Title: Problem 15-3A

QA_Ori:

Part 1

2013

Jan. 20 Long-Term Investments—AFS (J&J) 20,740

Feb. 9 Long-Term Investments—AFS (Sony) 55,665

June 12 Long-Term Investments—AFS (Mattel) 40,695

Dec. 31 Unrealized LossEquity 3,650

Fair Value Adjustment—AFS (LT)* 3,650

Annual adjustment to fair values.

* Cost Fair

Value

J & J $ 20,740 $ 21,500

J & J: 1,000 x $21.50 = $21,500

2014

Apr. 15 Cash 22,975

July 5 Cash 35,615

July 22 Long-Term Investments—AFS (Sara Lee) 13,980

Aug. 19 Long-Term Investments—AFS (Eastman Kodak) 15,498

Dec. 31 Unrealized LossEquity 10,168

* Cost Fair

Value

Kodak $15,498 $17,325

2015

Feb. 27 Long-Term Investments—AFS (Microsoft) 161,325

June 21 Cash 56,720

June 30 Long-Term Investments—AFS (Black & Decker) 50,835

Aug. 3 Cash 9,315

Nov. 1 Cash 19,850

Gain on Sale of Investments 4,352

Dec. 31 Fair Value Adjustment—AFS (LT)* 21,858

* Cost Fair

Value

Black & Decker $ 50,835 $ 54,600

Fair Value Adjustment account:

Part 2

12/31/2013 12/31/2014 12/31/2015

Long-Term AFS Securities (cost) $117,100 $85,143 $212,160

2013 2014 2015

Realized gains (losses)

* Equals the balance of the Fair Value Adjustment account.

Title: Problem 15-4A

QA_Ori:

Part 1

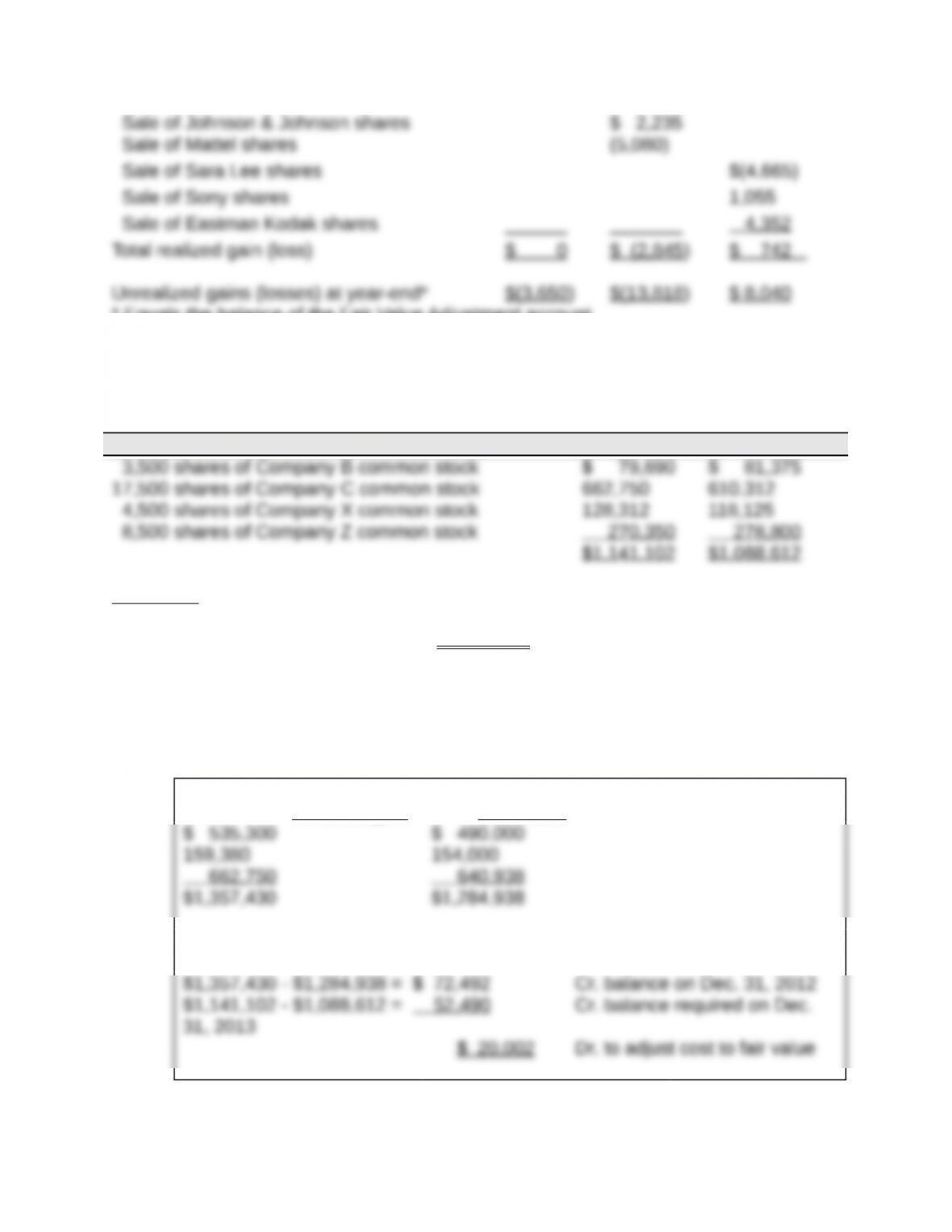

Available-for-sale securities on December 31, 2013

Security Cost Fair Value

Disclosure

The portfolio of available-for-sale securities would be reported on the December 31,

2013, balance sheet at its fair value of $1,088,612.

Part 2

Dec. 31 Fair Value Adjustment—AFS* 20,002

Unrealized Loss—Equity 20,002

Adjustment to fair value for AFS securities..

* December 31, 2012, available-for-sale securities

Cost _ Fair Value

December 31, 2013, adjustment to the Fair Value Adjustment account:

Part 3

Only gains or losses realized on the sale of available-for-sale securities appear on the

Year 2013 realized gains (losses)

Stock Sold Cost Sale Gain (Loss)

Title: Problem 15-5A

QA_Ori:

Part 1

1. Journal entries (assuming significant influence)

2013

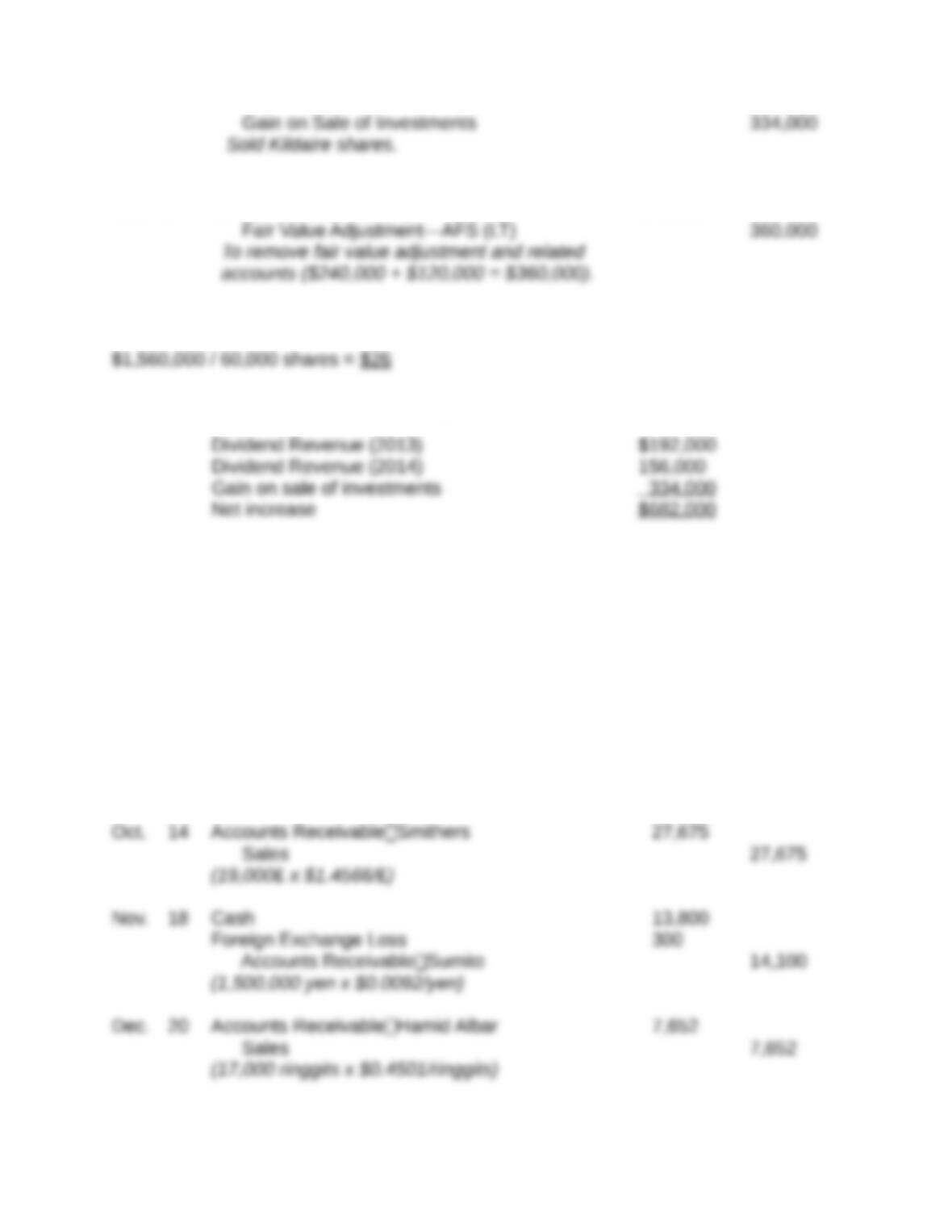

Oct. 23 Cash 192,000

Dec. 31 Long-Term Investments—Kildaire 232,800

2014

Oct. 15 Cash 156,000

Dec. 31 Long-Term Investments—Kildaire 295,200

2015

Jan. 2 Cash 1,894,000

Original cost $1,560,000

3. Change in Selk’s equity due to stock investment

Part 2

1. Journal entries (assuming NO significant influence)

2013

Oct. 23 Cash 192,000

Dec. 31 Fair Value Adjustment—AFS (LT)* 240,000

2014

Oct. 15 Cash 156,000

Dec. 31 Fair Value Adjustment—AFS (LT)* 120,000

2015

Jan. 2 Cash 1,894,000

Jan. 2 Unrealized Gain—Equity 360,000

2. Investment cost per share, January 1, 2015

3. Change in Selk’s equity due to stock investment

Title: Problem 15-6A

QA_Ori:

Part 1

2013

Apr. 8 Cash 5,938

Sales 5,938

July 21 Accounts ReceivableSumito 14,100

Sales 14,100

(1,500,000 yen x $0.0094/yen)

Dec. 31 Accounts ReceivableSmithers. 103

Foreign Exchange Gain * 103

Dec. 31 Foreign Exchange Loss* 77

Accounts ReceivableHamid Albar 77

2014

Jan. 12 Cash* 27,928

Jan. 19 Cash* 7,514

Part 2

Foreign exchange loss reported on the 2013 income statement

Part 3

To reduce the risk of foreign exchange gain or loss, Doering could attempt to negotiate

foreign customer sales that are denominated in U.S. dollars. To accomplish this,

NOTE: A few students may also understand Doering’s opportunity for hedging. This

involves selling foreign currency futures to be delivered at the time the receivables from

foreign customers will be collected.