5-1

CHAPTER 5

ACCOUNTING FOR MERCHANDISING OPERATIONS

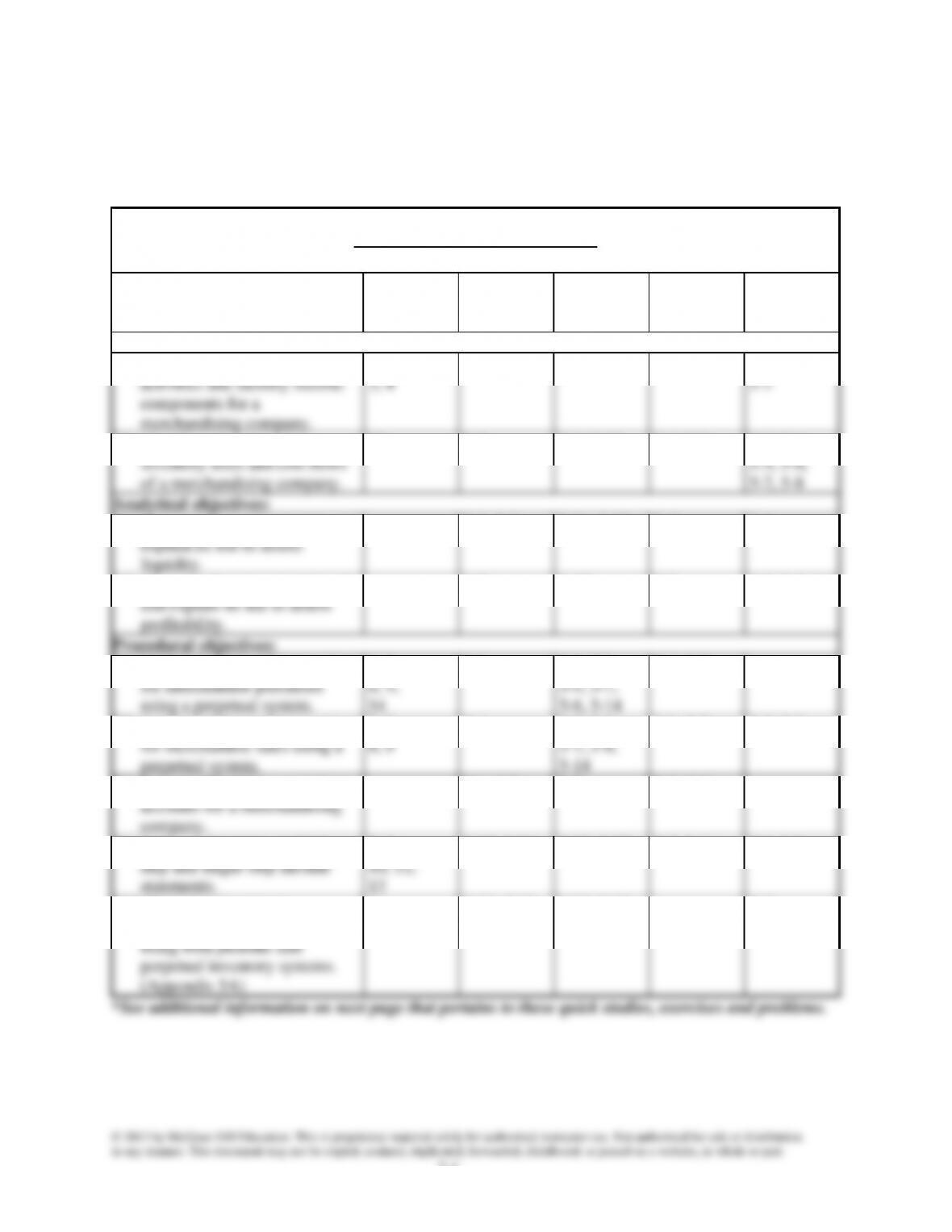

Related Assignment Materials

Student Learning Objectives

Questions

Quick

Studies*

Exercises*

Problems*

Beyond the

Numbers

Conceptual objectives:

C1. Describe merchandising

activities and identify income

components for a

merchandising company.

1, 2,

3, 4

5-1, 5-15

5-6, 5-10

5-3, 5-6,

5-7

C2. Identify and explain the

inventory asset and cost flows

of a merchandising company.

12

5-2

5-1, 5-10

5-4, 5-5

5-1, 5-4,

5-5, 5-6,

5-7, 5-8

Analytical objectives:

A1. Compute the acid-test ratio and

explain its use to assess

liquidity.

5-8, 5-9

5-11, 5-13

5-3

5-1

A2. Compute the gross margin ratio

and explain its use to assess

profitability.

5-5

5-12

5-3

5-2, 5-5, 5-9

Procedural objectives:

P1. Analyze and record transactions

for merchandise purchases

using a perpetual system.

6, 7,

8, 9,

14

5-3

5-2, 5-3,

5-4, 5-7,

5-8, 5-14

5-1, 5-2

P2. Analyze and record transactions

for merchandise sales using a

perpetual system.

5, 7

8, 9

5-4

5-3, 5-5,

5-7, 5-8,

5-14

5-1, 5-2

5-3, 5-4

P3. Prepare adjustments and close

accounts for a merchandising

company.

5-6, 5-7

5-9

5-3, 5-5

P4. Define and prepare multiple-

step and single-step income

statements.

2, 3,

10, 11,

13

5-10, 5-14

5-15, 5-20

5-3, 5-4

5-7, 5-9

P5A. Record and compare

merchandising transactions

using both periodic and

perpetual inventory systems.

(Appendix 5A)

5-11, 5-12,

5-13

5-16, 5-17,

5-18, 5-19

5-4

5-2

Additional Information on Related Assignment Material

The Serial Problem for Success Systems continues in this chapter. Problems 5-3A can be completed

using Excel. Problem 5-1A, 5-5A and the Serial Problem can be completed with Sage 50 Software or

QuickBooks.

Connect (Available on the instructor’s course-specific website) repeats all numerical Quick Studies, all

Exercises and Problems Set A. Connect provides new numbers each time the Quick Study, Exercise or

Problem is worked. It allows instructors to monitor, promote, and assess student learning. It can be used

in practice, homework, or exam mode.

Synopsis of Chapter Revisions

• Faithful Fish: NEW opener with new entrepreneurial assignment

• Enhanced exhibit on transportation costs and FOB terms, with inclusion of entries

• New discussion of online ordering, tracking numbers, RFID, and FOB

• Revised the two-step explanation of recording merchandise sales

• New discussion on the importance and risks of accounting for sales returns

• Revised visual display of a sales invoice

• Revised discussion of merchandising purchases and sales

• New Volkswagen example for IFRS income statement

Narrated PowerPoint Correlation Guide

Learning Objective

Slides

C1

2-4

C2

5-7

P1

8-21

P2

22-30

P3

31-32

P4

33-34

A1

37

A2

38-39

P5

40-42

Chapter Outline

Notes

I. Merchandising Activities

A. Merchandise consists of products, also called goods, that a

company acquires to resell to customers. Merchandisers can be

either wholesalers (those that buy from manufacturers or other

wholesalers and sell to retailers or other wholesalers) or retailers

(those that buy from wholesalers or manufacturers and sell to

consumers).

B. Reporting Income for a Merchandiser

Revenue from selling merchandise (net sales) minus the cost of

goods (merchandise) sold to customers is called gross profit.

Gross profit minus expenses (generally called operating expenses)

determines the net income or loss for the period.

C. Reporting Inventory for a Merchandiser

A merchandiser’s balance sheet is the same as service businesses

with the exception of one additional current asset called:

1. Merchandise Inventory, or Inventory, refers to products a

company owns and intends to sell.

2. The cost of this asset includes the cost incurred to buy the

goods, ship them to the store, and make them ready for sale.

D. Operating Cycle for a Merchandiser

Begins by purchasing merchandise and ends by collecting cash

from selling the merchandise.

E. Inventory Systems

Two alternative inventory systems that can be used to collect

information about the cost of goods sold and the inventory (cost of

goods available) are:

1. Perpetual inventory system which continually updates

accounting records for merchandising transactions—

specifically, those records of inventory available for sale and

inventory sold. Technological advances and competitive

pressures have dramatically increased the use of this method.

2. Periodic inventory system which updates the accounting

records for merchandise transactions only at the end of a

period.

Note: This outline describes the accounting using a Perpetual

Inventory System. Periodic Inventory is only discussed in the

appendix section of this outline. Also note, the terms inventory

Chapter Outline

Notes

II. Accounting for Merchandise Purchases

The invoice serves as a source document for this event.

A. Trade Discounts

Deductions from list price (catalog price) to arrive at invoice price

(actual selling price). Trade discounts are not entered into

accounts.

1. Transactions are recorded using invoice price.

2. Entry to record purchase: debit Inventory, credit Cash or

Accounts Payable.

B. Purchase Discounts

Credit terms describe cash discounts offered to purchasers by

seller for payment within a specified period of time called the

discount period. Buyers view cash discounts as purchase

discounts and sellers view them as sales discounts.

1. Example: credit terms, 2/10 n/30, offer a 2 % discount if

invoice is paid within 10 days of invoice date, if not full

payment is due within 30 days of invoice date.

2. Entry (for buyer) for payment within discount period: debit

Accounts Payable (full invoice amount), credit Cash (amount

paid = invoice – discount), credit Inventory (amount of

discount).

C. Managing Discounts

Missing out on cash discounts can be very costly. A system

should be set-up to ensure that all invoices are paid on the last day

of discount period.

D. Purchase Returns and Allowances

1. Purchase returns refers to merchandise a buyer acquires but

then returns to the seller.

2. A purchase allowance is a reduction in the cost of defective

merchandise that a buyer acquires.

3. A debit memorandum is a document that a buyer issues to

inform the seller of a debit made to the seller’s account in the

buyers records.

4. Entry on buyer’s books: debit Accounts Payable or Cash (if

refund given) and credit Inventory.

E. Discounts and Returns

Discounts can only be taken on the remaining balance on the

invoice after the return.

F. Transportation Costs and Ownership Transfer

The point at which ownership is transferred (called FOB or free on

board) determines who is responsible for paying any freight costs

and/or bearing any loss. Two alternative points of title transfer

are:

Chapter Outline

Notes

1. FOB shipping point—title transfers at shipping point and

buyer bears any loss and pays shipping costs.

a. Increases cost of merchandise (cost principle)

b. Debit Inventory, credit Cash or Accounts Payable (if to be

paid for with merchandise later)

2. FOB destination—title transfers at destination and seller bears

any loss and pays shipping costs.

a. Operating expense for seller

b. Debit Delivery Expense (or Transportation-Out or Freight-

Out), credit Cash.

G. Recording Purchases Information

The net cost of purchased merchandise according to the cost

principle is recorded in the inventory account. (Inventory is

debited, or increased, for invoice and transportation costs, and

credited, or reduced, for returns, allowances, and discounts.

Supplemental records are often used to collect information about

each of the cost elements for management to evaluate and control.

III. Accounting for Merchandise Sales—involves sales, sales discount,

sales returns and allowances and cost of goods sold

A. Each sale of merchandise transaction involves two parts (resulting

in two journal entries; the revenue entry and the cost entry.

1. Recognize revenue—debit Accounts Receivable (or cash),

credit Sales (both for the invoice amount).

2. Recognize cost—debit Cost of Goods Sold, credit Inventory

(both for the cost of the inventory sold).

B. Sales Discounts

Cash discounts awarded to customers for payment within the

discount period. Recorded upon collection for sale.

1. Collection after discount period—Debit Cash, Credit Accounts

Receivable (full invoice amount).

2. Collection within discount period—debit Cash (invoice

amount less discount), debit Sales Discount (discount

amount), credit Accounts Receivable (invoice amount).

3. Sales Discounts is a contra-revenue account—subtraction

from Sales.

C. Sales Returns and Allowances

1. Sales returns—merchandise that a customer returned to the

seller after a sale.

2. Sales allowances—reductions in the selling price of

merchandise sold to customers (usually for damaged

merchandise that a customer is willing to keep at a reduced

price).

Chapter Outline

Notes

3. Entry: debit Sales Returns and Allowances and credit

Accounts Receivable; additional entry to restore cost of

returned goods to inventory if merchandise is returned and it is

salable: debit Inventory, credit Cost of Goods Sold.

4. Sales Returns and Allowances is a contra-revenue account that

is subtracted from Sales.

5. Net Sales = Sales – (Sales Discount + Sales Returns and

Allowances).

6. Credit Memorandum—document issued by the seller to

confirm a buyer’s return or allowance and the credit to

Accounts Receivable on the seller’s books.

IV. Completing the Accounting Cycle

A. Adjusting Entries for Merchandisers

Generally same as discussed in chapter 4 for a service business

with an additional adjustment needed to update inventory to reflect

any loss referred to as shrinkage.

1. Shrinkage is determined by comparing a physical count of the

inventory with recorded quantities.

2. Adjusting entry: debit Cost of Goods Sold, credit Inventory.

B. Preparing Financial Statements

Statements similar to service business with the following

differences:

1. Income Statement includes the cost of goods sold and gross

profit. Also, net sales is affected by discounts, returns, and

allowances and delivery expense as an additional possible

expense.

2. Balance Sheet includes merchandise inventory as part of

current assets.

C. Closing Entries

Similar to a service business except there are additional temporary

accounts to close (sales, sales discount, sales returns and

allowances, and cost of goods sold). Debit balance accounts are

closed with the expense accounts to Income Summary.

V. Financial Statement Formats—GAAP does not require any specific

format. Common formats:

A. Multiple-Step Income Statement—shows details of net sales and

other costs and expenses. Has three main parts:

1. Gross profit—net sales less cost of goods sold.

2. Income from operations—gross profit less operating expenses

(classified into selling and general & administrative).

Chapter Outline

Notes

B. Single-Step Income Statement

Lists cost of goods sold as another expense and shows only one

subtotal for total expenses, one subtraction to arrive at net income.

C. Classified Balance Sheet—reports merchandise inventory as a

current asset, usually after accounts receivable (use liquidity

order).

VI. Global View—Compares U.S.GAAP to IFRS

A. Accounting for Merchandise Purchases and Sales—both systems

are identical in and account as illustrated in this chapter.

B. Income Statement Preparation—IFRS tends to use the term profit

whereas U.S. GAAP tends to use net income. Presentation is

similar through CGS, followed by these difference:

1. Expense presentation—IFRS requires separate disclosures for

financing expenses, income tax, and some other special items.

2. IFRS permits expense presentation by function or nature;

GAAP has SEC requirement of presentation by function.

3. IFRS permits alternative measures of income on statement;

GAAP does not.

C. Balance Sheet Presentation—same as discussed in chapter 2 & 3.

VII. Decision Analysis—Acid Test Ratio and Gross Margin Ratio

A. Acid-Test Ratio

1. Used to assess the company‘s liquidity or ability to pay its

current debts. Differs from current ratio in that it is based on

quick assets (which excludes less liquid current assets such as

inventory and prepaid expenses) rather than all current assets.

2. Calculated by dividing quick assets by current liabilities.

3. Quick assets are cash, short-term investments, and receivables.

B. Gross Margin Ratio

1. Used to determine the percent of every sales dollar that is

gross profit.

2. Calculated by dividing gross margin by net sales.

5-8

VIII. Periodic Inventory System (Appendix 5A)—textbook show

comparison of periodic and perpetual in this appendix. The

following chapter notes relate only to the periodic system because

the preceding notes outline the perpetual system.

A. A periodic inventory system records merchandise acquisitions,

discounts and returns in temporary accounts (Purchases, Purchase

Returns, Purchases Discounts) rather than the merchandise

inventory account.

B. Records only the revenue aspect of sales related events. Updates

inventory and determines cost of goods sold only at the end or the

accounting period. During the period, inventory account remains

unchanged.

C. The inventory account can be updated as part of the adjusting or

closing process.

D. Requires closing additional temporary accounts.

5-9

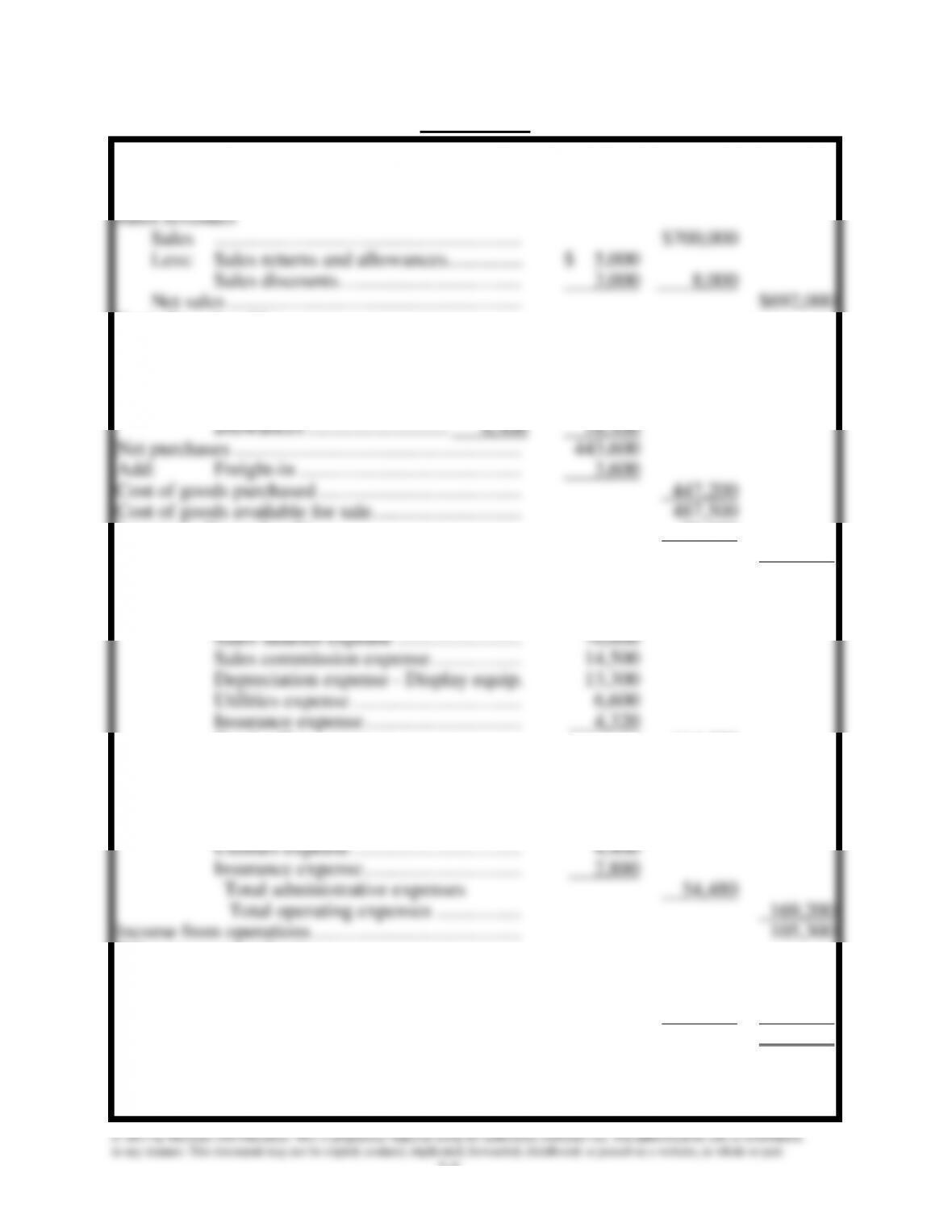

VISUAL #5-1

THE OUTDOOR STORE

Income Statement

For the Year Ended December 31, 20xx

Sales revenues

Sales ………………………………………..

$700,000

Less: Sales returns and allowances. …………..

$ 5,000

Sales discounts ……………………….

3,000

8,000

Net sales ………………………………………

$692,000

Cost of goods sold

Inventory, January 1 ………………………….

40,300

Purchases ……………………………………..

462,000

Less: Purchase discounts ……….. $12,000

Purchase returns and

allowances ………………………. 6,400

18,400

Net purchases ……………………………………..

443,600

Add: Freight-in …………………………….

3,600

Cost of goods purchased ………………………….

447,200

Cost of goods available for sale …………………..

487,500

Inventory, December 31…………………………..

70,000

Cost of goods sold ……………………

417,500

Gross profit on sales ………………………………

274,500

Operating expenses

Selling expenses

Sales salaries expense ……………….

76,000

Sales commission expense …………..

14,500

Depreciation expense – Display equip.

13,300

Utilities expense ……………………..

6,600

Insurance expense ……………………

4,320

Total selling expenses ……………….

114,720

Administrative expenses

Office salaries expense ………………

32,000

Depreciation expense – building …….

10,400

Property tax expense …………………

4,800

Utilities expense ……………………..

4,400

Insurance expense ……………………

2,880

Total administrative expenses

54,480

Total operating expenses ………….

169,200

Income from operations …………………………..

105,300

Other revenues and gains

Interest revenue ………………………………

4,000

Other expenses and losses

Interest expense ………………………………

11,000

7,000

Net income ………………………………………..

$ 98,300

5-10

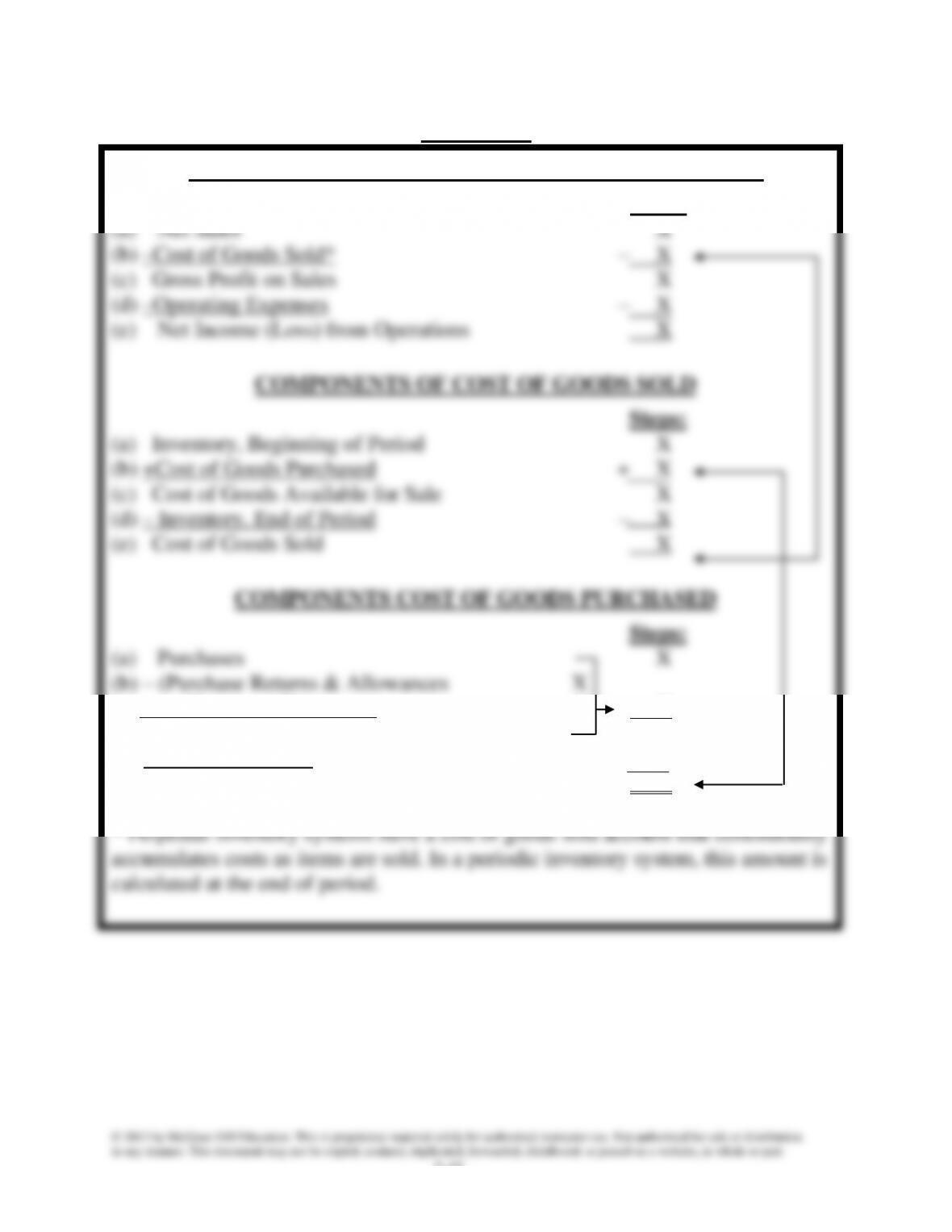

VISUAL #5-2

COMPONENTS OF NET INCOME (FROM OPERATIONS)

Steps:

+ Purchases Discounts) + X – X

(c) Net Purchases X

(d) + Transportation In + X

(e) Cost of Goods Purchased X

5-11

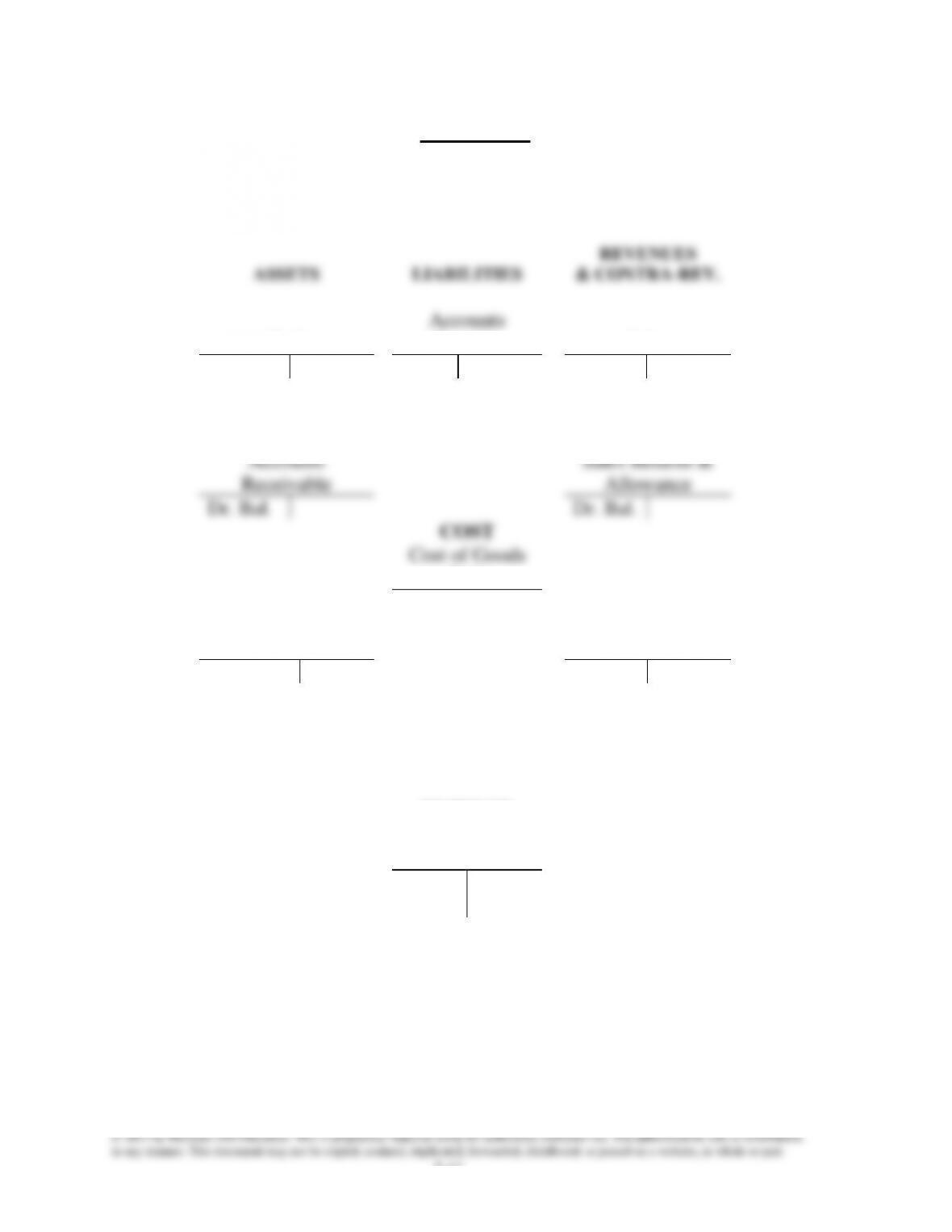

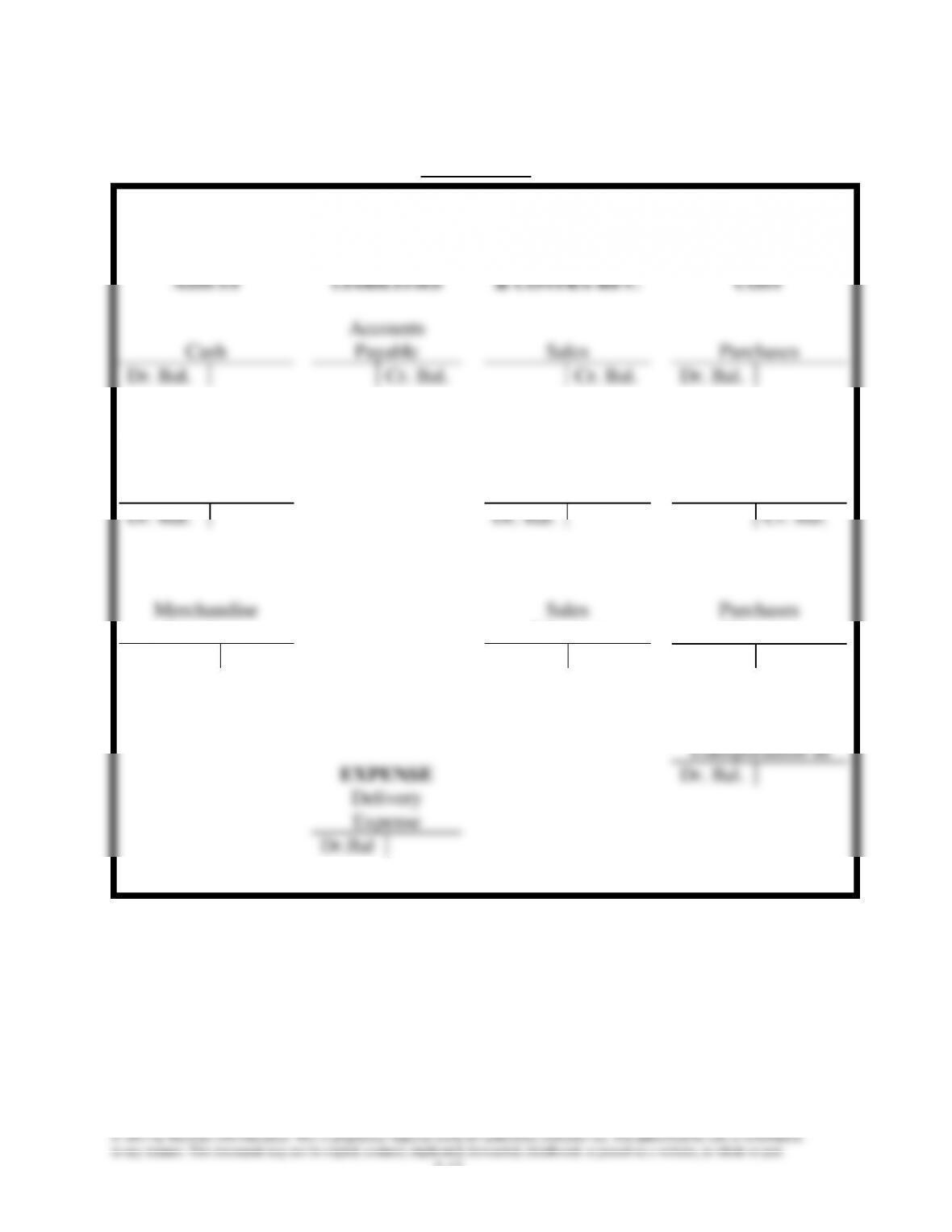

VISUAL #5-3

ACCOUNTS USED IN BASIC MERCHANDISING TRANSACTIONS

WITH A PERPETUAL INVENTORY SYSTEM

ASSETS

LIABILITIES

REVENUES

& CONTRA-REV.

Cash

Accounts

Payable

Sales

Dr. Bal.

Cr. Bal.

Cr. Bal.

Accounts

Receivable

Sales Returns &

Allowance

Dr. Bal.

Dr. Bal.

COST

Cost of Goods

Sold

Dr. Bal.

Merchandise

Inventory

Sales

Discount

Dr. Bal.

Dr. Bal.

EXPENSE

Delivery

Expense

Dr.

Bal.

5-12

VISUAL #5-4

ACCOUNTS USED IN BASIC MERCHANDISING TRANSACTIONS

WITH A PERIODIC INVENTORY SYSTEM

ASSETS

LIABILITIES

REVENUES

& CONTRA-REV.

COST & CONTRA-

COST

Cash

Accounts

Payable

Sales

Purchases

Dr. Bal.

Cr. Bal.

Cr. Bal.

Dr. Bal.

Accounts

Receivable

Sales Returns &

Allowance

Purchase Returns

& Allowances

Dr. Bal.

Dr. Bal.

Cr. Bal.

Merchandise

Inventory

Sales

Discount

Purchases

Discount

Dr. Bal.

Dr. Bal.

Cr. Bal.

Transportation–In

EXPENSE

Dr. Bal.

Delivery

Expense

Dr.Bal

5-13

Alternate Demonstration Problem

Chapter Five

The following data was taken from ledger account balances and

supplementary data for the Whisk Company.

Merchandise inventory, beginning …………………………………………

$ 20,000

Merchandise inventory, ending ……………………………………………..

23,000

Purchases …………………………………………………………………………….

215,000

Purchases discounts …………………………………………………………….

6,000

Purchases returns and allowances …………………………..……………

3,000

Sales …………………………………………………………………………………….

400,000

Sales discounts …………………………………………………………………….

3,200

Sales returns and allowances ………………………………………………..

1,800

Transportation-in …………………………………………………………………..

10,000

Required:

Show the computation, in Income Statement format, of net sales, cost of

goods sold, and gross profit for the year ended December 31, 20XX.

5-14

Solution: Alternate Demonstration Problem

Chapter Five

WHISK COMPANY

Income Statement

For the Year Ended December 31, 20XX

Revenue from sales:

Sales …………………………………..

$400,000

Less: Sales discounts ………….

$ 3,200

Sales returns and

allowances ……………..

1,800

5,000

Net sales ……………………………..

395,000

Cost of goods sold:

Merchandise inventory, 1/1/XX

20,000

Purchases …………………………..

$215,000

Less: Purchase discounts ……

$6,000

Purchases returns and

allowances ……………..

3,000

9,000

Net purchases ……………………..

206,000

Add transportation–in …………..

10,000

Cost of goods purchased …….

216,000

Goods available for sale ………

236,000

Merchandise inventory, 12/31/XX

23,000

Cost of goods sold ………………….

213,000

Gross profit from sales ……………

$182,000