Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

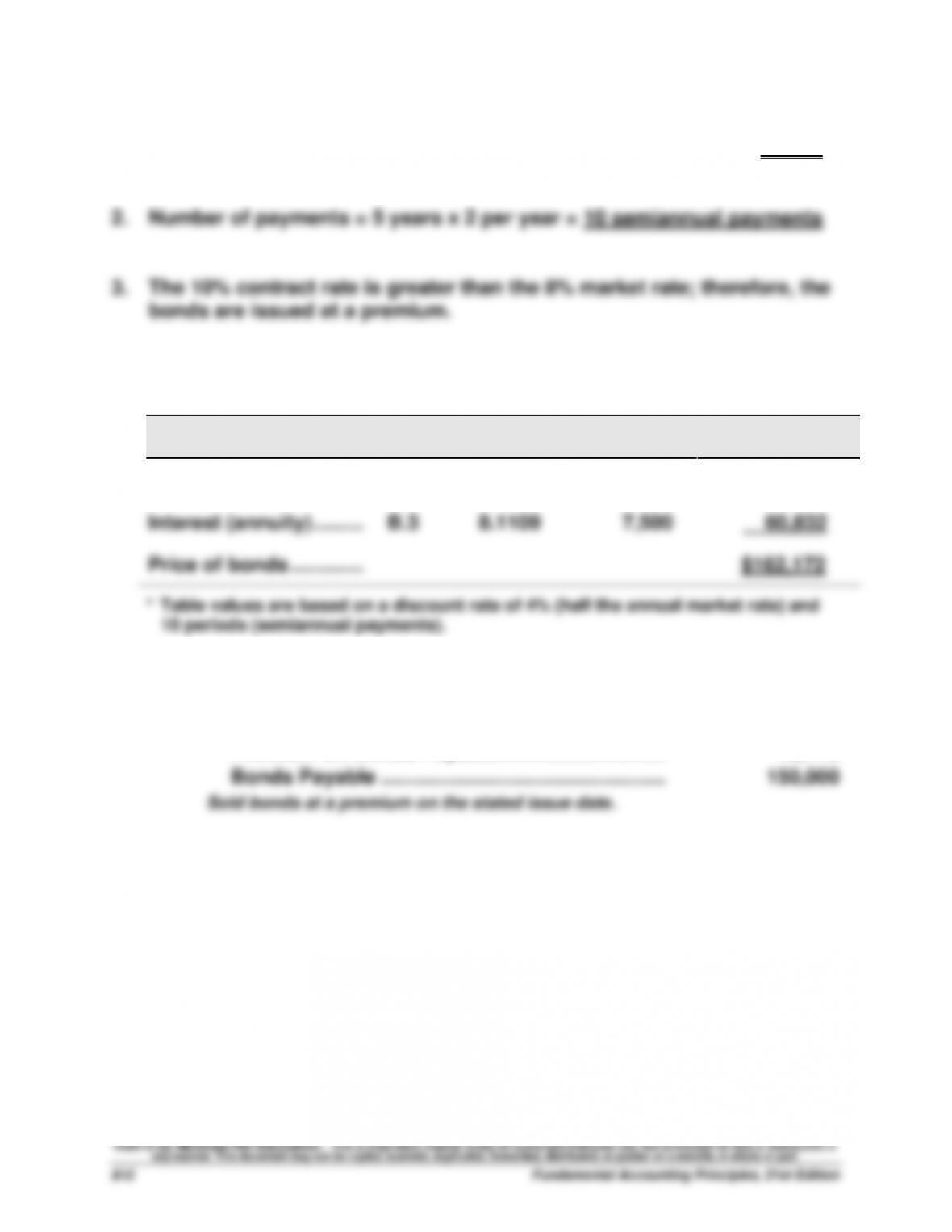

Exercise 14-10 (25 minutes)

1. Semiannual cash interest payment = $150,000 x 10% x ½ year = $7,500

4. Estimation of the market price at the issue date

Cash Flow

Table

Table Value*

Amount

Present Value

Par (maturity) value ........

B.1

0.6756

$150,000

$101,340

5.

Cash ................................................................................

162,172

Premium on Bonds Payable................................

12,172

Exercise 14-11 (20 minutes)

1. Cash proceeds from sale of bonds at issuance

2. Discount at issuance

3. Total amortization for first 6 years

The first six years (from 1/1/13 to 12/31/18) equals 40% of the bonds’ 15-

4. Carrying value of the bonds at 12/31/2018

Discount at issuance (from part 2) ......

$ 15,750

Entire Group

Retired 20%

Par value .................................................

$700,000

$140,000

5. Cash purchase price

($700,000 x 20%) x 104.5% = $146,300

6. Loss on retirement

Cash paid (from part 5) ......................

$ 146,300

7. Journal entry at retirement for 20% of bonds

2019

Jan. 1

Bonds Payable ...............................................................

140,000

Loss on Retirement of Bonds Payable ........................

8,190

Exercise 14-12C (20 minutes)

1. Semiannual cash interest payment = $3,400,000 x 9% x ½ year = $153,000

2. Journal entries

2013

May 1

Cash ................................................................................

3,502,000

June 30

Interest Payable .............................................................

102,000

Bond Interest Expense ..................................................

51,000

Exercise 14-13 (40 minutes)

1. Straight-line amortization table (($100,000-$95,948)/8 = $506.5)

Semiannual

Period-End

Unamortized

Discount †

Carrying

Value

6/01/2013 .....................

$4,052

$95,948

11/30/2013 .....................

3,546

96,454

5/31/2014 .....................

3,040

96,960

11/30/2016 .....................

506*

99,494

5/31/2017 .....................

0

100,000

* Adjusted for rounding difference.

Exercise 14-13 (Concluded)

† Supporting computations

Eight payments of $3,500** ....................

$ 28,000

Par value at maturity ...............................

100,000

Total repaid .............................................

128,000

2.

2013

Nov. 30

Bond Interest Expense ..................................................

4,006

Discount on Bonds Payable ................................

506

Cash ..........................................................................

3,500

To record 6 months’ interest and discount amortization.

2014

May 31

Interest Payable .............................................................

584

Bond Interest Expense ..................................................

3,338

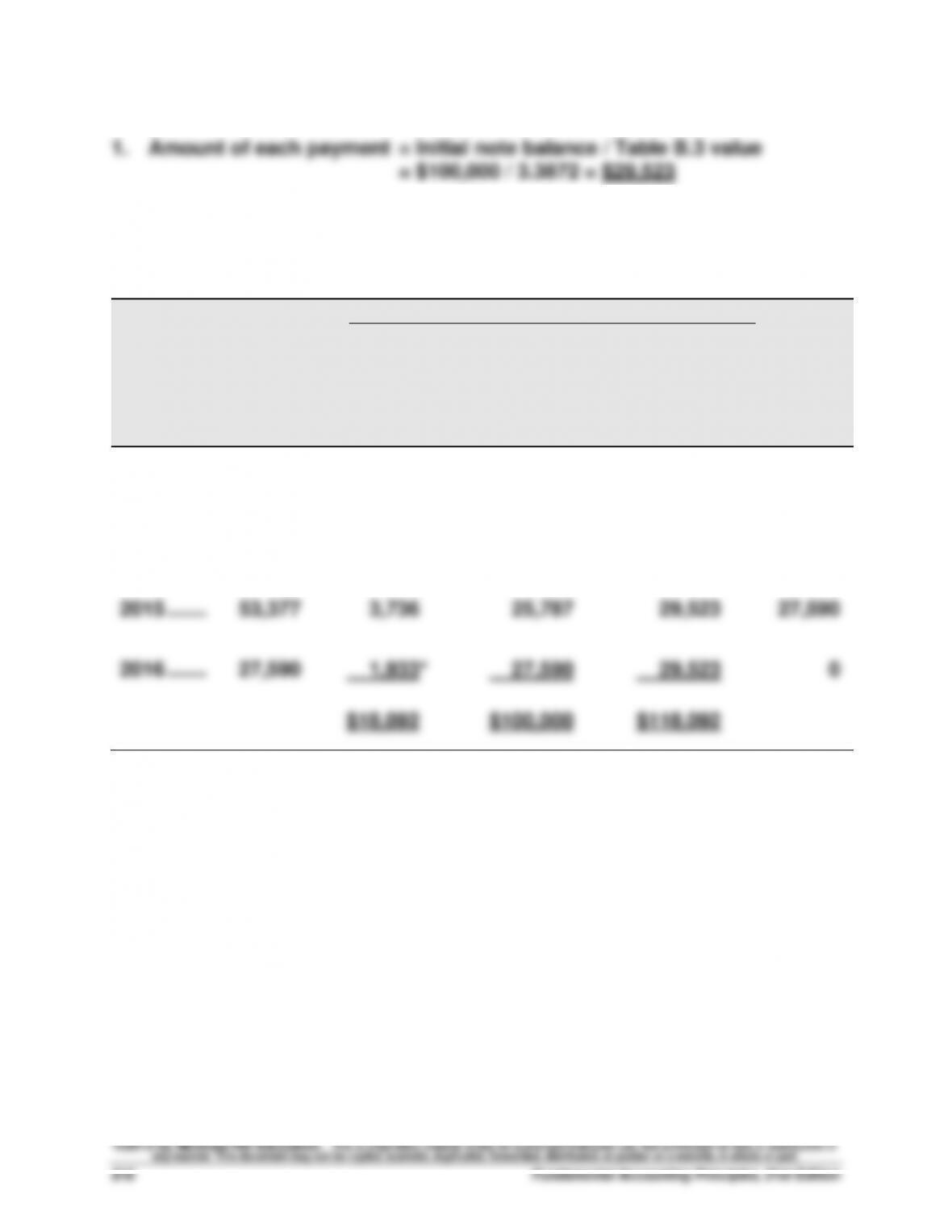

Exercise 14-14 (20 minutes)

2. Amortization table for the loan

Payments

Period

Ending

Date

(A)

Beginning

Balance

[Prior (E)]

(B)

Debit

Interest

Expense

[7% x (A)]

+

(C)

Debit

Notes

Payable

[(D) - (B)]

=

(D)

Credit

Cash

[computed]

(E)

Ending

Balance

[(A) - (C)]

2013 .......

$100,000

$ 7,000

$ 22,523

$ 29,523

$77,477

2014 .......

77,477

5,423

24,100

29,523

53,377

*Adjusted for rounding.

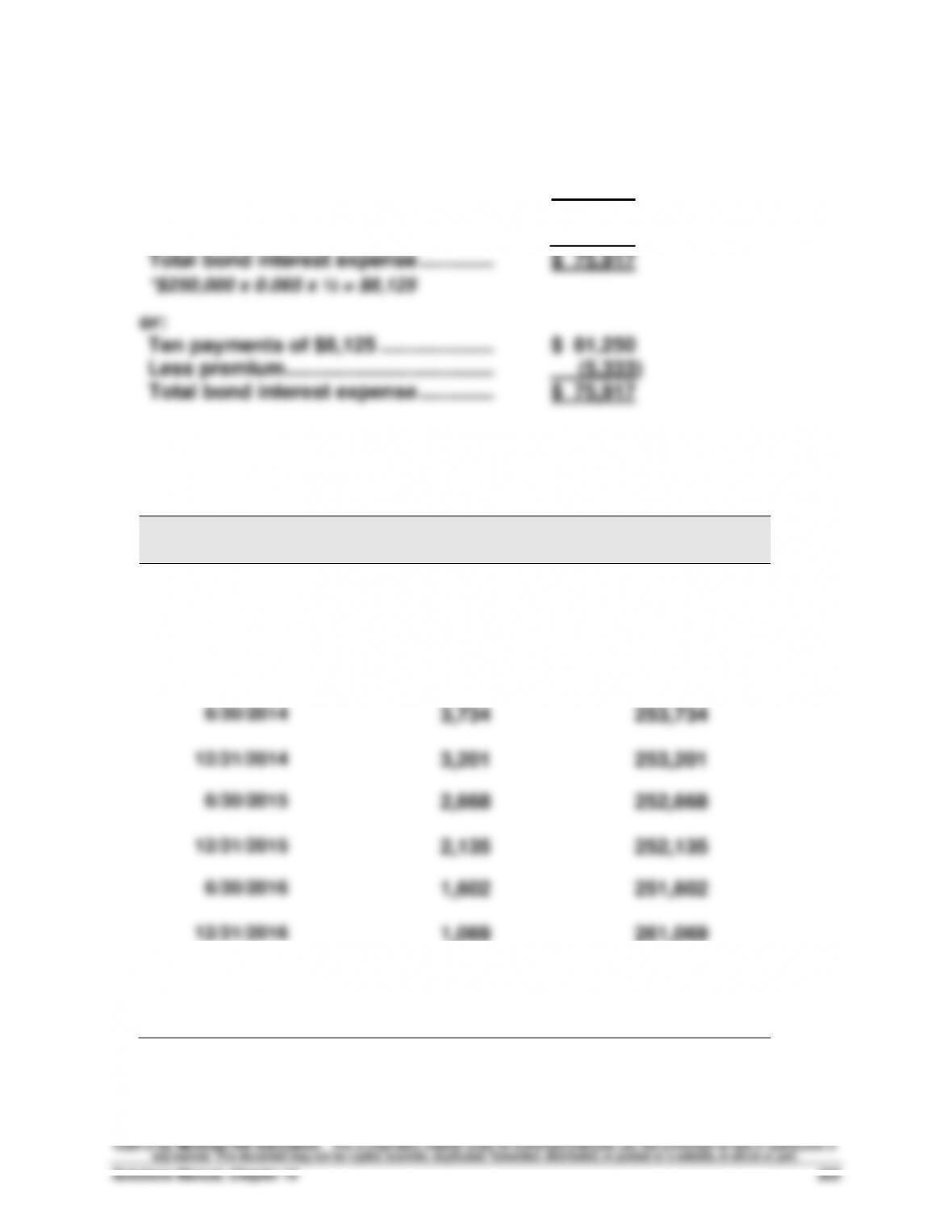

Exercise 14-15 (20 minutes)

2013

Jan. 1

Cash ................................................................................

100,000

Notes Payable ..........................................................

100,000

Borrowed $100,000 by signing a 7%

installment note.

2013

2015

Dec. 31

Interest Expense ............................................................

3,736

Notes Payable ................................................................

25,787

Cash ..........................................................................

29,523

To record third installment payment.

Exercise 14-16 (15 minutes)

1a. Current debt-to-equity ratio = $220,000 / $390,000* = 0.564

*Total equity = $610,000 - $220,000 = $390,000

Exercise 14-17D (10 minutes)

Exercise 14-18D (20 minutes)

1.

Leased Asset—Office Equipment ................................

41,000

Lease Liability ..........................................................

41,000

To record capital lease of office equipment.

Exercise 14-19D (15 minutes)

[Note: 12% / 12 months = 1% per month as the relevant interest rate.]

Option 1: $1,750 per month for 25 months = $1,750 x 22.0232 = $38,541

Exercise 14-20 (20 minutes)

1.

Cash.................................................................................

1,920

2.

Loans and Borrowings ..................................................

3,000

Premium on Loans and Borrowings ............................

32

3. Heineken’s Loans and Borrowings carried a premium of € 78 as of

4. The contract rate was higher than the market rate at issuance. This is

PROBLEM SET A

Problem 14-1A (50 minutes)

Part 1

Instructor note: The first printing of the textbook has an erroneous marginal

check figure of $4,537 that should correctly read $5,437.

a.

Cash Flow

Table

Table Value*

Amount

Present Value

Par value .....................

B.1

0.4564

$40,000

$18,256

* Table values are based on a discount rate of 4% (half the annual market rate) and 20

periods (semiannual payments).

** $40,000 x 0.10 x ½ = $2,000

b.

2013

Jan. 1

Cash ................................................................

45,437

Part 2

a.

Cash Flow

Table

Table Value*

Amount

Present Value

Par value .....................

B.1

0.3769

$40,000

$15,076

* Table values are based on a discount rate of 5% (half the annual market rate) and 20

periods (semiannual payments). (Note: When the contract rate and market rate are the

same, the bonds sell at par and there is no discount or premium.)

b.

2013

Jan. 1

Cash ................................................................

4,000

Problem 14-1A (Concluded)

Part 3

a.

Cash Flow

Table

Table Value*

Amount

Present Value

Par value ....................

B.1

0.3118

$40,000

$12,472

Interest (annuity) .......

B.3

11.4699

2,000

22,940

b.

2013

Jan. 1

Cash ................................................................

35,412

Problem 14-2A (40 minutes)

Part 1

2013

Jan. 1

Cash ................................................................

3,456,448

Part 2

[Note: The semiannual amounts for (a), (b), and (c) below are the same throughout the bonds’

life because this company uses straight-line amortization.]

(a) Cash Payment = $4,000,000 x 6% x 6/12 year = $120,000

Part 3

Thirty payments of $120,000 ....................

$3,600,000

Par value at maturity ................................

4,000,000

Total repaid .................................................

7,600,000

Less amount borrowed .............................

(3,456,448)

Part 4 (Semiannual amortization: $543,552/30 = $18,118.4)

Semiannual

Period-End

Unamortized

Discount

Carrying

Value

1/01/2013 .....................

$543,552

$3,456,448

6/30/2013 .....................

525,434

3,474,566

Problem 14-2A (Concluded)

Part 5

2013

June 30

Bond Interest Expense ..................................................

138,118

Discount on Bonds Payable ................................

18,118

Cash ................................................................

120,000

To record six months’ interest and

discount amortization.

2013

Problem 14-3A (40 minutes)

Part 1

2013

Jan. 1

Cash ................................................................................

4,895,980

Part 2

(a) Cash Payment = $4,000,000 x 6% x 6/12 = $120,000

Part 3

Thirty payments of $120,000 ....................

$3,600,000

Par value at maturity ................................

4,000,000

Total repaid .................................................

7,600,000

Fundamental Accounting Principles, 21st Edition

824

Problem 14-3A (Concluded)

Part 4

Semiannual

Period-End

Unamortized

Premium

Carrying

Value

1/01/2013 .....................

$895,980

$4,895,980

Part 5

2013

June 30

Bond Interest Expense ................................

90,134

2013

Dec. 31

Bond Interest Expense ................................

90,134

Premium on Bonds Payable ................................

29,866

Problem 14-4A (45 minutes)

Part 1

Ten payments of $8,125* ..........................

$ 81,250

Par value at maturity ................................

250,000

Total repaid .................................................

331,250

Less amount borrowed .............................

(255,333)

Part 2

Straight-line amortization table ($5,333/10 = $533*)

Semiannual

Interest Period-End

Unamortized

Premium

Carrying

Value

1/01/2013

$5,333

$255,333

6/30/2013

4,800

254,800

12/31/2013

4,267

254,267

6/30/2017

533**

250,533

12/31/2017

0

250,000

* Rounded to nearest dollar. ** Adjusted for rounding.

Problem 14-4A (Concluded)

Part 3

2013

June 30

Bond Interest Expense ................................

7,592

2013

Dec. 31

Bond Interest Expense ................................

7,592

Premium on Bonds Payable ................................

533