medicare Taxes Payable …………………….….

232

Employee Fed. Income Taxes Payable …………..….

1,050

Cash ……………………………………………………….

2,274

To record payment of FICA and

federal income taxes.

15

State Unemployment Taxes Payable ……………..….

440

Cash ……………………………………………………….

440

To record payment of SUTA taxes.

31

Federal Unemployment Taxes Payable ………….….

88

Cash ……………………………………………………….

88

To record payment of FUTA taxes.

31

No entry required upon mailing Form 941.

Serial Problem — SP 11

Serial Problem — SP 11, Success Systems (30 minutes)

1.

Gross pay (8 days x $125 per day) ……………………………..

$1,000.00

FICA Social Security tax deduction (6.2%)* ………………...

$ 62.00

FICA Medicare tax deduction (1.45%) ………………………...

14.50

Income tax deduction ………………………………………………..

159.00

Total deductions ……………………………………………………….

235.50

Net Pay ……………………………………………………………………..

$ 764.50

*Employee has not reached the maximum limit.

2. 2014

Feb. 26

Wages Expense ……………………………………………….

1,000.00

FICA—Social Security Taxes Payable ………….

62.00

FICA—Medicare Taxes Payable ……………….….

14.50

Employee Federal Income Taxes Payable ..…..

159.00

Cash ……………………………………………………….

764.50

To record payroll period.

3. 2014

Feb. 26

Payroll Taxes Expense ………………………………….….

124.50

FICA—Social Sec. Taxes Payable …………….….

62.00

FICA—Medicare Taxes Payable ……………….….

14.50

State Unemployment Taxes Payable* ……….….

40.00

Federal Unemployment Taxes Payable** …….….

8.00

To record employer payroll taxes.

* $1,000 x .04 = $40.00

**$1,000 x .008 = $8.00

4. 2014

Mar. 25

Accounts Receivable – Wildcat Services ……….….

2,912

Sales ……………………………………………………….

2,800

Sales Taxes Payable ……………………………….….

112

Sold merchandise on credit and collected

sales tax of 4%.

Mar. 25

Cost of Goods Sold ………………………………………….

2,002

Merchandise Inventory ……………………………….

2,002

To record cost of March 25 sale.

Comprehensive Problem

Bug-Off Exterminators (100 minutes)

Part 1

a. Correct ending balance of cash and the amount of the omitted check

Balance per bank …………………………..

$15,100

Plus deposit in transit …………………..…

2,450

Less outstanding checks …………………

(1,800)

Reconciled balance …………………………

$15,750

Balance per books ………………………..…

$17,000

Plus interest earned…………………………

52

Less service charges ………………………

(15)

Balance before omitted check ……….…

17,037

Reconciled balance (from above) …………

(15,750)

Omitted check …………………………………

$ 1,287

b. Allowance for doubtful accounts

Unadjusted balance …………………………

$ 828

credit

Anticipated write-off ……………………..…

(679)

debit

Revised unadjusted balance ……………

149

credit

Desired ending balance ………………..…

700

credit

Necessary adjustment …………………..…

$ 551

credit

c. Depreciation expense on the truck

Cost ……………………………………………..………..

$32,000

Less salvage value ……………………….….

(8,000)

Depreciable cost …………………………..

$24,000

Useful life (years) …………………………..

4

Annual depreciation for 2013 ………..…………….

$ 6,000

d. Depreciation expense on the equipment

Sprayer

Injector

Cost ……………………………………………..…

$27,000

$18,000

Less salvage value ……………………….…

(3,000)

(2,500)

Depreciable cost …………………………..

$24,000

$15,500

Useful life (years) …………………………..

8

5

Depreciation for 2013 ………………………

$ 3,000

$ 3,100

Comprehensive Problem (Continued)

e. Adjusted revenue and unearned revenue balances

Total advance received ………………………………….

$ 3,840

Months in contract …………………………………………

12

Revenue per month ……………………………………….

$ 320

Months of services provided ………………………….

5

Total earned ($320 x 5 months) ………………………

(1,600)

Overstatement of revenue ($3,840 – $1,600) ……

$ 2,240

Extermination Services Revenue account

Unadjusted balance ……………………………………….

$60,000

Overstatement ……………………………………………….

(2,240)

Adjusted balance …………………………………………..

$57,760

Unearned Services Revenue account

Unadjusted balance ……………………………………….

$ 0

Adjustment ……………………………………………………

2,240

Adjusted balance …………………………………………..

$ 2,240

f. Warranty expense

Adjusted services revenue for the year (from e) ….

$57,760

Warranty percent ………………………………………….

2.5%

Warranty expense (estimated) ……………………….

$ 1,444

Estimated warranty liability

Unadjusted balance ………………………………………

$ 1,400

credit

Warranty expense …………………………………………

1,444

credit

Ending adjusted balance ………………………………

$ 2,844

credit

g. Note payable and interest accrual

The note originated on December 31, 2013. The first time interest

Comprehensive Problem (Continued)

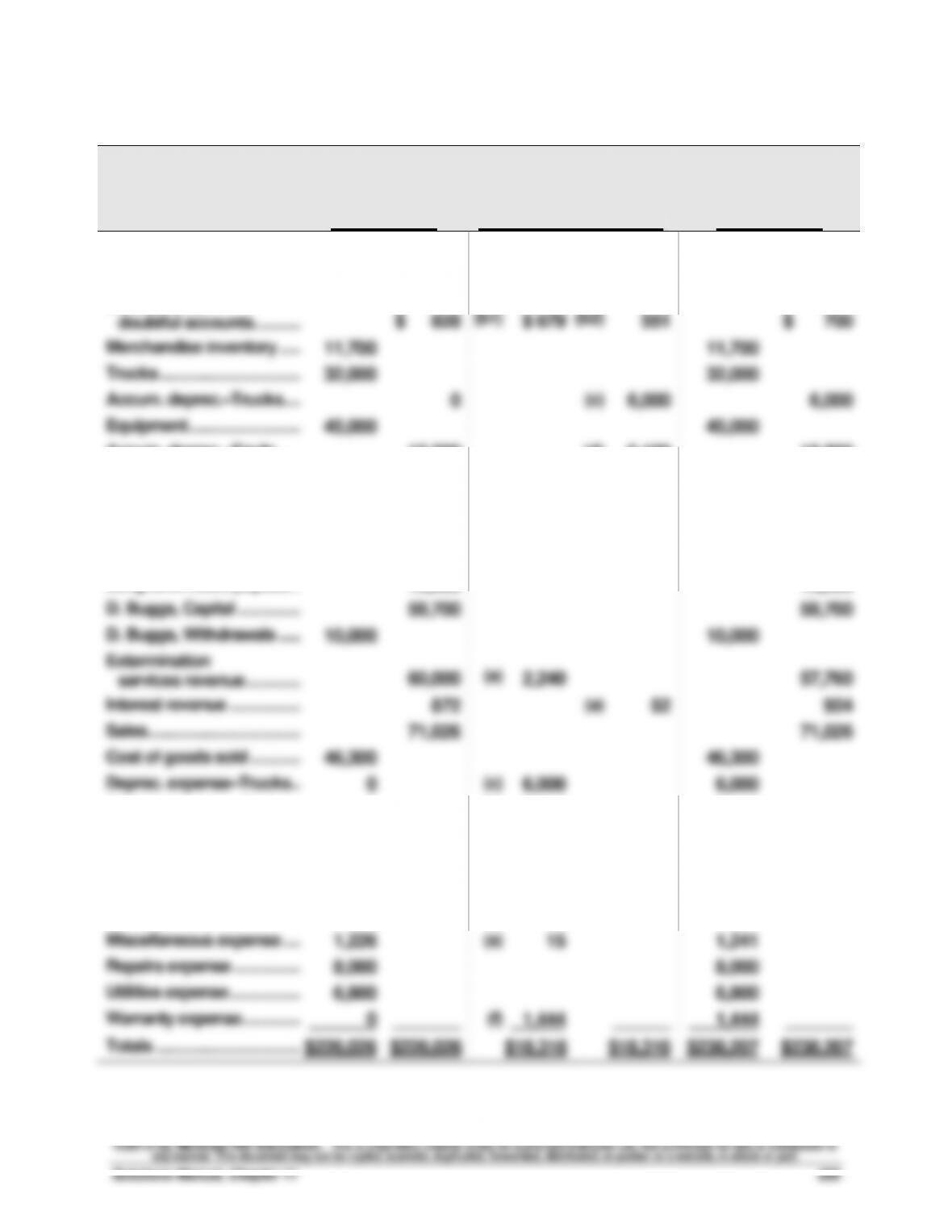

Part 2

BUG-OFF EXTERMINATORS

December 31, 2013

Unadjusted

Trial Balance

Adjustments .

Adjusted

Trial Balance

Cash ……………………………….……

$ 17,000

(a)

$1,250

$ 15,750

Accounts receivable ………..……

4,000

(b1)

679

3,321

Allowance for

doubtful accounts ………………

$ 828

(b1)

$ 679

(b2)

551

$ 700

Merchandise inventory …………

11,700

11,700

Trucks ……………………………..……

32,000

32,000

Accum. deprec.–Trucks …..……

0

(c)

6,000

6,000

Equipment ……………………….….

45,000

45,000

Accum. deprec.–Equip …………

12,200

(d)

6,100

18,300

Accounts payable …………………

5,000

(a)

1,287

3,713

Estim. warranty liability …………

1,400

(f)

1,444

2,844

Unearned services rev …….……

0

(e)

2,240

2,240

Interest payable ……………………

0

0

Long–term notes payable ..……

15,000

15,000

D. Buggs, Capital …………….……

59,700

59,700

D. Buggs, Withdrawals …………

10,000

10,000

Extermination

services revenue …………..……

60,000

(e)

2,240

57,760

Interest revenue ……………………

872

(a)

52

924

Sales ………………………………..……

71,026

71,026

Cost of goods sold ………….……

46,300

46,300

Deprec. expense–Trucks ………

0

(c)

6,000

6,000

Deprec. expense–Equip …..……

0

(d)

6,100

6,100

Wages expense ……………….……

35,000

35,000

Interest expense ……………………

0

0

Rent expense …………………..……

9,000

9,000

Bad debts expense ………….……

0

(b2)

551

551

Miscellaneous expense …..……

1,226

(a)

15

1,241

Repairs expense ……………..……

8,000

8,000

Utilities expense ……………………

6,800

6,800

Warranty expense …………………

0

_______

(f)

1,444

______

1,444

_______

Totals ……………………………………

$226,026

$226,026

$18,316

$18,316

$238,207

$238,207