5-11

1.

Trophies

Plaques

Total

Direct materials

Forming

$13,000

$11,250

Assembly

2,600

9,375

Total

15,600

20,625

Direct Labor

Forming

15,600

9,000

Assembly

7,800

10,500

Total

23,400

19,500

Total direct costs

$39,000

$40,125

$79,125

Budgeted

overhead rate

=

($12,000 $10,386 $23,000 $10,960) $56,346

$79,125 $79,125

+ + + =

=

$0.712114

per dollar of direct cost

Trophies

Plaques

Total

Direct materials

$15,600

$20,625

$ 36,225

Direct labor

23,400

19,500

42,900

Total direct cost

39,000

40,125

79,125

Allocated overhead*

27,772

28,574

56,346

Total costs

$66,772

$68,699

$135,471

*Allocated overhead = Total direct cost Budgeted overhead rate (0.712114).

2.

Budgeted

overhead rate

Forming Dept.

—

=

Budgeted Forming Department overhead costs

Budgeted Forming Department direct-labor costs

=

$12,000 $10,386

$15,600 $9,000

+

+

=

$22,386

$24,600 =

$0.91 per Forming Department direct-labor dollar

Budgeted

overhead rate

Assembly Dept.

—

=

Budgeted Assembly Department overhead costs

Budgeted Assembly Department direct costs

=

$23,000 $10,960

($2,600 $9,375 $7,800 $10,500)

+

+ + +

=

$33,960

$30,275 =

$1.121718 per Assembly Department direct cost dollar

5-12

Trophies

Plaques

Total

Direct materials

$15,600

$20,625

$ 36,225

Direct labor

23,400

19,500

42,900

Total direct cost

39,000

40,125

79,125

Allocated overhead

Forming Dept.a

14,196

8,190

22,386

Assembly Dept.b

11,666

22,294

33,960

Total costs

$64,862

$70,609

$135,471

3.

Trophies

Plaques

Total

a Forming Dept.

Direct labor costs

$15,600

$ 9,000

$24,600

Allocated overhead

(0.91 × $15,600; $9,000)

$14,196

$ 8,190

$22,386

b Assembly Dept.

Total direct costs

($2,600 + $7,800; $9,375 + $10,500)

$10,400

$19,875

$30,275

Allocated overhead

(1.121718 $10,400; $19,875)

$11,666

$22,294

$33,960

Forming Department

Budgeted setup rate

=

$12,000

156 batches

= $76.92308 per batch

$18,300

5-13

Trophies

Plaques

Total

Direct material costs

$15,600

$20,625

$36,225

Direct labor costs

23,400

19,500

42,900

Total direct costs

39,000

40,125

79,125

Forming Dept. overhead

Set up

$76.92308 40; 116

3,077

8,923

12,000

Supervision

0.422195

$15,600; $9,000

6,586

3,800

10,386

Assembly Department overhead

Set up

$157.5342

43; 103

6,774

16,226

23,000

Supervision

0.598907

$7,800; $10,500

4,671

6,289

10,960

Total costs

$60,108

$75,363

$135,471

4. Tarquin uses more refined cost pools the costs of trophies decreases and costs of

plaques increases. This is because plaques use a higher proportion of cost drivers (batches of

set ups and direct manufacturing labor costs) than trophies whereas the direct costs (the

allocation base used in the simple costing system) are slightly smaller for plaques compared

5-14

1. Rates per unit cost driver.

Activity Cost Driver Rate

Machining Machine-hours $375,000 ÷ (25,000 + 50,000)

= $5 per machine-hour

2.

Mathematical

Financial

Manufacturing cost per unit:

Direct materials

$150,000 ÷ 50,000

$3.00

$300,000 ÷ 100,000

$3.00

Direct manufacturing labor

$50,000 ÷ 50,000

1.00

$100,000 ÷ 100,000

1.00

Manufacturing overhead (from requirement 1)

5.10

3.45

Manufacturing cost per unit

$9.10

$7.45

1. Total indirect costs = $150,000 + $90,000 + $36,000 + $40,000 + $39,000 + $48,000

= $403,000

Total machine-hours = (400

10) + (200

10) = 6,000

5-16

3.

Cost per job

Standard

Job

Special

Job

Simple Costing System

$1,051.70

$1,121.70

Activity-based Costing System

$ 947.14

$1,330.72

Difference (Simple – ABC)

$ 104.56

$ (209.02)

system.

4. Quikprint can use the information revealed by the ABC system to change its pricing

based on the ABC costs. Under the simple system, Quikprint was making a gross margin of 12%

on each standard job (($1,200 – $1,051.70)

$1,200) and 25% on each special job (($1,500 –

5-23 (30 min.) Activity-based costing, manufacturing.

1. Simple costing system:

Total indirect costs = $95,000 + $45,000 + $25,000 + $60,000 + $8,000 + 3%[($125 3,200) +

($200 1,800)]

5-18

ABC System

Interior

Exterior

Direct materials

$ 96,000

$ 81,000

Direct manufacturing labor

76,800

64,800

Indirect costs allocated:

Product scheduling ($760 per run

40; 85)

30,400

64,600

Material handling ($187.50 per move

72; 168)

13,500

31,500

Machine setup ($125 per setup

45; 155)

5,625

19,375

Assembly ($6 per MH × 5,500; 4,500)

33,000

27,000

Inspection ($20 per inspection × 250; 150)

5,000

3,000

Marketing (0.03

$125

3,200; 0.03

$200

1,800)

12,000

10,800

Total costs

$272,325

$302,075

Total cost per unit

($272,325 ÷ 3,200 units; $302,075 ÷ 1,800 units)

$ 85.10

$ 167.82

3.

Cost per unit

Interior

Exterior

Simple Costing System

$97.97

$144.95

Activity-based Costing System

$85.10

$167.82

Difference (Simple – ABC)

$12.87

$(22.87)

Relative to the ABC system, the simple costing system overcosts interior doors and undercosts

exterior doors. Under the simple costing system, the doors require a similar number of total

machine hours (5,500 for interior and 4,500 for exterior), even though interior doors take fewer

machine hours per unit. Under the simple costing system, the volume of the production of

interior doors is driving the amount of overhead allocated to that product. The ABC study

reveals that each exterior door requires more production runs, material moves, and setups. This

is reflected in the higher indirect costs allocated to exterior doors in the ABC system.

4. Open Doors, Inc. can use the information revealed by the ABC system to change its

pricing based on the ABC costs. Under the simple system, Open Doors was making an operating

margin of 21.6% on each interior door (($125 – $97.97)

$125) and 27.5% on each exterior

door (($200 – $144.95)

$200). But, the ABC system reveals that it is actually making an

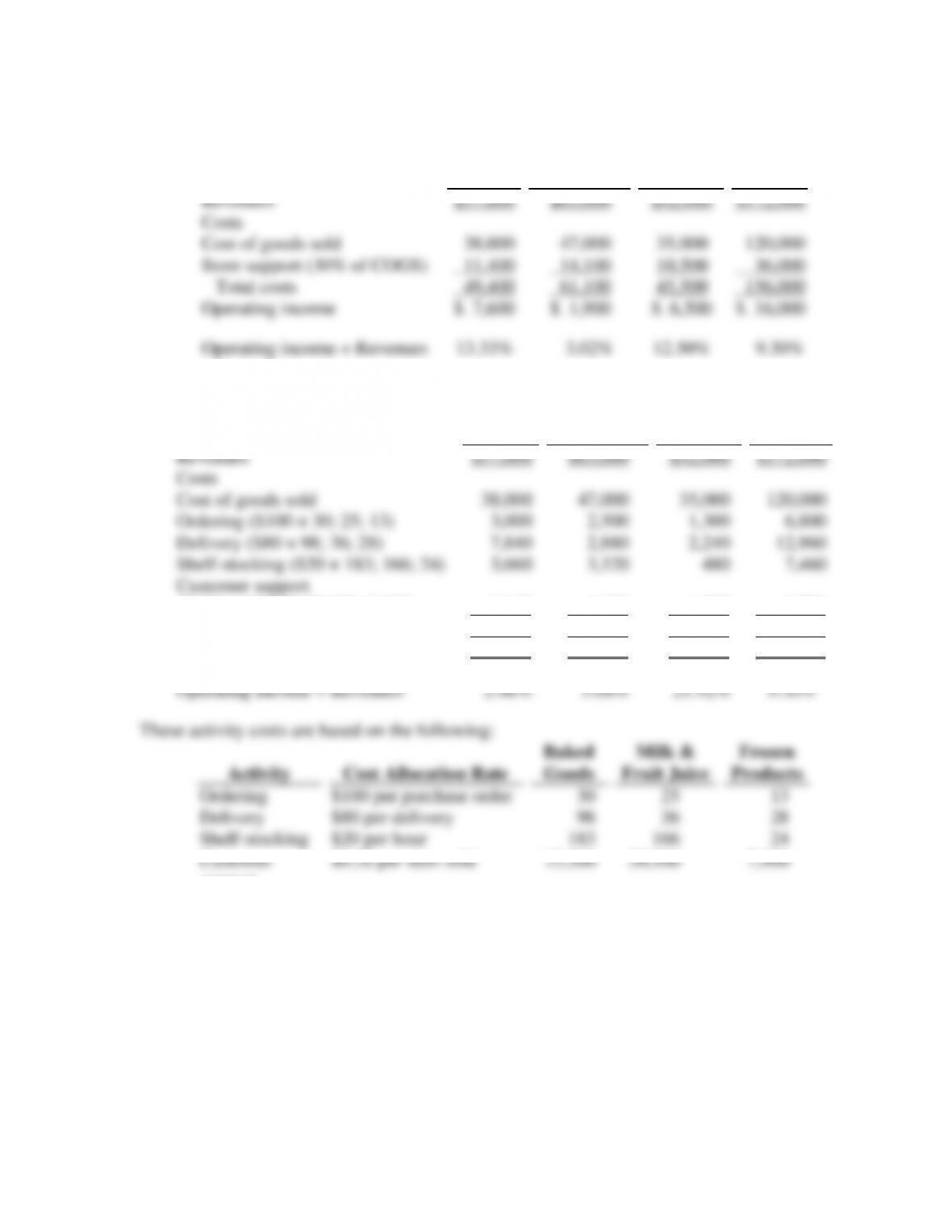

5-24 (30 min.) ABC, retail product-line profitability.

1. The simple costing system (Panel A of Solution Exhibit 5-24) reports the following:

Baked

Goods

Milk &

Fruit Juice

Frozen

Products

Total

Revenues

Costs

Cost of goods sold

Store support (30% of COGS)

Total costs

Operating income

Operating income ÷ Revenues

$57,000

38,000

11,400

49,400

$ 7,600

13.33%

$63,000

47,000

14,100

61,100

$ 1,900

3.02%

$52,000

35,000

10,500

45,500

$ 6,500

12.50%

$172,000

120,000

36,000

156,000

$ 16,000

9.30%

2. The ABC system (Panel B of Solution Exhibit 5-24) reports the following:

Baked

Goods

Milk &

Fruit Juice

Frozen

Products

Total

Revenues

Costs

Cost of goods sold

Ordering ($100 × 30; 25; 13)

Delivery ($80 × 98; 36; 28)

Shelf-stocking ($20 × 183; 166; 24)

Customer support

($0.20 × 15,500; 20,500; 7,900)

Total costs

Operating income

Operating income ÷ Revenues

$57,000

38,000

3,000

7,840

3,660

3,100

55,600

$ 1,400

2.46%

$63,000

47,000

2,500

2,880

3,320

4,100

59,800

$ 3,200

5.08%

$52,000

35,000

1,300

2,240

480

1,580

40,600

$11,400

21.92%

$172,000

120,000

6,800

12,960

7,460

8,780

156,000

$ 16,000

9.30%

These activity costs are based on the following:

Activity

Cost Allocation Rate

Baked

Goods

Milk &

Fruit Juice

Frozen

Products

Ordering

Delivery

Shelf-stocking

Customer

support

$100 per purchase order

$80 per delivery

$20 per hour

$0.20 per item sold

30

98

183

15,500

25

36

166

20,500

13

28

24

7,900