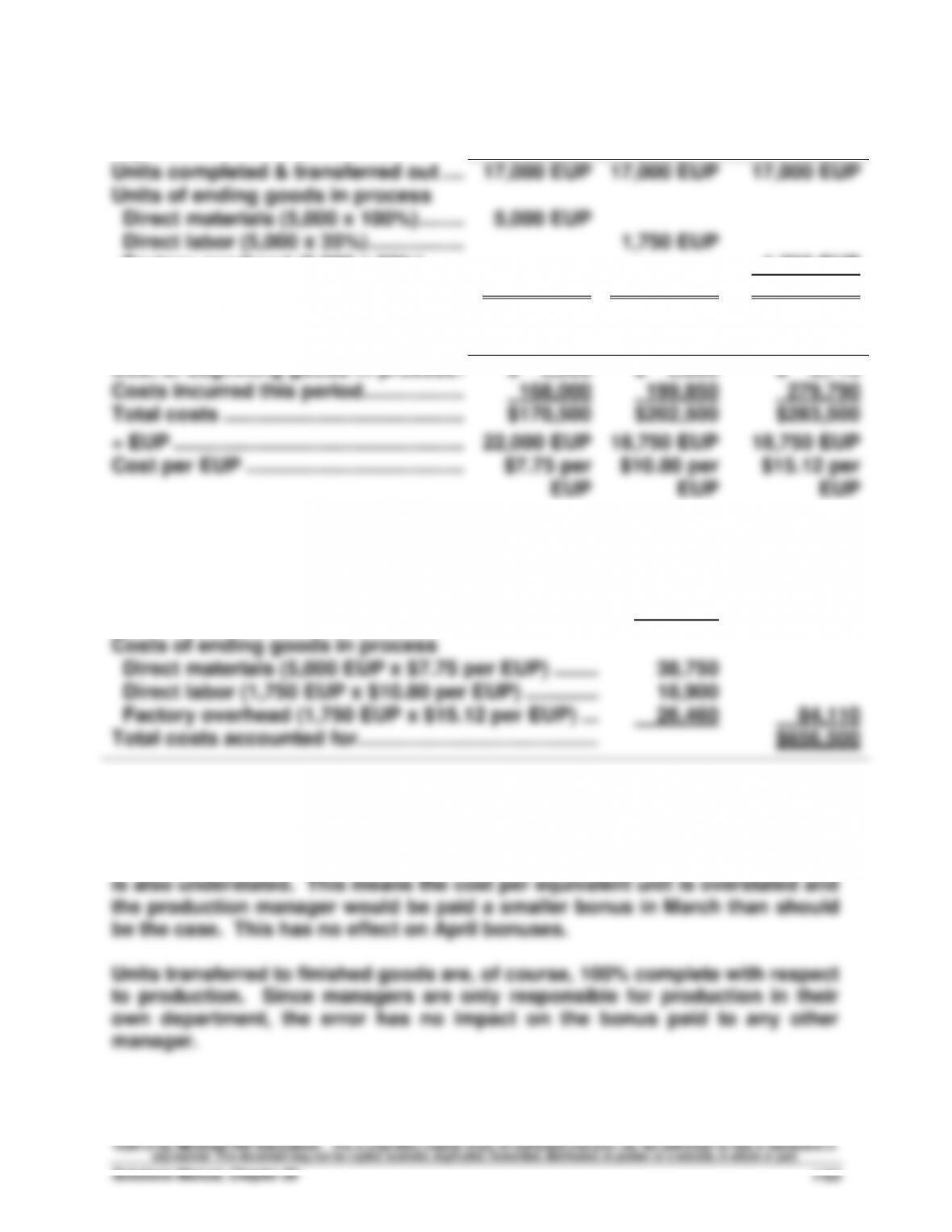

Problem 20-3A (Concluded)

Equivalent units of production

Direct

Materials

Direct

Labor

Factory

Overhead

Units completed & transferred out ….

17,000 EUP

17,000 EUP

17,000 EUP

Units of ending goods in process

Direct materials (5,000 x 100%) ……..

5,000 EUP

Direct labor (5,000 x 35%) ……………..

1,750 EUP

Factory overhead (5,000 x 35%) …….

__________

__________

1,750 EUP

Equivalent units of production ……….

22,000 EUP

18,750 EUP

18,750 EUP

Cost per EUP

Direct

Materials

Direct

Labor

Factory

Overhead

Cost of beginning goods in process .

$ 2,500

$ 2,650

$ 3,710

Costs incurred this period ………………

168,000

199,850

279,790

Total costs …………………………………….

$170,500

$202,500

$283,500

÷ EUP …………………………………………….

22,000 EUP

18,750 EUP

18,750 EUP

Cost per EUP …………………………………

$7.75 per

EUP

$10.80 per

EUP

$15.12 per

EUP

Cost assignment and reconciliation

Costs transferred out

Direct materials (17,000 EUP x $7.75 per EUP) ……

$131,750

Direct labor (17,000 EUP x $10.80 per EUP) ………..

183,600

Factory overhead (17,000 x $15.12 per EUP) ……….

257,040

$572,390

Costs of ending goods in process

Direct materials (5,000 EUP x $7.75 per EUP) ……..

38,750

Direct labor (1,750 EUP x $10.80 per EUP) ………….

18,900

Factory overhead (1,750 EUP x $15.12 per EUP) …

26,460

84,110

Total costs accounted for …………………………………….

$656,500

Part 3

If equivalent units of production for the production department’s ending

inventory for March are understated, then total equivalent units of production

Fundamental Accounting Principles, 21st Edition

1164

Problem 20-4A (75 minutes)

Part 1

FAST CO.

Process Cost Summary – Weighted Average Method

For the month ended October 31

Costs charged to Production

Costs of beginning goods in process

Direct materials ……………………………………………………….

$ 59,450

Direct labor ……………………………………………………………...

172,800

Factory overhead ……………………………………………………..

103,680

$ 335,930

Costs incurred this period

Direct materials ……………………………………………………….

102,050

Direct labor ……………………………………………………………...

408,200

Factory overhead ……………………………………………………..

244,920

755,170

Total costs to account for …………………………………………..

$1,091,100

Unit cost information

Units to account for

Units accounted for

Beginning goods in process ….……………………….

30,000

Completed & transferred out ..…………

150,000

Units started this period ………..…………………

140,000

Ending goods in process ….…………

20,000

Total units to account for …………………………..

170,000

Total units accounted for ….…………

170,000

Equivalent units of production

Direct

Materials

Direct

Labor

Factory

Overhead

Units completed & transferred out …..

150,000 EUP

150,000 EUP

150,000 EUP

Units of ending goods in process

Direct materials (20,000 x 100%) …...

20,000 EUP

Direct labor (20,000 x 80%) …………...

16,000 EUP

Factory overhead (20,000 x 80%) …..

__________

__________

16,000 EUP

Equivalent units of production

170,000 EUP

166,000 EUP

166,000 EUP

Cost per EUP

Direct

Materials

Direct

Labor

Factory

Overhead

Cost of beginning goods in process ...

$ 59,450

$172,800

$103,680

Costs incurred this period ……………...

102,050

408,200

244,920

Total costs ……………………………………..

$161,500

$581,000

$348,600

÷ EUP ……………………………………………..

170,000 EUP

166,000 EUP

166,000 EUP

Cost per EUP …………………………..……..

$0.95 per EUP

$3.50 per EUP

$2.10 per EUP

[Continued on next page]

Problem 20-4A (Concluded)

Cost assignment and reconciliation

Costs transferred out

Direct materials (150,000 EUP x $0.95 per EUP) ….

$142,500

Direct labor (150,000 EUP x $3.50 per EUP) ………..

525,000

Factory overhead (150,000 x $2.10 per EUP) ……….

315,000

$ 982,500

Costs of ending goods in process

Direct materials (20,000 EUP x $0.95 per EUP) ……

19,000

Direct labor (16,000 EUP x $3.50 per EUP) ………….

56,000

Factory overhead (16,000 EUP x $2.10 per EUP) …

33,600

108,600

Total costs accounted for …………………………………….

$1,091,100

Part 2

Oct. 31

Finished Goods Inventory ……………………………………..

982,500

Goods in Process Inventory …………………………..

982,500

Transfer of goods to finished goods inventory.

Fundamental Accounting Principles, 21st Edition

1166

Problem 20-5A (80 minutes)

Part 1

TAMAR CO.

Process Cost Summary – Weighted Average Method

For Month Ended May 31

Costs Charged to Production

Costs of beginning goods in process

Direct materials ………………………………………………..……..

$ 19,800

Direct labor ……………………………………………………….

123,300

Factory overhead ……………………………………………..………

98,640

$ 241,740

Costs incurred this period

Direct materials ………………………………………………..……..

496,800

Direct labor ……………………………………………………….

1,203,300

Factory overhead ……………………………………………..………

962,640

2,662,740

Total costs to account for …………………………………..………

$2,904,480

Unit cost information

Units to account for

Units accounted for

Beginning goods in process …………………………..

3,000

Completed & transferred out ….…….

22,200

Units started this period ……….………………….

21,600

Ending goods in process …………….

2,400

Total units to account for ……..……………………

24,600

Total units accounted for …………….

24,600

Equivalent units of production

Direct

Materials

Direct

Labor

Factory

Overhead

Units completed & transferred out …….

22,200 EUP

22,200 EUP

22,200 EUP

Units of ending goods in process ……..

Direct materials (2,400 x 100%) ……..

2,400 EUP

Direct labor (2,400 x 80%) ……………..

1,920 EUP

Factory overhead (2,400 x 80%) …….

__________

__________

1,920 EUP

Equivalent units of production ………..

24,600 EUP

24,120 EUP

24,120 EUP

Cost per EUP

Direct

Materials

Direct

Labor

Factory

Overhead

Cost of beginning goods in process ….

$ 19,800

$ 123,300

$ 98,640

Costs incurred this period ………………

496,800

1,203,300

962,640

Total costs ……………………………………..

$516,600

$1,326,600

$1,061,280

÷ EUP ……………………………………………..

24,600 EUP

24,120 EUP

24,120 EUP

Cost per EUP …………………………..……..

$21 per EUP

$55 per EUP

$44 per EUP

[Continued on next page]

Problem 20-5A (Concluded)

Cost assignment and reconciliation

Costs transferred out

Direct materials (22,200 EUP x $21.00 per EUP) ……………..

$

466,200

Direct labor (22,200 EUP x $55.00 per EUP) ………….………..

1,221,000

Factory overhead (22,200 x $44.00 per EUP) …………………..

976,800

$2,664,000

Costs of ending goods in process

Direct materials (2,400 EUP x $21.00 per EUP) ……..………..

50,400

Direct labor (1,920 EUP x $55.00 per EUP) ……………………..

105,600

Factory overhead (1,920 EUP x $44.00 per EUP) …..………..

84,480

240,480

Total costs accounted for ………………………………………………..

$2,904,480

Part 2

May 31

Finished Goods Inventory …………………………..

2,664,000

Goods in Process Inventory ………………….……….

2,664,00

0

Transfer of goods to finished inventory.

Part 3

3a. Two major estimates are the: i) overhead allocation rate, and ii)

3b. Management might want an overhead allocation rate that assigns the

least amount of overhead applied to their respective production

Fundamental Accounting Principles, 21st Edition

1168

Problem 20-6A (80 minutes)

Part 1

TAMAR CO.

Process Cost Summary – FIFO Method

For Month Ended May 31

Costs charged to Production

Costs of beginning goods in process

Direct materials ………………………………………………….……

$ 19,800

Direct labor ………………………………………………………..…….

123,300

Factory overhead ……………………………………………….…….

98,640

$ 241,740

Costs incurred this period

Direct materials ………………………………………………….……

496,800

Direct labor ………………………………………………………..…….

1,203,300

Factory overhead ……………………………………………….…….

962,640

2,662,740

Total costs to account for …………………………………….…….

$2,904,480

Unit cost information

Units to account for

Units accounted for

Beginning goods in process ….……………………….

3,000

Completed & transferred out ………..

22,200

Units started this period ………..…………………

21,600

Ending goods in process …….……..

2,400

Total units to account for …………………………..

24,600

Total units accounted for …….……..

24,600

Equivalent units of production

Direct

Materials

Direct

Labor

Factory

Overhead

Units to complete beginning goods in process

Direct materials (3,000 x 0%) ………………..……..

0 EUP

Direct labor (3,000 x 60%) …………………….…….

1,800 EUP

Factory overhead (3,000 x 60%) …………………..

1,800 EUP

Units started and completed …………………..……..

19,200 EUP

19,200 EUP

19,200 EUP

Units of ending goods in process

Direct materials (2,400 x 100%) …………….……..

2,400 EUP

Direct labor (2,400 x 80%) …………………….…….

1,920 EUP

Factory overhead (2,400 x 80%) …………………..

_________

_________

1,920 EUP

Equivalent units of production ……………….……..

21,600 EUP

22,920 EUP

22,920 EUP

[Continued on next page]

Problem 20-6A (Concluded)

Cost per EUP

Direct

Materials

Direct

Labor

Factory

Overhead

Costs incurred this period ………………

$ 496,800

$1,203,300

$ 962,640

÷ EUP …………………………………………….

÷ 21,600

÷ 22,920

÷ 22,920

Cost per EUP …………………………………

$23.00 per

EUP

$52.50 per

EUP

$42.00 per

EUP

Cost assignment and reconciliation

Costs transferred out

Cost of beginning goods in process …………………….

$ 241,740

Cost to complete beginning goods in process

Direct materials (0 EUP x $23.00 per EUP) ………….

$ 0

Direct labor (1,800 EUP x $52.50 per EUP) ………….

94,500

Factory overhead (1,800 EUP x $42.00 per EUP) …

75,600

170,100

Costs of units started and completed this period

Direct materials (19,200 EUP x $23.00 per EUP) ….

441,600

Direct labor (19,200 EUP x $52.50 per EUP) ………..

1,008,000

Factory overhead (19,200 EUP x $42.00 per EUP) .

806,400

2,256,000

Total cost of goods finished this period ……………….

2,667,840

Costs of ending goods in process

Direct materials (2,400 EUP x $23.00 per EUP) ……

55,200

Direct labor (1,920 EUP x $52.50 per EUP) ………….

100,800

Factory overhead (1,920 EUP x $42.00 per EUP) …

80,640

236,640

Total costs accounted for …………………………………….

$2,904,480

Part 2

May 31

Finished Goods Inventory …………………………..

2,667,840

Goods in Process Inventory …………………………..

2,667,840

Transfer of goods to finished inventory.

Fundamental Accounting Principles, 21st Edition

1170

Problem 20-7A (45 minutes)

1.

Units in beginning inventory …………………………………..

37,500

Units started and completed …………………………………..

150,000

Total units transferred to finished goods ………………..

187,500

2. Equivalent units of production—FIFO

Direct

Direct

Equivalent units of production

Materials

Labor

Units to complete beginning goods in process

Direct materials (37,500 x 40%) …………………………...

15,000

Direct labor (37,500 x 60%) ………………………………….

22,500

Units started and completed …………………………………

150,000

150,000

Units in ending work in process

Direct materials (51,250 x 60%) …………………………...

30,750

Direct labor (51,250 x 20%) ………………………………….

_______

10,250

Equivalent units of production ……………………………..

195,750

182,750

3. Cost per equivalent unit of direct materials and direct labor—FIFO

Direct

Direct

Materials

Labor

Costs incurred this period …………………………………….

$ 505,035

$ 396,568

÷ Equivalent units of production (from part 2) ……….

195,750

182,750

Cost per equivalent unit of production ………………….

$2.58 per

EUP

$2.17 per

EUP

Problem 20-7A (Concluded)

4. Assignment of costs to output of department—FIFO

Costs of goods transferred out

Cost of beginning goods in process inventory …..….

Direct materials ………………………………………………….

$74,075.00

Direct labor …………………………………………………….…

28,493.00

$ 102,568.00

Costs to complete beginning goods in process

Direct materials (15,000 EUP x $2.58 per EUP) …….

38,700.00

Direct labor (22,500 EUP x $2.17 per EUP) ……….….

48,825.00

Total costs to complete …………………………………..….

87,525.00

Cost of units started and completed this period

Direct materials (150,000 EUP x $2.58 per EUP) .….

387,000.00

Direct labor (150,000 EUP x $2.17 per EUP) ……..….

325,500.00

Total cost of units started and completed ………..….

712,500.00

Total costs of goods transferred out………………….….

902,593.00

Cost of ending goods in process inventory

Direct materials (30,750 EUP x $2.58 per EUP) …….

79,335.00

Direct labor (10,250 EUP x $2.17 per EUP) ……….….

22,242.50

Total costs of ending goods in process …………..….

101,577.50

Total costs accounted for ………………………………….….

$1,004,170.50

Fundamental Accounting Principles, 21st Edition

1172

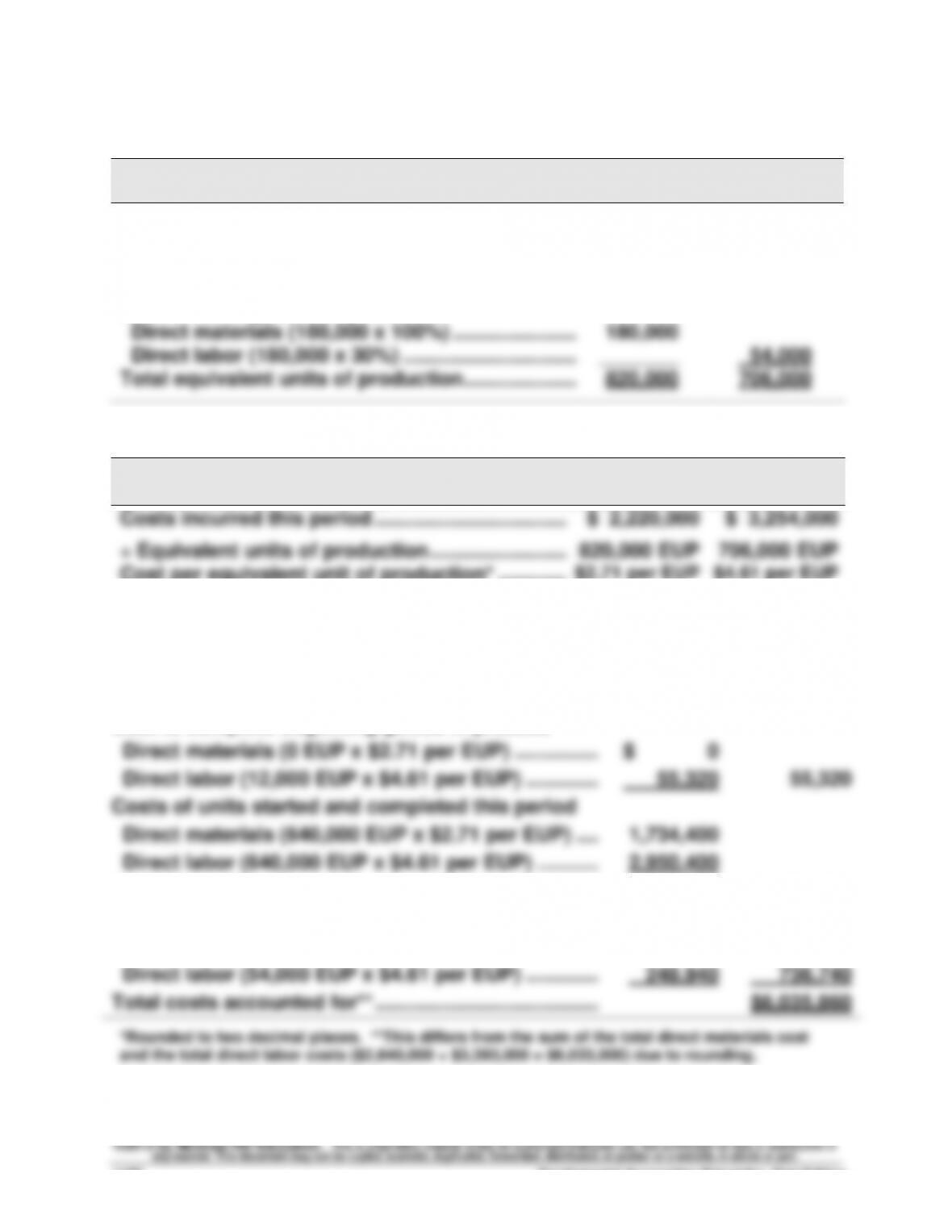

Problem 20-8A (50 minutes)

Part 1 Equivalent units with respect to direct materials and direct labor

Direct

Direct

Equivalent units of production (EUP)

Materials

Labor

Units to complete beginning goods in process

Direct materials (60,000 x 0%) ……………………….

0

Direct labor (60,000 x 20%) …………………………...

Units started and completed …………………………..

640,000

12,000

640,000

Units in ending work in process

Direct materials (180,000 x 100%) ………………….

180,000

Direct labor (180,000 x 30%) ………………………….

_______

54,000

Total equivalent units of production ………………..

820,000

706,000

Part 2

Cost per equivalent unit of production

Direct

Materials

Direct

Labor

Costs incurred this period ……………………………..………

$ 2,220,000

$ 3,254,000

÷ Equivalent units of production …………………….…….

820,000 EUP

706,000 EUP

Cost per equivalent unit of production* ………….………

$2.71 per EUP

$4.61 per EUP

Part 3 Assigning product costs to units

Cost assignment and reconciliation

Costs transferred out

Cost of beginning goods in process …………………….

$ 559,000

Cost to complete beginning goods in process

Direct materials (0 EUP x $2.71 per EUP) ……………

$ 0

Direct labor (12,000 EUP x $4.61 per EUP) ………….

55,320

55,320

Costs of units started and completed this period

Direct materials (640,000 EUP x $2.71 per EUP) ….

1,734,400

Direct labor (640,000 EUP x $4.61 per EUP) ………..

2,950,400

Total cost of goods finished this period ……………….

4,684,800

Costs of ending goods in process

Direct materials (180,000 EUP x $2.71 per EUP) ….

487,800

Direct labor (54,000 EUP x $4.61 per EUP) ………….

248,940

736,740

Total costs accounted for** ………………………………….

$6,035,860

*Rounded to two decimal places. **This differs from the sum of the total direct materials cost

and the total direct labor costs ($2,640,000 + $3,393,000 = $6,033,000) due to rounding.

Problem 20-8A (Concluded)

Part 4

MEMORANDUM

TO:

FROM:

DATE:

RE: Percentage of Completion Error Analysis

If the units in ending inventory are 60% complete instead of 30% with

respect to labor, the number of equivalent units in ending inventory with

inventory is greater.

Regarding financial statements, this error causes an overstatement of cost

Fundamental Accounting Principles, 21st Edition

1174

Problem 20-9A (80 minutes)

Part 1

DENGO CO.

Process Cost Summary – FIFO Method

For Month Ended October 31

Costs Charged to Production

Costs of beginning goods in process

Direct materials ………………………………………………….……

$ 9,900

Direct labor ………………………………………………………..…….

61,650

Factory overhead ……………………………………………….…….

49,320

$ 120,870

Costs incurred this period

Direct materials ………………………………………………….……

248,400

Direct labor ………………………………………………………..…….

601,650

Factory overhead ……………………………………………….…….

481,320

1,331,370

Total costs to account for …………………………………….…….

$1,452,240

Unit cost information

Units to account for

Units accounted for

Beginning goods in process …………………………..

3,000

Completed & transferred out ….…….

22,200

Units started this period ……….………………….

21,600

Ending goods in process …………….

2,400

Total units to account for ……..……………………

24,600

Total units accounted for …………….

24,600

Equivalent units of production

Direct

Materials

Direct

Labor

Factory

Overhead

Units to complete beginning goods in process

Direct materials (3,000 x 0%) ………………..……..

0 EUP

Direct labor (3,000 x 60%) …………………….…….

1,800 EUP

Factory overhead (3,000 x 60%) …………………..

1,800 EUP

Units started and completed …………………..……..

19,200 EUP

19,200 EUP

19,200 EUP

Units of ending goods in process

Direct materials (2,400 x 100%) …………….……..

2,400 EUP

Direct labor (2,400 x 80%) …………………….…….

1,920 EUP

Factory overhead (2,400 x 80%) …………………..

_________

_________

1,920 EUP

Equivalent units of production ……………….……..

21,600 EUP

22,920 EUP

22,920 EUP

[Continued on next page]

Problem 20-9A (Continued)

Cost per EUP

Direct

Materials

Direct

Labor

Factory

Overhead

Costs incurred this period ………………

$ 248,400

$ 601,650

$ 481,320

÷ EUP …………………………………………….

÷ 21,600

÷ 22,920

÷ 22,920

Cost per EUP …………………………………

$11.50 per

EUP

$26.25 per

EUP

$21.00 per

EUP

Cost assignment and reconciliation

Costs transferred out

Cost of beginning goods in process …………………….

$ 120,870

Cost to complete beginning goods in process

Direct materials (0 EUP x $11.50 per EUP) ………….

$ 0

Direct labor (1,800 EUP x $26.25 per EUP) ………….

47,250

Factory overhead (1,800 EUP x $21.00 per EUP) …

37,800

85,050

Costs of units started and completed this period

Direct materials (19,200 EUP x $11.50 per EUP) ….

220,800

Direct labor (19,200 EUP x $26.25 per EUP) ………..

504,000

Factory overhead (19,200 EUP x $21.00 per EUP) .

403,200

1,128,000

Total cost of goods finished this period ……………….

1,333,920

Costs of ending goods in process

Direct materials (2,400 EUP x $11.50 per EUP) ……

27,600

Direct labor (1,920 EUP x $26.25 per EUP) ………….

50,400

Factory overhead (1,920 EUP x $21.00 per EUP) …

40,320

118,320

Total costs accounted for …………………………………….

$1,452,240

Part 2

Oct. 31

Finished Goods Inventory ………………….……….

1,333,920

Goods in Process Inventory ………….……………….

1,333,920

Transfer of goods to finished goods

inventory.

Fundamental Accounting Principles, 21st Edition

1176

Problem 20-9A (Concluded)

Part 3

If equivalent units of production for the production department’s ending

inventory for October are understated, then total equivalent units of

production is also understated. This means the cost per equivalent unit for

PROBLEM SET B

Problem 20-1B (45 minutes)

Part 1: Cost of goods transferred and cost of goods sold

Beginning goods in process inventory …………………………………....

$156,000

Direct materials used in production ………………………………………...

120,000

Direct labor used in production ……………………………………………....

350,000

Overhead applied (75% of direct labor cost) ……………………………..

262,500

Total production costs …………………………………………………………....

888,500

Less ending goods in process inventory ………………………………....

(250,000)

Transferred to finished goods inventory (a) ……………………………..

$638,500

Beginning finished goods inventory …………………………..…………..

$160,000

Plus goods transferred from production ………………………………....

638,500

Goods available for sale ……………………………………………………….

798,500

Less ending finished goods inventory ……………………………………..

(198,000)

Cost of goods sold (b) …………………………………………………………....

$600,500

Part 2: Summary journal entries

a.

June 30

Raw Materials Inventory …………………………….………….

200,000

Accounts Payable ………………………………..………….

200,000

Purchased raw materials.

b.

June 30

Goods in Process Inventory ……………………….….

120,000

Raw Materials Inventory ………………………..…

120,000

Used direct materials.

c.

June 30

Factory Overhead ……………………………………..………….

42,000

Raw Materials Inventory ……………………….….

42,000

Used indirect materials.