Title: Serial Problem SP 1

QA_Ori:

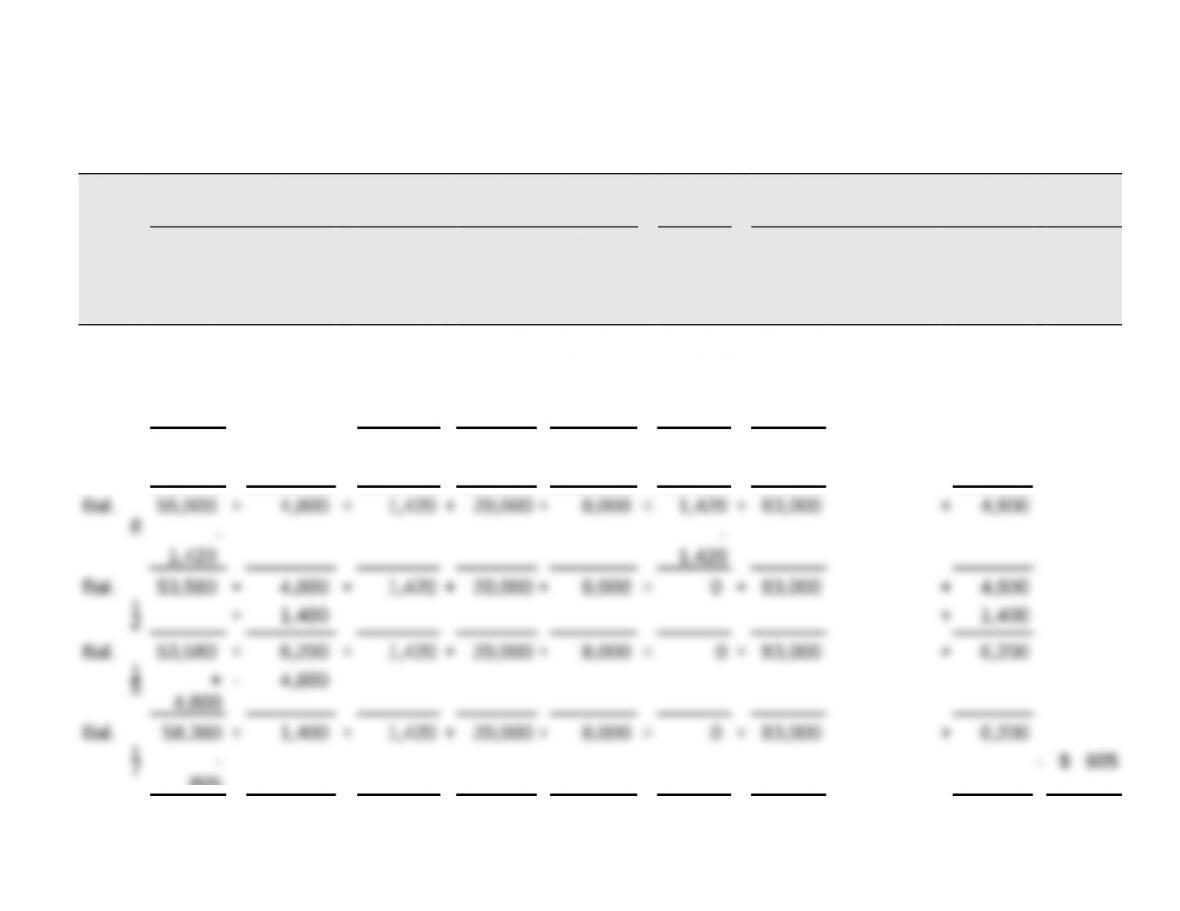

Assets = Liabiliti

es

+ Equity

Date Cash + Accounts

Receivab

le

+ Comput

er

Supplies

+ Comput

er

System

+ Office

Equipme

nt

= Accoun

ts

Payabl

e

+ A.

Lopez,

Capital

– A. Lopez,

Withdraw

als

+ Revenu

es

– Expens

es

Oct

.

1+

$55,000

$20,000 + $8,000 + $83,000

3 + $1,420 +

$1,420

Bal. 55,000 + 1,420 + 20,000 + 8,000 = 1,420 + 83,000

6 + $4,800 + $ 4,800

Bal. 57,575 + 1,400 + 1,420 + 20,000 + 8,000 = 0 + 83,000 + 6,200 – 805

2

0–

1,940

– 1,940

Bal. 55,635 + 1,400 + 1,420 + 20,000 + 8,000 = 0 + 83,000 + 6,200 – 2,745

2

2+

1,400

– 1,400

Title: Reporting in Action 1

QA_Ori:

An organization’s total assets are equal to its total liabilities plus total equity.

Title: Reporting in Action 2

QA_Ori:

Return on assets is net income divided by the average total assets invested.

Title: Reporting in Action 3

QA_Ori:

We know that net income equals total revenues less total expenses. For Polaris,

Title: Reporting in Action 4

QA_Ori:

Title: Reporting in Action 5

QA_Ori:

Title: Comparative Analysis

QA_Ori:

($ thousands) Polaris Arctic Cat

1. Total assets =

Liabilities + Equity $1,228,024 $272,906

2. Return on assets $227,575 $13,007

[($1,061,647 +

$1,228,024)/2]

[($246,084 + $272,906)/2]

19.9% 5.0%

3.

Revenues-Expense

s

= Net income

4. Analysis of return on assets: Polaris’s 19.9% return is good given the moderate risk Polaris confronts

5. Analysis conclusions:

Arctic Cat’s return is undesirable (poor when compared to the industry norm);

Title: Ethics Challenge 1

QA_Ori:

There are several parties affected. They include the users of financial

Title: Ethics Challenge 2

QA_Ori:

A major factor in the value of an auditor’s report is the auditor’s independence.

Title: Ethics Challenge

QA_Ori:

Thorne should not accept this fee arrangement. To avoid compromising the

auditor’s independence, Thorne should reject it. (Further, the AICPA Code of

Title: Ethics Challenge

QA_Ori:

Ethical considerations guiding this decision include the potential harm to

affected parties by allowing such a fee arrangement to exist. The

unacceptable nature of such a fee arrangement guards the profession against

unethical actions that could undermine its real and perceived value to society.

Title: Communicating in Practice 1

QA_Ori:

Deciding whether Twitter is a good loan risk can be difficult because the

planned expansion is risky if customer demand does not meet expectations.

Title: Communicating in Practice 2

QA_Ori:

How the company is organized is important to a loan officer. If it is a

pro-proprietorship (and not LLC), the personal assets of the owners are

Title: Taking It to the Net

QA_Ori:

1.

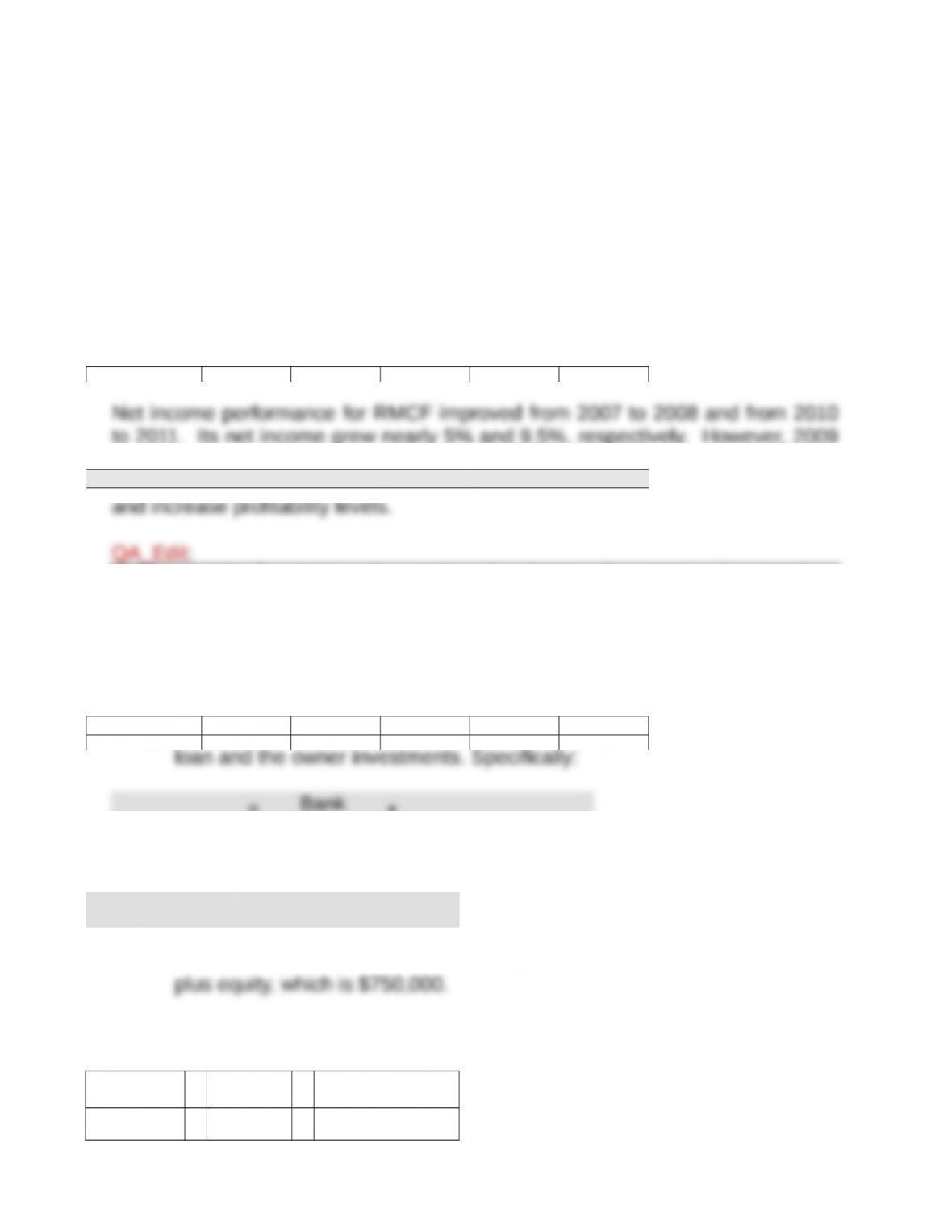

(in thousands) 2011 2010 2009 2008 2007

Revenues…………. $31,128 $28,437 $28,539 $31,878 $31,573

through 2008, declined in the recessionary period of 2008 through 2010, and

began to increase from 2010 to 2011. Management must work to continue a

trend of increasing revenues.

QA_Edit:

(in thousands) 2011 2010 2009 2008 2007

QA_Ori:

2.

(in thousands) 2011 2010 2009 2008 2007

Net income performance for RMCF improved from 2007 to 2008 and from 2010

to 2011. Its net income grew nearly 5% and 9.5%, respectively. However, 2009

and 2010 net income declined 25% and 4%, respectively.. Although 2009 and

2010 were recessionary times, management must continue to work to sustain

and increase profitability levels.

QA_Edit:

(in thousands) 2011 2010 2009 2008 2007

Title: Entrepreneurial Decision 1

QA_Ori:

(a) AccounTwit’s total amount of liabilities and equity consists of the bank

loan and the owner investments. Specifically:

Total assets =

Bank

Loan +

Owner investment

=

Liabilities +

Equity

(b) AccounTwit’s total amount of assets equals its total amount of liabilities

plus equity, which is $750,000.

Total assets =

Bank

Loan +

Owner investment

=

Liabilities +

Equity

Title: Entrepreneurial Decision 3

QA_Ori:

AccounTwit’s 10.7% return slightly exceeds its competitors’ average return of

Title: Global Decision 1

QA_Ori:

KTM’s net income and revenues figures are computed using Euros, which is

Moreover, KTM’s figures are computed according to International Financial

Reporting Standards (IFRS) following pronouncements of the IASB, while

Title: Global Decision 1

QA_Ori:

KTM’s return on assets ratio eliminates differences in monetary units (between

However, any comparisons using the return on assets ratio are still impacted