Archives

978-0132109178 Chapter 1 Solution Manual Part 1

1-1 CHAPTER 1 THE MANAGER AND MANAGEMENT ACCOUNTING See the front matter of this Solutions Manual for suggestions regarding your choices of assignment material for each chapter. 1-1 Management accounting measures, analyzes and reports financial and nonfinancial information that helps […]

978-0132109178 Chapter 1 Solution Manual Part 2

1-9 1-28 (30 min.) Pharmaceutical company, budgeting, ethics. 1. The overarching principles of the IMA Statement of Ethical Professional Practice are Honesty, Fairness, Objectivity and Responsibility. The statement’s corresponding “Standards for Ethical Conduct…” require management accountants to • Perform professional […]

978-0132109178 Chapter 10 Solution Manual

10-1 CHAPTER 10 DETERMINING HOW COSTS BEHAVE 1. Variations in the level of a single activity (the cost driver) explain the variations in the related total costs. 2. Cost behavior is approximated by a linear cost function within the relevant […]

978-0132109178 Chapter 10 Solution Manual Part 2

10-11 1. Slope coefficient (b) = Difference in cost Difference in labor-hours = $533,000 $400,000 6,500 3,000 − − = $38.00 Constant (a) = $533,000 – ($38.00 × 6,500) = $286,000 Cost function = $286,000 + ($38.00 professional labor-hours) […]

978-0132109178 Chapter 10 Solution Manual Part 3

10-21 Economic plausibility. The cost function shows a positive economically plausible relationship between machine-hours and maintenance costs. There is a clear-cut engineering relationship of 3. Using the cost function estimated in 1, predicted maintenance costs would be $2 × 100,000 […]

978-0132109178 Chapter 10 Solution Manual Part 4

10-37 (20–30 min.) Cost estimation, incremental unit-time learning model. 1. Cost to produce the 2nd through the 7th boats: Direct materials, 6 $200,000 $1,200,000 Direct manufacturing labor (DML), 72,6711 $40 2,906,840 Variable manufacturing overhead, 72,671 $25 1,816,775 […]

978-0132109178 Chapter 10 Solution Manual Part 5

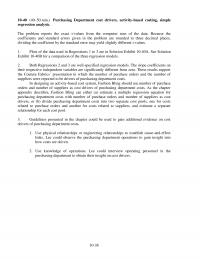

10-38 10-40 (40–50 min.) Purchasing Department cost drivers, activity-based costing, simple regression analysis. 1. Plots of the data used in Regressions 1 to 3 are in Solution Exhibit 10-40A. See Solution Exhibit 10-40B for a comparison of the three regression […]

978-0132109178 Chapter 11 Solution Manual

11-1 CHAPTER 11 DECISION MAKING AND RELEVANT INFORMATION 1. Identify the problem and uncertainties 2. Obtain information 3. Make predictions about the future 4. Make decisions by choosing among alternatives 5. Implement the decision, evaluate performance, and learn 11-2 Relevant […]

978-0132109178 Chapter 11 Solution Manual Part 2

11-11 11-23 (10 min.) Selection of most profitable product. Only Model 14 should be produced. The key to this problem is the relationship of manufacturing overhead to each product. Note that it takes twice as long to produce Model 9; […]

978-0132109178 Chapter 11 Solution Manual Part 3

11-32 (20 min.) Opportunity costs. (Please alert students that in some printed versions of the book there is a typographical error in the first line of requirement 2. “Wolverine” should be replaced by “Wild Boar.”) 1. The opportunity cost to […]

978-0132109178 Chapter 11 Solution Manual Part 4

7. (e) None of these. The correct answer is $3.55. This part always gives students trouble. The short-cut solution below is followed by a longer solution that is helpful to students. Short-cut solution: The highest price to be paid would […]

978-0132109178 Chapter 12 Solution Manual

12-1 CHAPTER 12 PRICING DECISIONS AND COST MANAGEMENT 1. Customers 2. Competitors 3. Costs 12-2 Not necessarily. For a one-time–only special order, the relevant costs are only those costs that will change as a result of accepting the order. In […]

978-0132109178 Chapter 12 Solution Manual Part 2

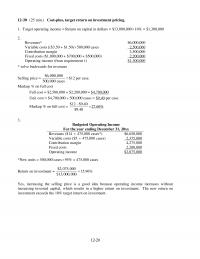

12-11 1. Target operating income = target return on investment invested capital Target operating income (25% of $900,000) $225,000 Total fixed costs 375,000 Target contribution margin $600,000 Target contribution per room-night, ($600,000 ÷ 15,000) $40 Add variable costs per […]

978-0132109178 Chapter 12 Solution Manual Part 3

12-20 12-30 (25 min.) Cost-plus, target return on investment pricing. 2. Revenues* $6,000,000 Variable costs [($3.50 + $1.50) 500,000 cases 2,500,000 Contribution margin 3,500,000 Fixed costs ($1,000,000 + $700,000 + $500,000) 2,200,000 Operating income (from requirement 1) $1,300,000 * […]

978-0132109178 Chapter 13 Solution Manual

13-1 CHAPTER 13 13-1 Strategy specifies how an organization matches its own capabilities with the opportunities in the marketplace to accomplish its objectives. 13-2 The five key forces to consider in industry analysis are: (a) competitors, (b) potential entrants into […]

978-0132109178 Chapter 13 Solution Manual Part 2

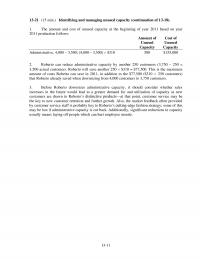

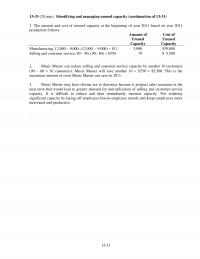

13-11 1. The amount and cost of unused capacity at the beginning of year 2011 based on year 2011 production follows: Amount of Cost of Unused Unused Capacity Capacity Administrative, 4,000 − 3,500; (4,000 – 3,500) $310 500 $155,000 […]

978-0132109178 Chapter 13 Solution Manual Part 3

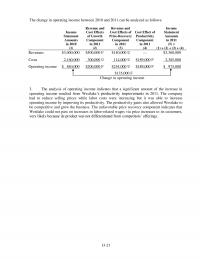

The change in operating income between 2010 and 2011 can be analyzed as follows: Income Statement Amounts in 2010 (1) Revenue and Cost Effects of Growth Component in 2011 (2) Revenue and Cost Effects of Price-Recovery Component in 2011 (3) […]

978-0132109178 Chapter 13 Solution Manual Part 4

13-33 (20 min.) Identifying and managing unused capacity (continuation of 13-31) 1. The amount and cost of unused capacity at the beginning of year 2011 based on year 2011 13-31 production follows: Amount of Cost of Unused Unused Capacity Capacity […]

978-0132109178 Chapter 14 Solution Manual

14-1 CHAPTER 14 14-1 Disagree. Cost accounting data plays a key role in many management planning and control decisions. The division president will be able to make better operating and strategy decisions by being involved in key decisions about cost […]

978-0132109178 Chapter 14 Solution Manual Part 2

14-11 2. Customer Distribution Channels (all amounts in $000s) Wholesale Customers Retail Customers Total Total North America South America Total Big Sam World (all customers) Wholesale Wholesaler Wholesaler Retail Stereo Market (1) = (2) + (5) (2) = (3) + […]

978-0132109178 Chapter 14 Solution Manual Part 3

14-21 14-25 (60 min.) Variance analysis, multiple products. 1. Budget for 2011 Orlem 7.50 5.50 2.00 1,200,000 50 2,400,000 Total 2,400,000 100% $5,424,000 Actual for 2011 Variable Contrib. Selling Cost Margin Units Sales Contribution Price per Unit per Unit Sold […]

978-0132109178 Chapter 14 Solution Manual Part 4

14-31 3. Dropping customers should be the last resort taken by Spring Distribution. Factors to consider include the following: a. What is the expected future profitability of each customer? Are the currently month? unprofitable (T) or low-profit (P) customers likely […]

978-0132109178 Chapter 14 Solution Manual Part 5

A summary of the variances is: Sales-Volume Variance Mint chocolate chip $24,360 F Vanilla 43,500 U 14-41 Rum Raisin 15,200 F Peach 2,520 U Coffee 43,860 F All flavors $37,400 F Sales-Mix Variance Mint chocolate chip $13,860 F Vanilla 63,800 […]

978-0132109178 Chapter 14 Solution Manual Part 6

The total direct labor mix variance can also be computed as the sum of the direct labor mix variances for each input: Direct labor mix variance for each input = Actual direct labor input mix percentage […]

978-0132109178 Chapter 15 Solution Manual

15-1 CHAPTER 15 15-1 The single-rate (cost-allocation) method makes no distinction between fixed costs and variable costs in the cost pool. It allocates costs in each cost pool to cost objects using the same rate per unit of the single […]

978-0132109178 Chapter 15 Solution Manual Part 2

15-11 SOLUTION EXHIBIT 15-22 Reciprocal Method of Allocating Support Department Costs for September 2012 at E-books Using Repeated Iterations Support Departments Operating Departments Human Resources Information Systems Corporate Sales Consumer Sales Total Budgeted manufacturing overhead costs before any interdepartmental cost […]

978-0132109178 Chapter 15 Solution Manual Part 3

15-28 (20 min.) Revenue allocation 1. a. Stand-alone method for the BegM + RCC package DVD Separate Revenue Percentage Joint Revenue Allocation BegM $ 50 $50 ÷ $80=0.625 $60 $37.50 RCC 30 $30 ÷ $80=0.375 60 22.50 $ 80 $60.00 […]

978-0132109178 Chapter 15 Solution Manual Part 4

15-31 3. To use the Shapley value method, consider each party as first the primary party and then the incremental party. Compute the average of the two to determine the allocation. Wright Inc.: Allocation as the primary party $40,000 4. […]

978-0132109178 Chapter 16 Solution Manual

16-1 16-1 Exhibit 16-1 presents many examples of joint products from four different general industries. These include: Industry Separable Products at the Splitoff Point Food Processing: • Lamb • Lamb cuts, tripe, hides, bones, fat • Turkey • Breasts, wings, […]

978-0132109178 Chapter 16 Solution Manual Part 2

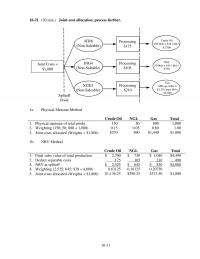

16-11 16-21 (30 min.) Joint-cost allocation, process further. Joint Costs = $1800 ICR8 (Non-Saleable) ING4 (Non-Saleable) XGE3 (Non-Saleable) Processing $175 Processing $210 Processing $105 Crude Oil 150 bbls × $18 / bbl = $2700 NGL 50 bbls × $15 / […]

978-0132109178 Chapter 16 Solution Manual Part 3

Computation of gross-margin percentages: a. Sales value at splitoff method: Super A Super B C Super D Total Revenues $300,000 $160,000 $24,000 $160,000 $644,000 Joint costs 33,600 28,800 9,600 24,000 96,000 Separable costs 249,600 102,400 0 152,000 504,000 Total cost […]

978-0132109178 Chapter 16 Solution Manual Part 4

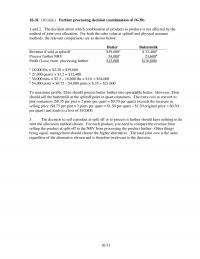

16-31 16-31 (10 min.) Further processing decision (continuation of 16-30). 1.and 2. The decision about which combination of products to produce is not affected by the method of joint cost allocation. For both the sales value at splitoff and physical […]

978-0132109178 Chapter 16 Solution Manual Part 5

16-38 Step 2 Standard Deluxe Module Module Total Final sales value of total production $14,000 $26,500 $40,500 Deduct gross margin using overall gross margin percentage (20.0%) 2,800 5,300 8,100 bits produced for each type of module follows: Standard Deluxe Module/ […]

978-0132109178 Chapter 17 Solution Manual

17-1 CHAPTER 17 PROCESS COSTING 17-1 Industries using process costing in their manufacturing area include chemical processing, 17-2 Process costing systems separate costs into cost categories according to the timing of when costs are introduced into the process. Often, only […]

978-0132109178 Chapter 17 Solution Manual Part 2

17-11 17-24 (25 min.) Weighted-average method, assigning costs. 1. & 2. Solution Exhibit 17-24A shows equivalent units of work done to date for Bio Doc Corporation for direct materials and conversion costs. Solution Exhibit 17-24B summarizes total costs to account […]

978-0132109178 Chapter 17 Solution Manual Part 3

17-21 17-30 (25 min.) Weighted-average method. 1. Since direct materials are added at the beginning of the assembly process, the units in this department must be 100% complete with respect to direct materials. Solution Exhibit 17-30A 2. & 3. Solution […]

978-0132109178 Chapter 17 Solution Manual Part 4

17-31 SOLUTION EXHIBIT 17-34B Steps 3, 4, and 5: Summarize Total Costs to Account For, Compute Cost per Equivalent Unit, and Assign Total Costs to Units Completed and to Units in Ending Work in Process; FIFO Method of Process Costing, […]

978-0132109178 Chapter 17 Solution Manual Part 5

17-40 The FIFO ending inventory is higher than the weighted-average ending inventory by $3,750. This is because FIFO assumes that all the lower-cost prior-period units in work in process (resulting from the lower transferred-in costs in beginning inventory) are the […]

978-0132109178 Chapter 18 Solution Manual

18-1 18-1 Managers have found that improved quality and intolerance for high spoilage have lowered overall costs and increased sales. 18-2 Spoilage—units of production that do not meet the standards required by customers for good units and that are discarded […]

978-0132109178 Chapter 18 Solution Manual Part 2

18-11 SOLUTION EXHIBIT 18-24 PANEL B: Steps 3, 4, and 5— Summarize Total Costs to Account For, Compute Cost per Equivalent Unit, and Assign Total Costs to Units Completed, to Spoiled Units, and to Units in Ending Work in Process […]

978-0132109178 Chapter 18 Solution Manual Part 3

18-21 SOLUTION EXHIBIT 18-31 PANEL B: Steps 3, 4, and 5— Summarize Total Costs to Account For, Compute Cost per Equivalent Unit, and Assign Total Costs to Units Completed, to Spoiled Units, and to Units in Ending Work in Process […]

978-0132109178 Chapter 18 Solution Manual Part 4

18-29 18-39 (30−35 min.) Weighted-average method, inspection at 80% completion (chapter appendix). The computation and allocation of spoilage is the most difficult part of this problem. The units in the ending inventory have passed inspection. Therefore, of the 100,000 units […]

978-0132109178 Chapter 19 Solution Manual

19-1 CHAPTER 19 19-1 Quality costs (including the opportunity cost of lost sales because of poor quality) can be as much as 10% to 20% of sales revenues of many organizations. Quality-improvement programs can result in substantial cost savings and […]

978-0132109178 Chapter 19 Solution Manual Part 2

19-11 3. Using information from requirement 2, Revenues $26,250,000 Fixed costs $7,500,000 Denote total variable costs by $x $26,250,000 – $x – $7,500,000 = $3,500,000 $x = $26,250,000 – $7,500,000 – $3,500,000 = $15,250,000 Total variable costs = $15,250,000 Variable […]

978-0132109178 Chapter 19 Solution Manual Part 3

19-21 19-29 (30–40 min.) Statistical quality control. 1. The + 2 rule will trigger a decision to investigate when mean weight per production run is outside the control limit: Double Bran Bits: Mean + 2 = 17.97 + (2 […]

978-0132109178 Chapter 19 Solution Manual Part 4

19-31 3. Delays occur in the processing of B7 and A3 because of (a) uncertainty about how many orders Brandt will actually receive (Brandt expects to receive 125 orders of B7 and 10 orders of A3), and (b) uncertainty about […]

978-0132109178 Chapter 19 Solution Manual Part 5

19-37 3. Solution Exhibit 19-37B presents a cause-and-effect or fishbone diagram for the problem of “late deliveries.” SOLUTION EXHIBIT 19-37B Cause-and-Effect Diagram for incidents of “late delivery” to customer at Pauli’s Pizza: Methods and Machine related Factors Materials Factors Human […]

978-0132109178 Chapter 2 Solution Manual Part 1

2-1 2-1 A cost object is anything for which a separate measurement of costs is desired. Examples include a product, a service, a project, a customer, a brand category, an activity, and a department. 2-2 Direct costs of a cost […]

978-0132109178 Chapter 2 Solution Manual Part 2

2-26 (20 min.) Total costs and unit costs 1. Number of attendees 0 100 200 300 400 500 600 Variable cost per person ($9 caterer charge – $5 student door fee) $4 $4 $4 $4 $4 $4 $4 Fixed Costs […]

978-0132109178 Chapter 2 Solution Manual Part 3

2-21 2-35 (15–20 min.) Interpretation of statements (continuation of 2-32). 1. The schedule in 2-34 can become a Schedule of Cost of Goods Manufactured and Sold simply by including the beginning and ending finished goods inventory figures in the supporting […]

978-0132109178 Chapter 20 Solution Manual

20-1 CHAPTER 20 20-1 Cost of goods sold (in retail organizations) or direct materials costs (in organizations with a manufacturing function) as a percentage of sales frequently exceeds net income as a percentage of sales by many orders of magnitude. […]

978-0132109178 Chapter 20 Solution Manual Part 2

20-11 1. (a). Record purchases of direct materials Inventory Control Accounts Payable Control 2,754,000 2,754,000 (b) Record conversion costs incurred Conversion Costs Control Various Accounts (such as 723,600 Wages Payable Control) 723,600 (c) Record cost of good finished units completed […]

978-0132109178 Chapter 20 Solution Manual Part 3

20-18 SOLUTION EXHIBIT 20-30 Annual Relevant Costs of Current Purchasing Policy and JIT Purchasing Policy for Margro Corporation Relevant Costs under Current Purchasing Policy Relevant Costs under JIT Purchasing Policy Required return on investment 20% per year $600,000 of […]

978-0132109178 Chapter 21 Solution Manual

21-1 21-1 No. Capital budgeting focuses on an individual investment project throughout its life, recognizing the time value of money. The life of a project is often longer than a year. Accrual accounting focuses on a particular accounting period, often […]

978-0132109178 Chapter 21 Solution Manual Part 2

21-11 21-21 (30 min.) Comparison of projects, no income taxes. 1. Total Present Value Year Present Discount Value Factors at 10% 0 1 2 3 Plan I $ (100,000) 1.000 $ (100,000) 2. Plan III has the lowest net present […]

978-0132109178 Chapter 21 Solution Manual Part 3

SOLUTION EXHIBIT 21-25 Total Present Value Present Value Discount Factors At 10% Sketch of Relevant After-Tax Cash Flows 0 1 2 3 4 5 1a. Initial motor investment $(75,000) 1.000 $(75,000) 1b. Initial working capital investment 0 1.000 $0 2a. […]

978-0132109178 Chapter 21 Solution Manual Part 4

21-31 1. Net Present Value of project: Period 0 1 – 10 Cash inflows $28,000 Cash outflows $(62,000) (18,000) Net cash flows $(62,000) $ 10,000 Annual net cash inflows $ 10,000 Present value factor for annuity, 10 periods, 8% × […]

978-0132109178 Chapter 21 Solution Manual Part 5

21-41 21-35 (40-45 min.) Recognizing cash flows for capital investment projects, NPV. 1. Net initial investment Initial equipment investment $(2,575,000) Initial working-capital investment (25,000) Net initial investment $(2,600,000) Cash flow from operations Annual after-tax cash flow from operations (excl. deprn. […]

978-0132109178 Chapter 22 Solution Manual

22-1 CHAPTER 22 22-1 A management control system is a means of gathering and using information to aid and coordinate the planning and control decisions throughout an organization and to guide the behavior of its managers and employees. The goal […]

978-0132109178 Chapter 22 Solution Manual Part 2

22-11 2. Bonus paid to division managers at 1% of division operating income will be as follows: Method A Internal Transfers at Market Prices Method B Internal Transfers at 110% of Full Costs Mining Division manager’s bonus (1% $6,000,000; […]

978-0132109178 Chapter 22 Solution Manual Part 3

22-21 2. If (a) A has excess capacity, (b) there is intermediate external demand for only 800 units at $200, and (c) the $200 price is to be maintained, then the opportunity costs per unit to the supplying division are […]

978-0132109178 Chapter 22 Solution Manual Part 4

22-32 (40 min.) Multinational transfer pricing, global tax minimization. This is a two-country two-division transfer-pricing problem with two alternative transfer-pricing methods. Summary data in U.S. dollars are: South Africa Mining Division Variable costs: 600 ZAR ÷ 6 = $100 per […]

978-0132109178 Chapter 23 Solution Manual

23-1 CHAPTER 23 23-1 Examples of financial and nonfinancial measures of performance are: Financial: ROI, residual income, economic value added, and return on sales. Nonfinancial: Customer perspective: Market share, customer satisfaction. Internal-business-processes perspective: Manufacturing lead time, yield, on-time performance, number […]

978-0132109178 Chapter 23 Solution Manual Part 2

23-11 1. Bleefl would be better off if the machine is replaced. Its cost of capital is 6% and the IRR of the investment is 11%, indicating that this is a positive net present value project. 2. The ROIs for […]

978-0132109178 Chapter 23 Solution Manual Part 3

23-21 23-29 (40–50 min.) ROI, measurement alternatives for performance measures 1. ROI = Operating income ÷ Net book value of total assets Denver ROI = $723,000 ÷ ($4,500,000 – $3,300,000 + 999,800) = $723,000 ÷ $2,199,800 = 60.25% Seattle ROI […]

978-0132109178 Chapter 23 Solution Manual Part 4

23-28 effects of these factors provides better information about a manager’s performance. What is critical, however, for benchmarking and relative performance evaluation to be effective is that similar noncontrollable factors affect each division. It is not clear that the same […]

978-0132109178 Chapter 3 Solution Manual Part 1

3-1 CHAPTER 3 COST-VOLUME-PROFIT ANALYSIS 3-1 Cost-volume-profit (CVP) analysis examines the behavior of total revenues, total costs, and operating income as changes occur in the units sold, selling price, variable cost per unit, or fixed costs of a product. 3-2 […]

978-0132109178 Chapter 3 Solution Manual Part 2

3-11 1. Breakeven point revenues = percentagemargin on Contributi costs Fixed Contribution margin percentage = = 0.60 or 60% $660,000 $1,100,000 2. Contribution margin percentage = price Selling unit per cost Variable price Selling − 0.60 = SP $16 SP […]

978-0132109178 Chapter 3 Solution Manual Part 3

3-21 Breakeven point in units = Net fixed costs Contribution margin per concert = $1,000 $74,000 = 74 concerts Check Donations $ 40,000 Revenue ($2,500 × 74) 185,000 Total revenue 225,000 Less variable costs Guest performers ($1,000 × 74) $74,000 […]

978-0132109178 Chapter 3 Solution Manual Part 4

3-31 Sales revenue 5,000 1.20 $60 $360,000 Variable costs 5,000 1.20 $25 × (1 – 0.20) 120,000 Operating income $ 95,000 The point of this problem is that managers always need to consider broader rather than […]

978-0132109178 Chapter 3 Solution Manual Part 5

3-41 0.40R = $11,700,000 R = $11,700,000 0.40 = $29,250,000 3-44 (15–25 min.) Sales mix, three products. 1. Sales of A, B, and C are in ratio 20,000 : 100,000 : 80,000. So for every 1 unit of A, […]

978-0132109178 Chapter 4 Solution Manual Part 1

4-1 CHAPTER 4 JOB COSTING 4-1 Cost pool––a grouping of individual indirect cost items. Cost tracing––the assigning of direct costs to the chosen cost object. 4-2 In a job-costing system, costs are assigned to a distinct unit, batch, or lot […]

978-0132109178 Chapter 4 Solution Manual Part 2

4-11 1. Quarter 1 2 3 4 Annual (1) Pools sold 700 500 150 150 1,500 (2) Direct manufacturing labor hours (0.5 Row 1) 350 250 75 75 750 (3) Fixed manufacturing overhead costs $10,500 $10,500 $10,500 $10,500 $42,000 […]

978-0132109178 Chapter 4 Solution Manual Part 3

4-21 The posting of entries to T-accounts is as follows: Materials Control Work-in–Process Control Bal 12 (2) 145 Bal. 2 (2) 145 (4) 90 (8) 63 (9) 294 (1) 150 (3) 10 Bal. 7 Bal. 6 Finished Goods Control Cost […]

978-0132109178 Chapter 4 Solution Manual Part 4

4-33 (25–30 min.) Service industry, job costing, two direct– and indirect-cost categories, law firm (continuation of 4-32). Although not required, the following overview diagram is helpful to understand Keating’s job– costing system. Professional Labor-Hours General Support COST OBJECT: JOB FOR […]

978-0132109178 Chapter 4 Solution Manual Part 5

4-39 1. Adjusting entry for 12/31 payroll. (a) Work-in–Process Control 3,850 Manufacturing Department Overhead Control 950 Wages Payable Control 4,800 To recognize payroll costs (b) Work-in–Process Control 4,620 Manufacturing Overhead Allocated 4,620 To allocate manufacturing overhead at 120% $3,850 […]

978-0132109178 Chapter 5 Solution Manual Part 1

5-1 CHAPTER 5 ACTIVITY-BASED COSTING AND ACTIVITY-BASED MANAGEMENT 5-1 Broad averaging (or “peanut-butter costing”) describes a costing approach that uses broad averages for assigning (or spreading, as in spreading peanut butter) the cost of resources 5-2 Overcosting may result in […]

978-0132109178 Chapter 5 Solution Manual Part 2

5-11 1. Trophies Plaques Total Direct materials Forming $13,000 $11,250 Assembly 2,600 9,375 Total 15,600 20,625 Direct Labor Forming 15,600 9,000 Assembly 7,800 10,500 Total 23,400 19,500 Total direct costs $39,000 $40,125 $79,125 Budgeted overhead rate = ($12,000 $10,386 $23,000 […]

978-0132109178 Chapter 5 Solution Manual Part 3

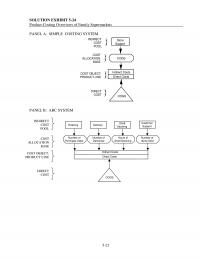

SOLUTION EXHIBIT 5-24 Product-Costing Overviews of Family Supermarkets PANEL A: SIMPLE COSTING SYSTEM COST OBJECT: PRODUCT LINE Indirect Costs Direct Costs Store Support COGS COGS INDIRECT COST POOL COST ALLOCATION BASE DIRECT COST PANEL B: ABC […]

978-0132109178 Chapter 5 Solution Manual Part 4

5-32 (50 min.) Plantwide, department, and activity-cost rates. 1. Plant-wide costing rate Fighters Cargo Total Direct materials Assembly $2.50 $3.75 $6.25 Painting 0.50 1.00 1.50 Total $3.00 $4.75 $7.75 Direct Labor Assembly $3.50 $2.00 $5.50 Painting 2.25 1.50 3.75 Total […]

978-0132109178 Chapter 5 Solution Manual Part 5

5-41 4. Backpacks Purses Total Direct materials $412,920 $379,290 $ 792,210 Direct manufacturing labor 120,000 98,000 218,000 Setup ($347 × 130; 60 batches) 45,110 20,820 65,930 Shipping ($389 × 130; 60 batches) 50,570 23,340 73,910 Design ($41,500 × 2; 2 […]

978-0132109178 Chapter 5 Solution Manual Part 6

5-47 The following table documents how the two job orders differ in the way they use each of the five activity areas included in indirect manufacturing costs: Usage Based on Analysis of Activity Area Cost Drivers Usage Assumed with Direct […]

978-0132109178 Chapter 6 Solution Manual Part 1

6-1 6-1 The budgeting cycle includes the following elements: a. Planning the performance of the company as a whole as well as planning the performance of its subunits. Management agrees on what is expected. b. Providing a frame of reference, […]

978-0132109178 Chapter 6 Solution Manual Part 2

6-11 6-26 (15 min.) Responsibility and controllability. 1. (a) Production manager (b) Purchasing Manager 2. (a) Production Manager (b) External Forces In the case of the utility rate hike the production manager would be responsible for the costs, but they […]

978-0132109178 Chapter 6 Solution Manual Part 3

6-21 4. Scarborough Corporation Direct Materials Purchases Budget (in dollars) for 2012 Budgeted Expected Purchases Purchase (Units) Price per unit Total Direct material A 469,000 $12 $5,628,000 Direct material B 256,000 5 1,280,000 Direct material C 42,000 3 126,000 Budgeted […]

978-0132109178 Chapter 6 Solution Manual Part 4

6-31 6-36 (30 min.) Cash budgeting, chapter appendix. 1. Projected Sales May June July August September October Sales in units 80 120 200 100 60 40 Revenues (Sales in units × $450) $36,000 $54,000 $90,000 $45,000 $27,000 Collections of Receivables […]

978-0132109178 Chapter 6 Solution Manual Part 5

6-40 11. Nonmanufacturing Costs Budget For the Year Ending December 31, 2011 Variable Fixed Total Marketing $14,100 $60,000 $74,100 Distribution 0 780 780 Total $14,100 $60,780 $74,880 12. Budgeted Income Statement For the Year Ending December 31, 2011 Revenue $352,000 […]

978-0132109178 Chapter 7 Solution Manual Part 1

7-1 CHAPTER 7 7-1 Management by exception is the practice of concentrating on areas not operating as expected and giving less attention to areas operating as expected. Variance analysis helps managers identify areas not operating as expected. The larger the […]

978-0132109178 Chapter 7 Solution Manual Part 2

7-11 2. May 2012 Actual Results Price Variance Actual Quantity Budgeted Price Efficiency Variance Flexible Budget (1) (2) = (1) – (3) (3) (4) = (3) – (5) (5) Units 550 550 Direct materials $11,828.36a $1,156.16 U $10,672.20b $772.20 […]

978-0132109178 Chapter 7 Solution Manual Part 3

7-21 1. This is a problem of two equations & two unknowns. The two equations relate to the number of cars detailed and the labor costs (the wages paid to the employees). X = number of cars detailed by the […]

978-0132109178 Chapter 7 Solution Manual Part 4

7-31 2. Direct Materials Price Variance (time of purchase = time of use) Direct Materials Control 10,640 Direct Materials Price Variance 304 Accounts Payable Control or Cash 10,336 Direct Materials Efficiency Variance Work in Process Control 9,870 Direct Materials Efficiency […]

978-0132109178 Chapter 7 Solution Manual Part 5

7-40 (30 min.) Comprehensive variance analysis. 1. Computing unit selling prices and unit costs of inputs: Actual selling price = $2,502,500 ÷ 275,000 = $9.10 Budgeting selling price = $2,700,000 ÷ 300,000 = $9.00 Selling-price variance = ( ) Actual […]

978-0132109178 Chapter 8 Solution Manual Part 1

8-1 CHAPTER 8 8-1 Effective planning of variable overhead costs involves: 1. Planning to undertake only those variable overhead activities that add value for customers using the product or service, and 2. Planning to use the drivers of costs in […]

978-0132109178 Chapter 8 Solution Manual Part 2

8-11 Fixed Manufacturing Costs and Variances a. Fixed Manufacturing Overhead Control 20,550 Salaries Payable, Acc. Depreciation, various other accounts 20,550 To record actual fixed manufacturing overhead costs incurred. b. Work–in–Process Control 20,736 Fixed Manufacturing Overhead Allocated 20,736 To record fixed […]

978-0132109178 Chapter 8 Solution Manual Part 3

8-25 (40−50 min.) Total overhead, 3-variance analysis. 1. This problem has two major purposes: (a) to give experience with data allocated on a total overhead basis instead of on separate variable and fixed bases and (b) to reinforce distinctions between […]

978-0132109178 Chapter 8 Solution Manual Part 4

8-31 Graph for planning and control purpose Graph for inventory costing purpose ($17 per machine-hour) Fixed Manufacturing Overhead Costs * Budgeted fixed manufacturing overhead rate per hour = Budgeted fixed manufacturing overhead Denominator level = $17,000,000/ 1,000,000 machine hours = […]

978-0132109178 Chapter 8 Solution Manual Part 5

8-41 7. Fixed Setup Overhead Variance Analysis for Jo Nathan Publishing Company for 2012 Actual Static Budget Standard Hours 8. Rejecting an order may have implications for future orders (i.e., professors would be reluctant to order books from this publisher […]

978-0132109178 Chapter 8 Solution Manual Part 6

8-48 SOLUTION EXHIBIT 8-39 Actual Costs Incurred: Actual Input Quantity Actual Input Quantity Budgeted Price Flexible Budget: Budgeted Input Quantity Allowed for Actual Output × Actual Rate Purchases Usage × Budgeted Price Direct Materials (25,000 $5.20) $130,000 (25,000 […]

978-0132109178 Chapter 9 Solution Manual Part 1

9-1 9-1 No. Differences in operating income between variable costing and absorption costing are due to accounting for fixed manufacturing costs. Under variable costing only variable manufacturing costs are included as inventoriable costs. Under absorption costing both variable and fixed […]

978-0132109178 Chapter 9 Solution Manual Part 2

9-11 1. Beginning Inventory + 2012 Production = 2012 Sales + Ending Inventory 85,000 units + 2012 Production = 345,400 units + 34,500 units 2012 Production = 294,900 units Income Statement for the Zwatch Company, Variable Costing for the Year […]

978-0132109178 Chapter 9 Solution Manual Part 3

9-21 1. a, b 2. a 3. d 4. c, d 5. c 6. d 7. a 8. b (or a) 9. b 10. c, d 11. a, b 9-26 (20 min.) Denominator-level problem. 1. Budgeted fixed manufacturing overhead costs […]

978-0132109178 Chapter 9 Solution Manual Part 4

9-30 (30–35 min.) Comparison of variable costing and absorption costing. 1. Since production volume variance is unfavorable, the budgeted fixed manufacturing overhead must be larger than the fixed manufacturing overhead allocated. Production-volume variance = Budgeted fixed manufacturing overhead – Fixed […]

978-0132109178 Chapter 9 Solution Manual Part 5

9-41 1. Fixed manufacturing overhead rate = $700,000/25,000 units = $28 per unit Manufacturing cost per unit: $24 direct materials + $36 direct mfg. labor + $12 var. mfg. OH + $28 fixed mfg. OH = $100 Selling price: $100 […]

978-0132109178 Chapter 9 Solution Manual Part 6

9-47 9-41 (60 min.) Absorption, variable, and throughput costing; performance evaluation NOTE: This problem can be broken up, with parts 1, 2, and 3 assigned to 3 or 6 different group members. The group members may reconvene to discuss parts […]

Cost Accounting 14th Edition Quiz Chapter 1

CHAPTER 1 QUIZ 1. Why do most companies adhere to GAAP for their basic internal financial statements? a. GAAP is required by law for publicly held companies. b. To use GAAP and another system of reporting would be too costly […]

Cost Accounting 14th Edition Quiz Chapter 10

CHAPTER 10 QUIZ 1. A mixed cost function has a constant component of $20,000. If the total cost is $60,000 and the independent variable has the value 200, what is the value of the slope coefficient? a. $200 b. $400 […]

Cost Accounting 14th Edition Quiz Chapter 11

CHAPTER 11 QUIZ 1. Which of the following should not be considered for every option in the decision process? a. Relevant revenues b. Relevant costs c. Historical costs d. Opportunity costs 2. What is always the question to ask to […]

Cost Accounting 14th Edition Quiz Chapter 12

CHAPTER 12 QUIZ 1. Major influences of competitors, costs, and customers on pricing decisions are factors of a. supply and demand. b. activity-based costing and activity-based management. c. key management themes that are important to managers attaining success in their […]

Cost Accounting 14th Edition Quiz Chapter 13

CHAPTER 13 QUIZ 1. Which of the following are two generic strategies described in the text that a company can use? a. Growth and product differentiation b. Price recovery and growth c. Product differentiation and cost leadership d. Cost leadership […]

Cost Accounting 14th Edition Quiz Chapter 14

CHAPTER 14 QUIZ 1. Which of the following is not a primary purpose given in the text for allocating costs? a. To provide information for economic decisions b. To motivate managers and other employees c. To measure income and assets […]

Cost Accounting 14th Edition Quiz Chapter 15

CHAPTER 15 QUIZ 1. The use of a dual-rate cost-allocation method recognizes a. the improvements in technology allowing for use of multiple cost pools. b. the need to use both budgeted and actual cost rates when allocating. c. the need […]

Cost Accounting 14th Edition Quiz Chapter 16

CHAPTER 16 QUIZ The following data apply to questions 1 through 5. Brant Corporation manufactures two products out of a joint process—Scout and Andro. The joint (common) costs incurred are $400,000 for a standard production run that generates 70,000 pounds […]

Cost Accounting 14th Edition Quiz Chapter 17

CHAPTER 17 QUIZ Use the following information for questions 1 through 10. Top That manufactures baseball-style hats. Material is introduced at the beginning of the process in the Cutting Department. Conversion costs are incurred (and allocated) uniformly throughout the process. […]

Cost Accounting 14th Edition Quiz Chapter 18

CHAPTER 18 QUIZ 1. [CPA Adapted] In manufacturing its products for the month of September 2008, El Dorado Corporation incurred normal spoilage of $7,000 and abnormal spoilage of $3,000. How much spoilage cost should El Dorado charge as inventoriable for […]

Cost Accounting 14th Edition Quiz Chapter 19

CHAPTER 19 QUIZ 1. The four cost categories in a cost of quality program are a. product design, process design, internal success, and external success. b. prevention, appraisal, internal failure, and external failure. c. design, conformance, control, and process. d. […]

Cost Accounting 14th Edition Quiz Chapter 2

CHAPTER 2 QUIZ 1. Galway Co. management desires cost information regarding its Celtic brand. The Celtic brand is a(n) a. cost object. b. cost driver. c. cost assignment. d. actual cost. 2. The cost of printer paper on a college […]

Cost Accounting 14th Edition Quiz Chapter 20

CHAPTER 20 QUIZ 1. Which of the following categories of costs are important when managing inventories of goods for sale according to the authors of the text? a. Purchasing, ordering, supply, spoilage, and opportunity b. Purchasing, stockout, carrying, ordering, and […]

Cost Accounting 14th Edition Quiz Chapter 21

CHAPTER 21 QUIZ 1. [CPA Adapted] If the algebraic sum of the present values of all cash flows related to a proposed capital expenditure discounted at the company’s required rate of return is positive, it indicates that the a. resultant […]

Cost Accounting 14th Edition Quiz Chapter 22

CHAPTER 22 QUIZ 1. If management decides to pursue an unwise goal, the management control system for that company should a. reinforce this company goal. b. be scrapped because an unwise goal will harm the company and should not be […]

Cost Accounting 14th Edition Quiz Chapter 23

CHAPTER 23 QUIZ 1. An example of a performance measure based on external financial information would be a. market share. b. stock prices. c. innovation measures. d. defect rates. 2. Which of the following does not describe the three steps […]

Cost Accounting 14th Edition Quiz Chapter 3

CHAPTER 3 QUIZ 1. Which of the following is not a factor in cost-volume-profit analysis? a. Units sold b. Selling price c. Total variable costs d. Fixed costs of a product 2. Which of the following is not an assumption […]

Cost Accounting 14th Edition Quiz Chapter 4

CHAPTER 4 QUIZ 1. A cost-allocation base may be any of the following except a a. cost driver. b. cost pool. c. way to link indirect costs to a cost object. d. nonfinancial quantity. 2. A company that manufactures dentures […]

Cost Accounting 14th Edition Quiz Chapter 5

CHAPTER 5 QUIZ 1. Production-cost cross-subsidization results from a. allocating indirect costs to multiple products. b. assigning traced costs to each product. c. assigning costs to different products using varied costing systems within the same organization. d. assigning broadly averaged […]

Cost Accounting 14th Edition Quiz Chapter 6

CHAPTER 6 QUIZ 1. Budgeting is the common accounting tool companies use for planning and controlling. Budgets a. provide a measure of planned financial results. b. are prepared independent of the company’s long term strategies. c. do not usually reflect […]

Cost Accounting 14th Edition Quiz Chapter 7

CHAPTER 7 QUIZ 1. [CMA Adapted] Flexible budgets a. accommodate changes in the inflation rate. b. accommodate changes in activity levels. c. are used to evaluate capacity utilization. d. are static budgets that have been revised for changes in price(s). […]

Cost Accounting 14th Edition Quiz Chapter 8

CHAPTER 8 QUIZ 1. Which of the following pertains primarily to the planning of fixed overhead costs? a. A standard rate per output unit is developed. b. Only essential activities are to be undertaken. c. Activities are to be undertaken […]

Cost Accounting 14th Edition Quiz Chapter 9

CHAPTER 9 QUIZ 1. The main difference between variable costing and absorption costing is a. the treatment of nonmanufacturing costs. b. the accounting for variable manufacturing costs. c. the accounting for fixed manufacturing costs. d. their value for decision makers. […]