21-31

1. Net Present Value of project:

Period

0

1 – 10

Cash inflows

$28,000

Cash outflows

$(62,000)

(18,000)

Net cash flows

$(62,000)

$ 10,000

Annual net cash inflows

$ 10,000

Present value factor for annuity, 10 periods, 8%

× 6.71

Present value of net cash inflows

$67,100

Initial investment

(62,000)

Net present value

$ 5,100

For a $62,000 initial outflow, the project now generates $10,000 in cash flows at the end of

each of years one through ten.

Using either a calculator or Excel, the internal rate of return for this stream of cash flows is

found to be 9.79%.

2. If revenues are 10% higher, the new Net Present Value will be:

Period

0

1 – 10

Cash inflows

$30,800

Cash outflows

$(62,000)

(18,000)

Net cash inflows

$(62,000)

$12,800

21-32

If revenues are 10% lower, the new net present value will be:

Period

0

1 – 10

Cash inflows

$25,200

Cash outflows

$(62,000)

(18,000)

Net cash inflows

$(62,000)

$ 7,200

Annual net cash inflows

$ 7,200

Present value factor for annuity, 10 periods, 6%

x 6.71

Present value of net cash inflows

$ 48,312

Initial investment

(62,000)

Net present value

$ (13,688)

For a $62,000 initial outflow, the project now generates $7,200 in cash flows at the end of each

of years one through ten.

Using either a calculator or Excel, the internal rate of return for this stream of cash flows is

found to be 2.82%.

3. If both revenues and costs are higher, the new Net Present Value will be:

Period

0

1 – 10

Cash inflows

$30,800

Cash outflows

$(62,000)

(19,260)

Net cash inflows

$(62,000)

$11,540

Annual net cash inflows

Present value factor for annuity, 10 periods, 6%

Present value of net cash inflows

Initial investment

Net present value

21-33

If both revenues and costs are lower, the new Net Present Value will be:

Period

0

1 – 10

Cash inflows

$25,200

Cash outflows

$(62,000)

(16,200)

Net cash inflows

$(62,000)

$ 9,000

4. To find the NPV with a different rate of return, use the same cash flows but with a different

discount rate, this time for ten periods at 10%.

Annual net cash inflows

$ 10,000

Present value factor for annuity, 10 periods, 10%

× 6.145

Present value of net cash inflows

$61,450

Initial investment

(62,000)

Net present value

$ (550)

5. The sensitivity analysis shows that the return on the project is sensitive to changes in the

projected revenues and costs. With the cost of capital (8%) as the discount rate, the NPV is

positive and the IRR exceeds the required rate of return in most cases. The exceptions occur

Net present value

Payback problem:

1.

Annual revenue

$140,000

Annual costs

Fixed

$96,000

Variable

14,000

110,000

Net annual cash inflow

$ 30,000

Payback period = Investment net cash inflows = $159,000 ÷ $30,000 = 5.30 years

Discounted Payback Period with even cash flows:

ioYear

Cash

Revenues

Fixed

Costs

Variable

Costs

Net

Cash

Inflows

Disc

Factor

(12%)

Discounted

Cash

Savings

Cumulative

Disc. Cash

Savings

Unrecovered

Investment

0

$159,000

1

$140,000

$96,000

$14,000

$30,000

.893

$26,790

$ 26,790

$132,210

2

$140,000

$96,000

$14,000

$30,000

.797

$23,910

$ 50,700

$108,300

3

$140,000

$96,000

$14,000

$30,000

.712

$21,360

$ 72,060

$ 86,940

4

$140,000

$96,000

$14,000

$30,000

.636

$19,080

$ 91,140

$ 67,860

5

$140,000

$96,000

$14,000

$30,000

.567

$17,010

$108,150

$ 50,850

6

$140,000

$96,000

$14,000

$30,000

.507

$15,210

$123,360

$ 35,640

7

$140,000

$96,000

$14,000

$30,000

.452

$13,560

$136,920

$ 22,080

8

$140,000

$96,000

$14,000

$30,000

.404

$12,120

$149,040

$ 9,960

9

$140,000

$96,000

$14,000

$30,000

.361

$10,830

$159,870

21-35

2.

Year

Revenue

(1)

Cash Fixed

Costs

(2)

Cash

Variable Costs

(3)

Net Cash Inflows

(4) = (1) − (2) − (3)

Cumulative

Amounts

1

$ 90,000

$ 96,000

$ 9,000

$(15,000)

$(15,000)

2

115,000

96,000

11,500

7,500

(7,500)

3

130,000

96,000

13,000

21,000

13,500

4

155,000

96,000

15,500

43,500

57,000

5

170,000

96,000

17,000

57,000

114,000

6

180,000

96,000

18,000

66,000

180,000

7

140,000

96,000

14,000

30,000

210,000

8

125,000

96,000

12,500

16,500

226,500

9

110,000

96,000

11,000

3,000

229,500

The cumulative amount exceeds the initial $159,000 investment for the first time at the end of year

6. So, payback happens in year 6.

Using linear interpolation, a more precise measure is that payback happens at:

5 years +

$159,000 – $114,000 5.68 years.

$66,000 =

21-36

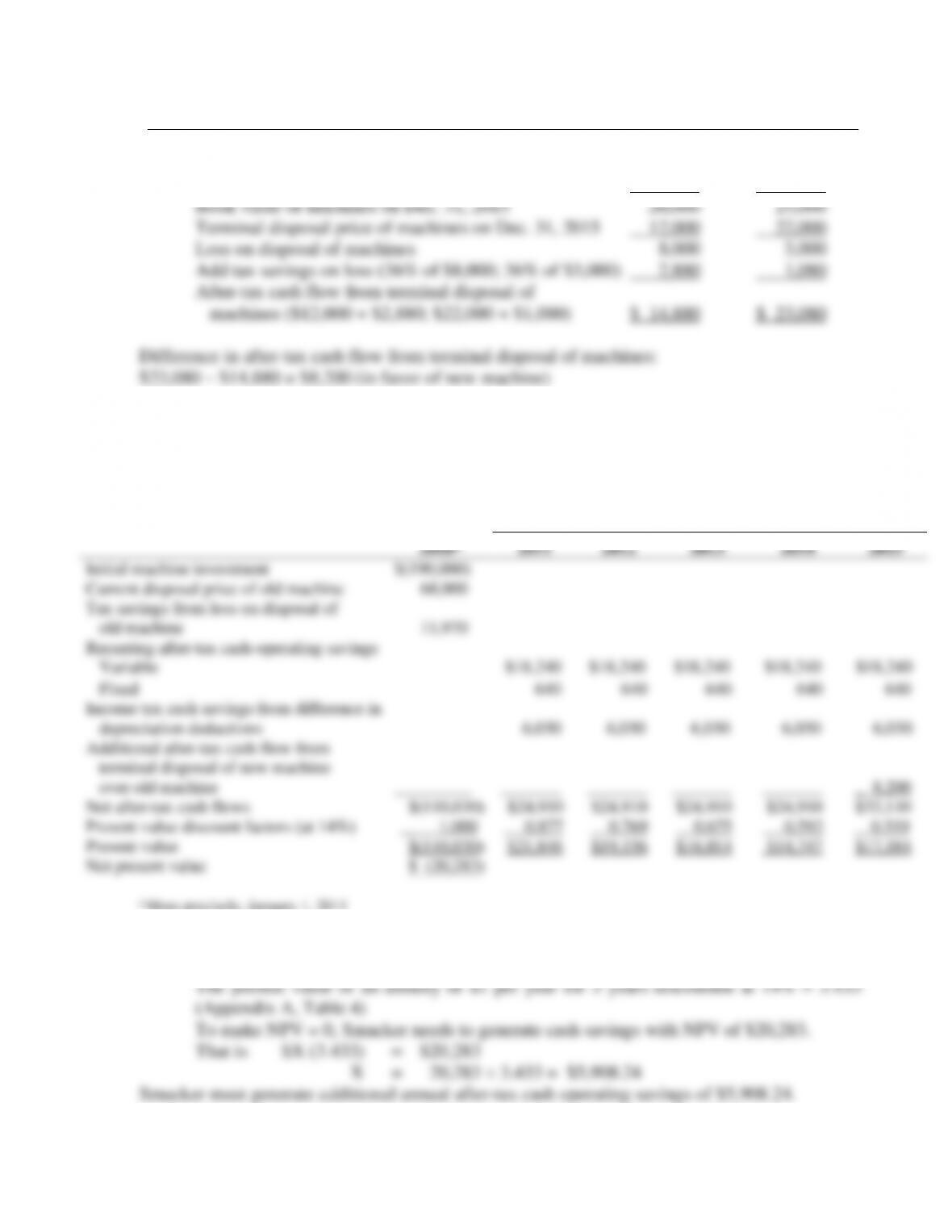

21-32 (40 min.) Replacement of a machine, income taxes, sensitivity.

1a. Original cost of old machine: $150,000

Depreciation taken during the first 3 years

{[($150,000 – $20,000) ÷ 8] 3} 48,750

Book value 101,250

21-37

1d.

Old Machine

New Machine

Original cost $150,000 $190,000

Total depreciation 130,000 165,000

2. The Smacker Company should retain the old equipment because the net present value of

the incremental cash flows from the new machine is negative. The computations, using the

results of requirement 1, are presented below. In this format the present value factors appear at

the bottom. All cash flows, year by year, are then converted into present values.

After-Tax Cash Flows

2010a

2011

2012

2013

2014

2015

Initial machine investment

$(190,000)

Current disposal price of old machine

68,000

Tax savings from loss on disposal of

old machine

11,970

Recurring after-tax cash-operating savings

Variable

$18,240

$18,240

$18,240

$18,240

$18,240

Fixed

640

640

640

640

640

Income tax cash savings from difference in

depreciation deductions

6,030

6,030

6,030

6,030

6,030

Additional after-tax cash flow from

terminal disposal of new machine

over old machine

_________

_______

_______

_______

_______

_ 8,200

Net after-tax cash flows

$(110,030)

$24,910

$24,910

$24,910

$24,910

$33,110

Present value discount factors (at 14%)

_ 1.000

0.877

0.769

0.675

0.592

0.519

Present value

$(110,030)

$21,846

$19,156

$16,814

$14,747

$17,184

Net present value

$ (20,283)

a More precisely, January 1, 2011

3. Let $X be the additional recurring after-tax cash operating savings required each year to

make NPV = $0.

21-33 (30–35 min.) NPV and AARR, goal-congruence issues.

1.

Annual cash flow from operations

$125,000

Income tax payments (35%)

43,750

After-tax cash flow from operations (excl. deprn.)

$ 81,250

Depreciation: $420,000 ÷ 7 = $60,000 per year

21-39

21-34 (35 min.) Recognizing cash flows for capital investment projects.

1. Partitioning relevant cash flows into categories:

(1) Net initial investment cash flows:

– The $98,000 cost of the new Flab-Buster 3000

– The disposal value of the old machine, $5,000, is a cash inflow

– The book value of the old machine $4,000 ($50,000 − $46,000), relative to the disposal

21-40

2. Net present value of the investment:

Net initial investment

Initial investment in Flab-Buster 3000

$(98,000)

Current disposal value of Fit-O-Matic

5,000

Tax on gain on sale of Fit-O-Matic, 40% × $1,000

(400)

Net initial investment

$(93,400)

Annual after-tax cash flow from operations (excl. deprn. effects)

After-tax savings in utilities costs, $4,320 × (1−0.40)

$ 2,592

After-tax savings in maintenance costs, $5,000 × (1−0.40)

3,000

Annual after-tax cash flow from operations

$ 5,592

Income-tax cash savings from annual additional depreciation

deductions ($8,800 − $400) × 40%

$ 3,360

After-tax cash flow from terminal disposal of machines

$ 10,000

These four amounts can be combined to determine the NPV at an 8% discount rate.

Present value of net initial investment, $(93,400) × 1.000

$(93,400)

Present value of 10-year annuity of annual after-tax cash flow

from operations (excl. deprcn. effects), $5,592 × 6.710

37,522

Present value of 10-year annuity of income-tax cash savings from

annual depreciation deductions, $3,360 × 6.710

22,546

Present value of after-tax cash flow from terminal disposal of

machines, $10,000 × 0.463

4,630

Net present value

$(28,702)

At the required rate of return of 8%, the net present value of the investment in the Flab-Buster

3000 is substantially negative. Ludmilla should therefore not make the investment.