Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

22-1

CHAPTER 22

MASTER BUDGETS AND PLANNING

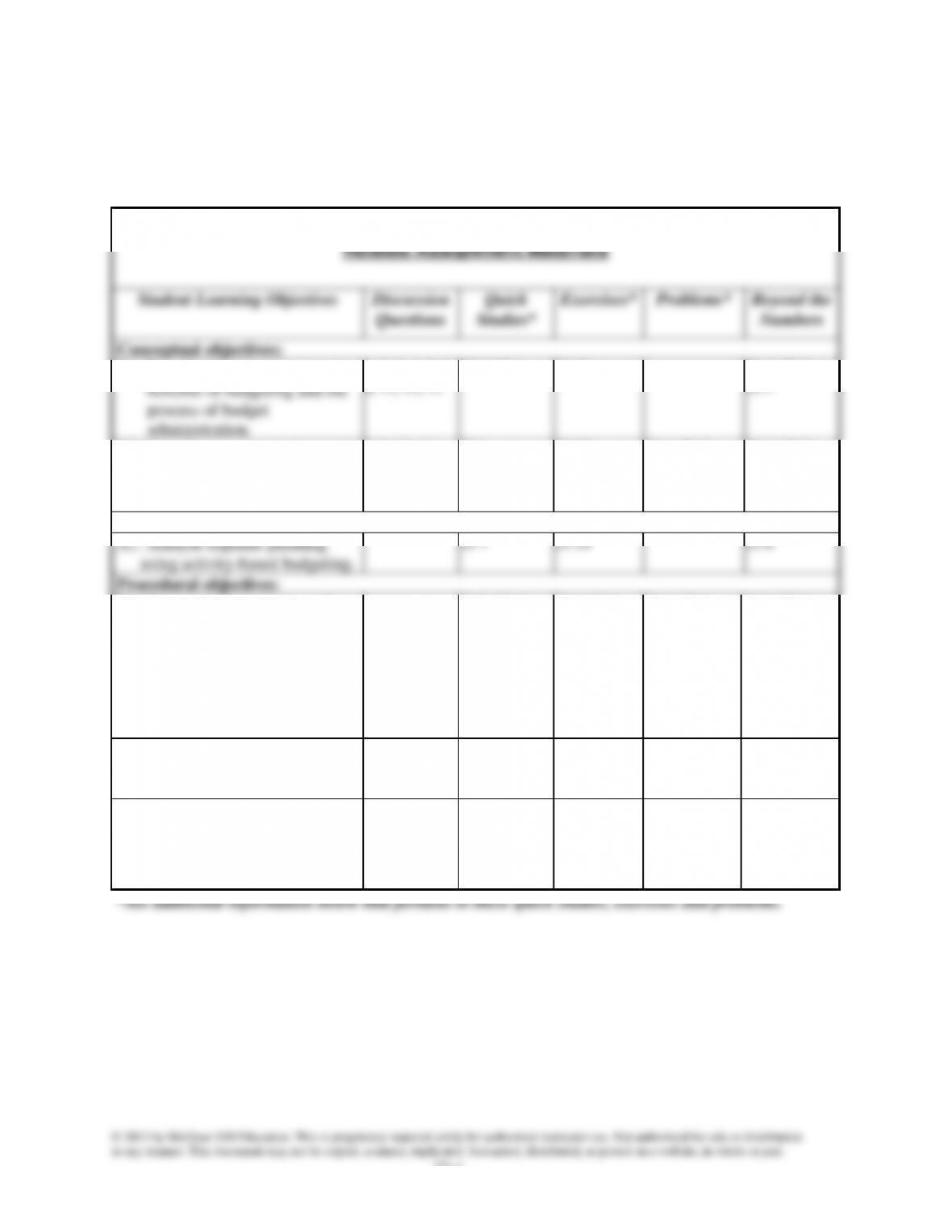

Related Assignment Materials

Student Learning Objectives

Discussion

Questions

Quick

Studies*

Exercises*

Problems*

Beyond the

Numbers

Conceptual objectives:

C1. Describe the importance and

benefits of budgeting and the

process of budget

administration.

1, 2, 3, 4, 5, 6,

9, 12, 13, 14

22-2, 22-4

22-23

22-3, 22-5,

22-7

C2. Describe a master budget and

the process of preparing it.

7, 8, 10, 11

22-1

22-22

22-1, 22-2,

22-3, 22-4,

22-5, 22-6,

22-7

22-4, 22-8

Analytical objectives:

A1. Analyze expense planning

using activity-based budgeting.

22-7

22-24

22-6

Procedural objectives:

P1. Prepare each component of a

master budget and link each to

the budgeting process.

22-3, 22-6,

22-10, 22-11,

22-12, 22-14,

22-15, 22-16,

22-17, 22-18,

22-19, 22-23,

22-24, 22-25,

22-26- 22-27

22-1, 22-2,

22-3, 22-5,

22-6, 22-7,

22-11, 22-12,

22-13, 22-14,

22-15, 22-16

22-1, 22-5,

22-7

22-8, 22-9

P2. Link both operating and capital

expenditures budgets to

budgeted financial statements.

22-5, 22-13

22-4, 22-7,

22-17, 22-18

22-2, 22-3,

22-4, 22-5,

22-7,

22-1, 22-2

P3 Prepare production and

manufacturing budgets.

(Appendix 22A)

11

22-8, 22-9,

22-20, 22-21,

22-22

22-8, 22-9,

22-10, 22-19,

22-20, 22-21,

22-25, 22-26,

22-27, 22-28

22-6, 22-7

22-2

Additional Information on Related Assignment Material

Connect (Available on the instructor’s course-specific website) repeats all numerical Quick Studies, all

Exercises and Problems Set A. Connect provides new numbers each time the Quick Study, Exercise or

Problem is worked. It allows instructors to monitor, promote, and assess student learning. It can be used

in practice, homework, or exam mode.

Corresponding problems in set B also relate to learning objectives identified in grid on previous page.

Problems 22-1A and 22-2A can be completed using EXCEL. The Serial Problem for Success Systems

starts in this chapter and continues throughout many chapters of the text. It is most readily solved

manually if you use the working papers that accompany text.

Narrated PowerPoint Correlation Guide

Learning Objective

Slides

C1

2-5

C2

6

P1

7-17

P2

18-36

A1

38

P3

39-42

Synopsis of Chapter Revision

• Freshii: NEW opener with new entrepreneurial assignment

22-3

Chapter Outline

I. Budget Process⎯Process of planning future business activities.

A. Strategic Budgeting

1. Budget⎯Formal statement of a company’s future short term

financial plans.

2. All managers should be involved.

3. Relevant focus of budgeting analysis is future.

4. Focus on future is important because daily operations may

divert management’s attention from planning.

5. Good budgeting system formalizes planning process and

demands relevant input; makes planning an explicit

management responsibility.

B. Benchmarking Budgets

1. Control function requires management to evaluate

(benchmark) business operations against some norm.

2. Evaluation involves comparing actual results against:

3. Evaluation assists management in identifying problems and

taking corrective actions if necessary.

4. Evaluation using expected performance is usually superior to

using past performance when deciding if actual results trigger

may affect current and future activities.

i. Changes in economic conditions.

ii. Shifts in competitive advantages within the industry.

iii. New product developments.

iv. Increased or decreased advertising.

v. Technological advances and innovations.

(participatory budgeting).

Notes

22-4

Chapter Outline

b. Budgeted levels of performance must be realistic (goals

must be attainable) to avoid discouraging employees.

c. Evaluation should be made carefully and allow affected

employees to explain reasons for apparent performance

deficiencies.

3. Management must be aware of negative outcomes

a. Employees may understate the sales budget and/or

overstate the expense budget to allow a budgetary slack in

unnecessary times to make sure their budgets are not

reduced in the next period

D. Budgeting as a Management Tool

1. Activities of all departments should contribute to meeting

2. Informal communication of business plans can create

uncertainty and confusion.

A. Budget Committee

1. Without active employee involvement, risk that employees

will feel as if budget fails to reflect their special problems and

needs.

2. Budget figures and estimates more useful if developed through

bottom-up process.

helps to ensure budgeted amounts are realistic and

coordinated.

figures that do not reflect efficient performance; originating

department should justify or adjust figures.

5. Ongoing communication should continue to ensure all parties

accept budget as reasonable, attainable, and desirable.

Notes

Chapter Outline

B. Budget Reporting

1. Usually coincides with the accounting period

2. Most companies prepare annual budgets; usually separated

into monthly or quarterly budgets.

3. Short-term budgets allow quick performance evaluation and

corrective action; reports compare actual results to budgets.

4. Variances are differences between actual and budgeted

amounts; management examines variances to identify areas for

improvement.

C. Budget Timing - Many companies apply continuous budgeting by

preparing rolling budgets; as each budget period passes:

1. New monthly or quarterly budgets are prepared to replace

those that have lapsed.

2. Entire set of budgets for months or quarters that remain is

III. The Master Budget⎯Formal, comprehensive plan for a company’s

future.

A. Master Budget Components

1. Contains several individual budgets that are linked with each

other to provide a coordinated plan for the company.

2. Typically includes individual budgets for sales, purchases or

other budgets are complete.

4. Undesirable outcomes might be revealed at any stage in

budgeting process; changes must be made to prior budgets and

previous steps repeated.

B. Operating Budgets⎯Four major types.

1. Sales budget

a. First step in preparing master budget.

c. Participatory budgeting approach ensures greater

commitment to goals, and draws on knowledge and

experience of people involved in activity.

d. More detailed than simple projections of total sales;

includes forecasts of both units sales and unit prices for

Notes

22-6

Chapter Outline

2. Merchandise Purchases Budget (Production and

Manufacturing Budgets in Appendix 22A)

a. Whether company manufacturers or purchases product

sold, budgeted future sales volume is primary factor in

inventory management decisions.

b. Budgets for just-in-time inventory systems cover short

periods to order just enough merchandise or materials to

satisfy immediate sales demand; inventory is held to a

minimum (zero in ideal situations).

c. Other companies keep enough inventory on hand to

reduce risk of running short (called safety stock); provides

protection against lost sales caused by unfulfilled

customer demands or delays in shipments from suppliers.

Expected unit sales

+ Budgeted ending inventory units

Total inventory units required

- Budgeted beginning inventory units

Inventory units to be purchased

Budgeted cost of merchandise purchases

e. Manufacturers (Appendix 22A) ⎯A manufacturer will

prepare a production budget instead of a purchases budget.

Sales budget used as basis for production budget.

i. Units to be produced is determined by:

Expected unit sales

manufacturing budgets.

Notes

Chapter Outline

iii. Direct Materials Budget:

Units to be produced

x Material requirements per unit

Materials needed for production

+ Desired ending inventory of direct materials

Total required materials

- Beginning inventory of direct materials

Direct materials to be purchased

x Materials price per unit of materials

a. Plan listing the type and amounts of selling expenses

expected during budget period.

b. Created to provide sufficient selling expenses to meet

sales goals reflected in sales budget.

4. General and Administrative Expense Budget

a. Plan showing predicted operating expenses not included in

selling expenses budget.

planned at this stage of budgeting process.

C. Capital Expenditures Budget

Notes

Chapter Outline

3. Capital budgeting is process of evaluating and planning for

capital (plant and equipment) expenditures, which involve

long-run commitments of large amounts.

4. Major effect on predicted cash flows and company’s need for

debt or equity financing; often linked with company’s ability

to take on more debt.

D. Financial Budgets

during budget period

Total available cash

- Budgeted cash expenditures

Preliminary cash balance

a. May include planned receipts from short-term loans (if

expected preliminary cash balance is inadequate), or use

v. Expected cash payments on accounts payable.

vi. Other expected cash payments such as owner’s

withdrawals or dividends, repayment of notes, etc

2. Budgeted Income Statement

Notes

22-9

Chapter Outline

3. Budgeted Balance Sheet

a. Final step in preparing master budget.

b. Shows predicted amounts for assets, liabilities, and

stockholders’ equity as of end of budget period.

c. Prepared using information from other budgets (see notes

to budgeted balance sheet for sources of amounts).

IV. Decision Analysis—Activity-Based Budgeting (ABB)-–-budget

system based on expected activities.

A. Traditional budgets are based on figures from previous year,

adjusted for changes in operating conditions.

B. Activity-based budgeting requires management to list activities

and to understand the resources required to perform these

activities.

1. Helps management assess how much expenses will increase

with increases in activity levels.

2. Helps management reduce costs by eliminating non-value-

added activities.

Notes

22-10

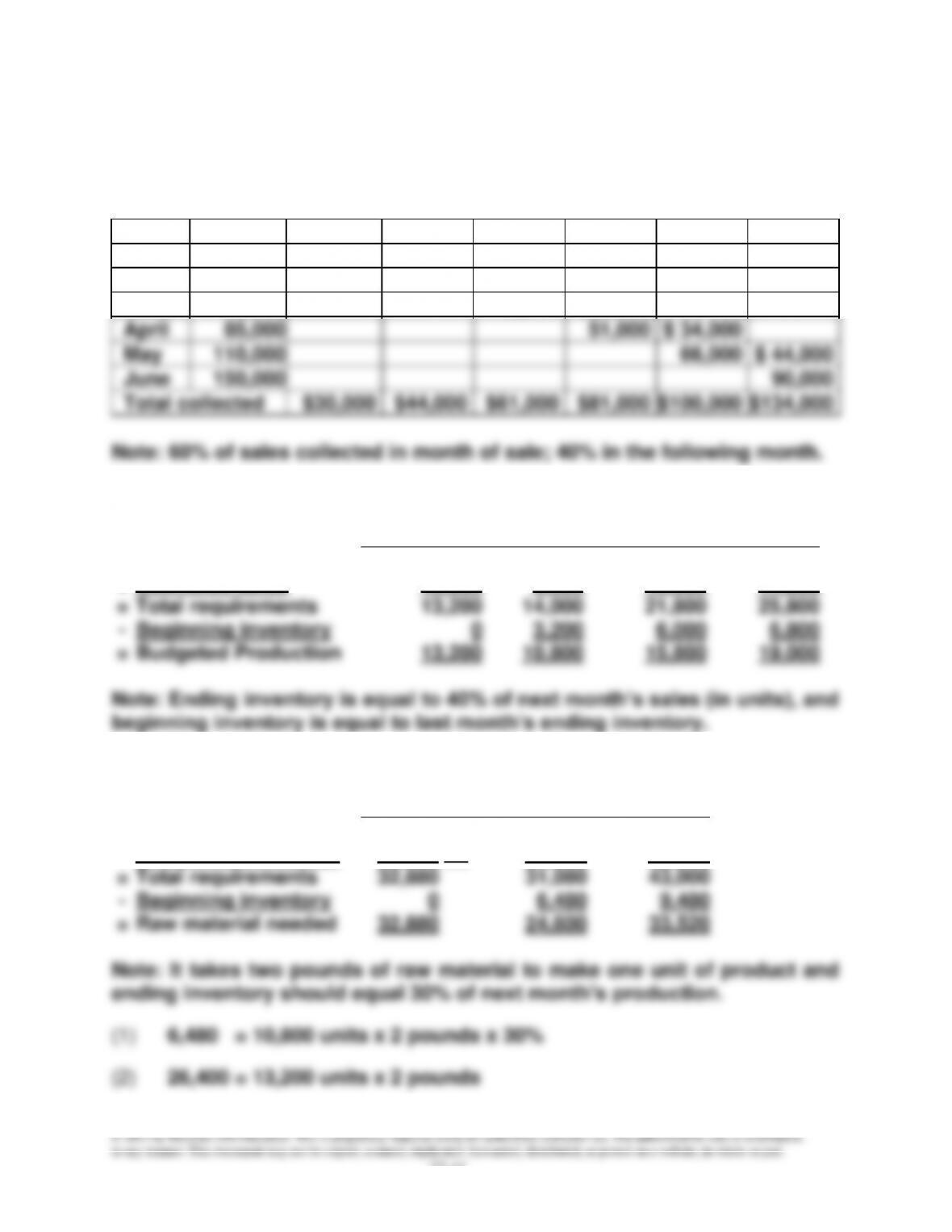

Alternate Demo Problem Twenty-Two

ABC Company started business on January 1, 20xx. The company

estimated that sales for the first six months would be as follows:

Month

Units

Dollars

January

10,000

$ 50,000

February

8,000

40,000

March

15,000

75,000

April

17,000

85,000

May

22,000

110,000

June

30,000

150,000

The company sells all items on account and expects collections of

accounts receivable to be as follows: 60% in the month of the sale, and the

remaining 40% in the month after the sale.

Required:

(a) Compute the expected cash collections during the months of January,

February, March, April, May and June.

(b) The company has decided that finished goods inventory at the end of

each month should ideally be equal to 40% of next month’s sales. What

should budgeted production be for each of the first four months?

(c) It takes two pounds of raw material to make one unit of finished

product. The com pany wants to keep an ending inventory of raw

material equal to 30% of next month’s production needs. How many

pounds of raw material should be purchased in each of the first three

months?

(d) The raw material costs $2 per pound. The company pays for 70% of its

purchases during the month of purchase and the remainder in the

following month. How much cash will be disbursed during the month of

March for the purchase of raw material?

(e) The projected cash balance on March 1 is $13,500. What is the

estimated cash balance at the end of the month? (Prepare a formal

cash budget for the month of March.)

22-11

Solution: Alternate Demo Problem Twenty-Two

(a)

Collections

Month

Sales

Jan.

Feb.

March

April

May

June

Jan.

$ 50,000

$30,000

$20,000

Feb.

40,000

24,000

$16,000

March

75,000

45,000

$30,000

April

85,000

51,000

$ 34,000

May

110,000

66,000

$ 44,000

June

150,000

90,000

Total collected

$30,000

$44,000

$61,000

$81,000

$100,000

$134,000

(b)

Jan.

Feb.

March

April

Ending inventory

3,200

6,000

6,800

8,800

+

Estimated sales

10,000

8,000

15,000

17,000

=

Total requirements

13,200

14,000

21,800

25,800

-

Beginning inventory

0

3,200

6,000

6,800

=

Budgeted Production

13,200

10,800

15,800

19,000

(c)

Jan.

Feb.

March

Ending inventory

6,480

(1)

9,480

11,400

+

Budgeted production

26,400

(2)

21,600

31,600

=

Total requirements

32,880

31,080

43,000

-

Beginning inventory

0

6,480

9,480

=

Raw material needed

32,880

24,600

33,520

22-12

(d)

Jan.

Feb.

March

Purchases (in units)

$32,880

24,600

33,520

X

Price per pound

2.00

2.00

2.00

=

Purchase cost

$65,760

$49,200

$67,040

March cash disbursement equals 70% of March purchases plus 30% of

February purchases.

Therefore, March cash disbursements equal:

Purchases from:

February

30% x $49,200

$14,760

March

70% x $67,040

+

46,928

Total cash paid for materials

$61,688

(e)

ABC COMPANY

Cash Budget

For the Month of March 20xx

Beginning cash balance

$13,500

Cash receipts from customers

61,000

Total cash available

74,500

Cash disbursements

61,688

Ending cash balance

$12,812