Problem 4-2B (Concluded)

Office Supplies Expense Acct. No. 650

Date Explanation PR Debit Credit Balance

July 31 Adjusting 875 875

31 Closing 875 0

Repairs Expense Acct. No. 684

Date Explanation PR Debit Credit Balance

Telephone Expense Acct. No. 688

Date Explanation PR Debit Credit Balance

July 30 400 400

31 Closing 400 0

Income Summary Acct. No. 901

Date Explanation PR Debit Credit Balance

Fundamental Accounting Principles, 21st Edition

256

Problem 4-3B (90 minutes) Part 1

POWER DEMOLITION COMPANY

Work Sheet

For Year Ended April 30, 2013

Unadjusted

Trial Balance

Adjustments

Adjusted

Trial Balance

Income

Statement

Balance Sheet

and Statement of

Owner’s Equity

No.

Account Title

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

101

Cash ………………………………………………….……

7,000

7,000

7,000

126

Supplies …………………………………………..……….

16,000

(a)

8,100

7,900

7,900

128

Prepaid insurance …………………………..

12,600

(b)

10,600

2,000

2,000

167

Equipment ……………………………………………….

200,000

200,000

200,000

168

Accumulated depreciation—

Equipment …………………………………….……….

14,000

(c)

7,000

21,000

21,000

201

Accounts payable …………………………..

6,800

(d)

800

7,600

7,600

203

Interest payable ……………………………………….

(h)

300

300

300

208

Rent payable …………………………………..……….

(f)

3,000

3,000

3,000

210

Wages payable ……………………………………….

(e)

2,000

2,000

2,000

213

Property taxes payable ………………..……….

(g)

550

550

550

251

Long–term notes payable …………….……….

30,000

30,000

30,000

301

J. Bonn, Capital ……………………………………….

86,900

86,900

86,900

302

J. Bonn, Withdrawals …………………………..

12,000

12,000

12,000

401

Demolition fees earned ………………..……….

187,000

187,000

187,000

612

Depreciation expense—Equip …..……….

(c)

7,000

7,000

7,000

623

Wages expense ……………………………..……….

41,400

(e)

2,000

43,400

43,400

633

Interest expense …………………………….……….

3,300

(h)

300

3,600

3,600

637

Insurance expense ……………………….….

(b)

10,600

10,600

10,600

640

Rent expense ………………………………….……….

13,200

(f)

3,000

16,200

16,200

652

Supplies expense …………………………..

(a)

8,100

8,100

8,100

683

Property taxes expense ……………….……….

9,700

(g)

550

10,250

10,250

684

Repairs expense …………………………………….

4,700

4,700

4,700

690

Utilities expense ……………………………..……….

4,800

______

(d)

800

______

5,600

______

5,600

______

______

______

Totals ………………………………………………..……..

324,700

324,700

32,350

32,350

338,350

338,350

109,450

187,000

228,900

151,350

Net Income ……………………………………………….

77,550

______

______

77,550

Totals ………………………………………………..……..

187,000

187,000

228,900

228,900

Problem 4-3B (Continued)

Part 2 Adjusting entries (all on April 30, 2013)

Instructor note: Entries are shown without an account reference column because no posting is required.

To record expiration of insurance.

(c) Depreciation Expense—Equipment……………. 7,000

Accumulated Depreciation–Equipment .. 7,000

To record depreciation.

(d) Utilities Expense ……………………………………….. 800

Accounts Payable ………………………………. 800

To record accrued utilities costs.

(e) Wages Expense ………………………………………… 2,000

Wages Payable …………………………………… 2,000

To record accrued wages.

Problem 4-3B (Continued)

Closing entries (all on April 30, 2013)

Instructor note: Entries are shown without an account reference column because no posting is required.

(1) Demolition Fees Earned ………………………… 187,000

Income Summary ……………………………. 187,000

To close the revenue account.

To close the expense accounts.

(3) Income Summary ………………………………….. 77,550

J. Bonn, Capital ………………………………. 77,550

To close the Income Summary account.

Problem 4-3B (Continued)

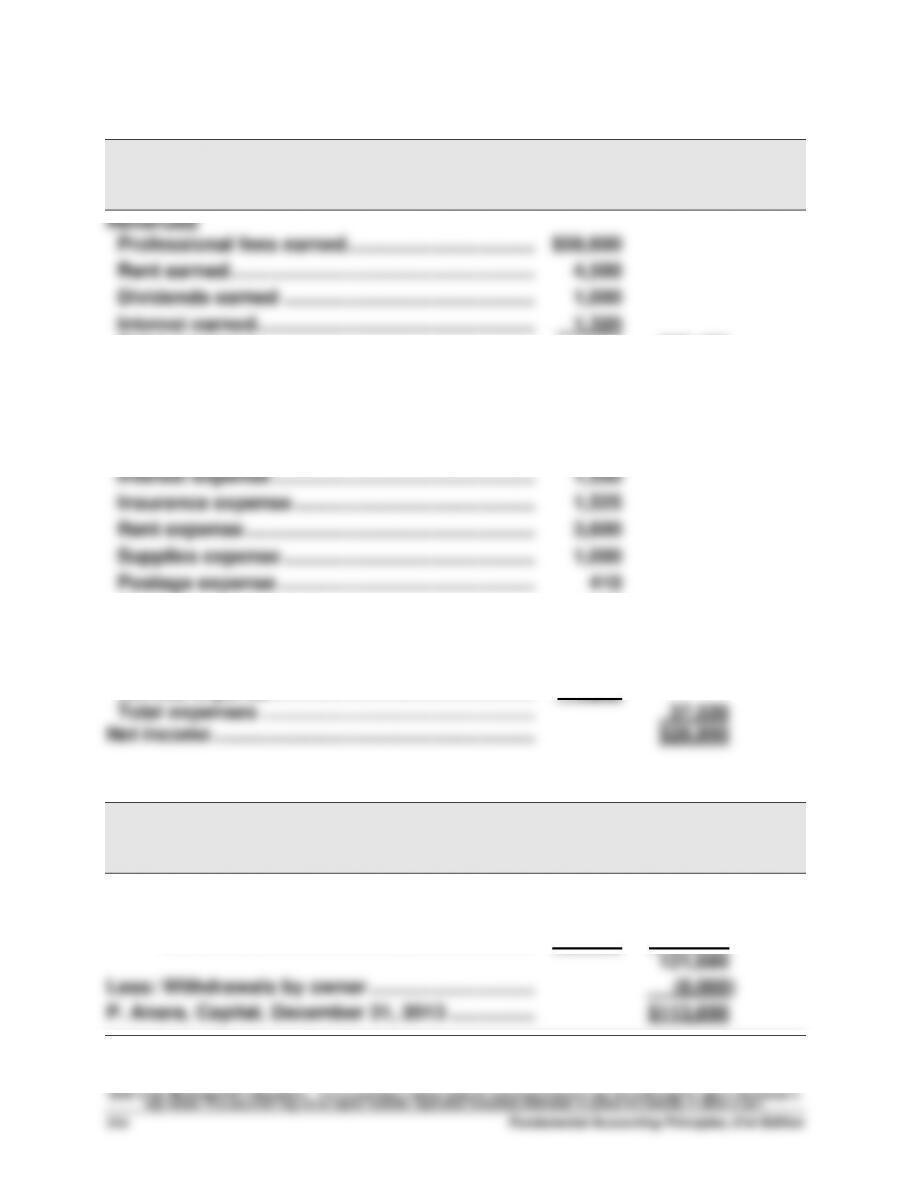

Part 3

POWER DEMOLITION COMPANY

Income Statement

For Year Ended April 30, 2013

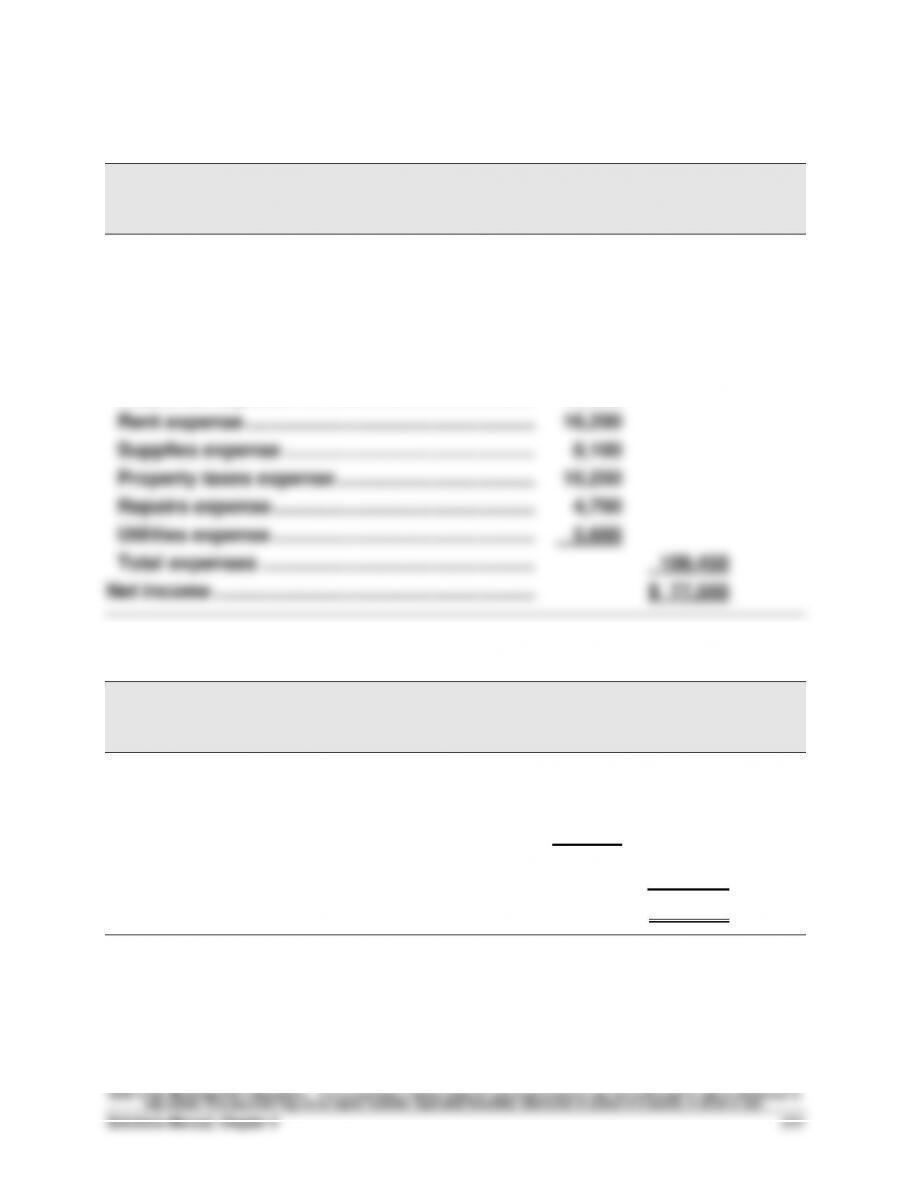

Demolition fees earned …………………………………. $187,000

Expenses

Depreciation expense–Equipment……………….. $ 7,000

Wages expense ………………………………………….. 43,400

Interest expense …………………………………………. 3,600

Insurance expense ……………………………………… 10,600

POWER DEMOLITION COMPANY

Statement of Owner’s Equity

For Year Ended April 30, 2013

J. Bonn, Capital, April 30, 2012 ……………………… $ 46,900

Add: Investments by owner ……………………….. $40,000

Net income ………………………………………… 77,550

117,550

Less: Withdrawals ………………………………………. (12,000)

J. Bonn, Capital, April 30, 2013 ……………………… $152,450

Problem 4-3B (Continued)

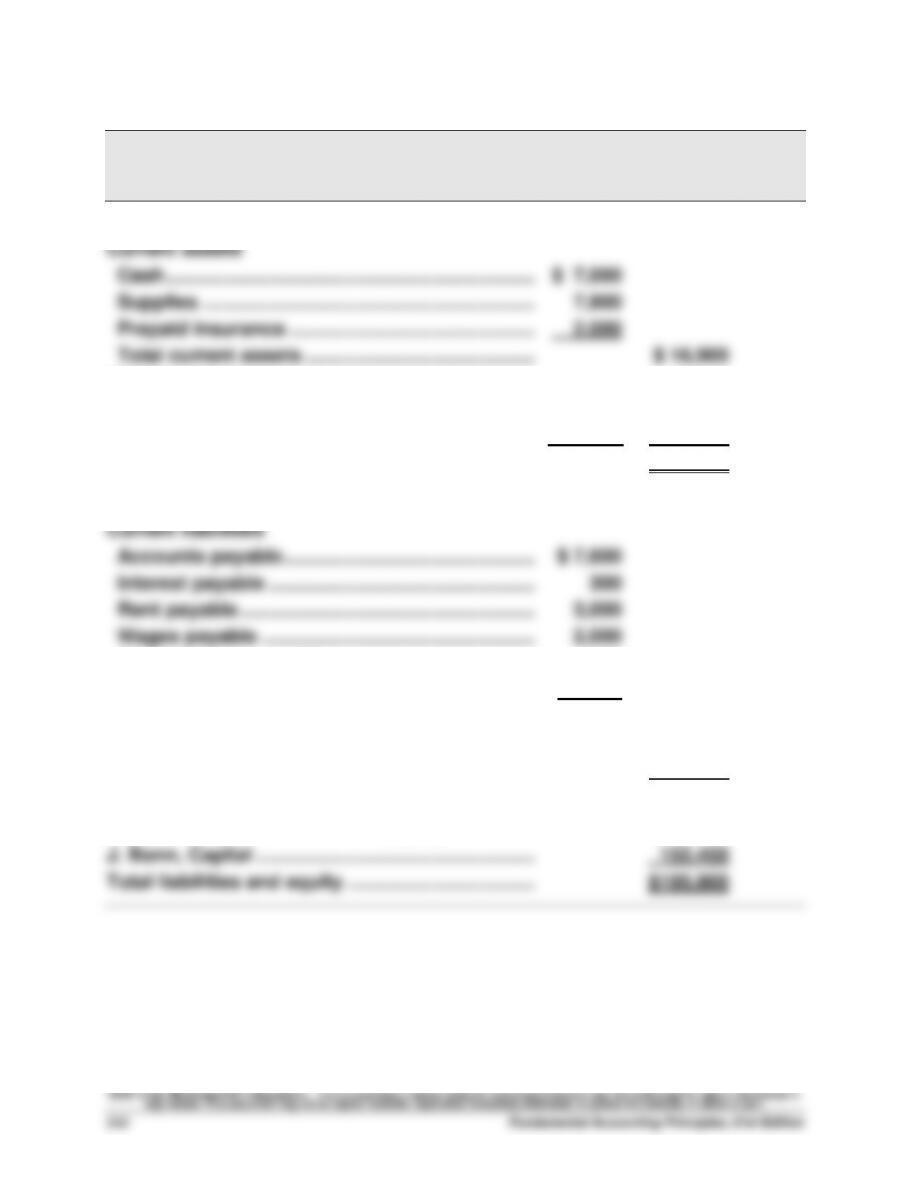

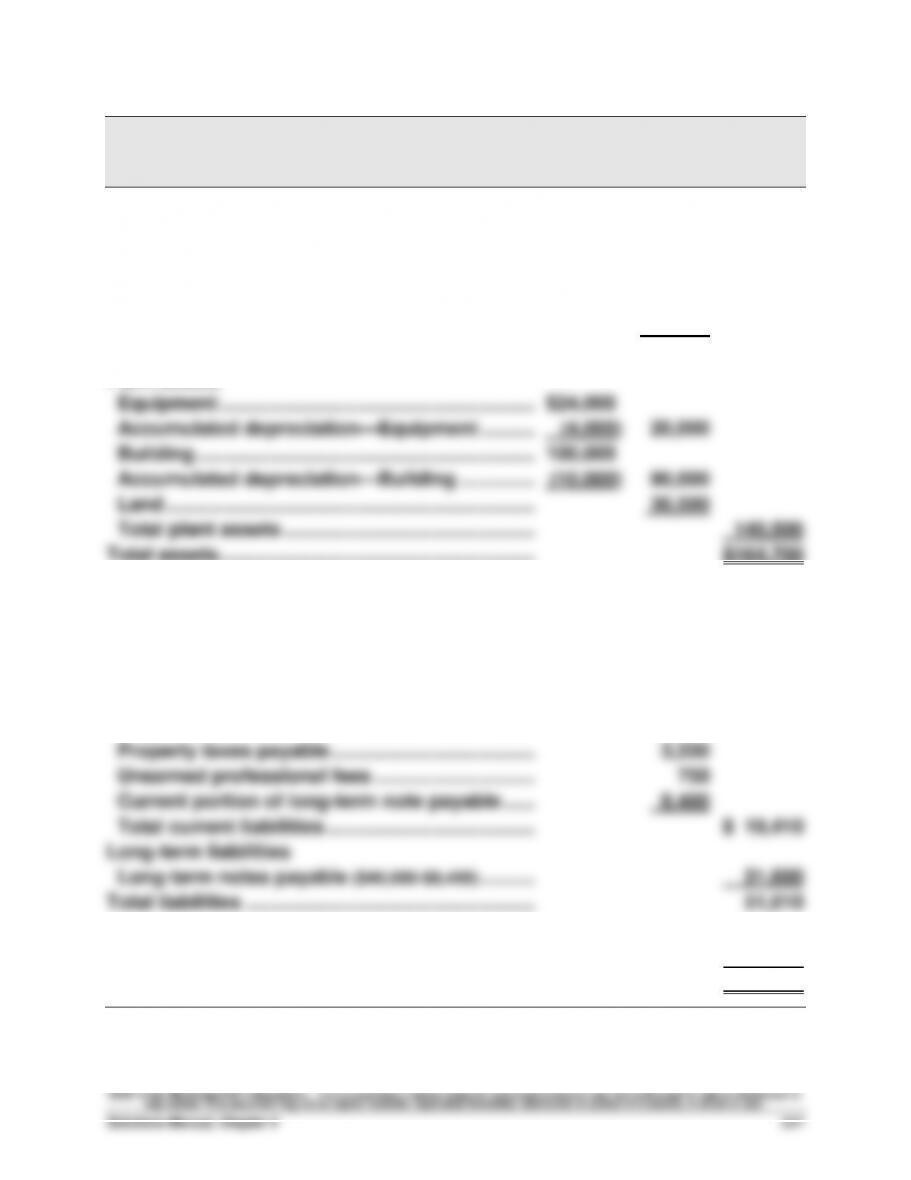

POWER DEMOLITION COMPANY

Balance Sheet

April 30, 2013

Assets

Plant assets

Equipment …………………………..……………………… 200,000

Accumulated depreciation–Equipment ………… (21,000) 179,000

Total assets ………………………………………………….. $195,900

Liabilities

Property taxes payable ……………………………….. 550

Current portion of long-term note payable …… 10,000

Total current liabilities ………………………………… $ 23,450

Long-term liabilities

Long-term note payable (less current portion) 20,000

Total liabilities ……………………………………………… 43,450

Equity

Problem 4-3B (Concluded)

Part 4

(a) This error enters the wrong amount in the correct accounts. The

ending balance of the Prepaid Insurance account should be $2,000,

but the entry reduces that account by $2,000. Because its

The adjusted trial balance columns in the work sheet will be equal,

but the error will cause the work sheet’s net income to be overstated

by $8,600 because of the understatement of the expense. In

the unexpired insurance and total equity by $8,600.

(b) This error inserts a debit in the balance sheet columns instead of the

income statement columns. In the unlikely event that this error is

omit the $4,700 expense for repairs.

In all likelihood, the error will be discovered in the process of

drafting the balance sheet because the accountant will realize that

repairs expense is not an asset. If it is detected and corrected, the

Problem 4-4B (90 minutes)

Part 1

SANTO COMPANY

Income Statement

For Year Ended December 31, 2013

Repair fees earned ………………………………. $54,700

Expenses

Depreciation expense—Equipment …….. $ 2,000

Wages expense …………………………………. 26,400

Insurance expense …………………………….. 600

SANTO COMPANY

Statement of Owner’s Equity

For Year Ended December 31, 2013

P. Santo, Capital, December 31, 2012 …… $35,650

Add: Net income …………………………..…….. 18,940

Problem 4-4B (Continued)

SANTO COMPANY

Balance Sheet

December 31, 2013

Assets

Current assets

Cash ………………………………………………….. $14,450

Store supplies ……………………………………. 5,140

Prepaid insurance ……………………………… 1,200

Total current assets …………………………... $20,790

Plant assets

Liabilities

Current liabilities

Accounts payable ………………………………. $ 1,500

Wages payable ………………………………….. 2,700

Total current liabilities ……………………….. 4,200

Equity

Problem 4-4B (Continued)

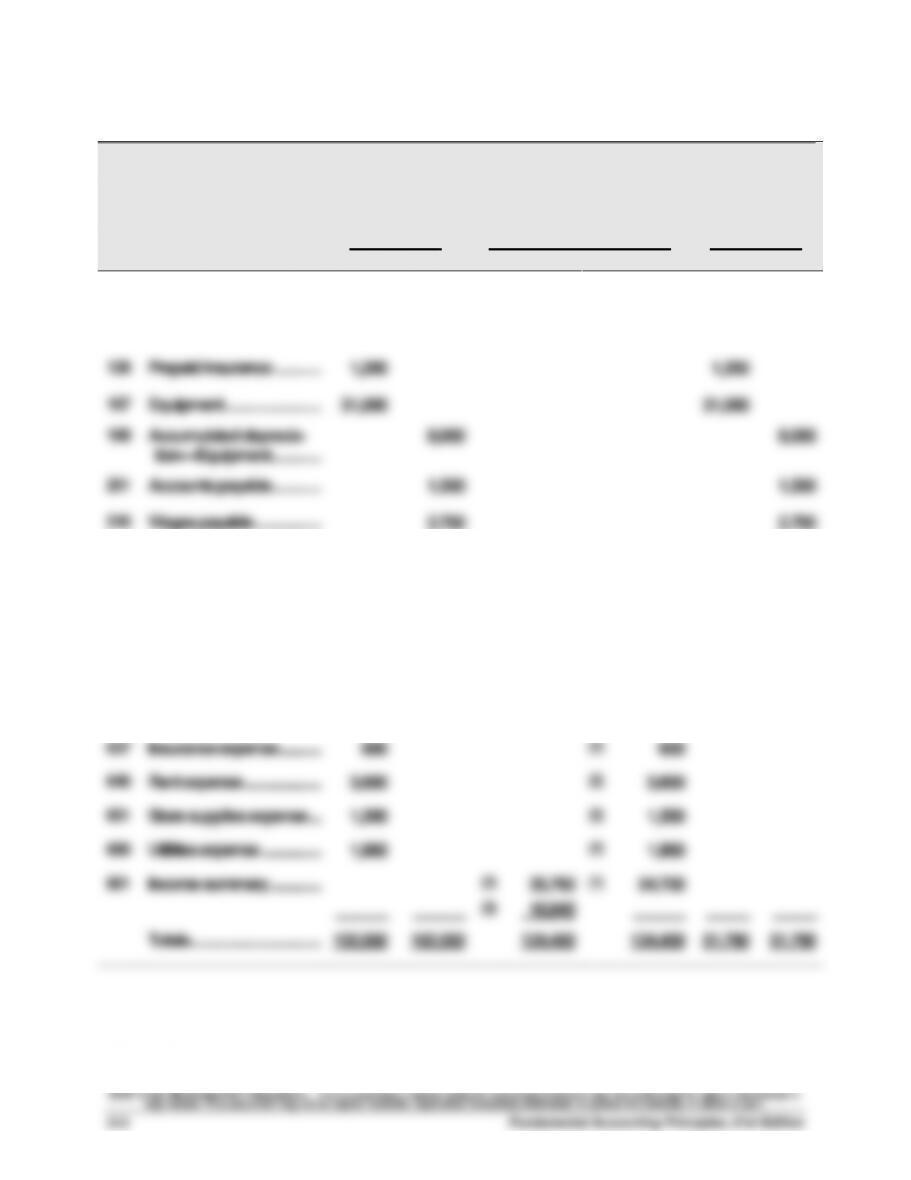

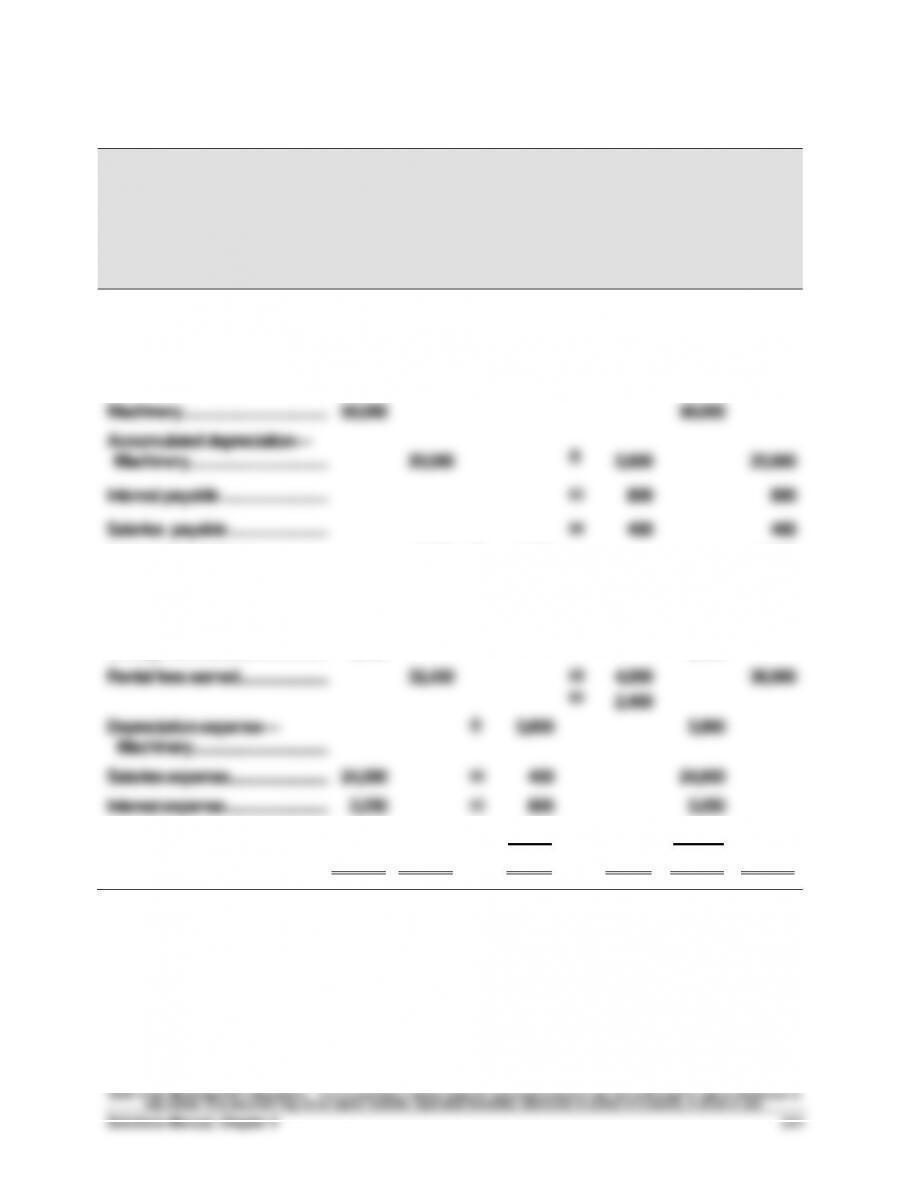

Parts 2 and 3

SANTO COMPANY

Work Sheet

For Year Ended December 31, 2013

Adjusted

Trial Balance

Closing Entry Information

Post–Closing

Trial Balance

No.

Account Title

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

101

Cash …………………………..……..…

14,450

14,450

125

Store supplies ………………….…

5,140

5,140

128

Prepaid insurance …………..…

1,200

1,200

167

Equipment ………………………..…

31,000

31,000

168

Accumulated deprecia–

tion—Equipment ………………

8,000

8,000

201

Accounts payable ………………

1,500

1,500

210

Wages payable ………………..…

2,700

2,700

301

P. Santo, Capital …………………

35,650

(4)

15,000

(3)

18,940

39,590

302

P. Santo, Withdrawals …….…

15,000

(4)

15,000

401

Repair fees earned ………….…

54,700

(1)

54,700

612

Depreciation expense—

Equipment …………………………

2,000

(2)

2,000

623

Wages expense ……………….…

26,400

(2)

26,400

637

Insurance expense ………….…

600

(2)

600

640

Rent expense …………………..…

3,600

(2)

3,600

651

Store supplies expense ….…

1,200

(2)

1,200

690

Utilities expense …………………

1,960

(2)

1,960

901

Income summary ………………

(2)

35,760

(1)

54,700

______

______

(3)

18,940

______

_____

_____

Totals……………………………………

102,550

102,550

124,400

124,400

51,790

51,790

Problem 4-4B (Concluded)

Part 3

Closing entries (all dated December 31, 2013)

Instructor note: Entries are shown without an account reference column because no posting is required.

(1) Repair Fees Earned ………………………………….. 54,700

Income Summary ………………………………. 54,700

To close the revenue account.

(2) Income Summary …………………………………….. 35,760

To close the expense accounts.

(3) Income Summary …………………………………….. 18,940

P. Santo, Capital………………………………… 18,940

To close the Income Summary account.

Part 4

(a) If none of the $600 insurance expense had expired, the income

statement would not report any insurance expense and net income

would be increased by $600.

Financial Statement Changes

The income statement would reflect the following:

• Net income would be increased by $600 + $2,700 = $3,300. (a) & (b)

The balance sheet would reflect the following:

Problem 4-5B (75 minutes)

Part 1

ANARA CO.

Income Statement

For Year Ended December 31, 2013

Total revenues ……………………………………………. $66,420

Expenses

Depreciation expense—Building …………………. 2,000

Depreciation expense—Equipment ……………… 1,000

Wages expense ………………………………………….. 18,500

Property taxes expense ………………………………. 4,825

Repairs expense …………………………..…………….. 679

Telephone expense …………………………………….. 521

Utilities expense …………………………………………. 1,920

ANARA CO.

Statement of Owner‘s Equity

For Year Ended December 31, 2013

P. Anara, Capital, December 31, 2012 ……………. $ 52,800

Add: Investments by owner …………………………. $40,000

Net income ………………………………………….. 28,890 68,890

Problem 4-5B (Continued)

ANARA CO.

Balance Sheet

December 31, 2013

Assets

Current assets

Cash …………………………………………………………… $ 7,400

Short-term investments ………………………………. 11,200

Supplies …………………………………………………….. 4,600

Prepaid insurance ………………………………………. 1,000

Total current assets ……………………………………. $ 24,200

Plant assets

Total assets ………………………………………………….. $164,700

Liabilities

Current liabilities

Accounts payable ……………………………………….. $ 3,500

Interest payable ………………………………………….. 1,750

Rent payable ………………………………………………. 400

Wages payable …………………………………………… 1,280

Equity

P. Anara, Capital …………………………..………………. 113,690

Total liabilities and equity …………………………….. $164,700

Problem 4-5B (Continued)

Part 2

Closing entries (all dated December 31, 2013)

Instructor note: Entries are shown without an account reference column because no posting is required.

(1) Professional Fees Earned ……………………… 59,600

Rent Earned …………………………..……………… 4,500

(2) Income Summary ………………………………….. 37,530

Depreciation Expense—Building …….. 2,000

Depreciation Expense—Equipment …. 1,000

Wages Expense………………………………. 18,500

Interest Expense …………………………….. 1,550

Insurance Expense …………………………. 1,525

Rent Expense …………………………………. 3,600

(3) Income Summary ………………………………….. 28,890

P. Anara, Capital …………………………….. 28,890

To close the Income Summary account.

Part 3

a. Return on assets = $28,890/[($160,000 + $164,700)/2] = 17.8% (or 0.178)

b. Debt ratio = $51,010/$164,700 = 0.31

Problem 4-6BA (40 minutes)

Part 1

SOLUTIONS CO.

Work Sheet

For Year Ended December 31, 2013

Unadjusted

Trial Balance

Adjustments

Adjusted

Trial Balance

Dr. Cr.

Dr. Cr.

Dr. Cr.

Cash ………………………………………………

10,000

10,000

Accounts receivable ……………………

(e)

2,450

2,450

Supplies ……………………………………..…

7,600

(b)

4,150

3,450

Machinery…………………………………..…

50,000

50,000

Accumulated depreciation—

Machinery ……………………………………

20,000

(f)

3,800

23,800

Interest payable …………………………..

(c)

800

800

Salaries payable ……………………….…

(a)

400

400

Unearned rental fees ………………..…

7,200

(d)

4,000

3,200

Notes payable ………………………………

30,000

30,000

G. Clay, Capital…………………………..

14,200

14,200

G. Clay, Withdrawals ………………..…

9,500

9,500

Rental fees earned …………………….…

32,450

(d)

(e)

4,000

2,450

38,900

Depreciation expense—

Machinery ………………………………..…

(f)

3,800

3,800

Salaries expense ……………………….…

24,500

(a)

400

24,900

Interest expense ………………………..…

2,250

(c)

800

3,050

Supplies expense ……………………..…

______

______

(b)

4,150

_____

4,150

______

Totals ………………………………………….…

103,850

103,850

15,600

15,600

111,300

111,300