17-21

17-30 (25 min.) Weighted-average method.

1. Since direct materials are added at the beginning of the assembly process, the units in this

department must be 100% complete with respect to direct materials. Solution Exhibit 17-30A

2. & 3. Solution Exhibit 17-30B summarizes the total Assembly Department costs for October

2012, calculates cost per equivalent unit of work done to date, and assigns these costs to units

completed (and transferred out) and to units in ending work in process using the weighted–

average method.

SOLUTION EXHIBIT 17-30A

SOLUTION EXHIBIT 17-30B

Steps 3, 4, and 5: Summarize Total Costs to Account For, Compute Cost per Equivalent Unit,

and Assign Total Costs to Units Completed and to Units in Ending Work in Process;

Weighted-Average Method of Process Costing, Assembly Department of Larsen Company,

for October 2012.

Total

Production

Costs

Direct

Materials

Conversion

Costs

(Step 3) Work in process, beginning (given)

$1,652,750

$1,250,000

$ 402,750

Costs added in current period (given)

6,837,500

4,500,000

2,337,500

Total costs to account for

$8,490,250

$5,750,000

$2,740,250

(Step 4) Costs incurred to date

$5,750,000

$2,740,250

Divide by equivalent units of work done to date

(Solution Exhibit 17-30A)

25,000

24,250

Cost per equivalent unit of work done to date

$ 230

$ 113

(Step 5) Assignment of costs:

Completed and transferred out (22,500 units)

$7,717,500

(22,500* $230) + (22,500* $113)

Work in process, ending (2,500 units)

772,750

(2,500† $230) + (1,750† $113)

Total costs accounted for

$8,490,250

$5,750,000 + $2,740,250

*Equivalent units completed and transferred out from Solution Exhibit 17-30A, Step 2.

†Equivalent units in work in process, ending from Solution Exhibit 17-30A, Step 2.

1. Work in Process––Assembly Department 4,500,000

2. Work in Process––Assembly Department 2,337,500

3. Work in Process––Testing Department 7,717,500

Work in Process––Assembly Department 7,717,500

1. The equivalent units of work done in the current period in the Assembly Department in

October 2012 for direct materials and conversion costs are shown in Solution Exhibit 17-32A.

2. The cost per equivalent unit of work done in the current period in the Assembly

3. Solution Exhibit 17-32B summarizes the total Assembly Department costs for October

2012, and assigns these costs to units completed (and transferred out) and units in ending work in

The FIFO ending inventory is lower than the weighted-average ending inventory by

$17,750. This is because FIFO assumes that all the higher-cost prior-period units in work in

process are the first to be completed and transferred out while ending work in process consists of

only the lower-cost current-period units. The weighted-average method, however, smoothes out

cost per equivalent unit by assuming that more of the lower-cost units are completed and

17-25

SOLUTION EXHIBIT 17-32B

Steps 3, 4, and 5: Summarize Total Costs to Account For, Compute Cost per Equivalent Unit, and Assign Total Costs to

Units Completed and to Units in Ending Work in Process;

FIFO Method of Process Costing, Assembly Department of Larsen Company for October 2012.

Total

Production

Costs

Direct

Materials

Conversion

Costs

(Step 3) Work in process, beginning (given)

$1,652,750

$1,250,000

$ 402,750

Costs added in current period (given)

6,837,500

4,500,000

2,337,500

Total costs to account for

$8,490,250

$5,750,000

$2,740,250

(Step 4) Costs added in current period

$4,500,000

$2,337,500

Divide by equivalent units of work done in

current period (Solution Exhibit 17-32A)

20,000

21,250

Cost per equivalent unit of work done in current period

$ 225

$ 110

(Step 5) Assignment of costs:

Completed and transferred out (22,500 units):

Work in process, beginning (5,000 units)

Costs added to beg. work in process in current period

$1,652,750

220,000

$1,250,000 + $ 402,750

(0* $225) + (2,000* $110)

Total from beginning inventory

Started and completed (17,500 units)

Total costs of units completed & transferred out

Work in process, ending (2,500 units)

Total costs accounted for

1,872,750

5,862,500

7,735,250

755,000

$8,490,250

(17,500† $225) + (17,500† $110)

(2,500# $225) + (1,750# $110)

$5,750,000 + $2,740,250

*Equivalent units used to complete beginning work in process from Solution Exhibit 17-32A, Step 2.

†Equivalent units started and completed from Solution Exhibit 17-32A, Step 2.

#Equivalent units in ending work in process from Solution Exhibit 17-32A, Step 2.

17-26

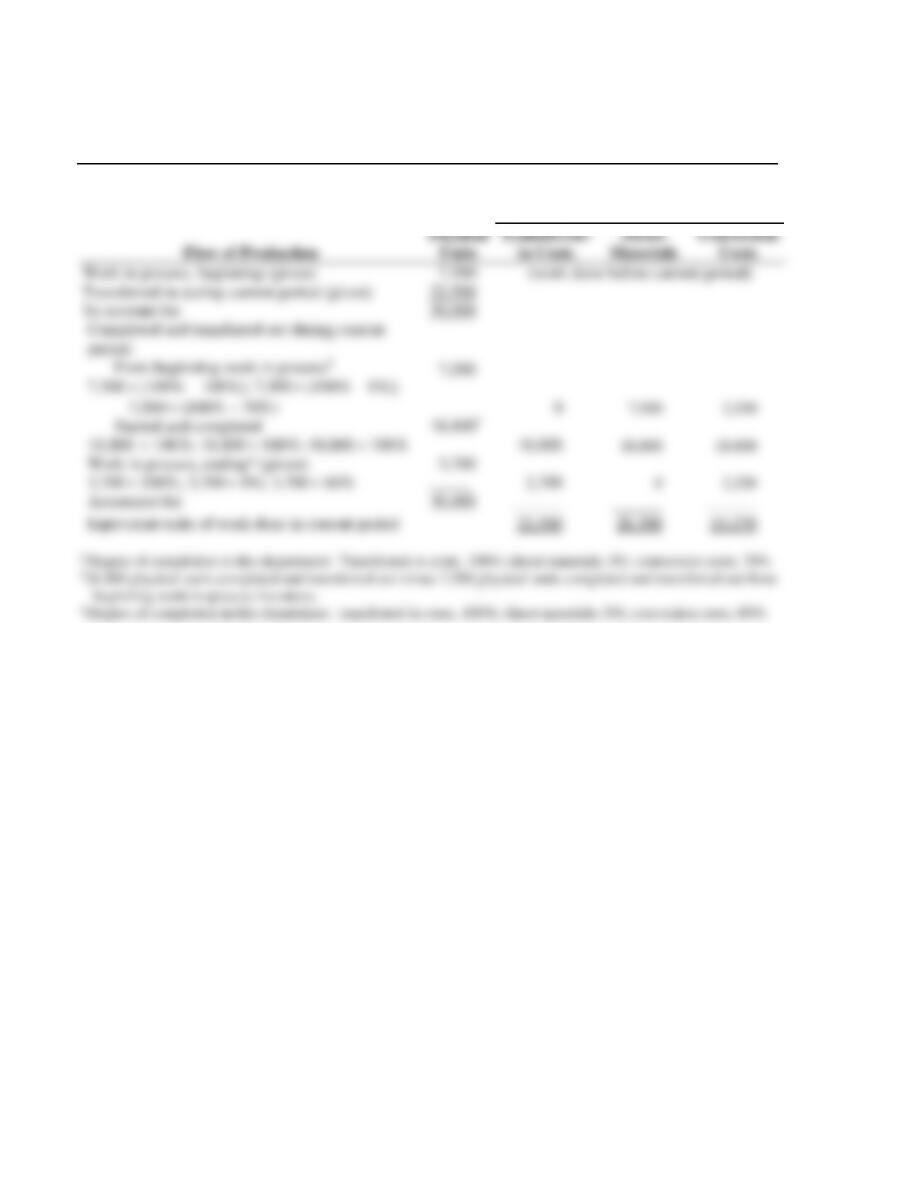

17-33 (30 min.) Transferred-in costs, weighted-average method (related to 17-30 to 17-32).

1. Transferred-in costs are 100% complete, and direct materials are 0% complete in both

beginning and ending work-in–process inventory. The reason is that transferred-in costs are

3. Solution Exhibit 17-33B summarizes total Testing Department costs for October 2012,

method.

4. Journal entries:

a. Work in Process––Testing Department 7,717,500

Work in Process––Assembly Department 7,717,500

17-27

SOLUTION EXHIBIT 17-33A

Steps 1 and 2: Summarize Output in Physical Units and Compute Output in Equivalent Units;

Weighted-Average Method of Process Costing,

Testing Department of Larsen Company for October 2012.

(Step 1)

(Step 2)

Equivalent Units

Flow of Production

Physical

Units

Transferred-in

Costs

Direct

Materials

Conversion

Costs

Work in process, beginning (given) 7,500

Transferred in during current period (given) 22,500

To account for 30,000

Completed and transferred out

during current period 26,300 26,300 26,300 26,300

Work in process, ending* (given) 3,700

3,700 100%; 3,700 0%; 3,700 60% 3,700 0 2,220

Accounted for 30,000

Equivalent units of work done to date 30,000 26,300 28,520

*Degree of completion in this department: transferred-in costs, 100%; direct materials, 0%; conversion costs, 60%.

17-28

SOLUTION EXHIBIT 17-33B

Steps 3, 4, and 5: Summarize Total Costs to Account For, Compute Cost per Equivalent Unit, and Assign Total Costs to Units Completed

and to Units in Ending Work in Process;

Weighted-Average Method of Process Costing,

Testing Department of Larsen Company for October 2012.

Total

Production

Costs

Transferred

-in Costs

Direct

Materials

Conversion

Costs

(Step 3) Work in process, beginning (given)

$ 3,767,960

$ 2,932,500

$ 0

$ 835,460

Costs added in current period (given)

21,378,100

7,717,500

9,704,700

3,955,900

Total costs to account for

$25,146,060

$10,650,000

$9,704,700

$4,791,360

(Step 4) Costs incurred to date

$10,650,000

$9,704,700

$4,791,360

Divide by equivalent units of work done to date

(Solution Exhibit 17-33A)

30,000

26,300

28,520

Equivalent unit costs of work done to date

$ 355

$ 369

$ 168

(Step 5) Assignment of costs:

Completed and transferred out (26,300 units)

$23,459,600

(26,300* $355) + (26,300* $369) + (26,300* $168)

Work in process, ending (3,700 units)

1,686,460

(3,700† $355) + (0† $369) + (2,220† $168)

Total costs accounted for

$25,146,060

$10,650,000 + $9,704,700 + $4,791,360

*Equivalent units completed and transferred out from Solution Exhibit 17-33A, Step 2.

†Equivalent units in ending work in process from Solution Exhibit 17-33A, Step 2.

17-29

1. As explained in Problem 17-33, requirement 1, transferred-in costs are 100% complete

and direct materials are 0% complete in both beginning and ending work-in-process inventory.

3. Solution Exhibit 17-34B summarizes total Testing Department costs for October 2012,

4. Journal entries:

a. Work in Process––Testing Department 7,735,250

Work in Process––Assembly Department 7,735,250

17-30

SOLUTION EXHIBIT 17-34A

Steps 1 and 2: Summarize Output in Physical Units and Compute Output in Equivalent Units;

FIFO Method of Process Costing,

Testing Department of Larsen Company for October 2012.

(Step 1)

(Step 2)

Equivalent Units

Flow of Production

Physical

Units

Transferred–

in Costs

Direct

Materials

Conversion

Costs

Work in process, beginning (given)

Transferred-in during current period (given)

To account for

7,500

22,500

30,000

(work done before current period)

Completed and transferred out during current

period:

From beginning work in process§

7,500

(100% − 100%); 7,500

(100% − 0%);

7,500

(100% − 70%)

7,500

0

7,500

2,250

Started and completed

18,800

100%; 18,800

100%; 18,800

100%

18,800†

18,800

18,800

18,800

Work in process, ending* (given)

3,700

100%; 3,700

0%; 3,700

60%

3,700

_____

3,700

0

2,220

Accounted for

30,000

Equivalent units of work done in current period

22,500

26,300

23,270

§ Degree of completion in this department: Transferred-in costs, 100%; direct materials, 0%; conversion costs, 70%.

†26,300 physical units completed and transferred out minus 7,500 physical units completed and transferred out from

beginning work-in-process inventory.

*Degree of completion in this department: transferred-in costs, 100%; direct materials, 0%; conversion costs, 60%.