Exercise 22-19 (10 minutes)

MANNER COMPANY

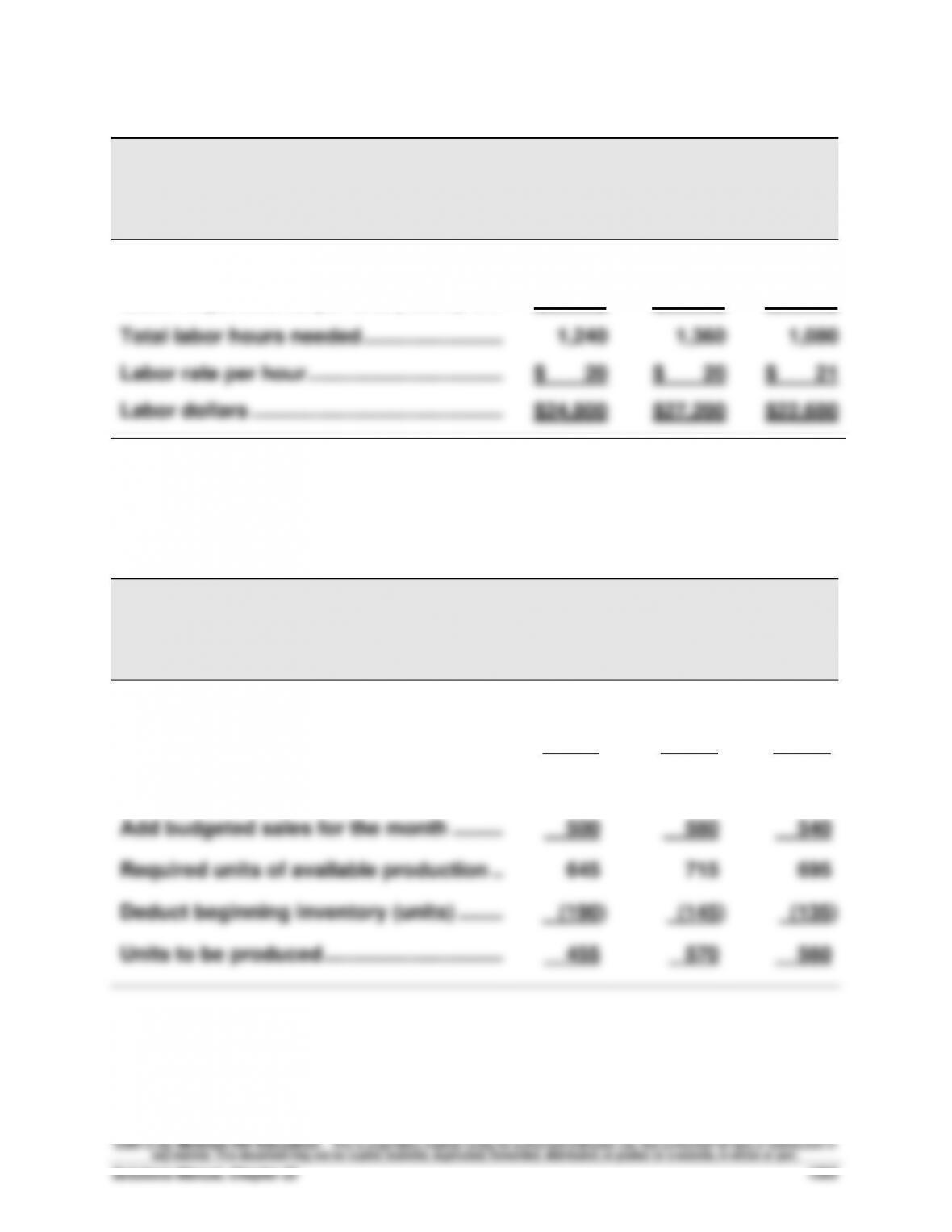

Direct Labor Budget

For July, August, and September

July

August

Sept.

Budgeted production (units) ……………….…

620

680

540

Labor requirements per unit (hours) ………

x 2

x 2

x 2

Total labor hours needed …………………….…

1,240

1,360

1,080

Labor rate per hour ……………………………..…

$ 20

$ 20

$ 21

Labor dollars …………………………………………

$24,800

$27,200

$22,680

Exercise 22-20 (15 minutes)

HOSPITABLE CO.

Production Budget

For April, May, and June

April

May

June

Next month’s budgeted sales (units) ………

580

540

620

Ratio of inventory to future sales ……………

x 25%

x 25%

x 25%

Budgeted ending inventory (units) ……..…

145

135

155

Add budgeted sales for the month …………

500

580

540

Required units of available production ..…

645

715

695

Deduct beginning inventory (units) ……..…

(190)

(145)

(135)

Units to be produced …………………………..

455

570

560

Fundamental Accounting Principles, 21st Edition

1294

Exercise 22-21 (15 minutes)

HOSPITABLE CO.

Direct Materials Budget

For April, May, and June

April

May

June

Budgeted production (units)* …………………

455

570

560

Materials requirements per unit …………..…

x 5

x 5

x 5

Materials needed for production (lbs.) ……

2,275

2,850

2,800

Add budgeted ending inventory** ………..…

855

840

810

Total materials requirements (lbs.) …………

3,130

3,690

3,610

Deduct beginning inventory (lbs.) ………..…

(663)

(855)

(840)

Materials to be purchased (lbs.) …………..…

2,467

2,835

2,770

* From Exercise 22-20

** 30% of next month’s materials needed for production.

Exercise 22-22 (10 minutes)

Exercise 22-23 (5 minutes)

Potential negative outcomes from participatory budgeting include the

Exercise 22-24 (15 minutes)

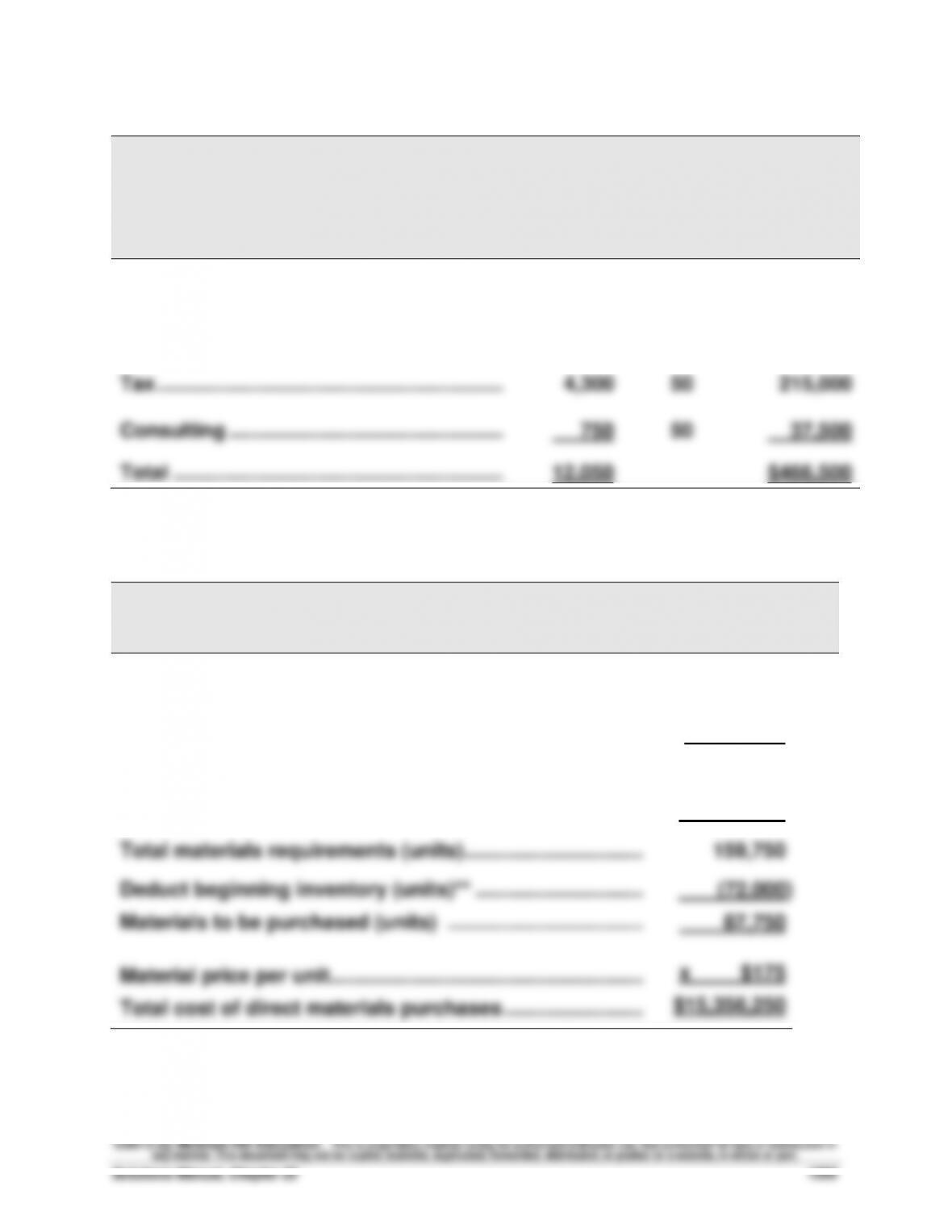

RENDER CO. CPA

Activity-Based Budget

For Year Ending December 31, 2013

Budgeted

Hours

Budgeted

Price/hour

Budgeted

Cost

Data-entry …………………………………………..…

2,200

$10

$ 22,000

Auditing ……………………………………………..…

4,800

40

192,000

Tax ……………………………………………………....

4,300

50

215,000

Consulting ………………………………………….…

Total …………………………………………………..…

750

12,050

50

37,500

$466,500

Exercise 22-25 (15 minutes)

RIDA INC.

Direct Materials Budget

Second Quarter

Units to be produced …………………………..…………………….……

240,000

Materials requirement per unit …………………………………..……

x .60

Materials needed for production (units) ……………………..……

144,000

Add budgeted ending inventory (units)* …………………….……

15,750

Total materials requirements (units) …………………………..

159,750

Deduct beginning inventory (units)** …………………………..

Materials to be purchased (units) ……………………………..……

Material price per unit………………………………………………..……

Total cost of direct materials purchases …………………….……

(72,000)

87,750

x $175

$15,356,250

*(52,500 x 0.60) x 50%

**144,000 x 50%

Fundamental Accounting Principles, 21st Edition

1296

Exercise 22-26 (15 minutes)

1.

RIDA INC.

Direct Labor Budget

Second Quarter

Units to be produced …………………………..…………………….……

240,000

Labor requirements per unit (hours) …………………………..

x 4

Total labor hours needed …………………………………………..……

960,000

Labor rate (per hour) ………………………………………………………

x $9

Labor dollars …………………………………………………………….……

$8,640,000

2.

RIDA INC.

Factory Overhead Budget

Second Quarter

Total labor hours needed …………………………………………..……

960,000

Variable overhead rate per DL hour …………………………………

x $11

Budgeted variable overhead ……………………………………………

$10,560,000

Budgeted fixed overhead …………………………………………..……

450,000

Budgeted total overhead …………………………………………………

$11,010,000

Exercise 22-27 (20 minutes)

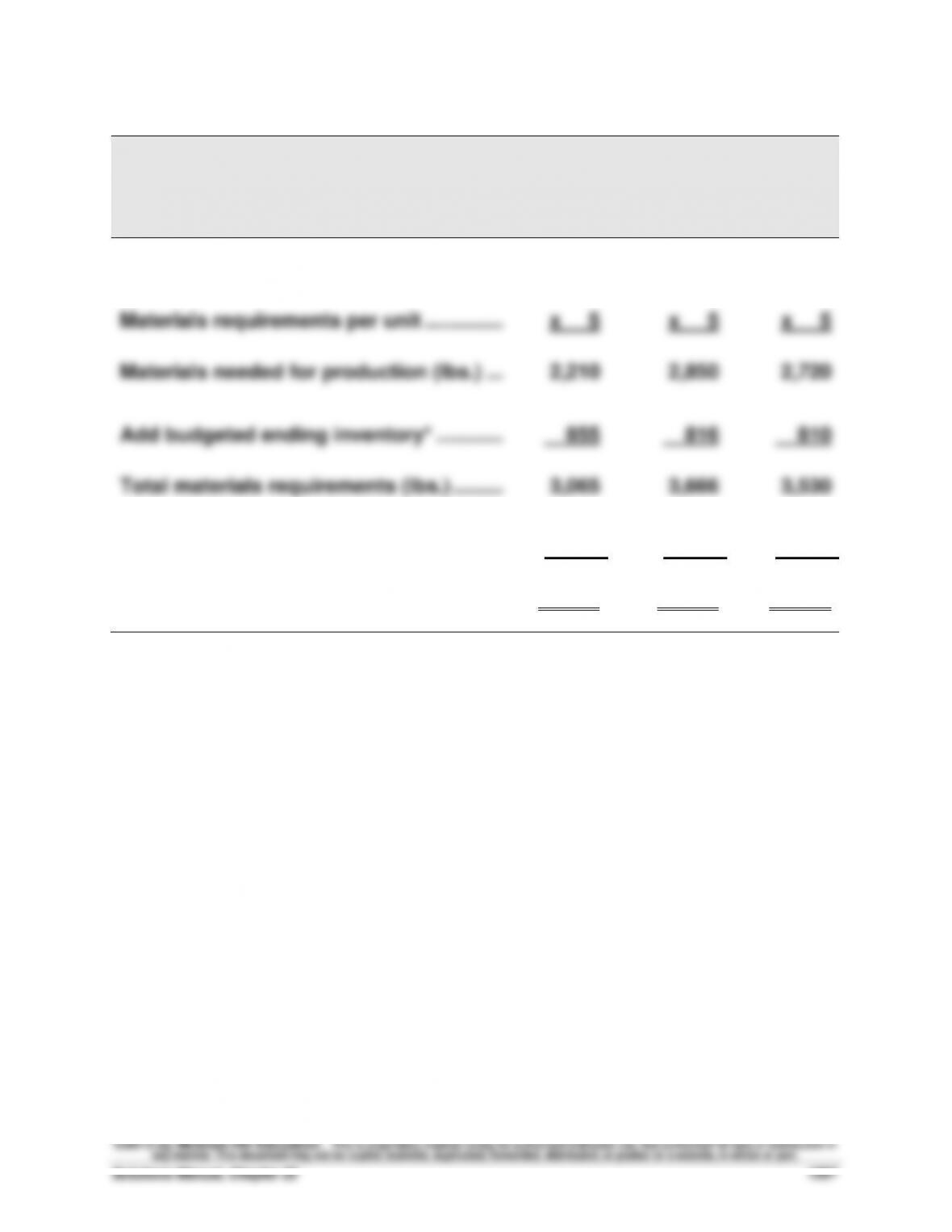

RAD CO.

Direct Materials Budget

For April, May, and June

April

May

June

Budget production (units) ………………………

442

570

544

Materials requirements per unit …………..…

x 5

x 5

x 5

Materials needed for production (lbs.) ……

2,210

2,850

2,720

Add budgeted ending inventory* ……………

855

816

810

Total materials requirements (lbs.) …………

3,065

3,666

3,530

Deduct beginning inventory (lbs.) ………..…

(663)

(855)

(816)

Materials to be purchased (lbs.) …………..…

2,402

2,811

2,714

*30% of next month’s materials needed for production. July’s materials needed for

production equals 2,700 pounds (540 units x 5).

Fundamental Accounting Principles, 21st Edition

1298

Exercise 22-28 (15 minutes)

1.

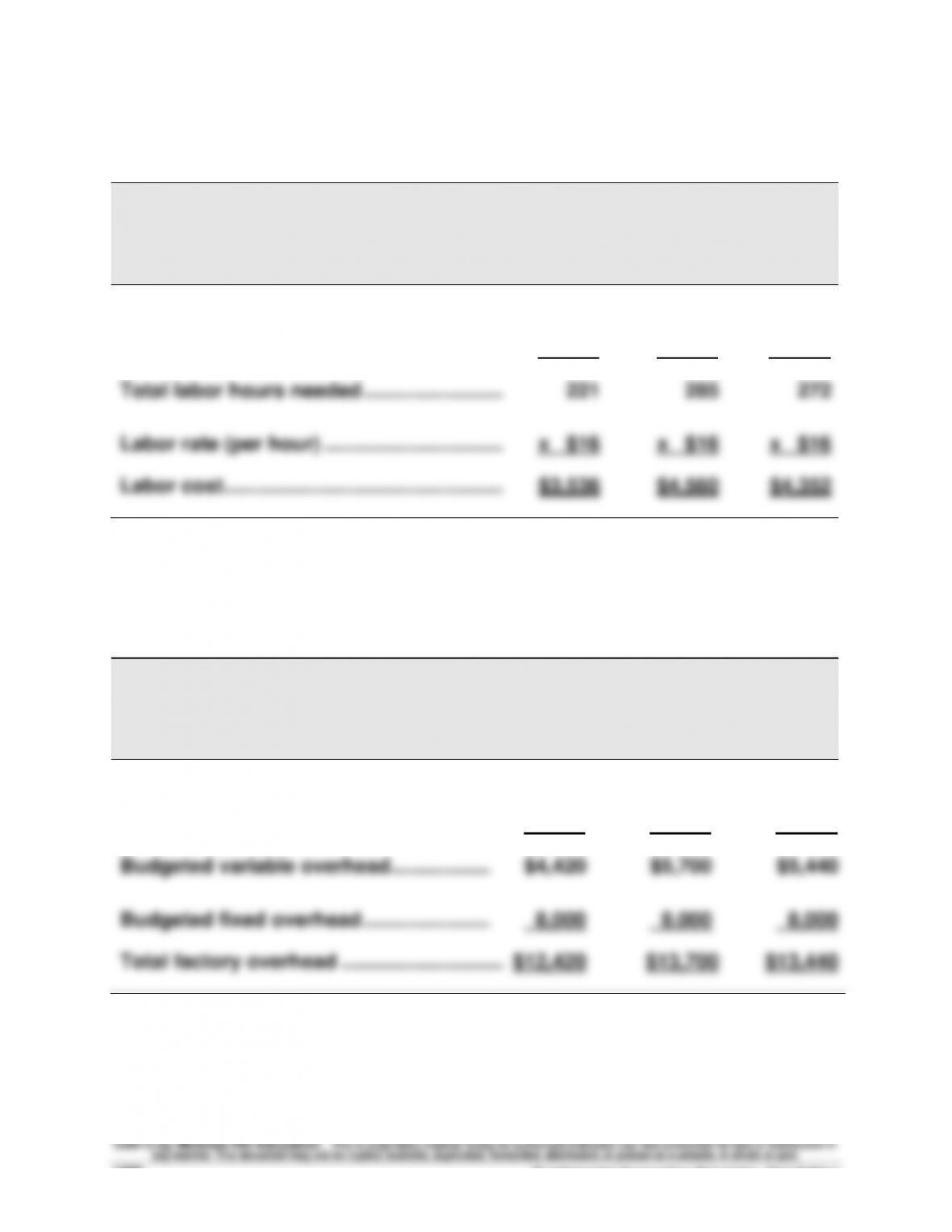

RAD CO.

Direct Labor Budget

For April, May, and June

April

May

June

Budget production (units) ………………………

442

570

544

Direct labor hours per unit …………………..…

x 0.50

x 0.50

x 0.50

Total labor hours needed …………………….…

221

285

272

Labor rate (per hour) …………………………..

x $16

x $16

x $16

Labor cost …………………………………………..…

$3,536

$4,560

$4,352

2.

RAD CO.

Factory Overhead Budget

For April, May, and June

April

May

June

Total labor hours needed …………………..…..

221

285

272

Variable factory overhead rate …………..…..

x $20

x $20

x $20

Budgeted variable overhead …………………..

$4,420

$5,700

$5,440

Budgeted fixed overhead …………………..…..

8,000

8,000

8,000

Total factory overhead ………………………..…

$12,420

$13,700

$13,440

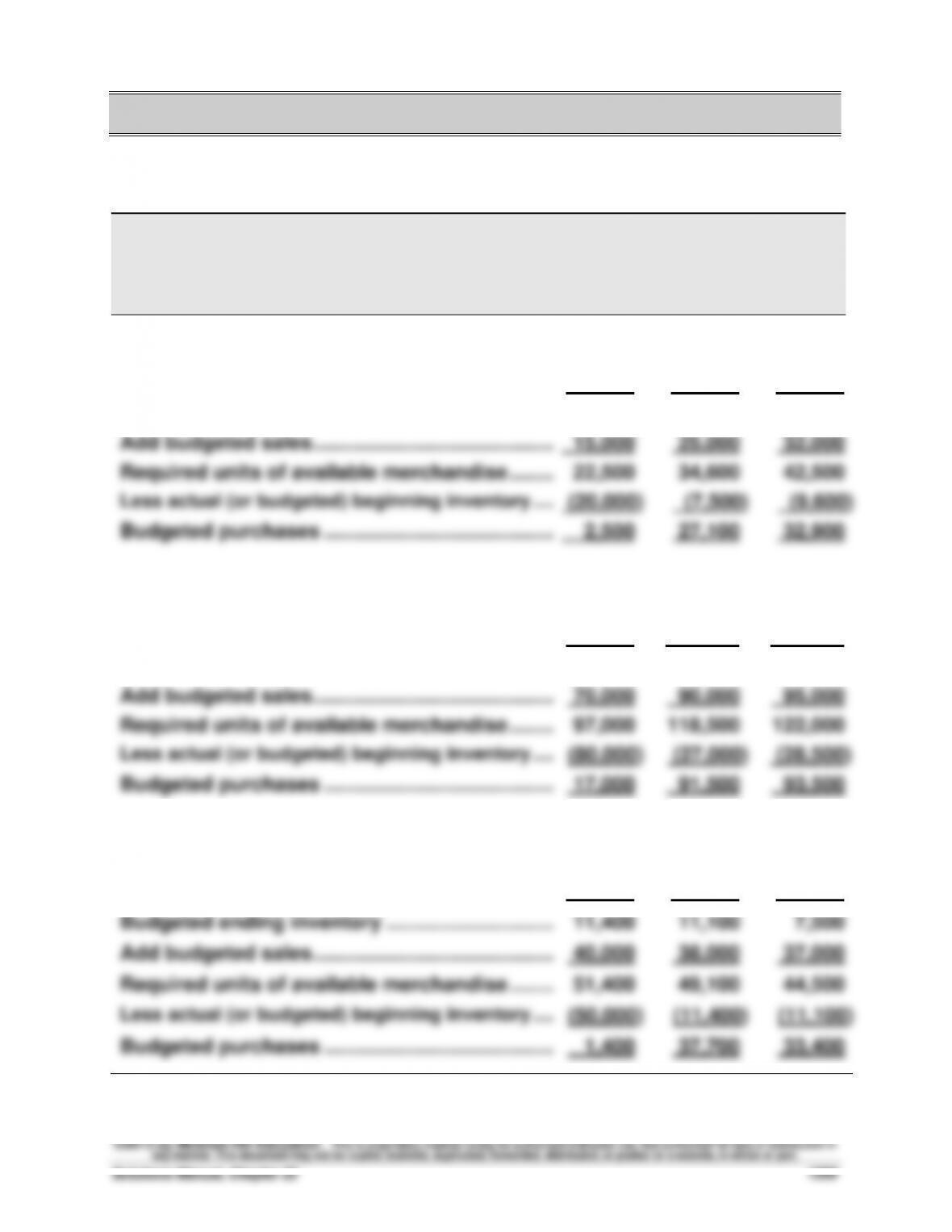

PROBLEM SET A

Problem 22-1A (60 minutes)

Part 1

KEGGLER’S SUPPLY

Merchandise Purchases Budgets

For March, April, and May

March

April

May

FOOTWEAR

Budgeted sales for next month ………………………

25,000

32,000

35,000

Ratio of ending inventory to future sales ……..…

30%

30%

30%

Budgeted ending inventory …………………………..

7,500

9,600

10,500

Add budgeted sales …………………………………….…

15,000

25,000

32,000

Required units of available merchandise ……..…

22,500

34,600

42,500

Less actual (or budgeted) beginning inventory ….…

(20,000)

(7,500)

(9,600)

Budgeted purchases …………………………………..…

2,500

27,100

32,900

SPORTS EQUIPMENT

Budgeted sales for next month ………………………

90,000

95,000

90,000

Ratio of ending inventory to future sales ……..…

30%

30%

30%

Budgeted ending inventory …………………………..

27,000

28,500

27,000

Add budgeted sales …………………………………….…

70,000

90,000

95,000

Required units of available merchandise ……..…

97,000

118,500

122,000

Less actual (or budgeted) beginning inventory ….…

(80,000)

(27,000)

(28,500)

Budgeted purchases …………………………………..…

17,000

91,500

93,500

APPAREL

Budgeted sales for next month ………………………

38,000

37,000

25,000

Ratio of ending inventory to future sales ……..…

30%

30%

30%

Budgeted ending inventory …………………………..

11,400

11,100

7,500

Add budgeted sales …………………………………….…

40,000

38,000

37,000

Required units of available merchandise ……..…

51,400

49,100

44,500

Less actual (or budgeted) beginning inventory ….…

(50,000)

(11,400)

(11,100)

Budgeted purchases …………………………………..…

1,400

37,700

33,400

Fundamental Accounting Principles, 21st Edition

1300

Problem 22-1A (Continued)

Part 2. Analysis Component

The factor that causes the first month’s purchases to be so much smaller is

the excess inventory that accumulated just prior to the budgeting period.

This overstocking factor could exist for a number of reasons, including:

• Management may have simply lost sight of inventory levels, thereby

allowing them to reach inappropriately high levels.

• A supplier may have recently located a new distribution facility nearby,

with the result that the merchandise can be delivered more promptly.

Problem 22-2A (50 minutes)

ONEIDA COMPANY

Cash Budget

For September, October, and November

September

October

November

Beginning balance ……………………………………

$ 5,000

$ 99,250

$ 69,500

Cash receipts

Collection on accounts receivable* …………

159,250

249,250

338,100

Receipts from bank loan …………………………

100,000

_______

_______

Total cash available ……………………………….…

264,250

348,500

407,600

Cash disbursements

Payments on accounts payable** ……………

100,000

217,000

228,000

Payroll ……………………………………………………

20,000

22,000

24,000

Rent …………………………………………………….…

10,000

10,000

10,000

Other expenses …………………………..……….…

35,000

30,000

20,000

Repayment on bank loan ……………………..…

100,000

Interest on bank loan*** ……………………….…

________

________

3,000

Total cash disbursements ………………………

165,000

279,000

385,000

Ending cash balance ……………………………..…

$ 99,250

$ 69,500

$ 22,600

*** Interest at 12% on $100,000 for 3 months is $3,000.

Supporting schedules

Collections of credit sales*

August

September

October

November

Aug. sales ($215,000)—[25%: 45%: 20%: 9%] ….…………

$ 53,750

$ 96,750

$ 43,000

$ 19,350

Sept. sales ($250,000)—[25%: 45%: 20%] ………..…………

–

62,500

112,500

50,000

Oct. sales ($375,000)—[25%: 45%] ………………….……….

–

–

93,750

168,750

Nov. sales ($400,000)—[25%] …………………………..

–

–

–

100,000

Total …………………………………………………………….…………

$ 53,750

$159,250

$249,250

$338,100

Payments on credit purchases**

August

September

October

November

Aug. purchases ($125,000)—(0%: 80%: 20%) …..………………………

$ 0

$100,000

$ 25,000

$ –

Sept. purchases ($240,000)—(0%: 80%: 20%) ….……………………….

–

0

192,000

48,000

Oct. purchases ($225,000)—(0%: 80%) …………………………..

–

–

0

180,000

Nov. purchases ($200,000)—(0%) …………………..………

–

–

–

0

Total …………………………………………………………….……………………..

$ 0

$100,000

$217,000

$228,000

Fundamental Accounting Principles, 21st Edition

1302

Problem 22-3A (70 minutes)

Part 1

Cash collections of credit sales (accounts receivable)

From sales in

Total

% Collected

June

July

April ………………………………….……

$ 720,000

28%

$201,600

May …………………………………..……

360,000

50

180,000

…………………………………..……

28

$100,800

June ………………………………….……

1,080,000

20

216,000

………………………………….……

50

540,000

July …………………………………..……

900,000

20

_______

180,000

Total collected …………………..……

$597,600

$820,800

Part 2

Budgeted ending inventories (in units)

April

May

June

July

Next month’s budgeted sales ………………...

2,000

6,000

5,000

3,800

Ratio of inventory to future sales …………...

20%

20%

20%

20%

Budgeted “base” ending inventory ………..

400

1,200

1,000

760

Plus safety stock…………………………………...

100

100

100

100

Budgeted ending inventory …………………...

500

1,300

1,100

860

Part 3

AZTEC COMPANY

Merchandise Purchases Budgets

For May, June, and July

May

June

July

Budgeted ending inventory (from part 2) …………

1,300

1,100

860

Add budgeted sales ……………………………………

2,000

6,000

5,000

Required units of available merchandise ….…

3,300

7,100

5,860

Deduct beginning inventory …………………….…

(500)

(1,300)

(1,100)

Budgeted purchases (units) …………………….…

2,800

5,800

4,760

Budgeted cost per unit …………………………….…

$110

$110

$110

Budgeted cost of merchandise purchases …..…

$308,000

$638,000

$523,600

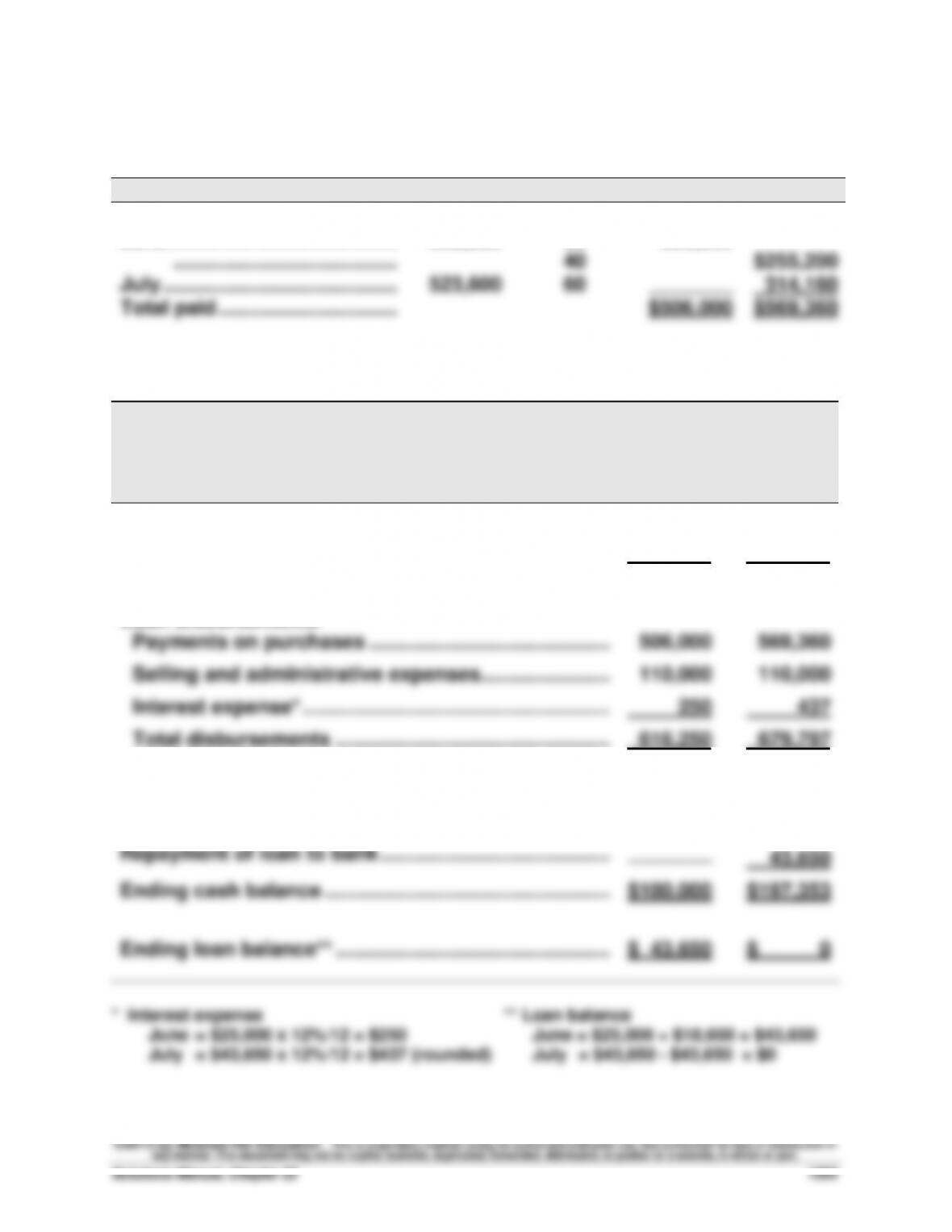

Problem 22-3A (Continued)

Part 4

Cash payments on product purchases (for June and July)

From purchases in

Total

% Paid

June

July

May …………………………………….…..

$308,000

40%

$123,200

June ………………………………………..

638,000

60

382,800

…………………………………..…..

40

$255,200

July …………………………………….…..

523,600

60

________

314,160

Total paid ………………………………..

$506,000

$569,360

Part 5

AZTEC COMPANY

Cash Budget

June and July

June

July

Beginning cash balance ………………………………………...

$100,000

$100,000

Cash receipts from customers ……………………………....

597,600

820,800

Total available cash ……………………………………………....

697,600

920,800

Cash disbursements

Payments on purchases ……………………………………...

506,000

569,360

Selling and administrative expenses …………………....

110,000

110,000

Interest expense* ………………………………………………...

250

437

Total disbursements …………………………………………...

616,250

679,797

Preliminary cash balance ……………………………………....

81,350

241,003

Additional loan from bank ……………………………………..

18,650

0

Repayment of loan to bank …………………………………....

________

43,650

Ending cash balance ……………………………………………..

$100,000

$197,353

Ending loan balance** …………………………………………...

$ 43,650

$ 0

* Interest expense ** Loan balance

June = $25,000 x 12%/12 = $250 June = $25,000 + $18,650 = $43,650

July = $43,650 x 12%/12 = $437 (rounded) July = $43,650 – $43,650 = $0

Fundamental Accounting Principles, 21st Edition

1304

Problem 22-3A (Concluded)

Part 6

Information about the need for cash in the near future would be helpful to

the management of Aztec Company because they would be able to enter

In addition, a good cash budget is likely to be helpful to management in

negotiating the terms of the loan. In this situation, the company can tell the

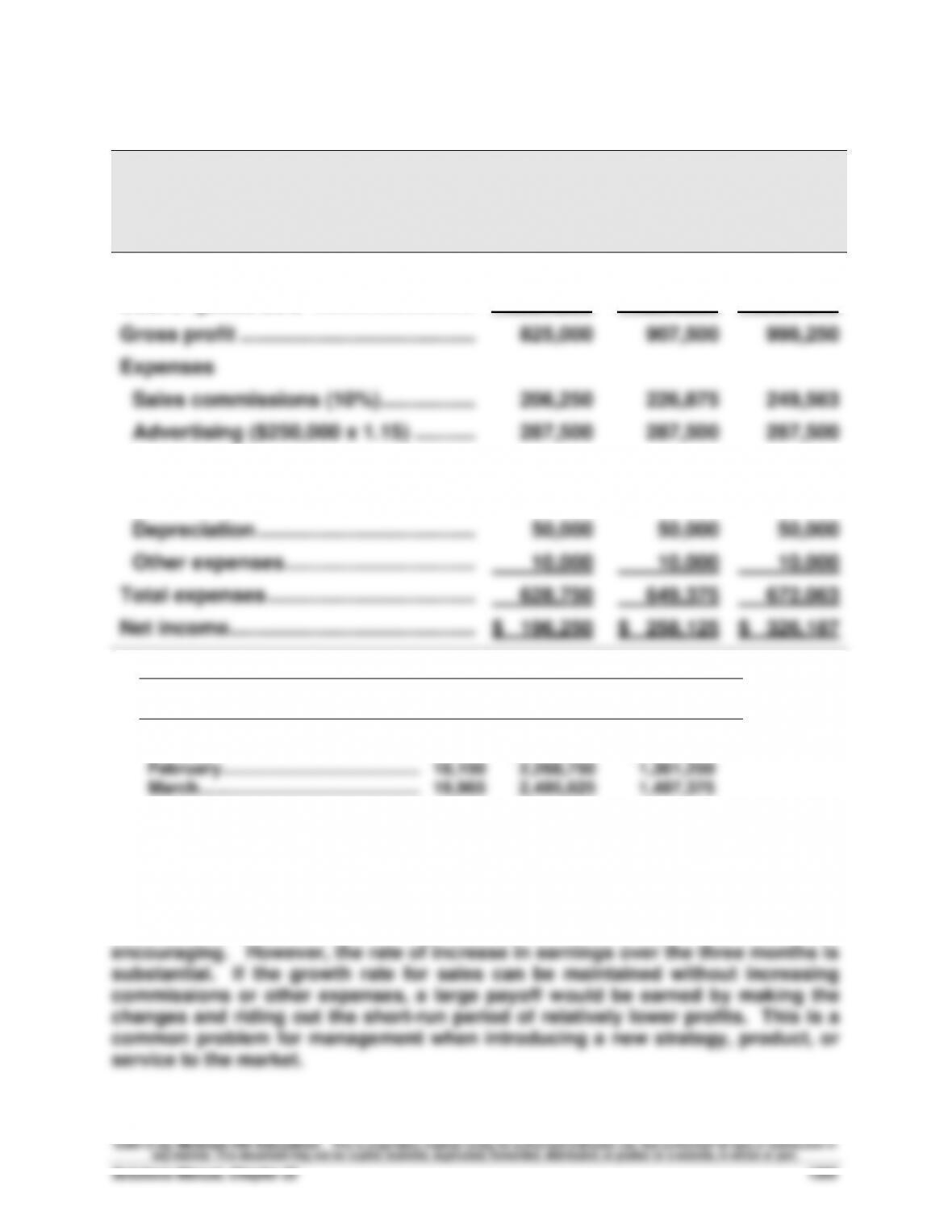

Problem 22-4A (50 minutes)

Part 1

MERLINE

Budgeted Income Statement

For Months of January, February, and March, 2014

January

February

March

Sales* …………………………………………….…

$2,062,500

$2,268,750

$2,495,625

Cost of goods sold* ………………………..…

1,237,500

1,361,250

1,497,375

Gross profit ………………………………………

825,000

907,500

998,250

Expenses

Sales commissions (10%) ……………..…

206,250

226,875

249,563

Advertising ($250,000 x 1.15) ………..…

287,500

287,500

287,500

Store rent ……………………………………..…

30,000

30,000

30,000

Administrative salaries ……………………

45,000

45,000

45,000

Depreciation ……………………………………

50,000

50,000

50,000

Other expenses …………………………….…

10,000

10,000

10,000

Total expenses …………………………..…..…

628,750

649,375

672,063

Net income ……………………………………..…

$ 196,250

$ 258,125

$ 326,187

* Volume for the next three months increases by 10% per month

Sales

Cost of Goods

Units

(@ $125)

Sold (@ $75)

December ($2,250,000/$150) …………………

15,000

January …………………………..……….…………

16,500

$2,062,500

$1,237,500

February …………………………………..…………

18,150

2,268,750

1,361,250

March ……………………………………….…………

19,965

2,495,625

1,497,375

Part 2: Analysis Component

The plan for increasing sales volume by reducing the price and increasing

advertising would cause the company to generate less net income in each of the

three months of the next quarter than was earned in December. This result is not

Fundamental Accounting Principles, 21st Edition

1306

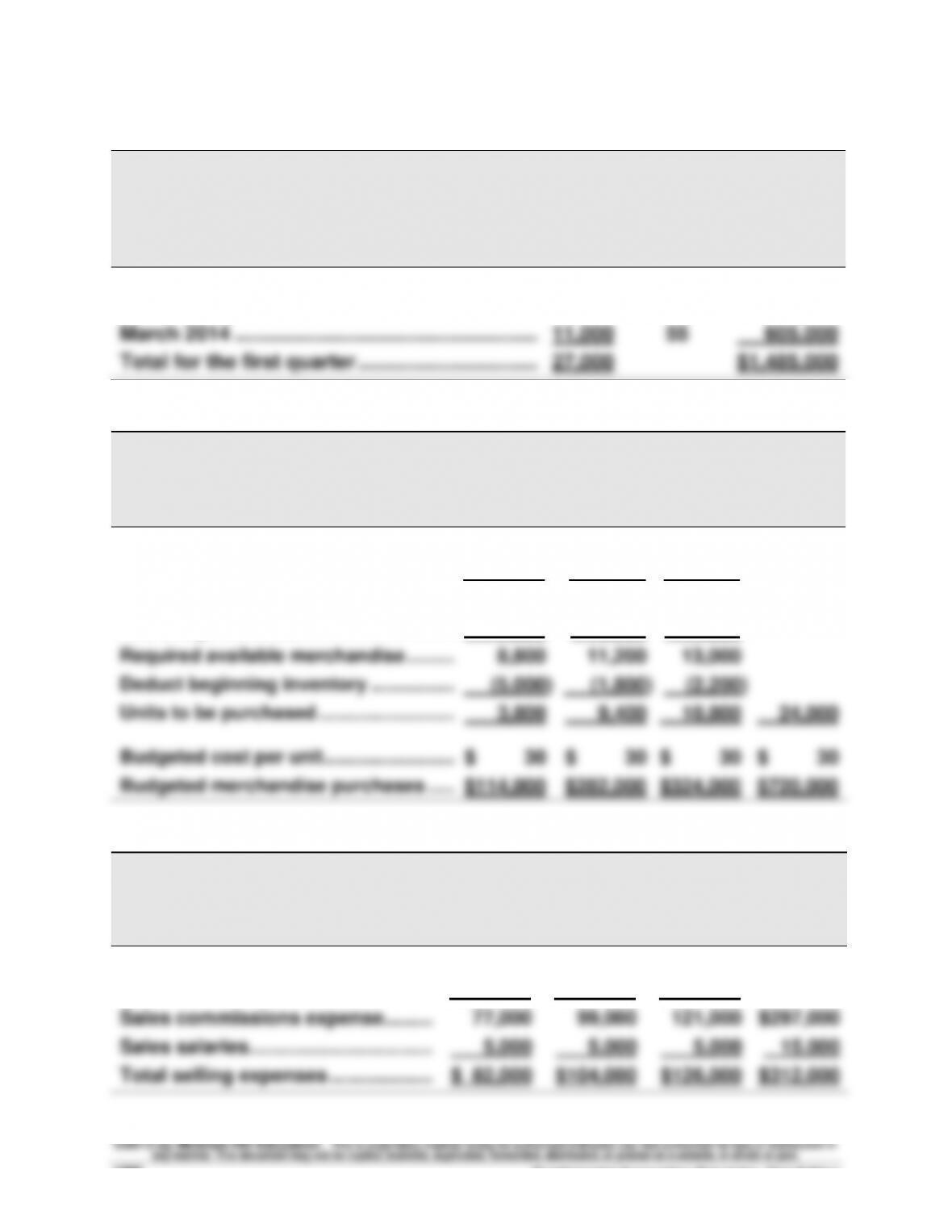

Problem 22-5A (130 minutes)

Part 1

DIMSDALE SPORTS CO.

Sales Budgets

January, February, and March 2014

Budgeted

Units

Budgeted

Unit Price

Budgeted

Total Dollars

January 2014 …………………………………………….….

7,000

$55

$ 385,000

February 2014……………………………………………….

9,000

55

495,000

March 2014 ……………………………………………….….

11,000

55

605,000

Total for the first quarter ……………………………….

27,000

$1,485,000

Part 2

DIMSDALE SPORTS CO.

Merchandise Purchases Budgets

January, February, and March 2014

January

February

March

Total

Next month’s budgeted sales …………...

9,000

11,000

10,000

Ratio of inventory to future sales ……...

x 20%

x 20%

x 20%

Budgeted ending inventory ……………...

1,800

2,200

2,000

Add budgeted sales ………………………….

7,000

9,000

11,000

Required available merchandise ……….

8,800

11,200

13,000

Deduct beginning inventory ……………..

(5,000)

(1,800)

(2,200)

Units to be purchased ……………………...

3,800

9,400

10,800

24,000

Budgeted cost per unit ……………………..

$ 30

$ 30

$ 30

$ 30

Budgeted merchandise purchases …...

$114,000

$282,000

$324,000

$720,000

Part 3

DIMSDALE SPORTS CO.

Selling Expense Budgets

January, February, and March 2014

January

February

March

Total

Budgeted sales …………………………..

$385,000

$495,000

$605,000

Sales commission percent ………….…..

x 20%

x 20%

x 20%

Sales commissions expense ……….…..

77,000

99,000

121,000

$297,000

Sales salaries……………………………..…..

5,000

5,000

5,000

15,000

Total selling expenses ………………..…..

$ 82,000

$104,000

$126,000

$312,000

Problem 22-5A (Continued)

Part 4

DIMSDALE SPORTS CO.

General and Administrative Expense Budgets

January, February, and March 2014

January

February

March

Total

Salaries ………………………………………..……..

$12,000

$12,000

$12,000

$36,000

Maintenance ………………………………………..

2,000

2,000

2,000

6,000

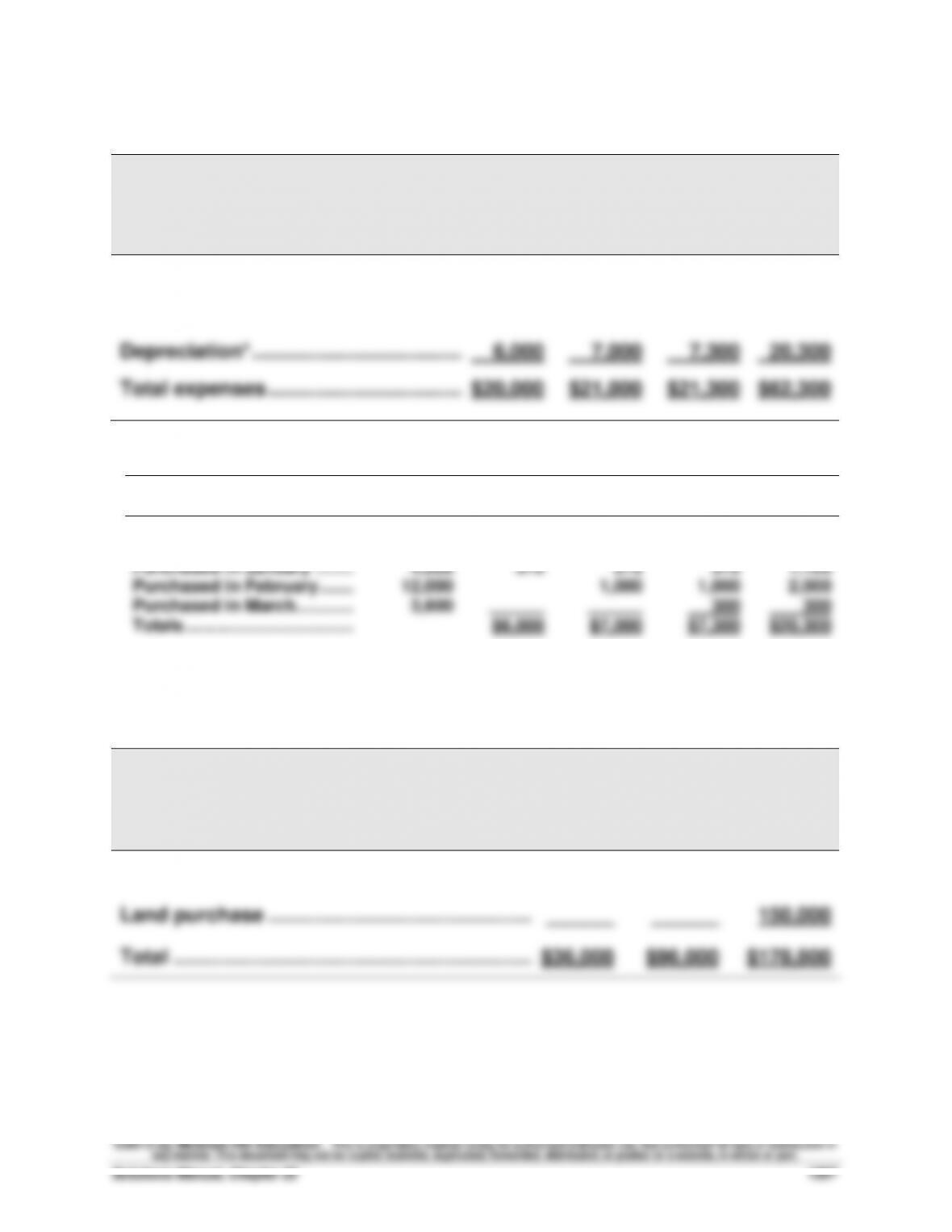

Depreciation* ………………………………..……..

6,000

7,000

7,300

20,300

Total expenses …………………………..………..

$20,000

$21,000

$21,300

$62,300

* Depreciation expense calculations

Annual

Amount

January

February

March

Total

Equipment owned

on 12/31/2013 ………………..

$67,500

$5,625

$5,625

$5,625

$16,875

Purchased in January ……..

4,500

375

375

375

1,125

Purchased in February …….

12,000

1,000

1,000

2,000

Purchased in March …………

3,600

______

______

300

300

Totals …………………………..…

$6,000

$7,000

$7,300

$20,300

Part 5

DIMSDALE SPORTS CO.

Capital Expenditures Budgets

January, February, and March 2014

January

February

March

Equipment purchases ……………………………..……

$36,000

$96,000

$ 28,800

Land purchase ………………………………………..……

______

______

150,000

Total ……………………………………………………….

$36,000

$96,000

$178,800