Title: Problem 23-5A

QA_Ori:

Part 1

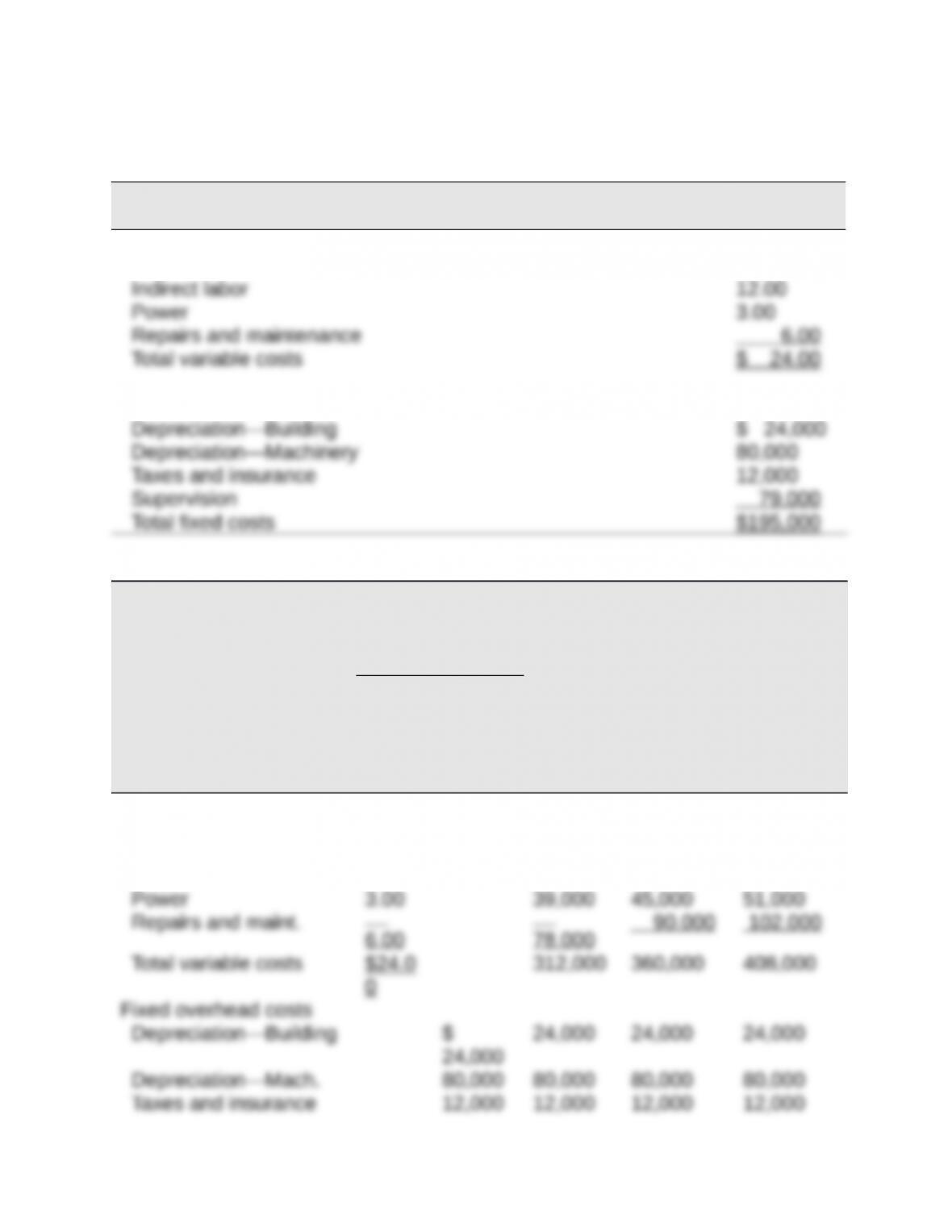

Variable or Fixed Classification

Per unit

Amount

Variable costs (total divided by 15,000 units)

Indirect materials $ 3.00

Fixed costs (per month)

Part 2

ANTUAN COMPANY

Flexible Overhead Budgets

For Month Ended October 31

Flexible Budget Flexible Flexible Flexible

Variab

le

Amou

nt per

Unit

Total

Fixed

Cost

Budget

for Unit

Sales of

13,000

Budget for

Unit Sales

of 15,000

Budget for

Unit Sales

of 17,000

Variable overhead costs

Indirect materials $

3.00

$

39,000

$ 45,000 $ 51,000

Indirect labor 12.00 156,000 180,000 204,000

0

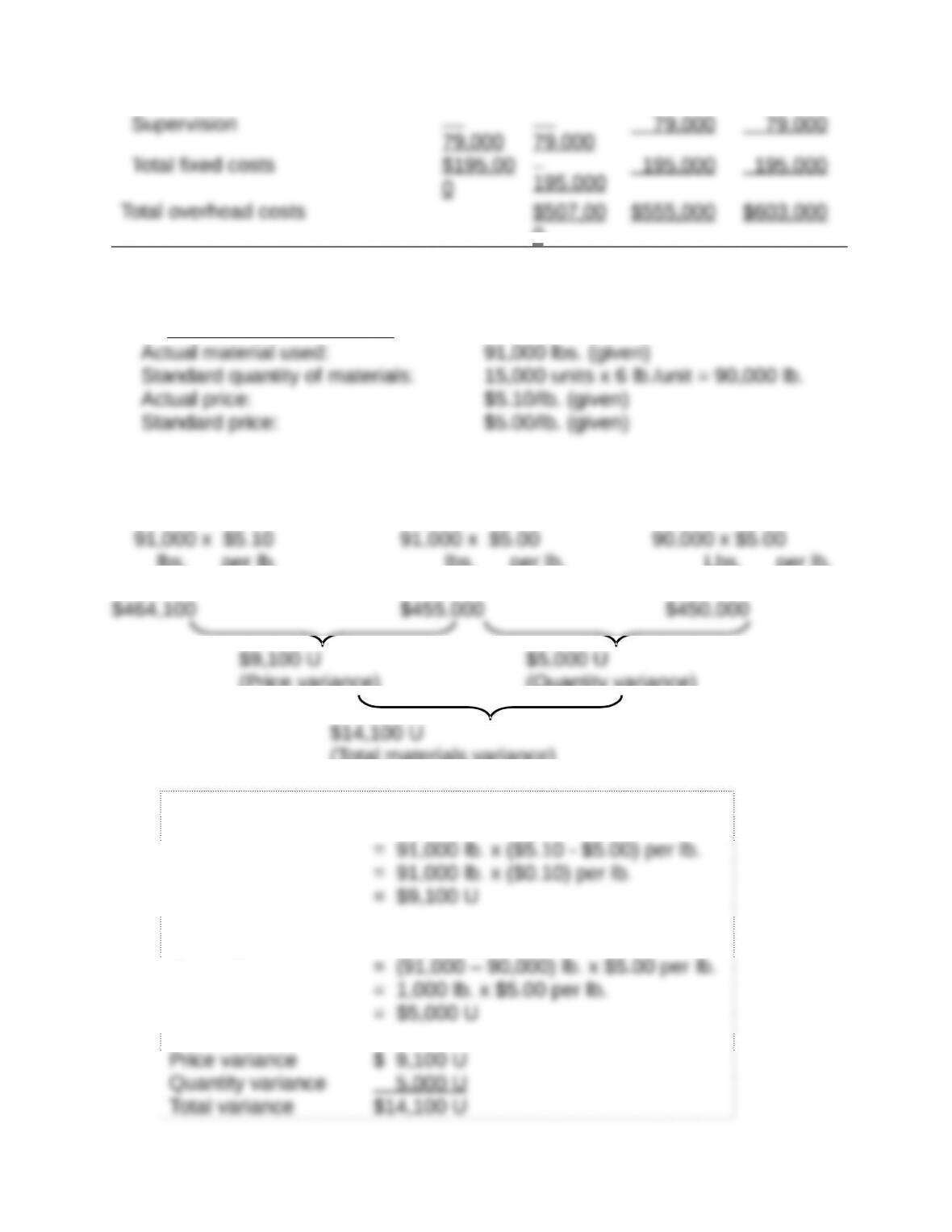

Part 3Direct Materials Variances

Preliminary computations

Direct Materials Price and Quantity Variances

Actual Costs

AQ x AP AQ x SP

Standard Costs

SQ x SP

lbs. per lb. lbs. per lb. Lbs. per lb.

(Price variance)

(Quantity variance)

(Total materials variance)

Alternate solution format

Price variance = AQ x (AP – SP)

Quantity variance = (AQ – SQ) x SP

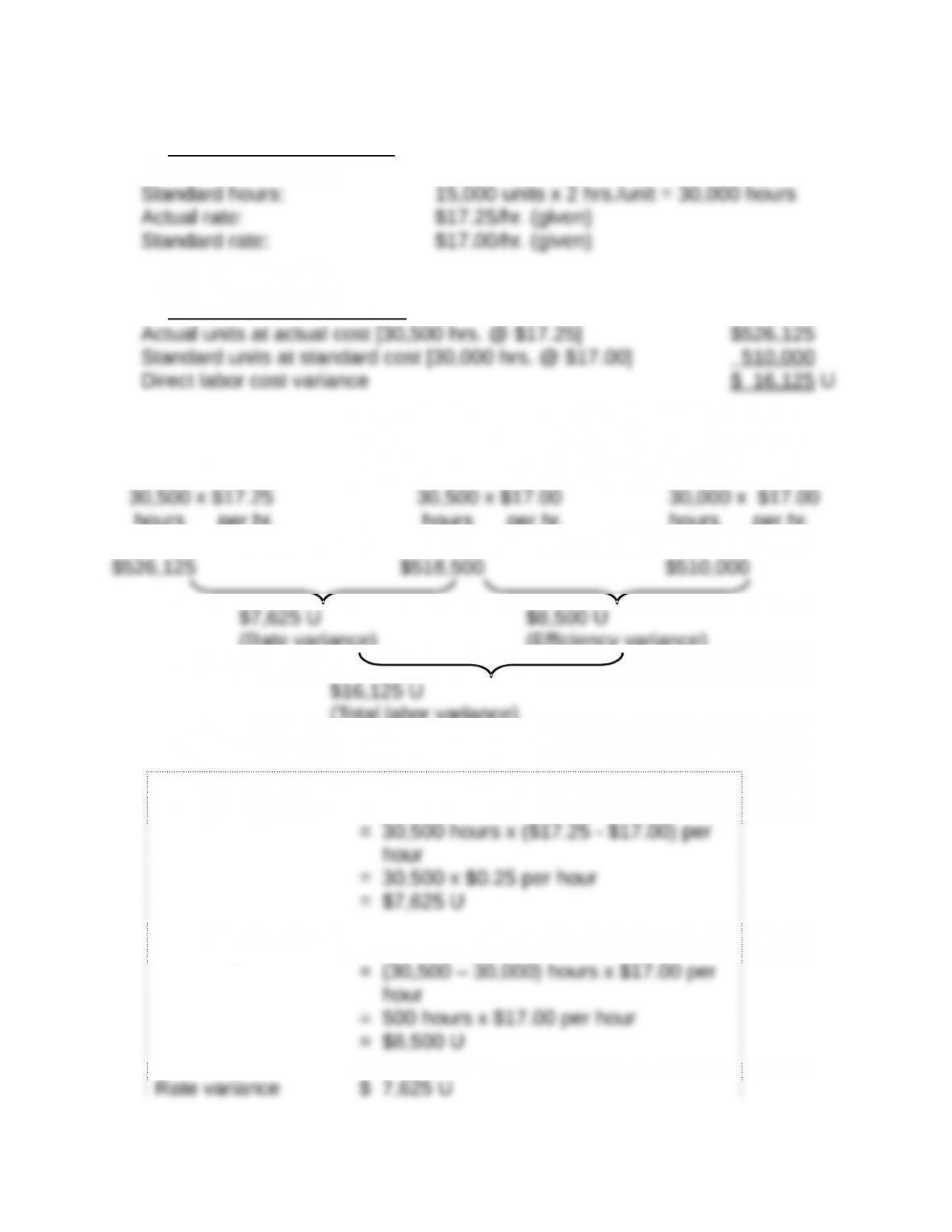

Part 4 Direct labor variances

Preliminary computations

Actual hours used: 30,500 hours (given)

Direct labor cost variances

Direct Labor Rate and Efficiency Variances

Actual Costs

AH x AR AH x SR

Standard Costs

SH x SR

hours per hr. hours per hr. hours per hr.

(Rate variance)

(Efficiency variance)

(Total labor variance)

Alternate solution format

Rate variance = AH x (AR – SR)

Efficiency variance = (AH – SH) x SR

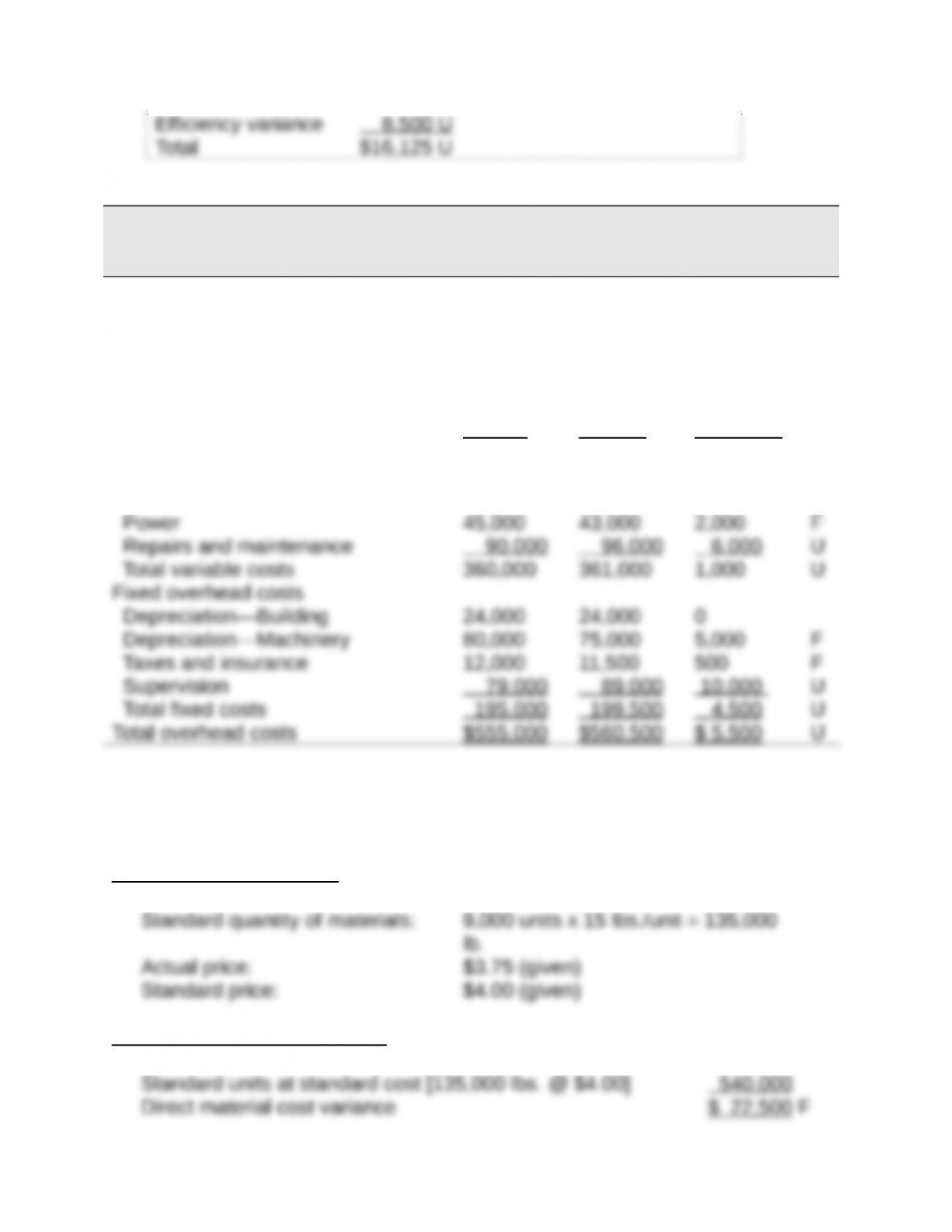

Part 5

ANTUAN COMPANY

Overhead Variance Report

For Month Ended October 31

Volume Variance

Expected production level 75% of capacity

Production level achieved 75% of capacity

Volume variance none

Flexible Actual

Controllable Variance Budget Results Variances*

Variable overhead costs

Indirect materials $ 45,000 $ 44,250 $ 750 F

Indirect labor 180,000 177,750 2,250 F

*F = Favorable variance; and U = Unfavorable variance.

Title: Problem 23-6AA

QA_Ori:

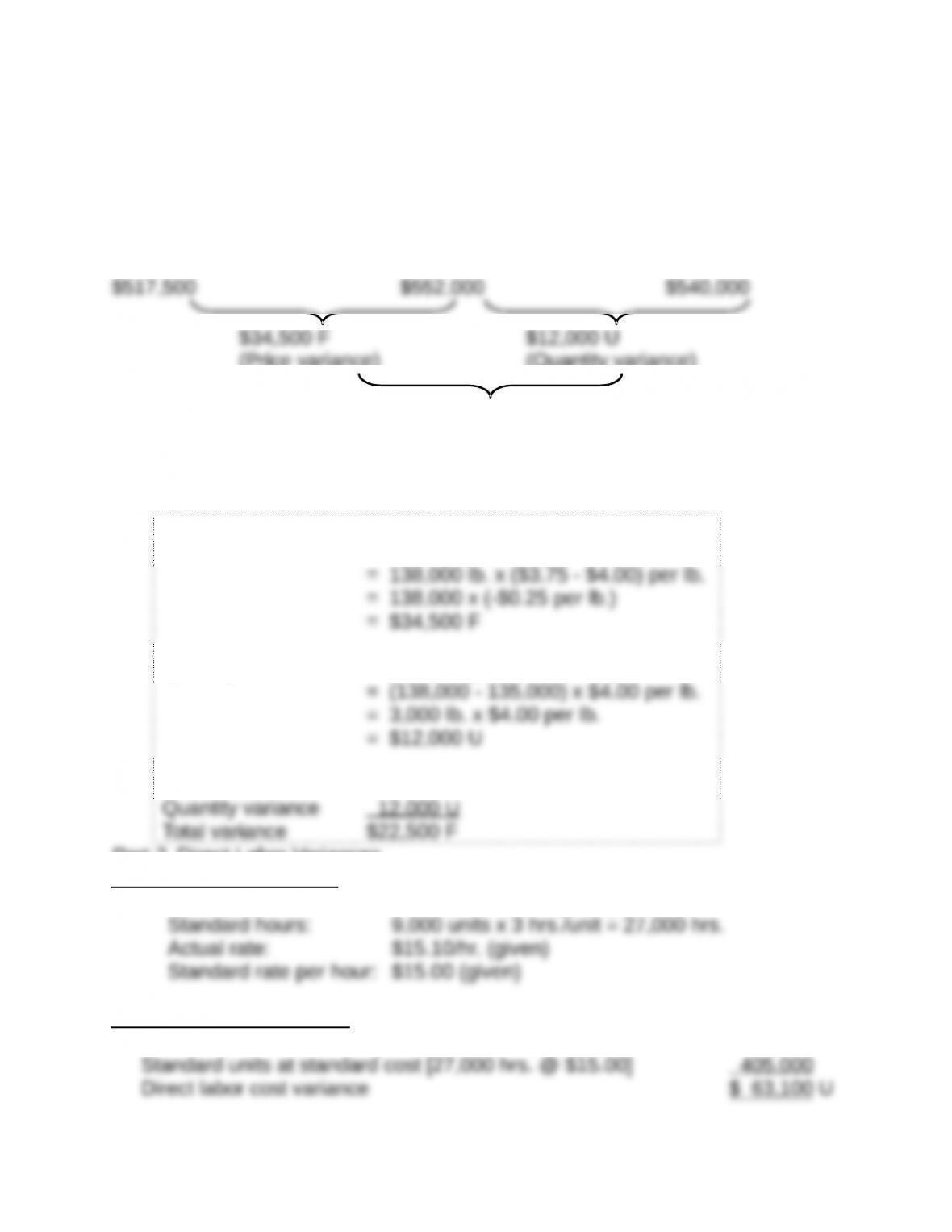

Part 1 Direct Materials Variances

Preliminary computations

Actual quantity of materials used: 138,000 lb. (given)

Direct materials cost variances

Actual units at actual cost [138,000 lbs. @ $3.75] $517,500

Direct Materials Price and Quantity Variances

Actual Cost

AQ x AP AQ x SP

Standard Cost

SQ x SP

138,000 x $3.75 138,000 x $4.00 135,000 x $4.00

lbs. per lb. lbs. per lb. lbs. per lb.

(Price variance)

(Quantity variance)

$22,500 F

(Total materials variance)

Alternate solution format

Price variance = AQ x (AP – SP)

Quantity variance = (AQ – SQ) x SP

Price variance $34,500 F

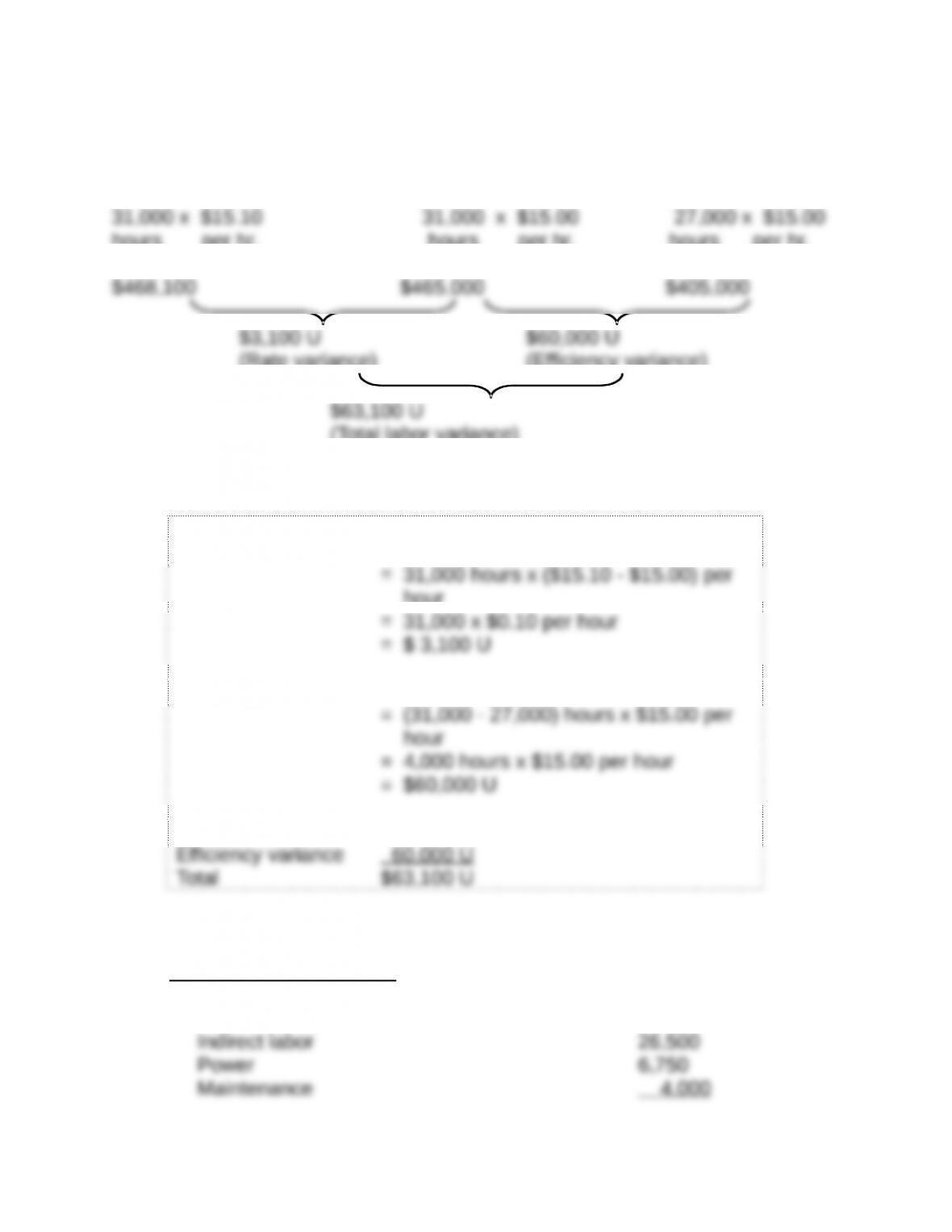

Part 2 Direct Labor Variances

Preliminary computations

Actual hours: 31,000 hrs. (given)

Direct labor cost variances

Actual units at actual cost [31,000 hrs. @ $15.10] $468,100

Direct Labor Rate and Efficiency Variances

Actual Costs

AH x AR AH x SR

Standard Costs

SH x SR

hours per hr. hours per hr. hours per hr.

(Rate variance)

(Efficiency variance)

(Total labor variance)

Alternate solution format

Rate variance = AH x (AR – SR)

hour

Efficiency variance = (AH – SH) x SR

Rate variance $ 3,100 U

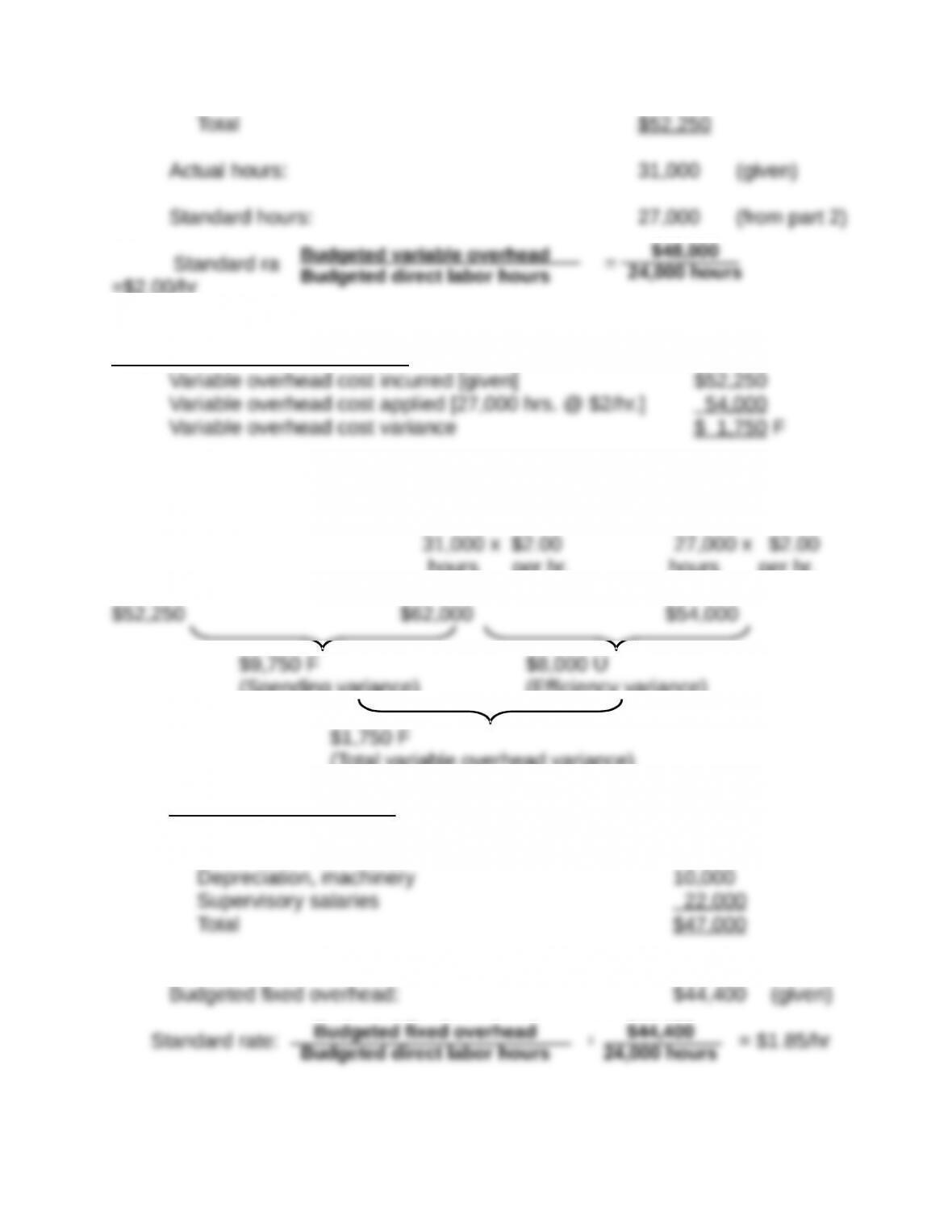

Part 3 Overhead Variances

(a) Variable overhead

Preliminary computations

Actual variable overhead (given):

Indirect materials $15,000

=$2.00/hr

Variable overhead cost variances

Variable Overhead Spending and Efficiency Variances

Actual Overhead

AH x AVR AH x SVR

Applied Overhead

SH x SVR

hours per hr. hours per hr.

(Spending variance)

(Efficiency variance)

(Total variable overhead variance)

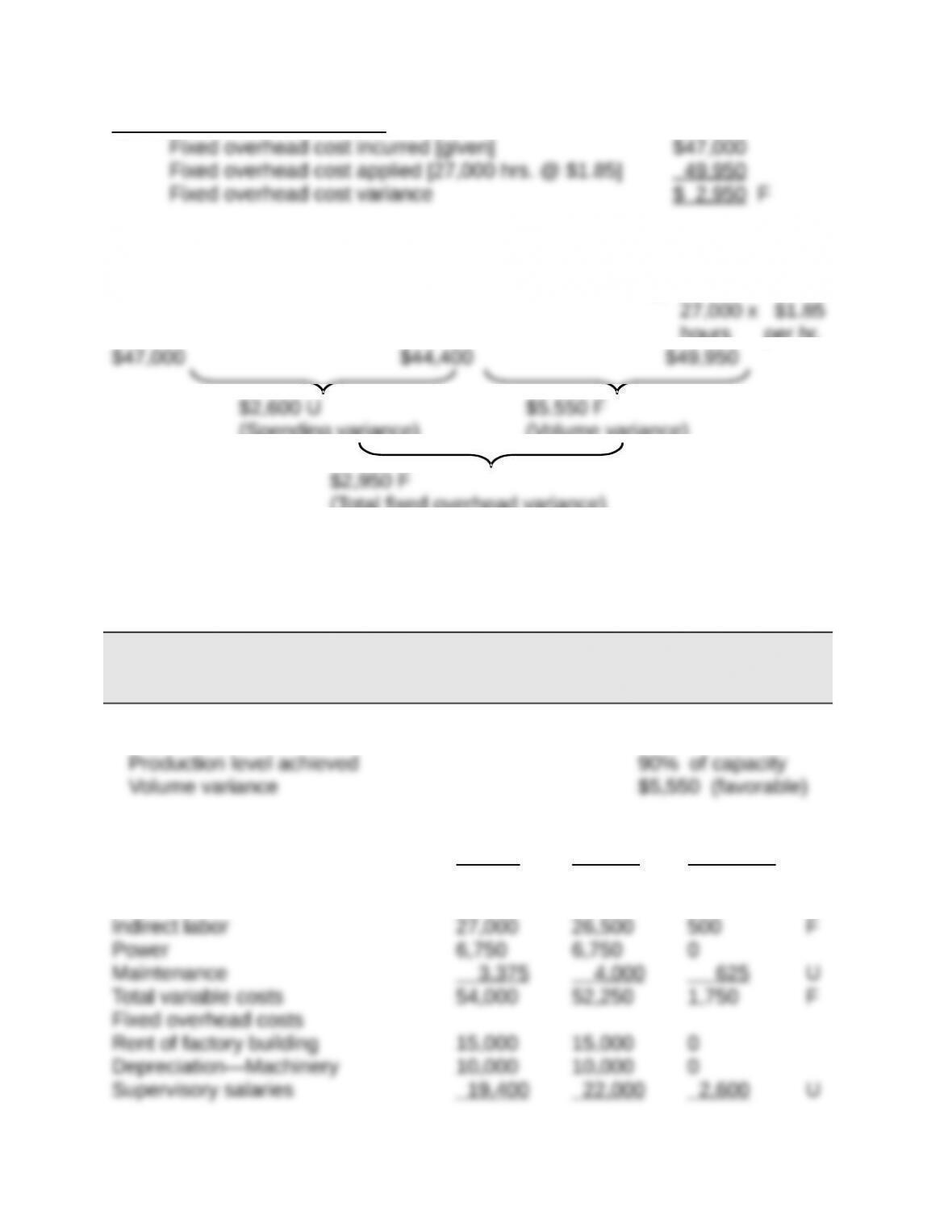

(b) Fixed overhead

Preliminary computations

Actual fixed overhead (given):

Rent of factory building $15,000

Fixed overhead cost variances

Fixed Overhead Spending and Volume Variances

Actual Overhead Budgeted Overhead Fixed Overhead

Applied

hours per hr.

(Spending variance)

(Volume variance)

(Total fixed overhead variance)

Part 4

KEGLER COMPANY

Overhead Variance Report

For Month Ended May 31

Volume Variance

Expected production level 80% of capacity

Flexible Actual

Controllable Variance Budget Results Variances*

Variable overhead costs

Indirect materials $16,875 $15,000 $1,875 F

* F = Favorable variance; and U = Unfavorable variance.

Title: Problem 23-7AA

QA_Ori:

Part 1

Dec. 31* Goods in Process Inventory 100,000

Direct Materials Quantity Variance 3,000

Dec. 31 Goods in Process Inventory 95,800

Direct Labor Rate Variance 1,200

Dec. 31 Goods in Process Inventory 354,000

* Alternatively, some companies compute and record the price

variance when materials are purchased. This would yield two

separate entries:

(1) Purchase of materials

Raw Materials Inventory 103,00

0

0

(2) Issuance of materials into production

0

Part 2

Under management by exception, the manager would first identify the largest

variances, attempt to uncover their causes, and then implement actions aimed at

correcting them. The smaller variances would be tackled after the major Title:

Problems were dealt with, if at all.

The largest variance amounts occur for the material quantity variance, the direct

labor efficiency variance, and the two overhead variances. The manager should

go to the production department to find out why the process used more materials

* The unfavorable volume variance indicates that the company produced