Chapter 10

Plant Assets, Natural Resources,

and Intangibles

QUESTIONS

1. A plant asset is tangible; it is used in the production or sale of other assets or services;

and it has a useful life longer than one accounting period.

4. Often the lump-sum or basket purchase includes assets with different lives that must be

depreciated separately. Sometimes the purchase may include land, which is never

depreciated.

5. The Accumulated Depreciation—Machinery account is a contra asset account with a

credit balance that cannot be used to buy anything. The balance of the Accumulated

6. The Modified Accelerated Cost Recovery System is not generally acceptable for financial

7. The materiality constraint justifies charging low-cost plant asset purchases to expense

because such amounts are unlikely to impact the decisions of financial statement users.

8. Ordinary repairs are made to keep a plant asset in normal, good operating condition, and

9. A company might sell or exchange an asset when it reaches the end of its useful life, or

10. The process of allocating the cost of natural resources to expense over the periods

11. No, depletion expense should be calculated on the units that are extracted (similar to the

units-of–production basis) and sold.

12. An intangible asset: (1) has no physical existence; (2) derives value from the unique

13. Intangible assets are generally recorded at their cost and amortized over their predicted

useful life. (However, some costs are not included, such as the research and

14. A company has goodwill when its value exceeds the value of its individual assets and

15. No; this type of goodwill would not be amortized. Instead, the FASB (SFAS 142) requires

that goodwill be annually tested for impairment. If the book value of goodwill does not

16. Total asset turnover is calculated by dividing net sales by average total assets.

17. The word “net” means that Polaris is reporting its property and equipment after

deducting accumulated depreciation to date.

18. Arctic Cat lists “Machinery, equipment and tooling” and “Land, building and

19. KTM titles its plant assets “Tangible fixed assets.” The book value of its Tangible fixed

assets is 84,256 EUR thousands.

QUICK STUDIES

Quick Study 10-1 (10 minutes)

1. The main difference between plant assets and current assets is that

2. The main difference between plant assets and inventory is that

3. The main difference between plant assets and long-term investments is

Quick Study 10-2 (10 minutes)

expenditure necessary to get the asset in place and ready for its intended use.

Quick Study 10-3 (10 minutes)

Straight-line:

Quick Study 10-4 (10 minutes)

($65,800 – $2,000) / 200 concerts = $ 319 depreciation per concert

Quick Study 10-5 (10 minutes)

$65,800

Cost

– 15,950

Accumulated depreciation (first year)

49,850

Book value at point of revision

– 2,000

Salvage value

47,850

Remaining depreciable cost

÷ 2

Years of life remaining

$23,925

Depreciation per year for years 2 and 3

Quick Study 10-6 (10 minutes)

Note: Double-declining-balance rate = (100% / 8 years) x 2 = 25%

First year:

$830,000 x 25% = $207,500

Second year:

Third year:

Quick Study 10-7 (10 minutes)

Impairment Loss …………………………………………………....

1,250

Accumulated Depreciation—Equipment …………..

1,250

To record impairment of equipment.

Quick Study 10-8 (10 minutes)

1. (a) Capital expenditure

2.

(a) Equipment……………………………………………………....

40,000

Cash ……………………………………………………….

40,000

To record an extraordinary repair.

(b)* Maintenance Expense ……………………………………..

200

Cash ……………………………………………………….

200

To record ordinary maintenance of a truck.

(c)* Maintenance Expense ……………………………………..

175

Cash ……………………………………………………….

175

To record ordinary maintenance for air conditioner.

(d) Building ……………………………………………………….....

225,000

Cash ……………………………………………………….

225,000

To record addition of a new wing.

*Although NOT required, entries are shown for transactions b and c for completeness

Quick Study 10-9 (15 minutes)

Book value of old equipment = $76,800 – $40,800 = $36,000

1.

Cash ……………………………………………………………………..

47,000

Accumulated depreciation ……………………………………..

40,800

Equipment …………………………………………………………….

76,800

Gain on sale of equipment* …………………………………….

11,000

To record the sale of equipment.

*(Gain = $47,000 – $36,000)

2.

Cash ……………………………………………………………………..

36,000

Accumulated depreciation ……………………………………..

40,800

Equipment …………………………………………………………….

76,800

To record the sale of equipment.

3.

Cash ……………………………………………………………………..

31,000

Accumulated depreciation ……………………………………..

40,800

Loss on sale of equipment*……………………………………….

5,000

Equipment……………………………………………………….

76,800

To record the sale of equipment.

*(Loss = $31,000 – $36,000)

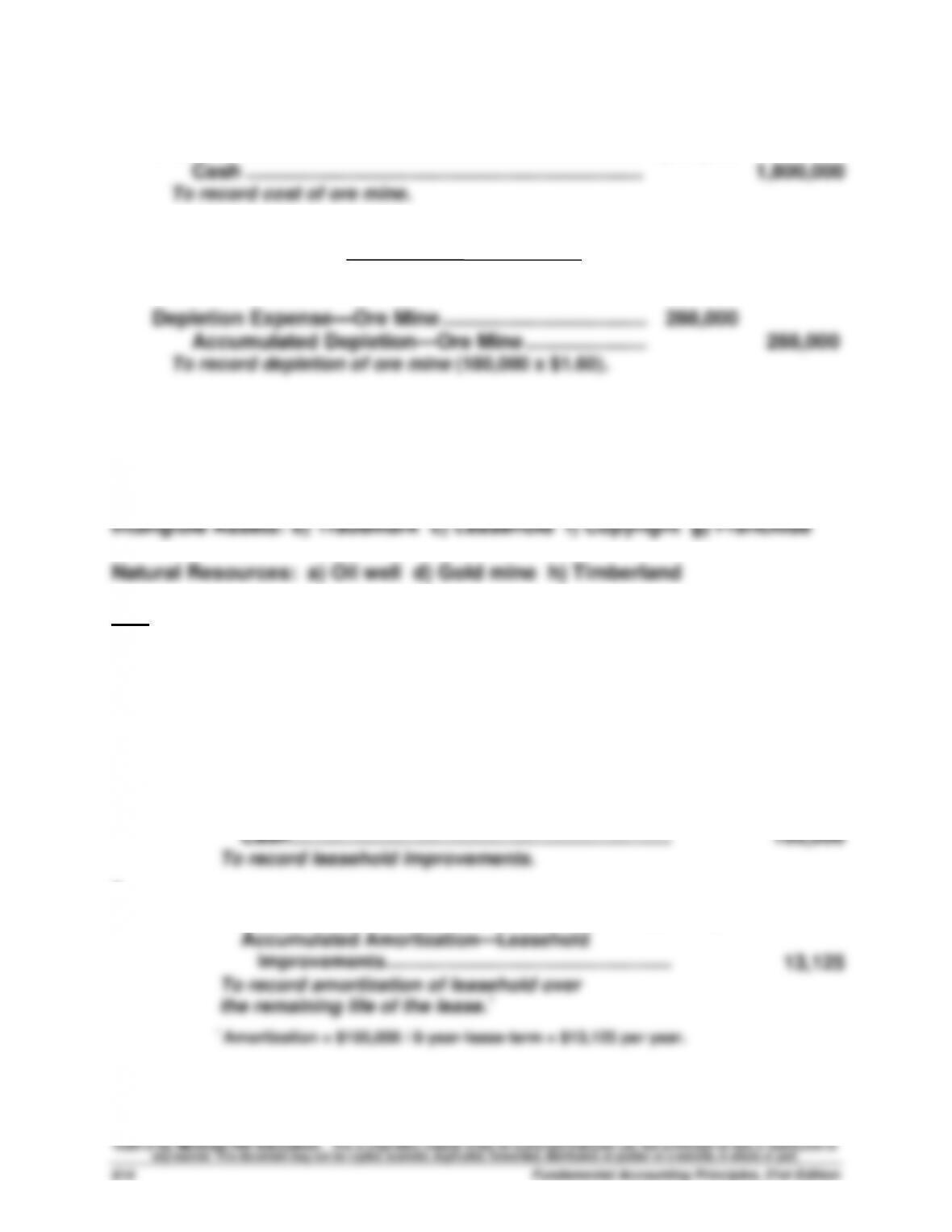

Quick Study 10-10 (10 minutes)

1.

Ore Mine ………………………………………………………………..

1,800,000

Cash ……………………………………………………………....

1,800,000

To record cost of ore mine.

2.

Depletion per unit = = $1.60 per ton

Depletion Expense—Ore Mine ………………………………..

288,000

Accumulated Depletion—Ore Mine …………………..

288,000

To record depletion of ore mine (180,000 x $1.60).

Quick Study 10-11 (10 minutes)

Note: e) Building is reported under plant assets.

Quick Study 10-12 (10 minutes)

1.

Jan. 4

Leasehold Improvements …………………………………..……

105,000

Cash …………………………………………………………..……

105,000

To record leasehold improvements.

2.

Dec. 31

Amortization Expense–Leasehold Improvements …………

13,125

Accumulated Amortization—Leasehold

Improvements …………………………………………………

13,125

To record amortization of leasehold over

the remaining life of the lease.*

* Amortization = $105,000 / 8-year-lease-term = $13,125 per year.

$1,800,000 – $200,000

1,000,000 tons

Quick Study 10-13 (10 minutes)

Total asset turnover = = 0.80 times

($ thousands)

Quick Study 10-14A (10 minutes)

Book value of old machine = $42,400 – $18,400 = $24,000

1.

Machinery (new) ………………………………………………..

52,000

Accumulated Depreciation–Machinery (old) ……….

18,400

Loss on Exchange of Assets* …………………………….

2,000

Machinery (old) ………………………………………….

42,400

Cash ………………………………………………………….

30,000

To record asset exchange assuming commercial

substance. *$52,000 – ($24,000 + $30,000) = $(2,000)

2.

Machinery (new)* …………………………..…………………..

46,000

Accumulated Depreciation–Machinery (old) ……….

18,400

Machinery (old) ………………………………………….

42,400

Cash ………………………………………………………….

22,000

To record asset exchange assuming lack of

commercial substance.

*Book value of old asset + cash given = $24,000 + $22,000

Quick Study 10-15 (10 minutes)

a. Accounting for plant assets involving cost determination,

depreciation, additional expenditures, and disposals of plant assets

b. U.S. GAAP prohibits companies to record increases in the value of

plant assets subsequent to acquisition. However, IFRS permits

$14,800

($15,869 + $17,819) / 2

EXERCISES

Exercise 10-1 (15 minutes)

Invoice price of machine …………………………………….…………..

$ 12,500

Less discount (.02 x $12,500) ……………………………..…………..

(250)

Net purchase price……………………………………………..………..

12,250

Freight charges (transportation–in) ……………………..……

360

Mounting and power connections …………………………..

895

Assembly …………………………………………………………..…………..

475

Materials used in adjusting ……………………………………………..

40

Total cost to be recorded ………………………………………………..

$ 14,020

Note: The $180 repair charge is an expense because it is not a normal and reasonable

expenditure necessary to get the asset in place and ready for its intended use.

Exercise 10-2 (15 minutes)

Cost of land

Purchase price for land …………………………………………………..

$ 280,000

Purchase price for old building …………………………..

110,000

Demolition costs for old building ………………………..…

33,500

Costs to fill and level lot …………………………………….…………..

47,000

Total cost of land ……………………………………………….………

$ 470,500

Cost of new building and land improvements

Cost of new building ………………………………………….…………..

$1,452,200

Cost of land improvements ………………………………..…………..

87,800

Total construction costs …………………………………….…………..

$1,540,000

Journal entry

Land ………………………………………………………………….….

470,500

Land Improvements ……………………………………………….

87,800

Building …………………………………………………………….….

1,452,200

Cash …………………………………………………………….….

2,010,500

To record costs of plant assets.

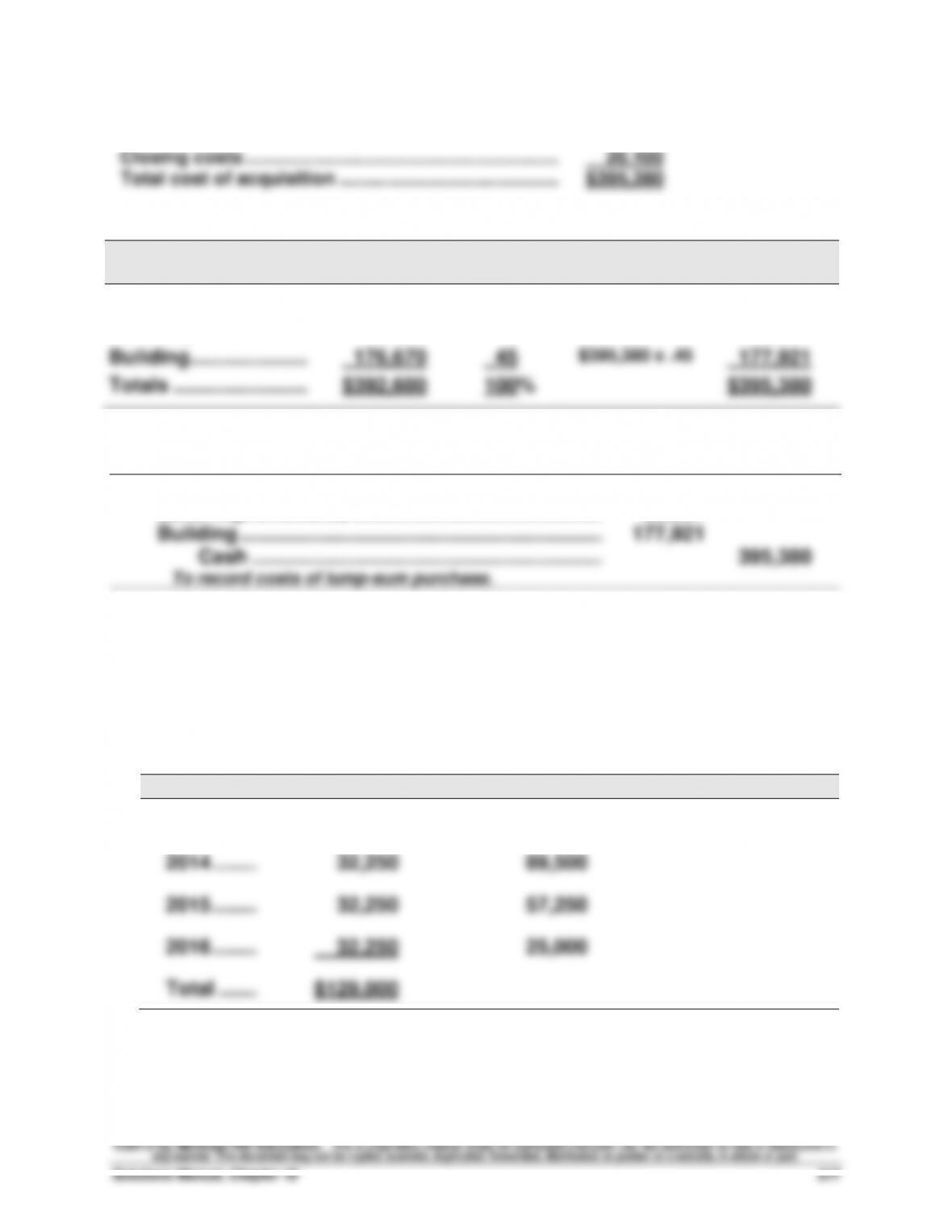

Exercise 10-3 (20 minutes)

Purchase price …………………………………………………..

$375,280

Closing costs …………………………………………………….

20,100

Total cost of acquisition …………………………………….

$395,380

Allocation of total cost

Appraised

Value

Percent

of Total

Applying %

to Cost

Apportioned

Cost

Land ……………………..….

$157,040

40%

$395,380 x .40

$158,152

Land improvements ..….

58,890

15

$395,380 x .15

59,307

Building …………………….

176,670

45

$395,380 x .45

177,921

Totals ……………………….

$392,600

100%

$395,380

Journal entry

Land ……………………………………………………………..…

158,152

Land Improvements …………………………………………

59,307

Building ………………………………………………………..…

177,921

Cash ……………………………………………………….

395,380

To record costs of lump-sum purchase.

Exercise 10-4 (15 minutes)

Straight-line depreciation: ($154,000 – $25,000) / 4 years = $32,250 per year

Year

Annual Depreciation

Year-End Book Value

2013 ……..

$ 32,250

$121,750

2014 ……..

32,250

89,500

2015 ……..

32,250

57,250

2016 ……..

32,250

25,000

Total …….

$129,000

Exercise 10-5 (20 minutes)

Double-declining-balance depreciation

Depreciation rate: 100% / 4 years = 25% x 2 = 50%

Year

Beginning-Year

Book Value

Depreciation

Rate

Annual

Depreciation

Year-End

Book Value

2013 …….

$154,000

50%

$ 77,000

$77,000

2014 …….

77,000

50

38,500

38,500

2015 …….

38,500

50

13,500*

25,000

2016 …….

25,000

—

—

25,000

Total …….

$129,000

* Do not depreciate more than $13,500 in the third year since the

salvage value is not subject to depreciation.

Exercise 10-6 (10 minutes)

Straight-line

Exercise 10-7 (10 minutes)

Units–of-production

Exercise 10-8 (15 minutes)

Double-declining-balance

Double-declining-balance rate = (100% / 10 years) x 2 = 20% per year

Exercise 10-9 (10 minutes)

Straight-line depreciation for 2012

[($280,000 – $40,000) / 5 years] x 9/12 = $36.000

Exercise 10-10 (15 minutes)

Double-declining-balance depreciation for 2012 and 2013:

Rate = (100% / 5 years) x 2 = 40%

Depreciation for 2012 ($280,000 x 40% x 9/12) ……………

$ 84,000

Book value at January 1, 2013 ($280,000 – $84,000) ……

$196,000

Depreciation for 2013 ($196,000 x 40%) ……………………..

$ 78,400

Alternate calculation

2012 depreciation ($280,000 x 40% x 9/12) …………………………...

$ 84,000

2013 depreciation

$280,000 x 40% x 3/12 …………………………………………………….

$ 28,000

($280,000 – $84,000 – $28,000) x 40% x 9/12 ………………………

50,400

Total 2013 depreciation ………………………………………………………

$ 78,400

Exercise 10-11 (15 minutes)

1.

Original cost of machine …………………………………………..………..

$ 23,860

Less two years’ accumulated depreciation

[($23,860 – $2,400) / 4 years] x 2 years …………………….…….

(10,730)

Book value at end of second year ……………………………..………..

$ 13,130

2.

Book value at end of second year ……………………………..………..

$ 13,130

Less revised salvage value ……………………………………….………..

(2,000)

Remaining depreciable cost ……………………………………..………..

$ 11,130

Revised annual depreciation = $11,130 / 3 years = $3,710

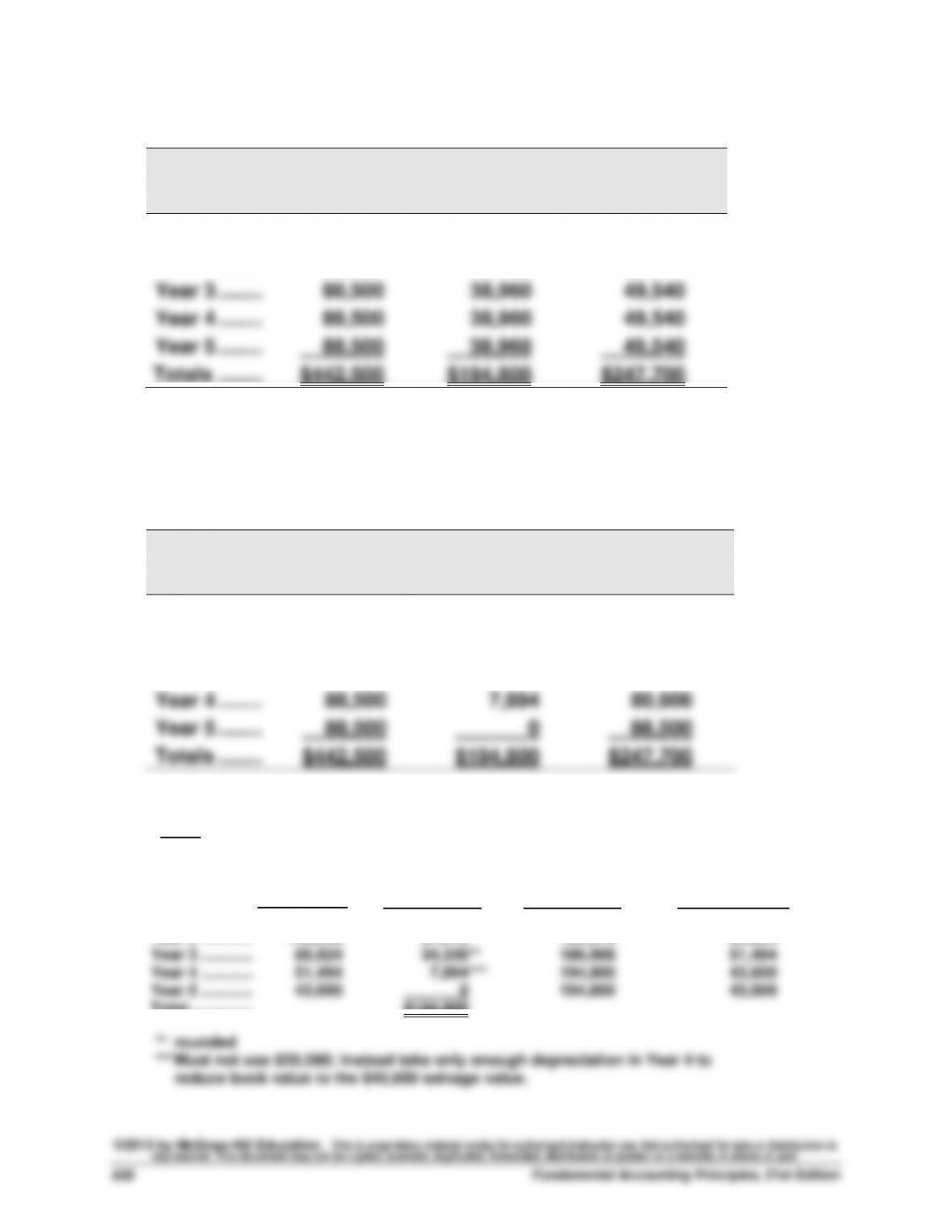

Exercise 10-12 (30 minutes)

Straight-line depreciation

Income

before

Depreciation

Depreciation

Expense*

Net

Income

Year 1 ……..

$ 88,500

$ 38,960

$ 49,540

Year 2 ……..

88,500

38,960

49,540

Year 3 ……..

88,500

38,960

49,540

Year 4 ……..

88,500

38,960

49,540

Year 5 ……..

88,500

38,960

49,540

Totals ……..

$442,500

$194,800

$247,700

*($238,400 – $43,600) / 5 years = $38,960

Exercise 10-13 (30 minutes)

Double-declining-balance depreciation

Income

before

Depreciation

Depreciation

Expense*

Net

Income

Year 1 ……..

$ 88,500

$ 95,360

$ (6,860)

Year 2 ……..

88,500

57,216

31,284

Year 3 ……..

88,500

34,330

54,170

Year 4 ……..

88,500

7,894

80,606

Year 5 ……..

88,500

0

88,500

Totals ……..

$442,500

$194,800

$247,700

Supporting calculations for depreciation expense

*Note: (100% / 5 years) x 2 = 40% depreciation rate

Beginning

Book

Value

Annual

Depreciation

(40% of

Book Value)

Accumulated

Depreciation at

the End of the

Year

Ending Book Value

($238,400 Cost Less

Accumulated

Depreciation)

Year 1 ……………

$238,400

$ 95,360

$ 95,360

$143,040

Year 2 ……………

143,040

57,216

152,576

85,824

Year 3 ……………

85,824

34,330**

186,906

51,494

Year 4 ……………

51,494

7,894***

194,800

43,600

Year 5 ……………

43,600

0

194,800

43,600

Total ………………

$194,800

** rounded

*** Must not use $20,598; instead take only enough depreciation in Year 4 to

reduce book value to the $43,600 salvage value.

Exercise 10-14 (25 minutes)

1. Annual depreciation = $572,000 / 20 years = $28,600 per year

2. Entry to record the extraordinary repairs

Building ……………………………………………………………..….

68,350

Cash …………………………………………………………..….

68,350

To record extraordinary repairs.

3.

Cost of building

Before repairs……………………………………………………….

$572,000

Add cost of repairs …………………………………………………

68,350

$640,350

Less accumulated depreciation …………………………..

429,000

Revised book value of building …………………………..

$211,350

4.

Revised book value of building (part 3) ………………………

$211,350

New estimate of useful life (20 – 15 + 5) ………………………

10 years

Revised annual depreciation ……………………………..………

$ 21,135

Depreciation Expense …………………………………………….

21,135

Accumulated Depreciation–Building …………………..

21,135

To record depreciation.

Exercise 10-15 (15 minutes)

1.

Equipment ………………………………………………………..….

22,000

Cash …………………………………………………………..….

22,000

To record betterment.

2.

Repairs Expense ……………………………………………….….

6,250

Cash …………………………………………………………..….

6,250

To record ordinary repairs.

3.

Equipment ………………………………………………………..….

14,870

Cash …………………………………………………………..….

14,870

To record extraordinary repairs.

Exercise 10-16 (20 minutes)

Note: Book value of milling machine = $250,000 – $182,000 = $68,000

1. Disposed at no value

Jan. 3

Loss on Disposal of Milling Machine …………………….

68,000

Accumulated Depreciation—Milling Machine ….…….

182,000

Milling Machine ………………………………………….…….

250,000

To record disposal of milling machine.

2. Sold for $35,000 cash

Jan. 3

Cash ……………………………………………………………..…….

35,000

Loss on Sale of Milling Machine ……………………..……

33,000

Accumulated Depreciation—Milling Machine ….…….

182,000

Milling Machine ………………………………………….…….

250,000

To record cash sale of milling machine.

3. Sold for $68,000 cash

Jan. 3

Cash ……………………………………………………………..…….

68,000

Accumulated Depreciation—Milling Machine ….…….

182,000

Milling Machine ………………………………………….…….

250,000

To record cash sale of milling machine.

4. Sold for $80,000 cash

Jan. 3

Cash ……………………………………………………………..…….

80,000

Accumulated Depreciation—Milling Machine ….…….

182,000

Gain on Sale of Milling Machine ………………….…….

12,000

Milling Machine ………………………………………….…….

250,000

To record cash sale of milling machine.

Exercise 10-17 (25 minutes)

2017

July 1

Depreciation Expense ………………………………………

7,500

Accumulated Depreciation—Machinery …………

7,500

To record one-half year depreciation.*

*Annual depreciation = $105,000 / 7 years = $15,000

Depreciation for 6 months in 2017 = $15,000 x 6/12 = $7,500

1. Sold for $45,500 cash

July 1

Cash ……………………………………………………………………

45,500

Accumulated Depreciation—Machinery …………..……

67,500

Gain on Sale of Machinery …………………………..

8,000

Machinery ……………………………………………………….

105,000

To record sale of machinery.*

2. Destroyed by fire with $25,000 cash insurance settlement

July 1

Cash ……………………………………………………………………

25,000

Loss from Fire ………………………………………………..……

12,500

Accumulated Depreciation—Machinery …………..……

67,500

Machinery ……………………………………………………….

105,000

To record disposal of machinery from fire.

Exercise 10-18 (10 minutes)

Dec. 31

Depletion Expense—Mineral Deposit ……………..…….

405,528

Accumulated Depletion—Mineral Deposit …..…….

405,528

To record depletion [$3,721,000/1,525,000 tons =

$2.44 per ton; 166,200 tons x $2.44 = $405,528].

Dec. 31

Depreciation Expense—Machinery ………………..…….

23,268

Accumulated Depreciation—Machinery ……..…….

23,268

To record depreciation [$213,500/1,525,000 tons=

$0.14 per ton; 166,200 tons x $0.14 = $23,268].