6-11

6-26 (15 min.) Responsibility and controllability.

1. (a) Production manager

(b) Purchasing Manager

2. (a) Production Manager

(b) External Forces

3. (a) Van 3 driver

(b) Service manager

4. (a) Anderson’s service manager

(b) Bigstore Warehouse manager

5. (a) Service manager

(b) This depends…

6-12

6. (a) Service manager

(b) External forces

6-13

1. The cash that Game Guys can expect to collect during May and June is calculated below.

Cash collected in May June

From service revenue

May ($1,400 x .97) $1,358.00

2. (a) Budgeted expenditures for May are as follows.

Costs

Inventory purchases

$4,350

Rent, utilities, etc.

1,400

Wages

1,000

TOTAL

$6,750

Yes, Game Guys will be able to cover its May costs since receipts are $6,965 and

expenditures are only $6,750.

(b)

Original

numbers

May

Revenues

decrease

10%

May

Revenues

decrease

5%

May Costs

increase

8%

Beginning cash

$100.00

$100.00

$100.00

$100.00

Collections

6,965.00

6,466.50a

6,715.75b

6,965.00

Cash Costs

6,750.00

6,750.00

6,750.00

7,290.00

Total

$315.00

$(183.50)

$ 65.75

$(225.00)

6-14

3. The cost of inventory purchases without the discount is $4,350, which Game Guys would

not have to pay until June if they buy the inventory on account in May. However, if they

take the discount and pay in May, the cost will be $4,350 x (100% – 2%) = $4,263. This

means they will save $87.

6-28 (40 min.) Budget schedules for a manufacturer.

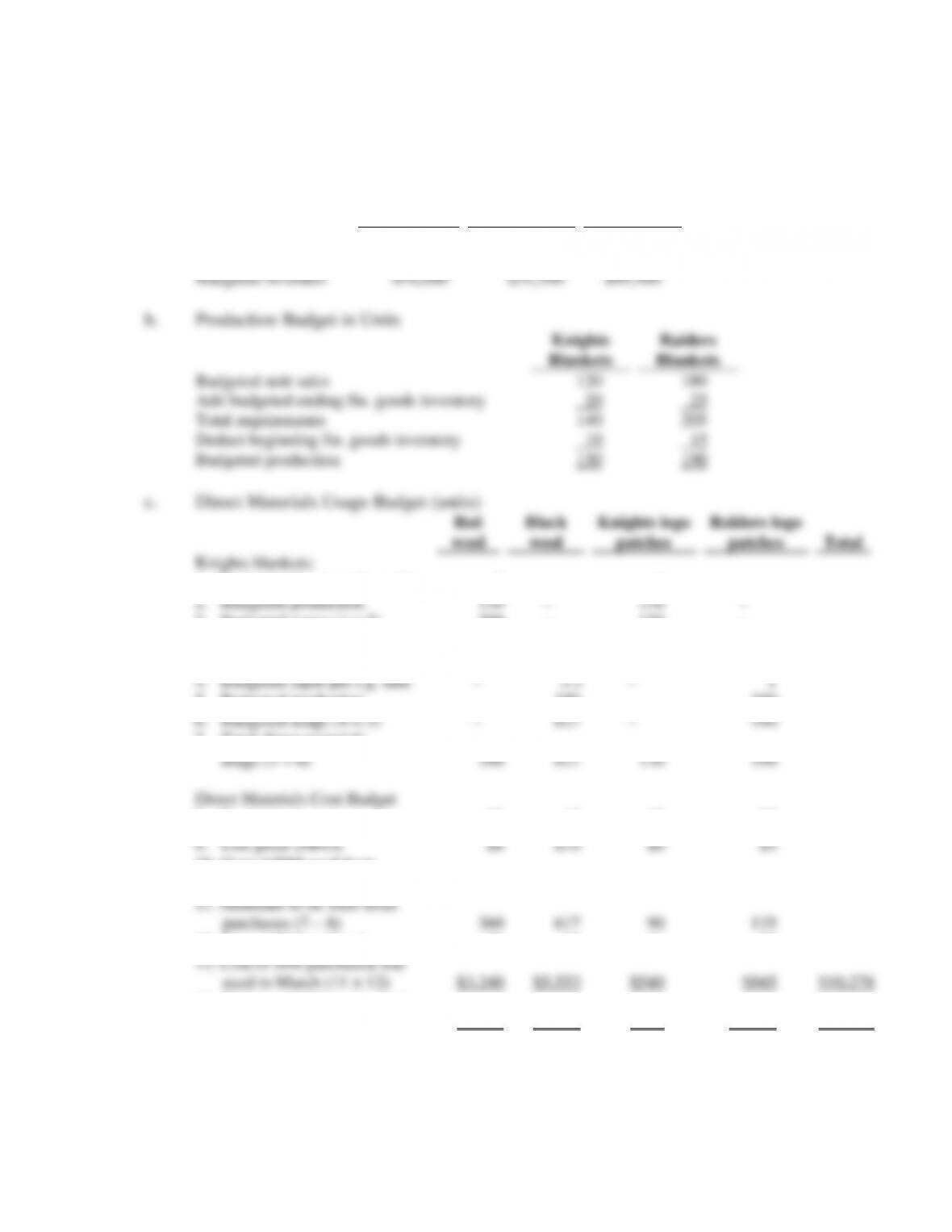

1a. Revenues Budget

Knights

Blankets

Raiders

Blankets

Total

Units sold

120

180

Selling price

$150

$175

Budgeted revenues

$18,000

$31,500

$49,500

Budgeted unit sales

Add budgeted ending fin. goods inventory

Total requirements

Deduct beginning fin. goods inventory

Budgeted production

Knights blankets:

1. Budgeted input per f.g. unit

1

2. Budgeted production

130

3. Budgeted usage (1 × 2)

390

Raiders blankets:

4. Budgeted input per f.g. unit

1

5. Budgeted production

6. Budgeted usage (4 × 5)

7. Total direct materials

usage (3 + 6)

390

Direct Materials Cost Budget

8. Beginning inventory

10

40

55

9. Unit price (FIFO)

$6

$5

360

90

12. Cost of DM in March

$9

$6

$7

$3,240

$10,278

$3,480

$11,133

Direct Materials Purchases Budget

Red wool

Black

wool

Knights

logos

Raiders

logos

Total

Budgeted usage

(from line 7)

390

627

130

190

Add target ending inventory

20

20

20

20

Total requirements

410

647

150

210

Deduct beginning inventory

30

10

40

55

Total DM purchases

380

637

110

155

Purchase price (March)

$9

$9

$6

$7

______

Total purchases

$3,420

$5,733

$660

$1,085

$10,898

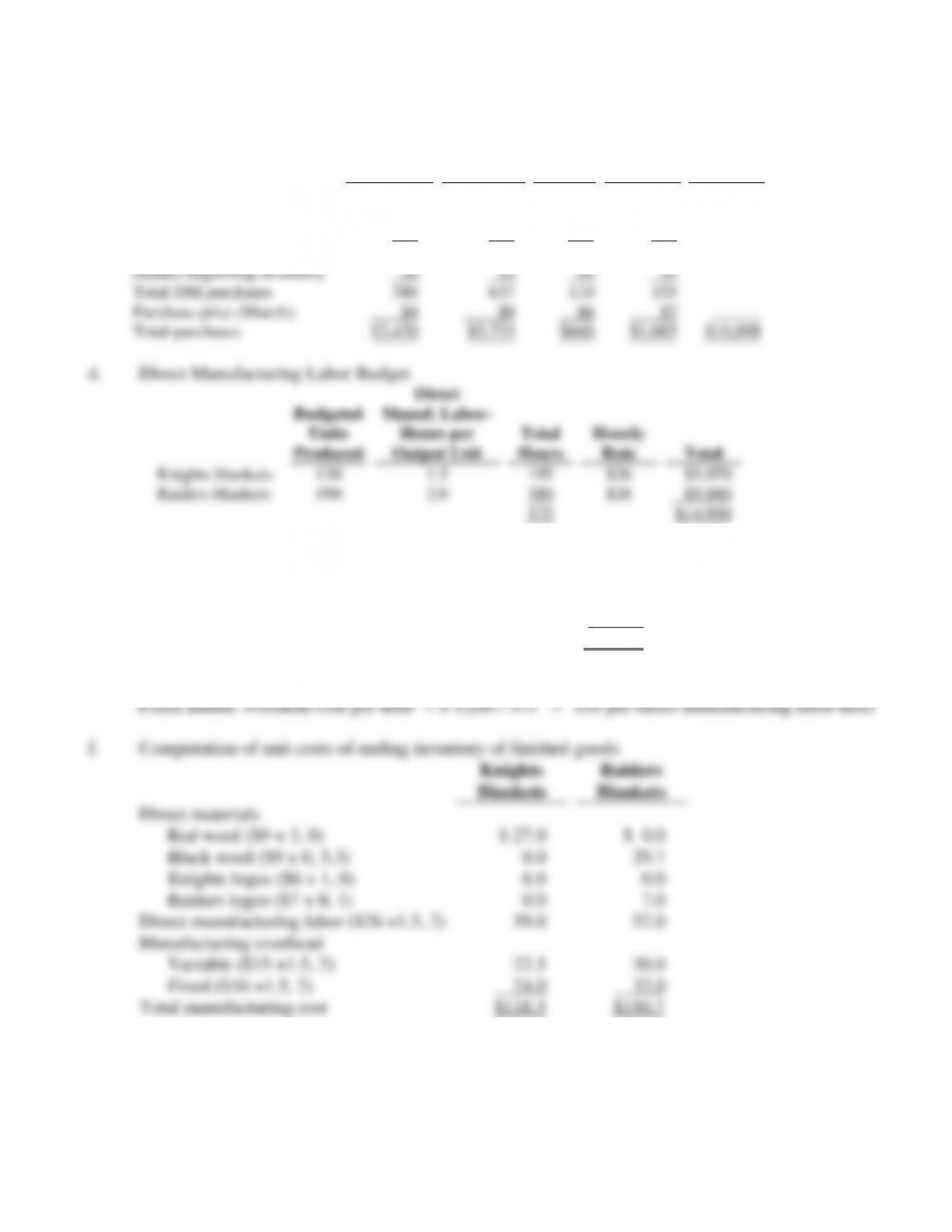

d. Direct Manufacturing Labor Budget

Budgeted

Direct

Manuf. Labor-

Units

Hours per

Total

Hourly

Produced

Output Unit

Hours

Rate

Total

Knights blankets

130

1.5

195

$26

$5,070

Raiders blankets

190

2.0

380

$26

$9,880

575

$14,950

e. Manufacturing Overhead Budget

Variable manufacturing overhead costs (575 × $15) $8,625

Fixed manufacturing overhead costs 9,200

Total manufacturing overhead costs $17,825

Total manuf. overhead cost per hour = $17,825 / 575 = $31 per direct manufacturing labor-hour

6-17

Ending Inventories Budget

Cost per Unit

Units

Total

Direct Materials

Red wool

$9.0

20

$ 180.0

Black wool

9.0

20

180.0

Knight logo

patches

6.0

20

120.0

Raider logo

patches

7.0

20

140.0

620.0

Finished Goods

Knight blankets

118.5

20

2,370.0

Raider blankets

150.7

25

3,767.5

6,137.5

Total

$6,757.5

g. Cost of goods sold budget

Beginning fin. goods inventory, March 1, 2012 ($1,210 + $2,235) $ 3,445.0

Direct materials used (from Dir. materials cost budget) $11,133.0

2. Areas where continuous improvement might be incorporated into the budgeting process:

(a) Direct materials. Either an improvement in usage or price could be budgeted. For

example, the budgeted usage amounts for the fabric could be related to the maximum

improvement (current usage – minimum possible usage) of yards of fabric for either

6-18

6-29 (45 min.) Activity-based budget: kaizen improvements.

1.

Increase in Costs for the Year

Assume DryPool uses New Dye

Units to dye

60,000

Cost differential ($1-$.20) per ounce x 3 ounces

x $2.40

Increase in costs

$144,000

Since the fine is only $102,000, they would be financially better off by not switching.

2. If DryPool switches to the new dye, costs will increase by $144,000.

If DryPool implements kaizen costing, costs will be reduced as follows:

Original monthly costs

Input

Unit cost

Number of units

Total cost

Annual cost

Fabric

$6

6,000*

$36,000

$432,000

Labor

$3

6,000*

$18,000

$216,000

Total

$54,000

$648,000

* (12,000 + 60,000)/12 months = 6,000 units

Monthly decrease in costs

Fabric

Labor cost

Month 1

$36,000

Month 1

$18,000

Month 2

35,640

Month 2

17,820

Month 3

35,284

Month 3

17,642

Month 4

34,931

Month 4

17,466

Month 5

34,581

Month 5

17,291

Month 6

34,235

Month 6

17,118

Month 7

33,893

Month 7

16,947

Month 8

33,554

Month 8

16,778

Month 9

33,218

Month 9

16,610

Month 10

32,886

Month 10

16,444

Month 11

32,557

Month 11

16,280

Month 12

32,231

Month 12

16,117

$409,010

$204,513

TOTAL

$613,523

Diff between costs with and without Kaizen improvements

$34,477

This means costs increase a net ($144,000 – 34,477) = $109,523

Since DryPool would otherwise have to spend $102,000 to pay the fine, their net costs would

only be $7,523 higher than if they did not switch to the new dye or implement kaizen costing.

6-19

3. Reduction in materials can be accomplished by reducing waste and scrap. Reduction in

direct labor can be accomplished by improving the efficiency of operations and decreasing down

6-20

6-30 (30–40 min.) Revenue and production budgets.

This is a routine budgeting problem. The key to its solution is to compute the correct quantities

or purchases =

inventory +

materials used –

1. Scarborough Corporation

Revenue Budget for 2012

2. Scarborough Corporation

Production Budget (in units) for 2012

Thingone

Thingtwo

Budgeted sales in units

60,000

40,000

Add target finished goods inventories,

December 31, 2012

25,000

9,000

Total requirements

85,000

49,000

Deduct finished goods inventories,

January 1, 2012

20,000

8,000

Units to be produced

65,000

41,000

3. Scarborough Corporation

Direct Materials Purchases Budget (in quantities) for 2012

Direct Materials

A

B

C

Direct materials to be used in production

• Thingone (budgeted production of 65,000

units times 4 lbs. of A, 2 lbs. of B)

260,000

130,000

—

• Thingtwo (budgeted production of 41,000

units times 5 lbs. of A, 3 lbs. of B, 1 lb. of C)

205,000

123,000

41,000

Total

465,000

253,000

41,000

Add target ending inventories, December 31, 2012

36,000

32,000

7,000

Total requirements in units

501,000

285,000

48,000

Deduct beginning inventories, January 1, 2012

32,000

29,000

6,000

Direct materials to be purchased (units)

469,000

256,000

42,000