Problem 4-2A (Continued)

Part 7—continued

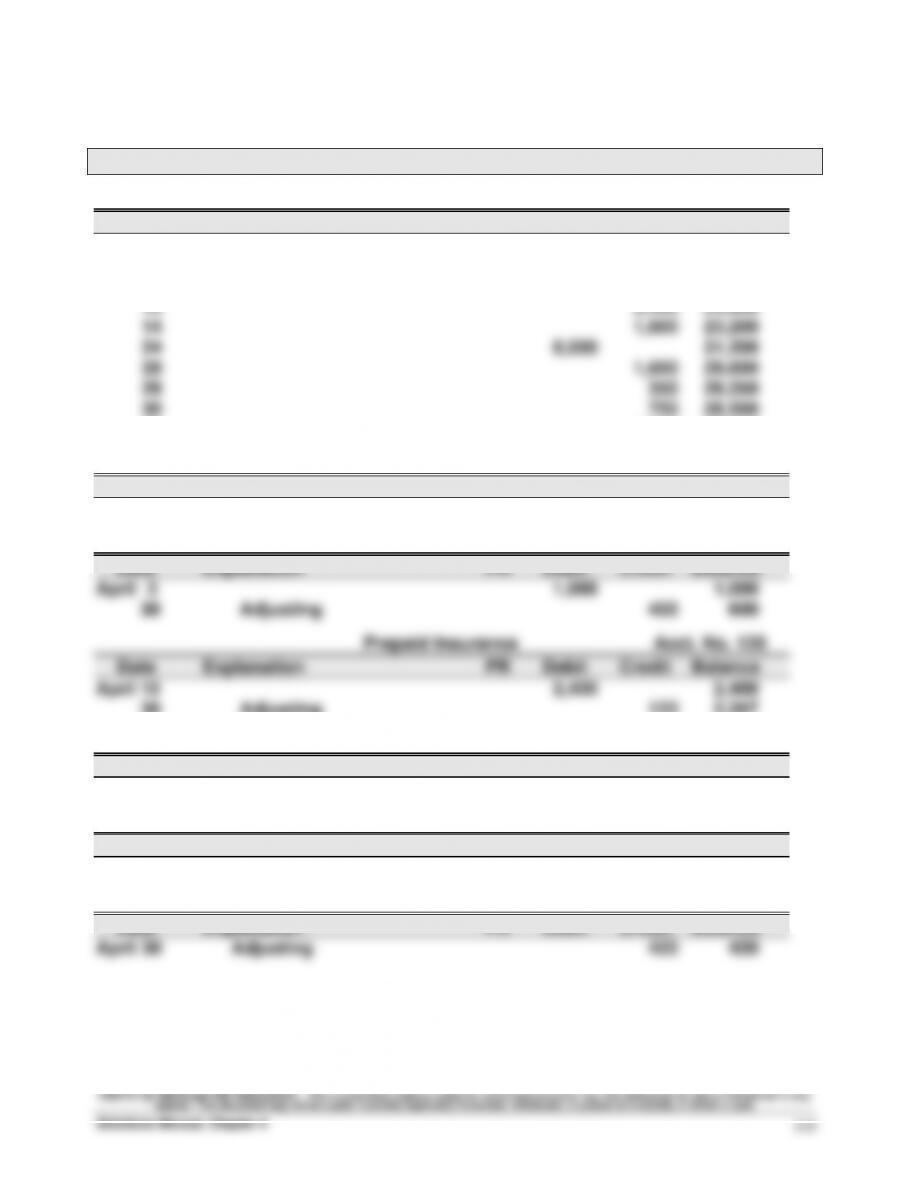

Ledger as of April 30

Cash Acct. No. 101

Date Explanation PR Debit Credit Balance

April 1 30,000 30,000

2 1,800 28,200

3 1,000 27,200

30 1,500 27,000

Accounts Receivable Acct. No. 106

Date Explanation PR Debit Credit Balance

April 30 Adjusting 1,750 1,750

Office Supplies Acct. No. 124

30 Adjusting 133 2,267

Computer Equipment Acct. No. 167

Date Explanation PR Debit Credit Balance

April 1 20,000 20,000

Accumulated Depreciation–Computer Equipment Acct. No. 168

Date Explanation PR Debit Credit Balance

April 30 Adjusting 500 500

Salaries Payable Acct. No. 209

Date Explanation PR Debit Credit Balance

Problem 4-2A (Continued)

J. Nozomi, Capital Acct. No. 301

Date Explanation PR Debit Credit Balance

J. Nozomi, Withdrawals Acct. No. 302

Date Explanation PR Debit Credit Balance

April 30 1,500 1,500

30 Closing 1,500 0

Commissions Earned Acct. No. 405

Date Explanation PR Debit Credit Balance

Depreciation Expense–Computer Equipment Acct. No. 612

Date Explanation PR Debit Credit Balance

April 30 Adjusting 500 500

30 Closing 500 0

Salaries Expense Acct. No. 622

Date Explanation PR Debit Credit Balance

Insurance Expense Acct. No. 637

Date Explanation PR Debit Credit Balance

April 30 Adjusting 133 133

30 Closing 133 0

Rent Expense Acct. No. 640

Date Explanation PR Debit Credit Balance

Office Supplies Expense Acct. No. 650

Date Explanation PR Debit Credit Balance

April 30 Adjusting 400 400

30 Closing 400 0

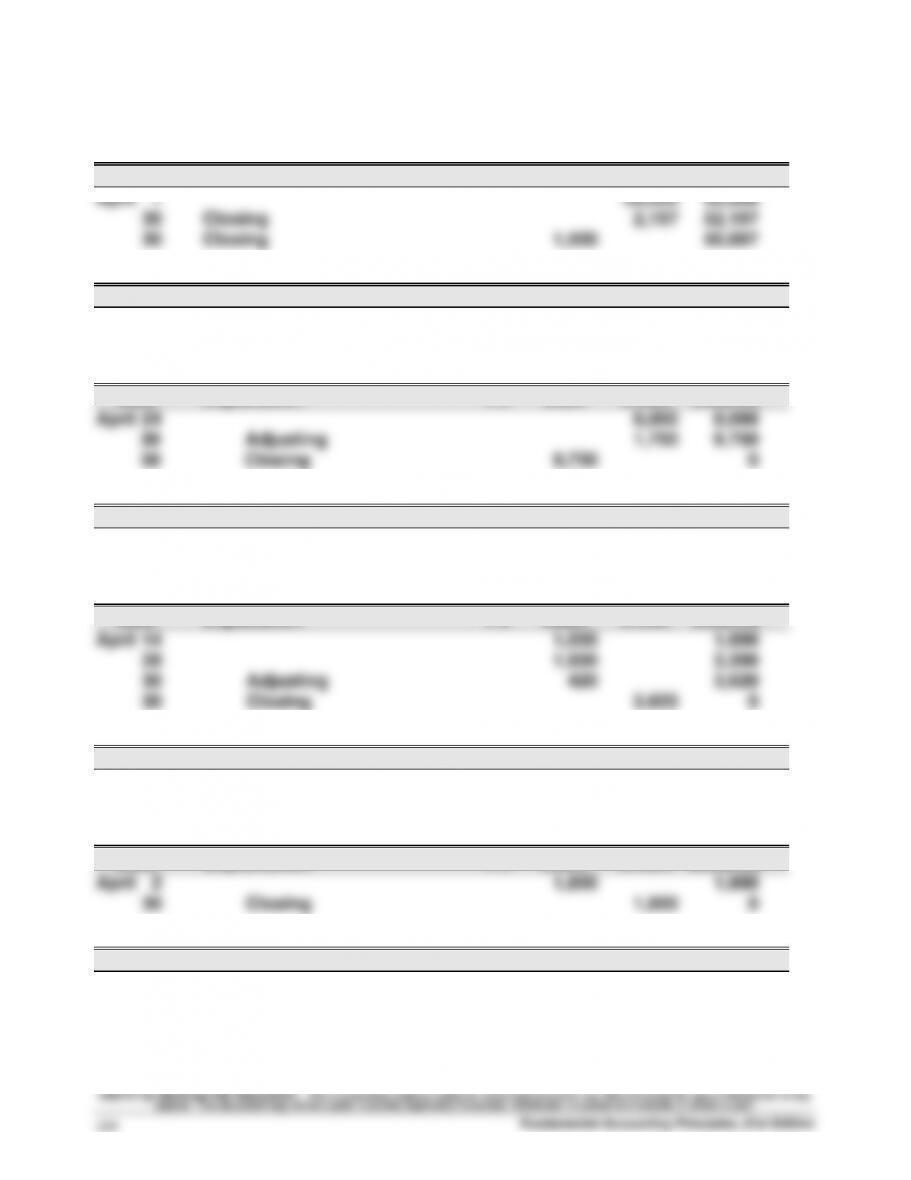

Problem 4-2A (Concluded)

Repairs Expense Acct. No. 684

Date Explanation PR Debit Credit Balance

Telephone Expense Acct. No. 688

Date Explanation PR Debit Credit Balance

April 30 750 750

30 Closing 750 0

Income Summary Acct. No. 901

Date Explanation PR Debit Credit Balance

©2013 by McGraw–Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned,

duplicated, forwarded, distributed, or posted on a website, in whole or part.

Fundamental Accounting Principles, 21st Edition

228

Problem 4-3A (90 minutes) Part 1

ACE CONSTRUCTION CO.

Work Sheet

For Year Ended June 30, 2013

Unadjusted

Trial Balance

Adjustments

Adjusted

Trial Balance

Income

Statement

Balance Sheet

No.

Account Title

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

101

Cash ………………………………………………………

18,500

18,500

18,500

126

Supplies ……………………………………..…………

9,900

(a)

6,600

3,300

3,300

128

Prepaid insurance …………………………..

7,200

(b)

3,800

3,400

3,400

167

Equipment ……………………………………………

132,000

132,000

132,000

168

Accumulated depreciation—

Equipment …………………………………..…………

26,250

(c)

8,400

34,650

34,650

201

Accounts payable …………………………..

6,800

(d)

650

7,450

7,450

203

Interest payable ………………………..…

(h)

250

250

250

208

Rent payable ……………………………..…………

(f)

500

500

500

210

Wages payable …………………………..

(e)

1,800

1,800

1,800

213

Property taxes payable …………..…………

(g)

1,000

1,000

1,000

251

Long–term notes payable …………………

25,000

25,000

25,000

301

V. Ace, Capital …………………………..

88,660

88,660

88,660

302

V. Ace, Withdrawals ………………..…………

33,000

33,000

33,000

401

Construction fees earned …………………

132,100

132,100

132,100

612

Depreciation expense—

Equipment ……………………………….…………

(c)

8,400

8,400

8,400

623

Wages expense ……………………….….

46,860

(e)

1,800

48,660

48,660

633

Interest expense ……………………….….

2,750

(h)

250

3,000

3,000

637

Insurance expense ………………….……….

(b)

3,800

3,800

3,800

640

Rent expense ………………………………………

12,000

(f)

500

12,500

12,500

652

Supplies expense …………………….…….

(a)

6,600

6,600

6,600

683

Property taxes expense ………….…………

7,800

(g)

1,000

8,800

8,800

684

Repairs expense …………………………..

2,910

2,910

2,910

690

Utilities expense ……………………….….

5,890

______

(d)

650

_____

6,540

______

6,540

______

______

______

Totals…………………………………………..…………

278,810

278,810

23,000

23,000

291,410

291,410

101,210

132,100

190,200

159,310

Net Income ………………………………..…………

30,890

______

______

30,890

Totals…………………………………………..…………

132,100

132,100

190,200

190,200

Problem 4-3A (Continued)

Part 2 Adjusting entries (all dated June 30, 2013)

Instructor note: Entries are shown without an account reference column because no posting is required.

(a) Supplies Expense ………………………………………. 6,600

Supplies ……………………………………………… 6,600

To record consumption of supplies.

(f) Rent Expense …………………………………………….. 500

Rent Payable ………………………………………. 500

To record remainder of annual rent.

(g) Property Taxes Expense …………………………….. 1,000

Property Taxes Payable ………………………. 1,000

To record additional property taxes.

Problem 4-3A (Continued)

Closing entries (all dated June 30, 2013)

Instructor note: Entries are shown without an account reference column because no posting is required.

(1) Construction Fees Earned ……………………… 132,100

Income Summary ……………………………. 132,100

To close the revenue account.

(2) Income Summary ………………………………….. 101,210

Depreciation Expense–Equipment …… 8,400

Wages Expense………………………………. 48,660

(3) Income Summary ………………………………….. 30,890

V. Ace, Capital ………………………………… 30,890

To close the Income Summary account.

Problem 4-3A (Continued)

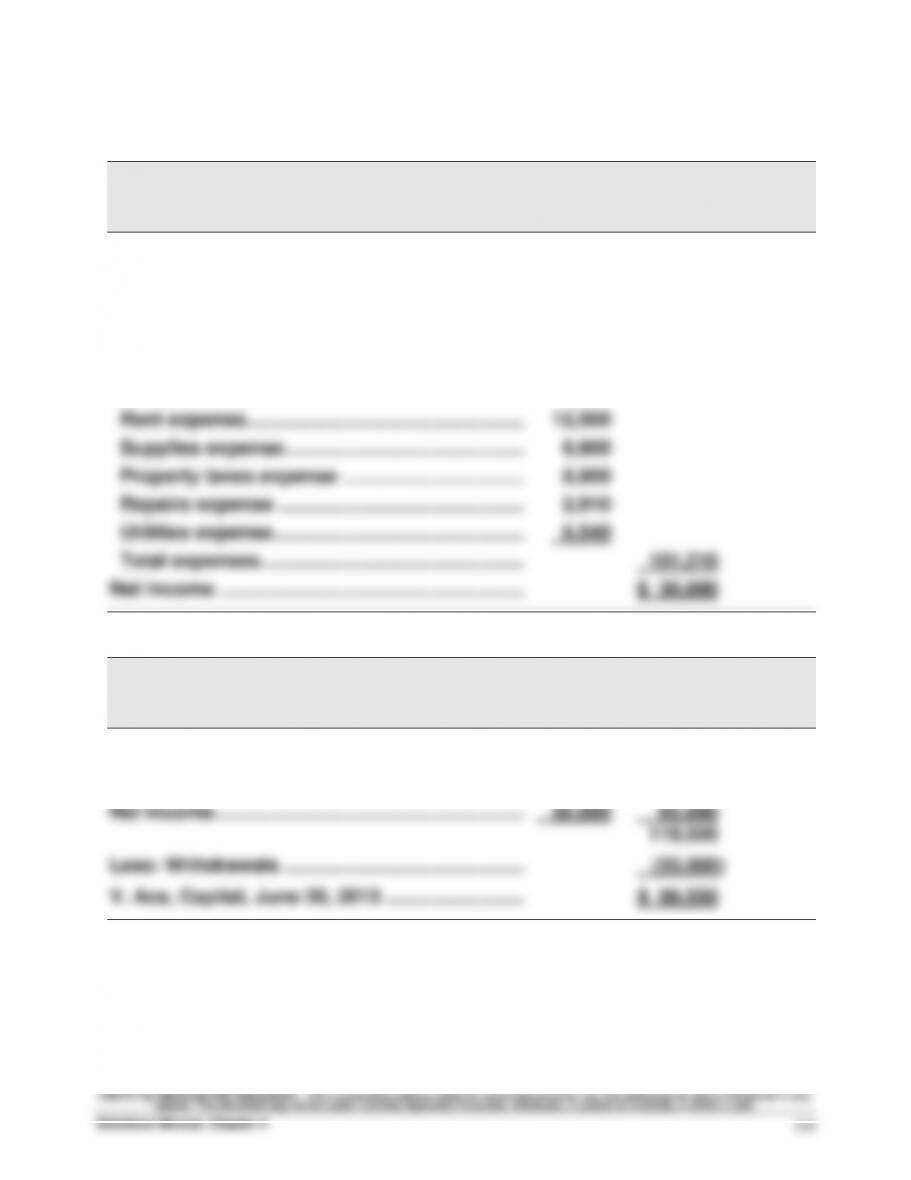

Part 3

ACE CONSTRUCTION CO.

Income Statement

For Year Ended June 30, 2013

Construction fees earned …………………………... $132,100

Expenses

Depreciation expense—Equipment …………… $ 8,400

Wages expense ………………………………………… 48,660

Interest expense……………………………………….. 3,000

Insurance expense……………………………………. 3,800

ACE CONSTRUCTION CO.

Statement of Owner’s Equity

For Year Ended June 30, 2013

V. Ace, Capital, June 30, 2012 …………………….. $ 53,660

Add: Owner contribution …………………………... $35,000

Problem 4-3A (Continued)

ACE CONSTRUCTION CO.

Balance Sheet

June 30, 2013

Assets

Current assets

Cash …………………………………………………………….. $ 18,500

Supplies ……………………………………………………….. 3,300

Accumulated depreciation—Equipment…………. (34,650) 97,350

Total assets ……………………………………………………. $122,550

Liabilities

Current liabilities

Accounts payable …………………………………………. $ 7,450

Interest payable ……………………………………………. 250

Total current liabilities ………………………………….. $ 16,000

Noncurrent liabilities

Long-term note payable ………………………………… 20,000

Total liabilities ………………………………………………… 36,000

Equity

Problem 4-3A (Concluded)

Part 4

(a) This error enters the wrong amount in the correct accounts. The

ending balance of the Supplies account should be $3,300, but the entry

reduces Supplies by $3,300. Because its unadjusted balance was

This error is not likely to be detected as a result of completing the

work sheet. If it is not, the income statement will overstate net income

(b) This error inserts a credit in the adjusted trial balance when a debit

should have been inserted. As a result, the trial balance will not

balance (the credit column will be greater than the debit column by

Problem 4-4A (90 minutes)

Part 1

KARISE REPAIRS

Income Statement

For Year Ended December 31, 2013

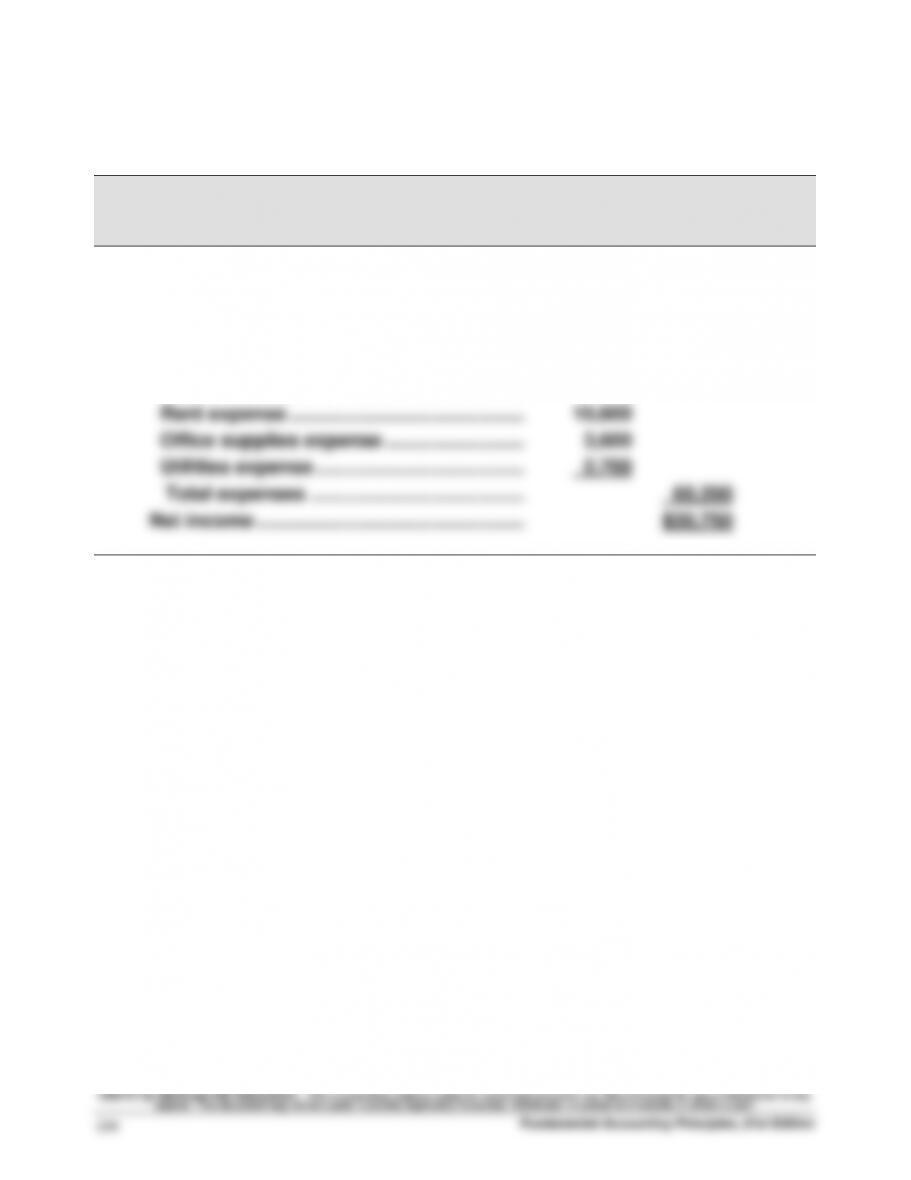

Repair fees earned ………………………………. $90,950

Expenses

Depreciation expense—Equipment …….. $ 5,000

Wages expense …………………………………. 37,500

Insurance expense …………………………….. 800

Problem 4-4A – (Continued)

KARISE REPAIRS

Statement of Owner‘s Equity

For Year Ended December 31, 2013

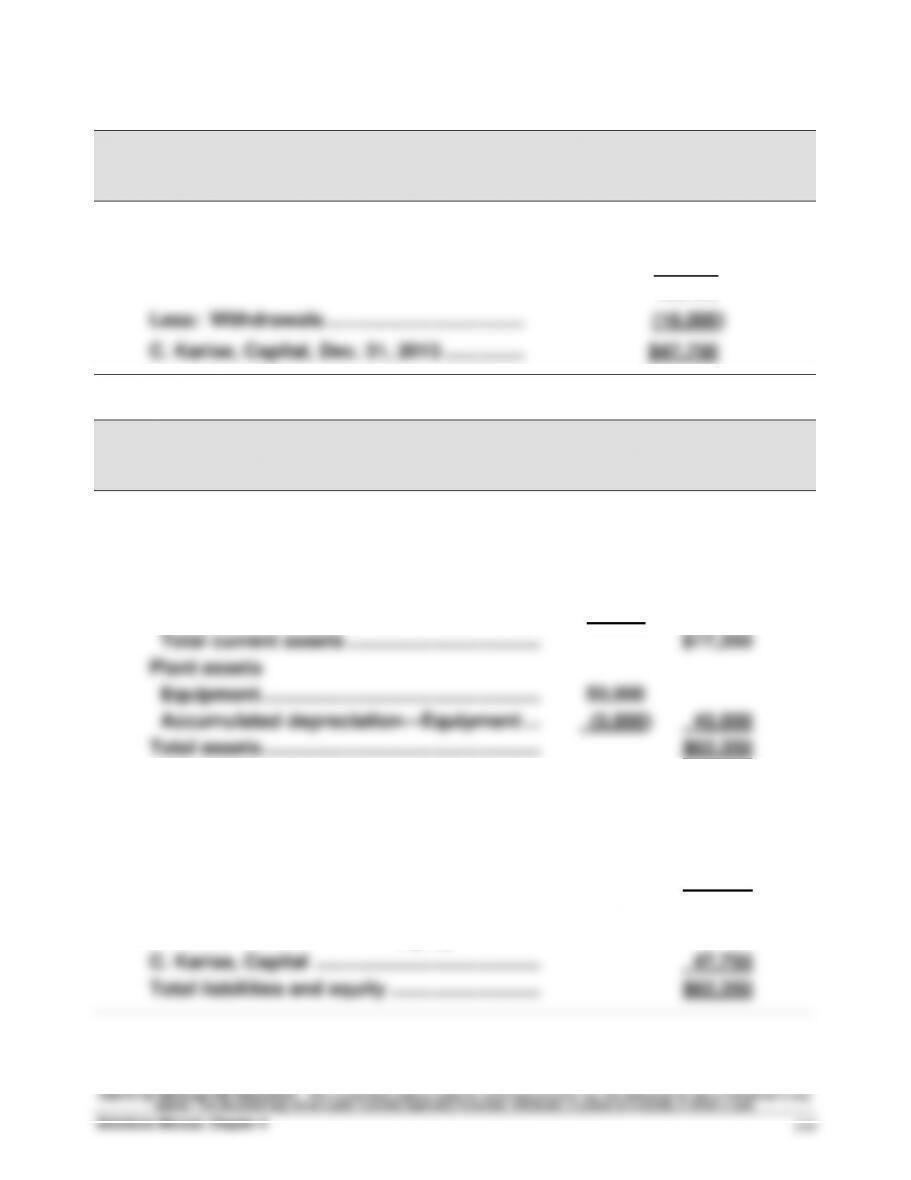

C. Karise, Capital, Jan. 1, 2013……………… $33,000

Add: Net income ……………………………….. 30,750

63,750

KARISE REPAIRS

Balance Sheet

December 31, 2013

Assets

Current assets

Cash …………………………………………………….. $14,000

Office supplies ……………………………………… 1,300

Prepaid insurance ………………………………… 2,050

Liabilities

Current liabilities

Accounts payable …………………………………. $14,000

Wages payable …………………………………….. 600

Total current liabilities ………………………….. 14,600

Equity

Problem 4-4A (Continued)

Parts 2 and 3

KARISE REPAIRS

Work Sheet

For Year Ended December 31, 2013

Adjusted

Trial Balance

Closing Entry Information

Post–Closing

Trial Balance

No.

Account Title

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

101

Cash ……………………………………….

14,000

14,000

124

Office supplies ……………………...

1,300

1,300

128

Prepaid insurance ……………….

2,050

2,050

167

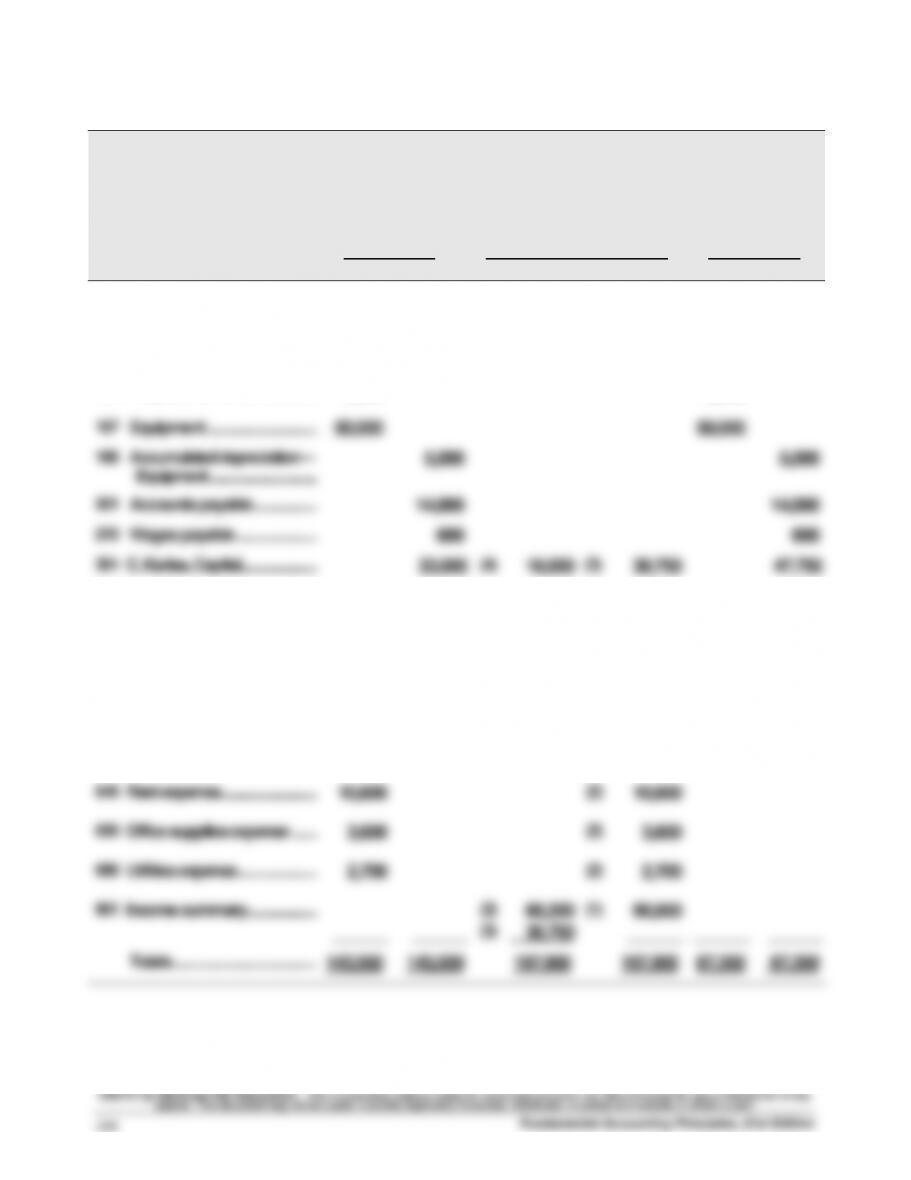

Equipment …………………………….

50,000

50,000

168

Accumulated depreciation—

Equipment ……………………………..

5,000

5,000

201

Accounts payable ………………..

14,000

14,000

210

Wages payable …………………….

600

600

301

C. Karise, Capital …………………..

33,000

(4)

16,000

(3)

30,750

47,750

302

C. Karise, Withdrawals ………..

16,000

(4)

16,000

401

Repair fees earned ………………

90,950

(1)

90,950

612

Depreciation expense—

Equipment …………………………..

5,000

(2)

5,000

623

Wages expense ……………………

37,500

(2)

37,500

637

Insurance expense ………………

800

(2)

800

640

Rent expense ………………………..

10,600

(2)

10,600

650

Office supplies expense ……..

3,600

(2)

3,600

690

Utilities expense ……………………

2,700

(2)

2,700

901

Income summary …………………

(2)

60,200

(1)

90,950

______

______

(3)

30,750

______

______

______

Totals ……………………………………..

143,550

143,550

197,900

197,900

67,350

67,350

Problem 4-4A (Continued)

Closing entries (all dated December 31, 2013)

Instructor note: Entries are shown without an account reference column because no posting is required.

(1) Repair Fees Earned ………………………………….. 90,950

Income Summary ………………………………. 90,950

To close the revenue account.

(2) Income Summary …………………………………….. 60,200

Depreciation Expense—Equipment ……. 5,000

Wages Expense…………………………………. 37,500

(3) Income Summary …………………………………….. 30,750

C. Karise, Capital ………………………………. 30,750

To close the Income Summary account.

Problem 4-4A (Concluded)

Part 4

(a) If none of the $800 insurance expense had expired, the income statement

would not report any insurance expense and net income would be

increased by $800.

Financial Statement Changes

The income statement would reflect the following:

• Net income would be increased by $800 + $600 = $1,400.

The balance sheet would reflect the following:

Problem 4-5A (75 minutes)

Part 1

TYBALT CONSTRUCTION

Income Statement

For Year Ended December 31, 2013

Revenues

Professional fees earned …………………………….. $97,000

Rent earned ………………………………………………… 14,000

Expenses

Depreciation expense—Building …………………. 11,000

Depreciation expense—Equipment ……………… 6,000

Wages expense …………………………..……………… 32,000

Property taxes expense ………………………………. 5,000

Repairs expense …………………………………………. 8,900

Telephone expense …………………………………….. 3,200

TYBALT CONSTRUCTION

Statement of Owner‘s Equity

For Year Ended December 31, 2013

O. Tybalt, Capital, December 31, 2012 …………… $121,400

Add: Investments by owner ………………………… $5,000

Net income …………………………………………. 4,300 9,300