Title: Question 1

QA_Ori: The seven broad principles are: Establish responsibilities; Maintain adequate records; Insure assets and

Title: Question 2

Title: Question 3

Title: Question 4

QA_Ori: Separation of custody from recordkeeping of an asset encourages the asset custodian to avoid misplacing,

Title: Question 5

QA_Ori: If individual departments were permitted to deal directly with suppliers, the amount of merchandise

Title: Question 6

Title: Question 7

Title: Question 8

Title: Question 9

Title: Question 10

Title: Question 11

QA_Ori: Arctic Cat’s net income for 2011 was $13,007 thousand. Further, it reported a net decrease in cash (and

Title: Question 12

QA_Ori: KTM’s cash (liquid assets) at December 31, 2011, equals €14,962 (all in EUR thousands). It is the third

largest current asset and makes up about 7.7% of its current assets.

Title: Question 13

QA_Ori: Piaggio’s cash and equivalents decreased by €2,956 thousand during 2011; specifically, from €154,758

thousand to €151,802 thousand (Instructor note: these cash numbers are somewhat different than what is

Title: Quick Study 8-1

QA_Ori: The main objective of internal control procedures is to safeguard the assets of the business. This objective

QA_Ori: Separation of recordkeeping for assets from the custody over assets is intended to reduce theft and fraud.

QA_Ori: The responsibility for a transaction should be divided between two or more individuals or departments to

Title: Quick Study 8-2

1. QA_Ori: The cash category includes currency and coins along with amounts on deposit in bank accounts,

2. QA_Ori: The cash equivalents category includes short-term, highly liquid investment assets meeting two

criteria: (1) readily convertible to a known cash amount and (2) sufficiently close to their due dates so that

3. QA_Ori: Liquidity refers to a company’s ability to pay for its near-term obligations.

Title: Quick Study 8-3

QA_Ori:

1. The three basic guidelines for safeguarding cash are:

2. (a) Voucher system of control, and (b) Petty cash system of control.

Title: Quick Study 8-4

QA_Ori:

(1) (2)

a. (i) Book (ii) Addition Adjusting entry required

d. (i) Bank (ii) Subtraction No adjustment required

Title: Quick Study 8-5

QA_Ori:

1. (a) Petty Cash……………………………………………………………………………… 150

(b) Entertainment Expense…………………………………………………………….. 70

2. The Petty Cash account is credited when either (1) the dollar amount of the fund is being reduced, or (2) the

fund is being eliminated.

Title: Quick Study 8-6

QA_Ori:

NOLAN COMPANY

Bank Reconciliation

June 30, 2013

Bank statement balance…………………………. $21,332 Book balance………………………………………………………………………………………………………………………$22,352

Add: Add:

Title: Quick Study 8-7

a. QA_Ori: A bank reconciliation is a formal review process that requires the person to precisely identify all

b. QA_Ori: A bank reconciliation has the potential to uncover several kinds of frauds or errors that an online

review is unlikely to reveal. Those include the following:

QA_Ori: A company makes a deposit to its account but that deposit is incorrectly added to another

QA_Ori: The bank incorrectly pays a common vendor’s bill from the company’s cash account, when that

QA_Ori: The bank incorrectly pays a larger amount to a payee than what is written on the company’s check

to that payee. An online review would not identify this bank overpayment as the payment to the payee

QA_Ori: A company check writer incorrectly records a check to a regular vendor for services provided at an

Numerous other examples can be listed…

Title: Quick Study 8-8

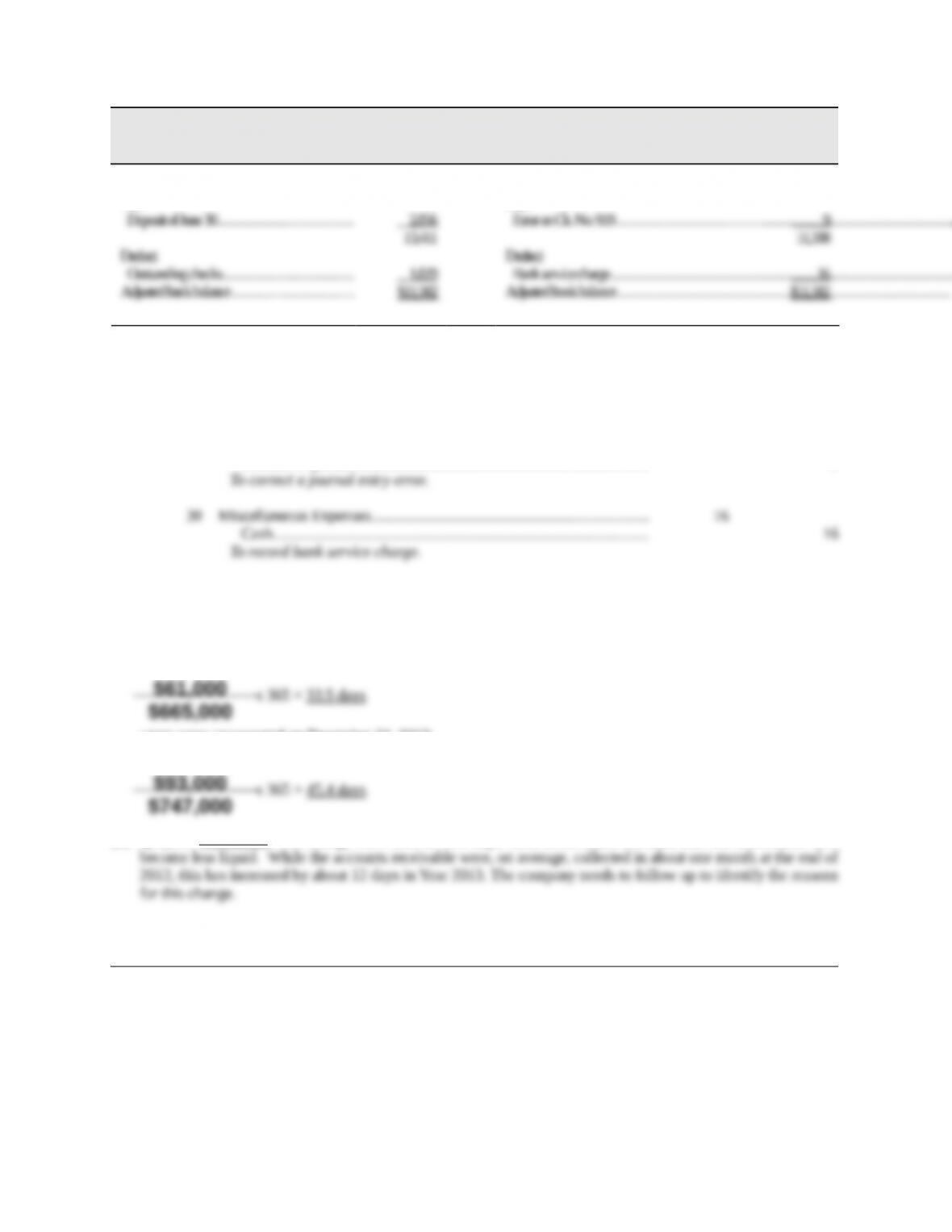

QA_Ori:

Days’ sales uncollected = x 365

2013 2012

Interpretation: The collection of accounts receivable seems to be slightly improving. It took the company

slightly over one-half day less to collect on its accounts receivable in 2013 than in 2012.

Title: Quick Study 8-9A

Title: Quick Study 8-10B

(a) QA_Ori: A Discounts Lost account is employed with the Net Method of recording purchases of inventory.

(b) QA_Ori: The advantage of this method is that the Discounts Lost account highlights for management (on the

income statement) the costs incurred by the business that have resulted from the failure to take cash discounts.

Accounts receivable

Net sales

$80,485

Title: Quick Study 8-11

a. QA_Ori: The purposes and principles of internal control systems are fundamentally the same for accounting

b. QA_Ori: Internal controls for cash are fundamentally the same worldwide. Accordingly, there is global

Title: Exercise 8-1

Evaluation:

QA_Ori: The company’s internal control system failed to require separation of asset custody from asset

recordkeeping.

Principles Ignored

QA_Ori: If regular, independent reviews of the accounting records had been done, the payments of salary checks to

a nonemployee may have been discovered earlier.

Title: Exercise 8-2

(a) Internal Control Problems

(1) QA_Ori: A major internal control problem is that the recordkeeper (who has control over the accounting

(2) QA_Ori: The recordkeeper might also delay recording a cash receipt from a customer until more cash

(3) QA_Ori: The recordkeeper also could pocket cash and claim that a payment was never received and

apparently lost in the mail.

(b) Internal Control Recommendations

(1) QA_Ori: If only one person is present when the mail is opened, that person may steal cash and claim it

(2) QA_Ori: It is important the recordkeeper not have physical control over cash.

Title: Exercise 8-3

QA_Ori: A cash register (with a locked record) should be used at the sales stand—it should also be anchored to the

stand. If a cash register cannot be used, the total sales value of the towels, coolers, and sunglasses given to the

QA_Ori: The employee should sign a receipt for the total amount of cash he or she is given each weekend. Each

time the employee makes a purchase, he or she should obtain a signed sales receipt for the payment. The sales

Title: Exercise 8-4

QA_Ori: A liquid asset refers to an asset that can be readily converted into another type of asset or be used to satisfy

QA_Ori: Companies usually invest idle cash in cash equivalents to earn a higher return on these assets.

QA_Ori: Effective cash management applies the following five principles:

a. Encourages collection of receivables.

Title: Exercise 8-5

1.

Jan. 1 Petty Cash……………………………………………………………………………………. 200

2.

Jan. 8 Postage Expense…………………………………………………………………………… 74

Cash………………………………………………………………………………………. 162

3.

Jan. 8 Postage Expense…………………………………………………………………………… 74

Jan. 8 Petty Cash……………………………………………………………………………………. 250

** The two January 8 entries can be combined into one entry.

Title: Exercise 8-6

1.

2.

Sept. 30 Merchandise Inventory*…………………………………………………………………. 40

Postage Expenses………………………………………………………………………….. 123

3.

Oct. 1 Petty Cash……………………………………………………………………………………. 50

Cash………………………………………………………………………………………. 50

To increase the petty cash fund to $400.

Title: Exercise 8-7

Bank Balance Book Balance Not Shown on

Add Deduct Add Deduct Adjust Reconciliation

1. NSF check from customer returned on Sept. 25 but not

recorded by this company. x Cr.

2. Interest earned on the account. x Dr.

8. Principal and interest on a note receivable to this company is

collected by the bank but not yet recorded by the company. x Dr.

9. Checks written and mailed to payees on October 2.

x

Title: Exercise 8-8

QA_Ori: The voucher system of control establishes procedures for: (a) Verifying, approving, and recording

Title: Exercise 8-9

WRIGHT COMPANY

Bank Reconciliation

May 31, 2013

Bank statement balance……………………….. $25,800 Book balance………………………………………………………………………………………………………………………$27,500

Add

Deposit of May 31…………………………… 6,200

Bank error……………………………………. 400

32,400

Title: Exercise 8-10

DEL GATO CLINIC

Bank Reconciliation

June 30, 2013

Bank statement balance……………………….. $10,555 Book balance………………………………………………………………………………………………………………………$11,589

Add Add

Title: Exercise 8-11

June 30 Cash……………………………………………………………………………………… 9

Utilities Expense……………………………………………………………….. 9

Title: Exercise 8-12

(a) Days’ sales uncollected on December 31, 2012:

(b) QA_Ori: Evaluation: The change from 33.5 to 45.4 days’ sales uncollected indicates that the receivables have

Title: Exercise 8-13A