PROBLEM SET B

Problem 21-1B (25 minutes)

Parts 1 and 2

Gilmore Company

Contribution Margin Income Statement

For Year Ended December 31, 2013

(12,000 units) Per unit % of sales

Sales ($18 x 12,000) ………………….…….

$216,000

$18.000

100.00%

Variable costs

Plastic for CD sets ………………….…….

$ 1,500

$0.125

Assembly worker wages …………..…….

30,000

2.500

Labeling ……………………………….…….

3,000

0.250

Sales commissions ………………..…….

6,000

40,500

0.500

3.375

18.75%

Contribution margin ……………………….

$14.625

Fixed costs

4,520

20,000

15,000

Income tax (25%) ……………………….….

Net income ………………………………..…….

$ 6,135

Part 3 Analysis Component

Contribution margin shows how much of total sales are available to cover

fixed costs and contribute to operating income. This is why the title for this

Fundamental Accounting Principles, 21st Edition

1246

Problem 21-2B (40 minutes)

Part 1

(a) Instructor note: Use the equation in Exhibit 21.11

Break-even in unit sales = Fixed costs / Contribution margin per unit

(b) Instructor note: Use the equation in Exhibit 21.12

Problem 21-2B (Continued)

Part 2

Part 3

HIP-HOP CO.

Contribution Margin Income Statement (at Break-Even) — Keyboards

Sales (300 x $350) ……………………………………………………………………..

$105,000

Variable costs (300 x $210) ……………………………………………………….

Fixed costs (given) …………………………………………………………………...

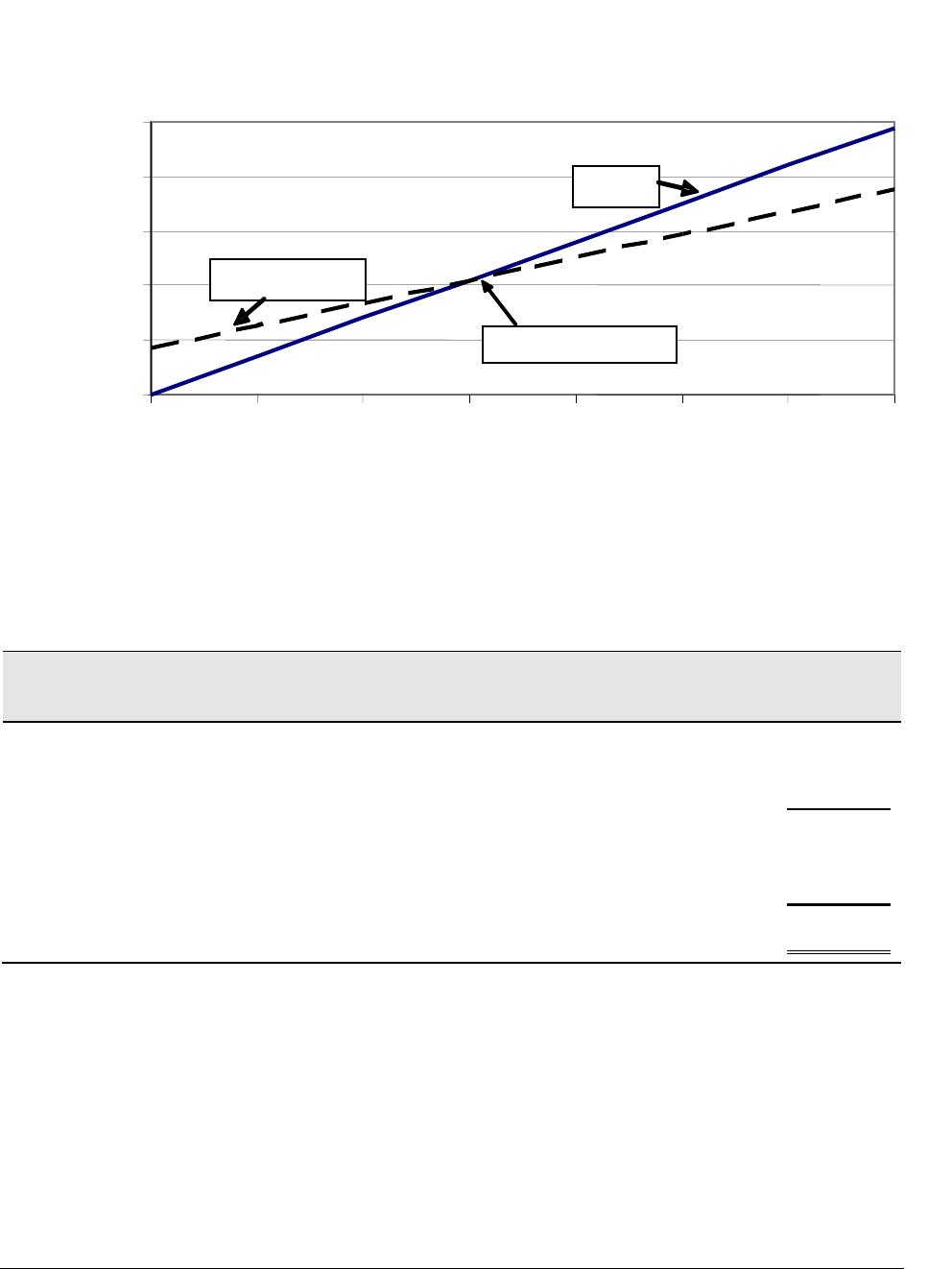

Hip-Hop Company CVP chart

$ 0

$50,000

$200,000

$250,000

0

100

200

300

400

500

600

700

Units

Fundamental Accounting Principles, 21st Edition

1248

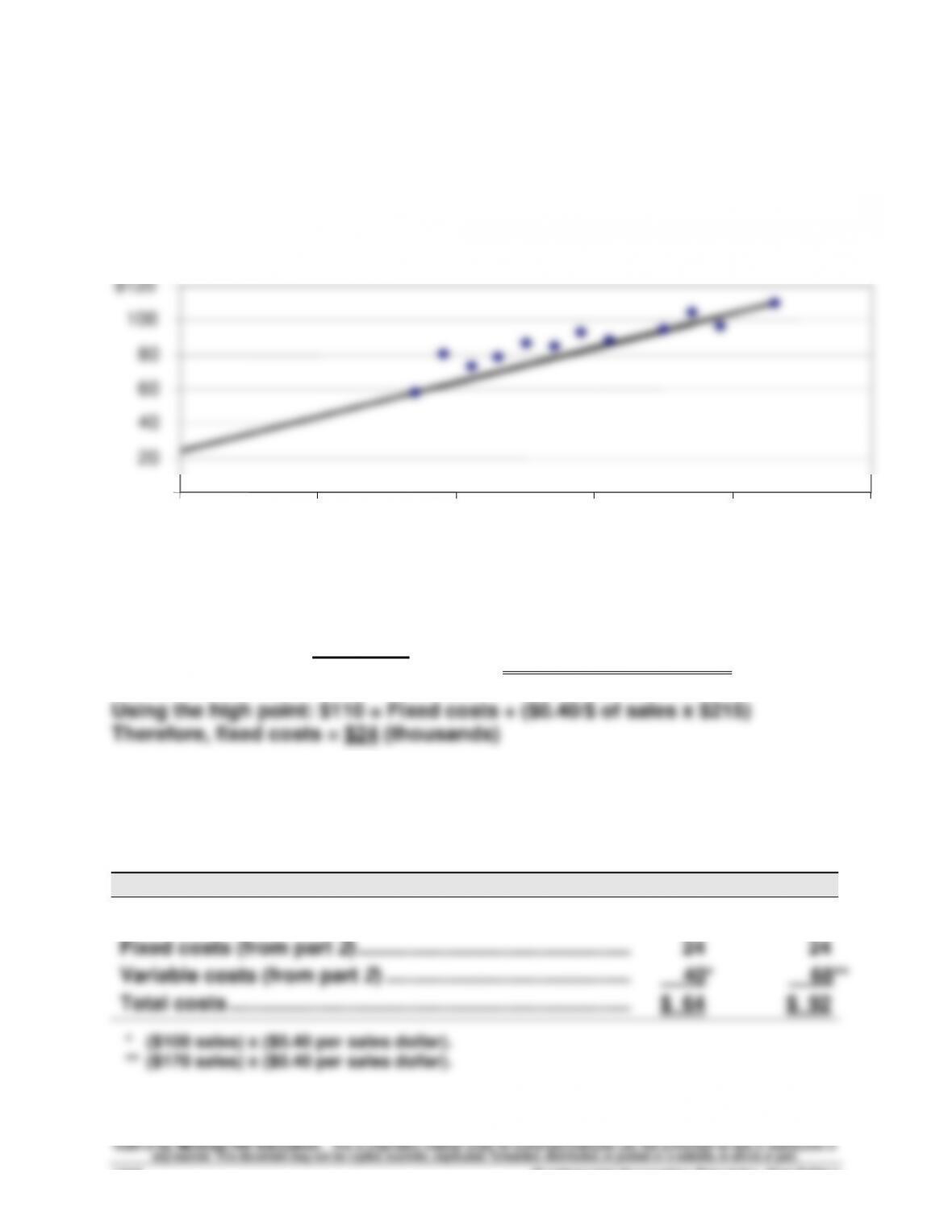

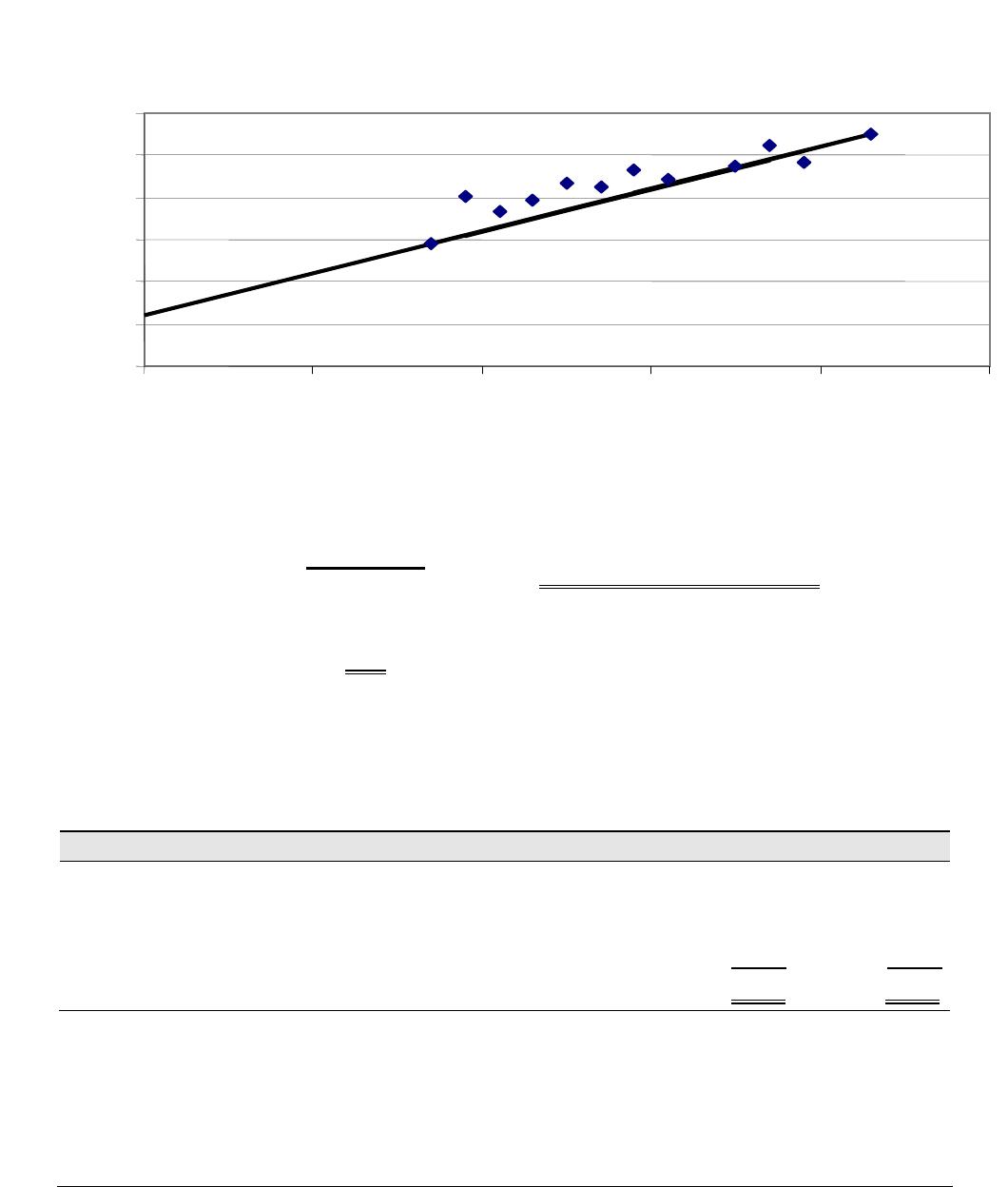

Problem 21-3B (45 minutes)

Parts 1 and 2

The scatter diagram and its estimated line of cost behavior appear below.

Sales and cost amounts are in thousands of dollars.

Part 2 Calculation of variable and fixed costs

Variable costs = = $0.40 per dollar of sales

Part 3

The estimates in Part 2 can be used to predict the total costs that will be

incurred at sales levels of $100 and $170 (both in thousands).

(‘000s)

Predictions

Sales (given) …………………………………………………………………..

$100

$170

Kyo Company

0

20

40

60

80

100

0

$50

$100

$150

$200

$250

Sales Dollars

Total

Costs

$110 – $58

$215 – $85

Problem 21-4B (75 minutes)

Part 1 Instructor note: Use the equation in Exhibit 21.12

2013 break-even in dollar sales = Fixed costs / Contribution margin ratio

Part 2 Instructor note: Use equation in Exhibit 21.12 with predicted numbers

Part 3

RIVERA COMPANY

Forecasted Contribution Margin Income Statement

For Year Ended December 31, 2014

Sales (20,000 x $37.50) ……………………………………………………………..….

$750,000

Variable costs (20,000 x $15) …………………………………………………….…

300,000

Contribution margin (20,000 x $22.50) ……………………………………….….

450,000

Fixed costs ………………………………………………………………………………….

350,000

Net income ……………………………………………………………………………….….

Fundamental Accounting Principles, 21st Edition

1250

Problem 21-4B (Continued)

Part 4 Instructor note: Use equations in Exhibit 21.22 and 21.23 with predicted

numbers

(Fixed costs + Pretax income)

Required sales in dollars = Contribution margin ratio

= ($350,000* + $200,000**) / 60%***

= $550,000 / 60%

= $916,667 (rounded to the next dollar)

* 2013 fixed costs plus 2014 increase ($200,000 + $150,000) …………………….…..

$350,000

** Target after-tax income (given) ……………………………………………………………..…..

$140,000

Pretax target income = After-tax target income / (1 – Tax rate)

= $140,000 / (1 – 0.30) = $200,000

$916,667

Part 5

RIVERA COMPANY

Forecasted Contribution Margin Income Statement

For Year Ended December 31, 2014

Sales (24,445 units x $37.50) ……………………………………………....

$916,688

Variable costs (24,445 units x $15) ……………………………………...

366,675

Contribution margin (24,445 units x $22.50) ………………………...

550,013

Income before income taxes ……………………………………………....

200,013

60,004

$140,009

*Slightly greater than the targeted $140,000 income due to rounding of units from part 4.

Problem 21-5B (65 minutes)

Part 1 Instructor note: Use the equation in Exhibit 21.12

Break-even in dollar sales = Fixed costs / Contribution margin ratio

Product BB:

*To compute contribution margin ratio

Sales price per unit

Product BB ($800,000 / 50,000) ……………………………………………………….

Product TT ($800,000 / 50,000) ……………………………………………………….

BB

$16.00

TT

$16.00

Variable costs per unit

$11.20

Contribution margin ratio

Part 2

Forecasted contribution margin income statements for each product

assuming sales decline to 33,000 units with no change in unit sales price

MINGEI CO.

Forecasted Contribution Margin Income Statement

Product BB

Product TT

Sales* …………………………………………………………………

$528,000

$ 528,000

Variable costs** ………………………………………………..…

369,600

66,000

Contribution margin ……………………………………………

158,400

462,000

100,000

560,000

18,688

(31,360)

Net income ……………………………………………………….

Unit sales price and variable costs are computed in Part 1 and used in these computations:

* Product BB sales = 33,000 units x $16; Product TT sales = 33,000 units x $16.

Fundamental Accounting Principles, 21st Edition

1252

Problem 21-5B (Continued)

Forecasted contribution margin income statements for each product

assuming sales increase to 64,000 units with no change in unit sales price

MINGEI CO.

Forecasted Contribution Margin Income Statement

Product BB

Product TT

Sales* …………………………………………………………………

$1,024,000

$1,024,000

Variable costs** ………………………………………………..…

716,800

128,000

Contribution margin ……………………………………………

307,200

896,000

207,200

336,000

66,304

107,520

Part 4

If sales were to greatly increase, Product TT would experience the greater

increase in income because it would gain more contribution margin per

Part 5

Factors that could cause Product BB to have lower fixed costs include:

• Labor arrangement that pays workers for units produced.

rent based on asset usage.

In contrast, the fixed costs for Product TT could be higher because of:

• Salary structure that is not based on production or sales.

Problem 21-6B (45 minutes)

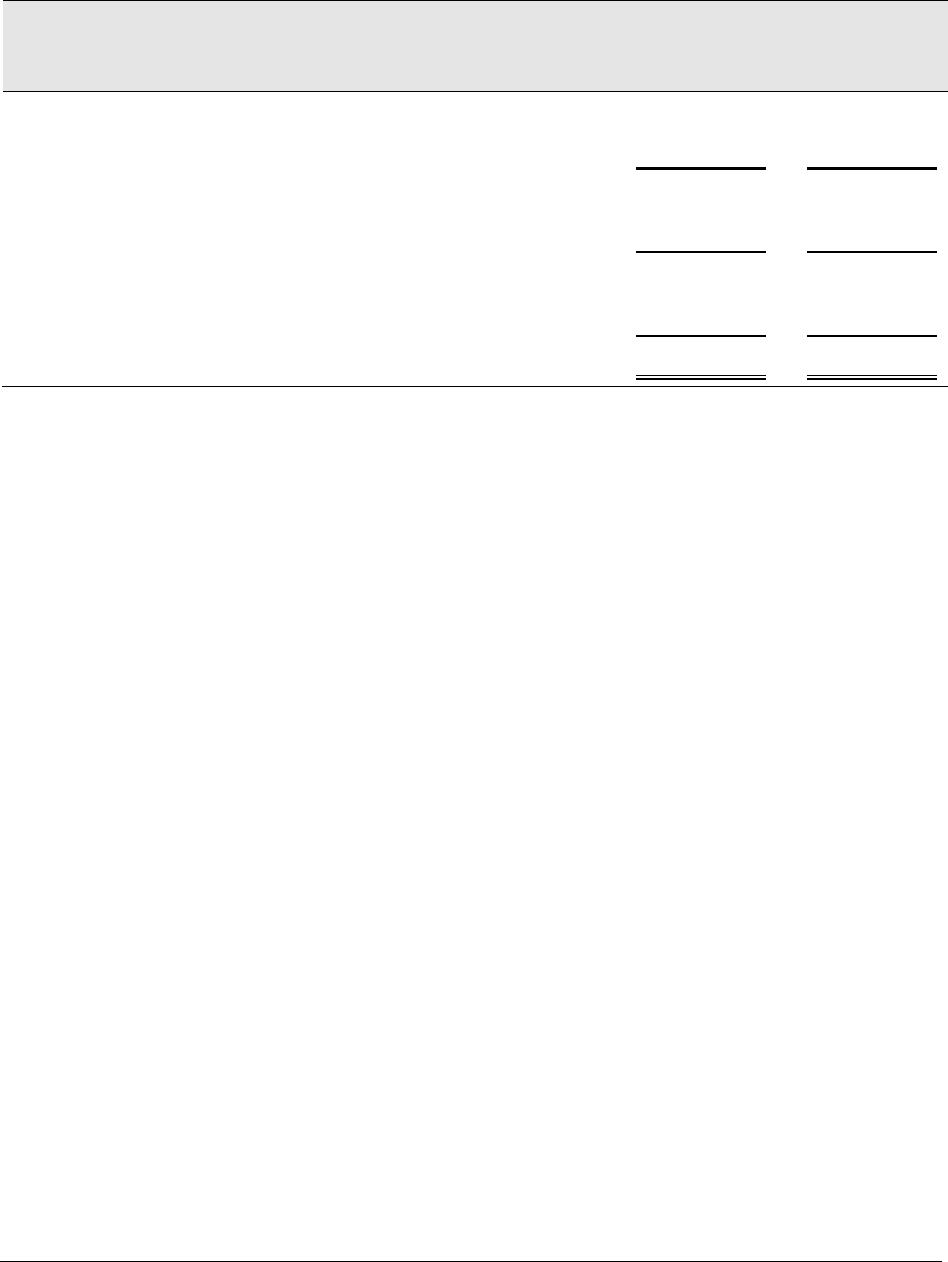

Part 1 Instructor note: Use the equation in Exhibit 21.12

Break-even in dollar sales = Fixed costs / Contribution margin ratio

*To compute contribution margin ratio

Sales price per unit

Existing strategy ……………………………………………………….

New strategy [$20.00 x (1 – 20%)] ………………………………..……………………..

Existing

Strategy

$20.00

New

Strategy

$16.00

Total variable costs per unit

Unit costs ($800,000 / 100,000) ……………………………………………………….

$ 8.00

Existing strategy ($20.00 – $9.00) / $20.00) …………………..………

Part 2

BEST COMPANY

Forecasted Contribution Margin Income Statement

Existing Strategy

New Strategy

Sales* …………………………………………………………………

$2,000,000

$2,880,000

Variable costs** ………………………………………………..…

900,000

1,296,000

Contribution margin ……………………………………………

1,100,000

1,584,000

Fixed costs ……………………………………………………….

950,000

950,000

Income before taxes ……………………………………………

37,500

158,500

Net income ……………………………………………………….