92. Mach Co. operates three production departments as profit centers. The following

information is available for its most recent year. Department 1’s contribution to overhead as a

percent of sales is:

Cost of Direct Indirect

Dept. Sales Goods Sold Expenses Expenses

1 $1,000,000 $700,000 $100,000 $ 80,000

2 400,000 150,000 40,000 100,000

3 700,000 300,000 150,000 20,000

A. 8%.

B. 40%.

C. 20%.

D. 30%.

E. 12%.

93. Mach Co. operates three production departments as profit centers. The following

information is available for its most recent year. Which department has the greatest

departmental contribution to overhead and what is the amount contributed?

Cost of Direct Indirect

Dept. Sales Goods Sold Expenses Expenses

1 $1,000,000 $700,000 $100,000 $ 80,000

2 400,000 150,000 40,000 100,000

3 700,000 300,000 150,000 20,000

A. Dept. 3; $ 400,000.

B. Dept. 1; $1,000,000.

C. Dept. 2; $ 100,000.

D. Dept. 3; $ 250,000.

E. Dept. 2; $ 150,000.

94. For an investment center, the hurdle rate is:

A. The cost of obtaining financing.

B. The desired return on investments.

C. The difference between the projected rate and the earned rate.

D. Not evaluated in determining the performance of an investment center.

E. Not important to management.

24–43

95. A system of performance measures, including nonfinancial measures, used to assess

company and division manager performance is:

A. Hurdle rate.

B. Return on investment.

C. Balanced scorecard.

D. Residual income.

E. Investment turnover.

96. Abbe Company reported the following financial numbers for one of its divisions for the

year; average total assets of $4,100,000; sales of $4,525,000; cost of goods sold of

$2,550,000; and operating expenses of $1,372,000. Compute the division’s return on assets:

A. 30.3%.

B. 23.6%.

C. 13.3%.

D. 10.4%.

E. 14.7%.

97. Abbe Company reported the following financial numbers for one of its divisions for the

year; average total assets of $4,100,000; sales of $4,525,000; cost of goods sold of

$2,550,000; and operating expenses of $1,372,000. Assume a target income of 10% of

average invested assets. Compute residual income for the division:

A. $203,000.

B. $193,000.

24–44

C. $150,500.

D. $ 60,300.

E. $197,500.

98. Yoho Company reported the following financial numbers for one of its divisions for the

year; average total assets of $5,800,000; sales of $5,375,000; cost of goods sold of

$3,225,000; and operating expenses of $1,147,000. Compute the division’s return on assets:

A. 18.6%.

B. 21.3%.

C. 17.3%.

D. 10.4%.

E. 14.7%.

99. Yoho Company reported the following financial numbers for one of its divisions for the

year; average total assets of $5,800,000; sales of $5,375,000; cost of goods sold of

$3,225,000; and operating expenses of $1,147,000. Assume a target income of 15% of

average invested assets. Compute residual income for the division:

A. $150,450.

B. $196,750.

C. $150,500.

D. $133,000.

E. $100,300.

100. Belgrade Lakes Properties is developing a golf course subdivision that includes 225

home lots; 100 lots are golf course lots and will sell for $95,000 each; 125 are street frontage

lots and will sell for $65,000. The developer acquired the land for $1,800,000 and spent

another $1,400,000 on street and utilities improvement. Compute the amount of joint cost to

be allocated to the golf course lots using value basis.

A. $1,724,800.

B. $1,777,920.

C. $2,018,920.

D. $1,422,080.

E. $1,475,200.

101. Belgrade Lakes Properties is developing a golf course subdivision that includes 225

home lots; 100 lots are golf course lots and will sell for $95,000 each; 125 are street frontage

lots and will sell for $65,000. The developer acquired the land for $1,800,000 and spent

another $1,400,000 on street and utilities improvement. Compute the amount of joint cost to

be allocated to the street frontage lots using value basis.

A. $1,724,800.

B. $1,777,920.

C. $2,018,920.

D. $1,422,080.

E. $1,475,200.

102. The following is a partially completed lower section of a departmental expense

allocation spreadsheet for Stoneham. It reports the total amounts of direct and indirect

expenses for the four departments. Purchasing department expenses are allocated to the

operating departments on the basis of purchase orders. Maintenance department expenses are

allocated based on square footage. Compute the amount of Purchasing department expense to

be allocated to Fabrication.

Purchasing Maintenance Fabrication Assembly

Operating costs $32,000 $18,000 $96,000 $62,000

No. of purchase orders 16 4

Sq. ft. of space 3,300 2,700

A. $6,400.

B. $9,900.

C. $8,100.

D. $17,600.

E. $25,600.

103. The following is a partially completed lower section of a departmental expense

allocation spreadsheet for Stoneham. It reports the total amounts of direct and indirect

expenses for the four departments. Purchasing department expenses are allocated to the

operating departments on the basis of purchase orders. Maintenance department expenses are

allocated based on square footage. Compute the amount of Purchasing department expense to

be allocated to Assembly.

Purchasing Maintenance Fabrication Assembly

Operating costs $32,000 $18,000 $96,000 $62,000

No. of purchase orders 16 4

Sq. ft. of space 3,300 2,700

A. $6,400.

B. $9,900.

C. $8,100.

D. $14,400.

E. $25,600.

24–48

104. The following is a partially completed lower section of a departmental expense

allocation spreadsheet for Stoneham. It reports the total amounts of direct and indirect

expenses for the four departments. Purchasing department expenses are allocated to the

operating departments on the basis of purchase orders. Maintenance department expenses are

allocated based on square footage. Compute the amount of Maintenance department expense

to be allocated to Fabrication.

Purchasing Maintenance Fabrication Assembly

Operating costs $32,000 $18,000 $96,000 $62,000

No. of purchase orders 16 4

Sq. ft. of space 3,300 2,700

A. $6,400.

B. $9,900.

C. $8,100.

D. $9,000.

E. $25,600.

105. The following is a partially completed lower section of a departmental expense

allocation spreadsheet for Stoneham. It reports the total amounts of direct and indirect

expenses for the four departments. Purchasing department expenses are allocated to the

operating departments on the basis of purchase orders. Maintenance department expenses are

allocated based on square footage. Compute the amount of Maintenance department expense

to be allocated to Fabrication.

Purchasing Maintenance Fabrication Assembly

Operating costs $32,000 $18,000 $96,000 $62,000

No. of purchase orders 16 4

Sq. ft. of space 3,300 2,700

A. $6,400.

B. $9,900.

C. $8,100.

D. $9,000.

E. $25,600.

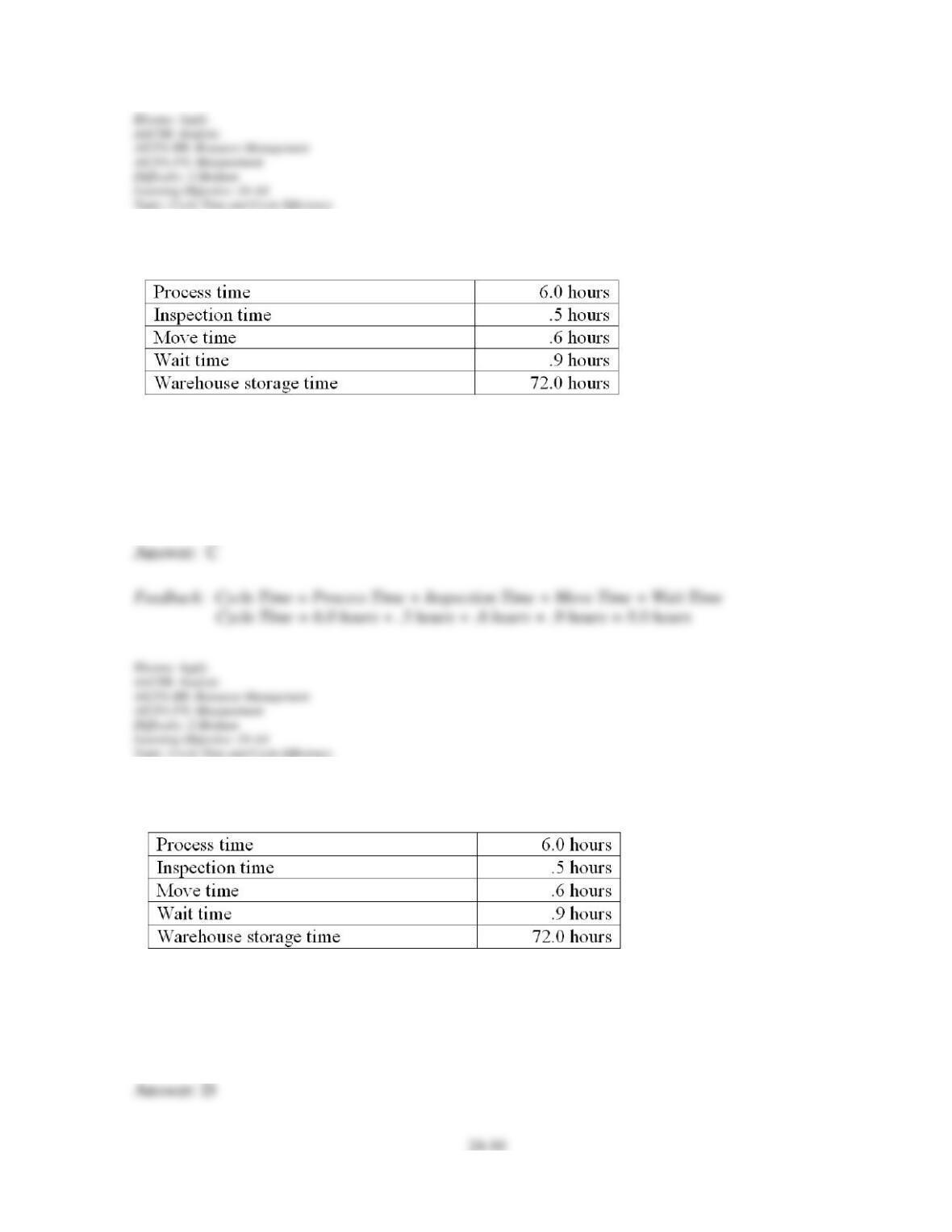

106. Which of the following represents the correct formula for calculating cycle time for a

manufacturer?

A. Process time + inspection time – move time – wait time.

B. Process time – inspection time + move time + wait time.

C. Process time + inspection time + move time + wait time.

D. Process time – inspection time – move time – wait time.

E. Process time + inspection time + move time – wait time.

107. Which of the following statements is correct concerning the elements of cycle time?

A. Move time is the time spent moving (1) raw materials from storage to production and (2)

goods in process from one factory location to another factory location.

B. Inspection time is the time spent producing the product.

C. Process time is considered non-value-added time.

D. Wait time is considered value-added time.

E. Cycle efficiency is the ratio of non-value-added time to total cycle time.

108. Using the information below, compute the manufacturing cycle time:

A. 7.5 hours.

B. 6.5 hours.

C. 8.0 hours.

D. 80.0 hours.

E. 7.1 hours.

109. Using the information below, compute the cycle efficiency:

A. 93.8%.

B. 81.3%.

C. 100.0%.

D. 75.0%.

E. 88.8%.

110. When the selling division in an internal transfer has unsatisfied demand from outside

customers for the product that is being transferred, then the lowest acceptable transfer price as

far as the selling division is concerned is:

A. variable cost of producing a unit of product.

B. the full absorption cost of producing a unit of product.

C. the market price charged to outside customers, less costs saved by transferring internally.

D. the amount that the purchasing division would have to pay an outside seller to acquire a

similar product for its use.

E. all the costs of producing a unit of product.

111. Division X makes a part that it sells to customers outside of the company. Data

concerning this part appear below:

Division Y of the same company would like to use the part manufactured by Division X in

one of its products. Division Y currently purchases a similar part made by an outside

company for $70 per unit and would substitute the part made by Division X. Division Y

requires 5,000 units of the part each period. Division X can already sell all of the units it can

produce on the outside market. What should be the lowest acceptable transfer price from the

perspective of Division X?

A. $75

B. $66

C. $16

D. $50

E. $25

112. Part WY4 costs the Eastern Division of Tyble Corporation $26 to make-direct materials

are $10, direct labor is $4, variable manufacturing overhead is $9, and fixed manufacturing

overhead is $3. Eastern Division sells Part WY4 to other companies for $30. The Western

Division of Tyble Corporation can use Part WY4 in one of its products. The Eastern Division

has enough idle capacity to produce all of the units of Part WY4 that the Western Division

would require. What is the lowest transfer price at which the Eastern Division should be

willing to sell Part WY4 to the Central Division?

A. $30

B. $26

C. $23

D. $27

E. $21

113. Division P of Turbo Corporation has the capacity for making 75,000 wheel sets per year

and regularly sells 60,000 each year on the outside market. The regular sales price is $100 per

wheel set, and the variable production cost per unit is $65. Division Q of Turbo Corporation

currently buys 30,000 wheel sets (of the kind made by Division P) yearly from an outside

supplier at a price of $90 per wheel set. If Division Q were to buy the 30,000 wheel sets it

needs annually from Division P at $87 per wheel set, the change in annual net operating

income for the company as a whole, compared to what it is currently, would be:

A. $600,000

B. $225,000

C. $750,000

D. $135,000

E. $700,000

114. Division X makes a part that it sells to customers outside of the company. Data

concerning this part appear below:

Division Y of the same company would like to use the part manufactured by Division X in

one of its products. Division Y currently purchases a similar part made by an outside

company for $49 per unit and would substitute the part made by Division X. Division Y

requires 5,000 units of the part each period. Division X has ample excess capacity to handle

all of Division Y’s needs without any increase in fixed costs and without cutting into outside

sales. According to the formula in the text, what is the lowest acceptable transfer price from

the standpoint of the selling division?

A. $50

B. $49

C. $46

D. $30

E. $20

115. Division A makes a part that it sells to customers outside of the company. Data

concerning this part appear below:

Division B of the same company would like to use the part manufactured by Division A in

one of its products. Division B currently purchases a similar part made by an outside company

for $38 per unit and would substitute the part made by Division A. Division B requires 5,000

units of the part each period. Division A has ample capacity to produce the units for Division

B without any increase in fixed costs and without cutting into sales to outside customers. If

Division A sells to Division B rather than to outside customers, the variable cost be unit

would be $1 lower. What should be the lowest acceptable transfer price from the perspective

of Division A?

A. $40

B. $38

C. $30

D. $29

E. $10

116. The Milk Chocolate Division of Mmmm Foods, Inc. had the following operating results

last year:

Milk Chocolate expects identical operating results this year. The Milk Chocolate Division has

the ability to produce and sell 200,000 pounds of chocolate annually. Assume that the Peanut

Butter Division of Mmmm Foods wants to purchase an additional 20,000 pounds of chocolate

from the Milk Chocolate Division. Milk Chocolate will be able to increase its profit by

accepting any transfer price above:

A. $0.40 per pound

B. $0.08 per pound

C. $0.15 per pound

D. $0.25 per pound

E. $0.10 per pound

117. The Milk Chocolate Division of Mmmm Foods, Inc. had the following operating results

last year:

Milk Chocolate expects identical operating results this year. The Milk Chocolate Division has

the ability to produce and sell 200,000 pounds of chocolate annually. Assume that the Peanut

Butter Division of Mmmm Foods wants to purchase an additional 20,000 pounds of chocolate

from the Milk Chocolate Division. Assume that the Milk Chocolate Division is currently

operating at its capacity of 200,000 pounds of chocolate. Also assume again that the Peanut

Butter Division wants to purchase an additional 20,000 pounds of chocolate from Milk

Chocolate. Under these conditions, what amount per pound of chocolate would Milk

Chocolate have to charge Peanut Butter in order to maintain its current profit?

A. $0.40 per pound

B. $0.08 per pound

C. $0.15 per pound

D. $0.25 per pound

E. $0.30 per pound

118. Division X makes a part with the following characteristics:

Division Y of the same company would like to purchase 10,000 units each period from

Division X. Division Y now purchases the part from an outside supplier at a price of $17

each. Suppose Division X has ample excess capacity to handle all of Division Y’s needs

without any increase in fixed costs and without cutting into sales to outside customers. If

Division X refuses to accept the $17 price internally and Division Y continues to buy from the

outside supplier, the company as a whole will be:

A. worse off by $70,000 each period.

B. better off by $10,000 each period.

C. worse off by $60,000 each period.

D. worse off by $20,000 each period.

E. better off by $60,000 each period.

24–59

119. Division A produces a part with the following characteristics:

Division B, another division in the company, would like to buy this part from Division A.

Division B is presently purchasing the part from an outside source at $28 per unit. If Division

A sells to Division B, $1 in variable costs can be avoided. Suppose Division A is currently

operating at capacity and can sell all of the units it produces on the outside market for its

usual selling price. From the point of view of Division A, any sales to Division B should be

priced no lower than:

A. $27

B. $29

C. $20

D. $28

E. $21

120. Match the appropriate definition with the following terms:

24–60

(a) A department or unit that incurs costs without directly generating revenues.

(b) A center in which a manager is responsible for using the center’s assets to generate income

for the center.

(c) Costs that are incurred for the joint benefit of more than one department and cannot be

readily traced to only one department.

(d) Costs readily traced to a specific department because they are incurred for the sole benefit

of that department.

(e) Costs incurred to produce two or more products at the same time.

(f) Costs which a manager can strongly influence or control.

(g) A department that incurs costs and generates revenues.

__________ (1) Direct expenses

__________ (2) Profit center

__________ (3) Controllable costs

__________ (4) Indirect expenses

__________ (5) Cost center

__________ (6) Joint cost

__________ (7) Investment center

121. Match the appropriate definition a through h with the following terms:

(a) A department whose manager is judged on the ability to generate revenues in excess of the

department’s costs.

(b) A center whose manager is responsible for using the center’s assets to generate income for

the center.

(c) Provides information that management can use to evaluate the performance of a

department’s managers.

(d) Compares actual and budgeted costs and expenses under the control of a manager.

(e) A department whose manager is judged on the ability to control costs by keeping them

within a satisfactory range.

(f) Departmental sales in excess of its direct costs and expenses.