CHAPTER 20

PROCESS COST ACCOUNTING

Related Assignment Materials

Student Learning Objectives

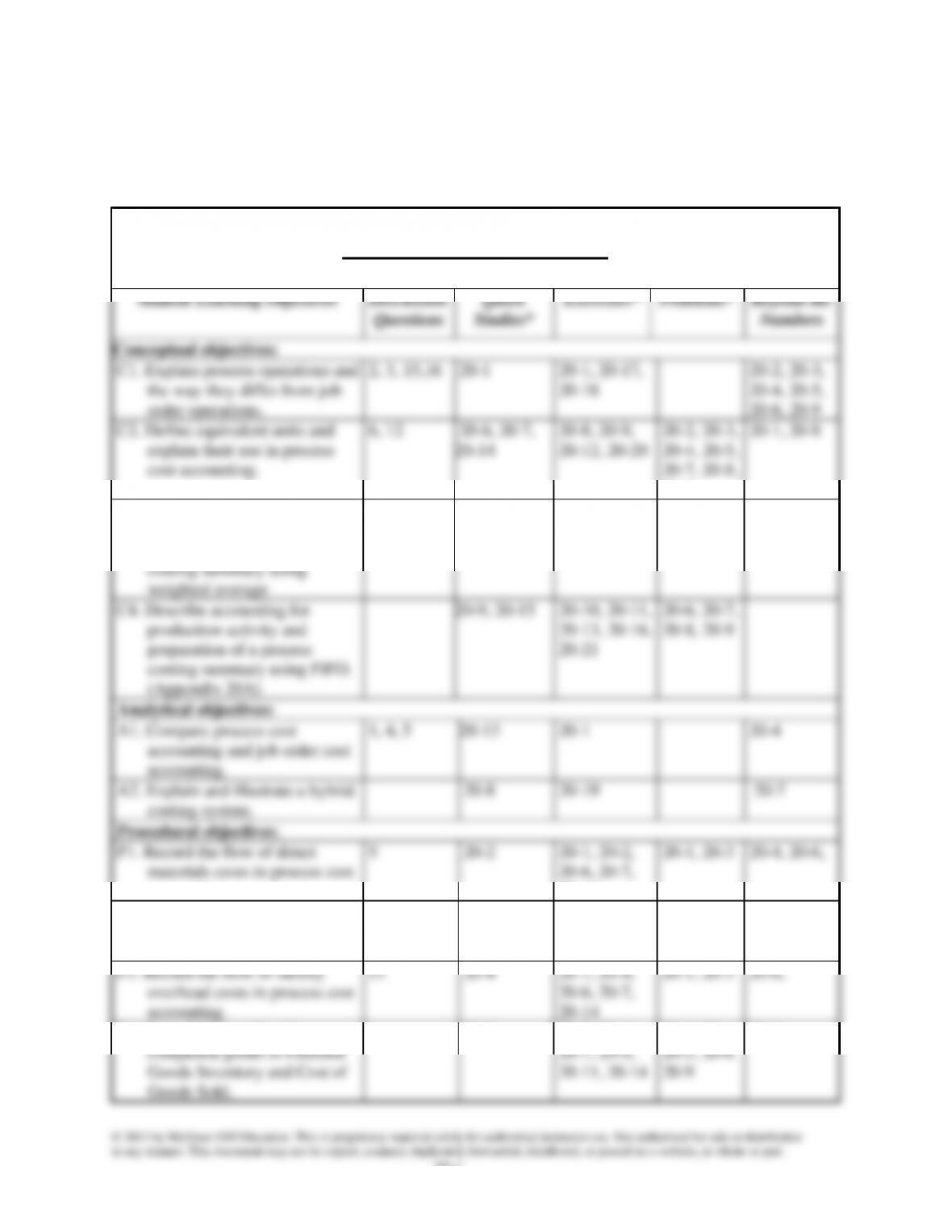

Discussion

Questions

Quick

Studies*

Exercises*

Problems*

Beyond the

Numbers

Conceptual objectives:

C1. Explain process operations and

the way they differ from job

order operations.

2, 3, 15,16

20-1

20-1, 20-17,

20-18

20-2, 20-3,

20-4, 20-5,

20-6, 20-9

C2. Define equivalent units and

explain their use in process

cost accounting.

6, 12

20-6, 20-7,

20-14

20-8, 20-9,

20-12, 20-20

20-2, 20-3,

20-4, 20-5,

20-7, 20-8,

20-9

20-1, 20-8

C3. Describe accounting for

production activity and

preparation of a process

costing summary using

weighted average

14

20-10, 20-11,

20-12

20-15, 20-16,

20-22

20-2, 20-4,

20-5, 20-6,

20-8, 20-9

20-7

C4. Describe accounting for

production activity and

preparation of a process

costing summary using FIFO.

(Appendix 20A)

20-9, 20-15

20-10, 20-11,

20-13, 20-16,

20-21

20-6, 20-7,

20-8, 20-9

Analytical objectives:

A1. Compare process cost

accounting and job order cost

accounting.

1, 4, 5

20-13

20-1

20-4

A2. Explain and illustrate a hybrid

costing system.

20-8

20-19

20-7

Procedural objectives:

P1. Record the flow of direct

materials costs in process cost

accounting.

5

20-2

20-1, 20-2,

20-6, 20-7,

20-14

20-1, 20-3

20-4, 20-6,

P2. Record the flow of direct

labor costs in process cost

accounting.

8, 9, 10

20-3

20-1, 20-3

20-6 , 20-7,

20-14

20-1, 20-3

20-4, 20-6,

P3. Record the flow of factory

overhead costs in process cost

accounting.

11

20-4

20-1, 20-4,

20-6, 20-7,

20-14

20-1, 20-3

20-6,

P4. Record the transfer of

completed goods to Finished

Goods Inventory and Cost of

Goods Sold.

20-5

20-5, 20-6,

20-7, 20-9,

20-11, 20-14

20-1, 20-4,

20-5, 20-6

20-9

20-6

*See additional information below that pertains to these quick studies, exercises and problems.

Note: A Comprehensive Problem is also included that provides a review of chapters 2, 5, 18, and 20.

Additional Information on Related Assignment Material

Connect (Available on the instructor’s course-specific website) repeats all numerical Quick Studies, all

Exercises and Problems Set A. Connect provides new numbers each time the Quick Study, Exercise or

Problem is worked. It allows instructors to monitor, promote, and assess student learning. It can be used

in practice, homework, or exam mode.

Corresponding problems in set B also relate to learning objectives identified in grid on previous page.

Problems 20-2A and 20-4A can be completed using EXCEL. The Serial Problem for Success Systems

starts in this chapter and continues throughout many chapters of the text. It is most readily solved

manually if you use the working papers that accompany text.

Narrated PowerPoint Correlation Guide

Learning Objective

Slides

C1

2

A1

3-10

C2

11-27

C3

28-33

A2

35

P1

37

P2

38

P3

39

P4

40

C4

41-46

Synopsis of Chapter Revisions

• Three Twins Ice Cream: NEW opener with new entrepreneurial assignment

20-3

Chapter Outline

I. Process Operations⎯Also called process manufacturing or process

production, is mass production of products in a continuous flow of steps

A. Comparing Job Order and Process Operations

1. Both manufacturers and service companies can use job order and

process production systems.

a. Custom orders

b. Heterogeneous products and services

c. Low production volume

d. High product flexibility

b. Homogeneous products and services

c. High production volume

d. Low product flexibility

with the output of the prior department.

3. Last department produces the finished goods that are ready for

sale and the accumulated costs are transferred to Finished Goods

Inventory.

1. Product is produced by mixing its active ingredient with other

materials, molding it into tablets, and then packaging the tablets.

cost per unit of a product or service.

A. Comparing Job Order and Process Cost Accounting Systems

1. Similar in that they both combine materials, labor and overhead

in the process of making products

dividend total costs for the job by the number of units in that

job.

Notes

20-4

Chapter Outline

b. Process costing measures unit costs at the end of a period by

dividing the total costs for that process by the number of units

passing through the process to determine the cost per

equivalent unit.

B. Direct and Indirect Costs

1. Materials and labor that can be traced to a specific process are

assigned to those processes as direct costs.

2. Materials and labor that cannot be traced to a specific process are

Payable.

2. Assign costs of direct materials used in production by debiting the

Goods in Process Inventory and crediting Raw Materials

Inventory.

Overhead and crediting Raw Materials Inventory.

D. Accounting for Labor Costs

crediting Cash.

2. Assign costs of direct labor used in production by debiting the

3. Assign cost of indirect labor used by debiting Factory Overhead

and crediting Factory Payroll. (Factory Payroll account should

E. Accounting for Factory Overhead⎯Same steps as in chapter 19,

except performed now for each individual department (or process).

1. Record other factory overhead items incurred by debiting Factory

Overhead and crediting the related accounts.

2. Compute each department’s predetermined overhead rate. With

increasing automation, companies are more likely to use machine

hours to allocate the overhead costs.

4. Apply factory overhead costs to each department by debiting the

Goods in Process Inventory and crediting Factory Overhead.

5. At the end of the period, close the overapplied or underapplied

balance, if immaterial in amount, to Cost of Goods Sold or if

in Process Inventory, and Finished Goods Inventory accounts.

Notes

Chapter Outline

III. Computing and Using Equivalent Units of Production⎯used to

determine the cost per unit processed by each department.

A. Accounting for Goods in Process

1. Simple if a department (or process) has no beginning or ending

goods in process inventory⎯unit cost of goods transferred out of

the department equals the total cost assigned to the process (direct

materials, direct labor, and factory overhead) divided by the total

number of units started and finished during the period.

process), but denominator must measure the entire production

activity of the process during the period.

c. EUP are the number of units that could have been started and

completed given the costs incurred during the period. For

example, 100 units that are 60% processed had the same costs

that would be incurred to both start and finish 60 units.

B. Differences Between Equivalent Units for Materials and Equivalent

c. Factory overhead (the same as direct labor if direct labor is

used to apply overhead).

A. Step 1: Determine Physical Flow of Units

1. Reconciles the physical units started in a period with physical

units completed in that period.

Notes

20-6

Chapter Outline

B. Step 2: Compute Equivalent Units of Production (EUP)

1. The focus is on what was done during the period.

a. Can be calculated using first-in, first-out basis (FIFO),

weighted average, or last-in, first-out basis (LIFO).

b. Text assumes Gen-X uses weighted average method. (The

based on the amount of each input (direct materials, direct labor,

and overhead) that has been used.

the units are treated as part of a large pool with an average cost

per unit

two-step calculation:

a. Units completed during the period times 100% (since the

units have all required materials).

5. Equivalent Units⎯Direct Labor and Factory Overhead⎯add

together the results of a two-step calculation:

C. Step 3: Compute Cost per Equivalent Unit

1. The total of the costs in the beginning inventory and the costs

D. Step 4: Cost Assignment and Reconciliation

i. Cost of beginning inventory plus cost assigned to units

account for. (see 3 below).

Notes

20-7

Chapter Outline

3. Sources of amounts used in cost reconciliation:

a. Cost assigned to units completed during the period equals:

i. Direct material cost assigned during the period (equivalent

units in units completed for direct material times the

related equivalent cost per unit).

ii. Direct labor cost assigned during the period (equivalent

units in units completed for direct labor times the related

equivalent cost per unit).

iii. Factory overhead cost assigned during the period

(equivalent units in units completed for factory overhead

production department

3. Purposes:

a. Help managers control and monitor departments.

b. Helps factory managers evaluate department managers’

performance.

c. Provides cost information for financial statements.

4. Three sections:

d. Costs charged to production.

1. Record cost of units transferred out by debiting Finished Goods

Inventory and crediting Goods in Process Inventory.

costs through accounts reflects the flow of manufacturing activities

and products in the factory.

Notes

20-8

Chapter Outline

V. Decision Analysis—Hybrid Costing System

A. Contains features of both job order and process operations

1. Materials Costs are often applied to specific jobs as in a job order

B. A hybrid system of processes requires a hybrid costing system.

1. Assembly line costs may be compiled using process costing.

2. Customizing the product may use a job order system.

VI. Appendix 20A – FIFO method of process costing

A. The objectives, concepts, and journal entries (but not amounts) are the

same as for the weighted average method.

B. The computation of equivalent units of production and cost

units plus units started and completed) during the period plus

units in ending inventory equal units accounted for.

added during the period.

b. Units started and completed during the period times 100%

(since all materials were added during the period).

b. Units started and completed during the period times 100%

(since all labor and overhead was added during the period).

c. Units in ending inventory times the percent of labor and

overhead added during the period.

Notes

20-9

Chapter Outline

E. Step 3: Compute Cost per Equivalent Unit

cost per equivalent unit for the period.

2. Perform calculation separately for direct materials, direct labor,

F. Step 4: Cost Assignment and Reconciliation

1. Similar in concept to the reconciliation of the physical flow of

2. The following totals should agree:

a. Costs of beginning inventory plus costs incurred during the

period (i.e., amounts debited to the Goods in Process

Inventory during the period) equals total costs to account for.

b. Costs assigned to the completed beginning inventory units,

beginning balance of the Goods in Process Inventory plus the

following costs to complete the beginning inventory:

i. Direct material cost assigned: (EU to complete beginning

inventory for direct materials X the equivalent cost per

unit).

ii. Direct labor cost assigned: (EUs in ending inventory for

direct labor X equivalent cost per unit).

iii. Factory overhead cost assigned: (EU in ending inventory

for factory overhead X equivalent cost per unit).

Notes

20–10

Alternate Demo Problem Twenty

The Malbim Company uses a process costing system. Materials are added

at the beginning of the process. On July 1 there are 400 units in the

beginning inventory that are 100% complete as to materials. With regard to

labor and overhead, however, the units in beginning inventory (July 1) are

only 75% complete.

During July, 10,000 units were started in production; of these, 7,000 were

completed and transferred to the next department. On July 31, the

remaining 3,000 units were 20% complete with regard to labor and

overhead.

Required:

Using the Weighted Average method, calculate the equivalent units of

Direct Materials

Direct Labor and Factory Overhead

Using the FIFO method, calculate the equivalent units of

Direct Materials

Direct Labor and Factory Overhead

20–11

Solution: Alternate Demo Problem Twenty

Weighted-average Method

Direct

Materials

Direct Labor

and Factory

Overhead

Units completed this period*

7,400

7,400

Equivalent units in ending inventory

3,000 units x 100%

3,000

3,000 units x 20%

_____

600

Total equivalent units

10,400

8,800

Solution: Alternate Demo Problem Twenty

FIFO Method

Direct

Materials

Direct Labor

and Factory

Overhead

Equivalent units needed to complete

beginning inventory:

400 units x 0%*

0

400 units x 25%

100

Units started and completed

7,000

7,000

Equivalent units in ending inventory

3,000 units x 100%

3,000

3,000 units x 20%

_____

600

Total equivalent units

10,000

7,700